dima_zel

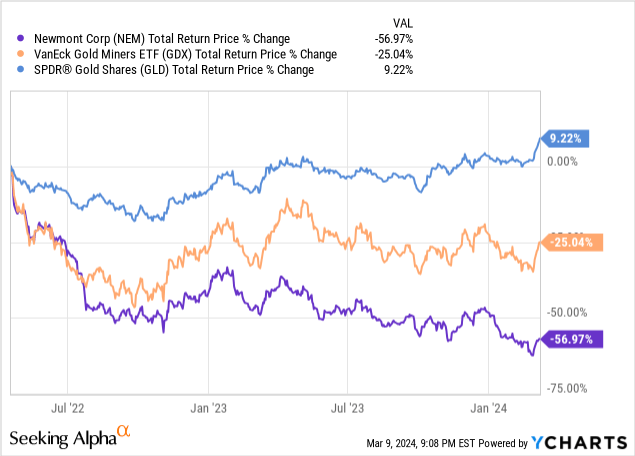

Newmont Corporation (NYSE:NEM) has been taken to the cleaners in recent years, massively underperforming Gold (GLD) and the broader gold mining index (GDX) since NEM stock peaked in April 2022:

However, its forward outlook looks very bright right now and its CEO Tom Palmer recently signaled extremely bullish sentiment on NEM stock, stating:

It’s a once-in-a-generation buy for anyone who’s thinking of putting a few dollars into gold equity…Newmont stock is sitting at a very good buying price… and as we deliver on our commitments, you can enjoy the ride up with us.

In this article, we will share six reasons why we agree with NEM’s CEO that the stock is an extremely attractive buy right now.

#1. The Balance Sheet Is Strong And Getting Stronger

NEM’s balance sheet is currently in solid shape, with $6.1 billion in total liquidity, a business that is generating free cash flow, and very strong credit ratings (BBB+ from S&P and A- from Fitch). Moreover, its balance sheet is set to improve even further in the coming two years as it is selling six of its assets in order to generate $2 billion in proceeds, about half of which will be used to reduce net debt and improve its liquidity to $7 billion, including $3 billion in total cash on hand. This will put the company on very strong financial footing and give it the flexibility it needs to buy back stock aggressively and make other investments opportunistically.

#2. Massive Synergies Projected In The Near Future

NEM also expects to generate significant synergies in the near future, projecting a total of $1 billion through ~$500 million in annual synergies from its Newcrest acquisition and an additional ~$500 million in annual synergies from productivity improvements. Given that they are projected to generate between $6.5 billion and $8.5 billion in EBITDA moving forward, these synergies will be a very meaningful improvement to the company’s bottom line.

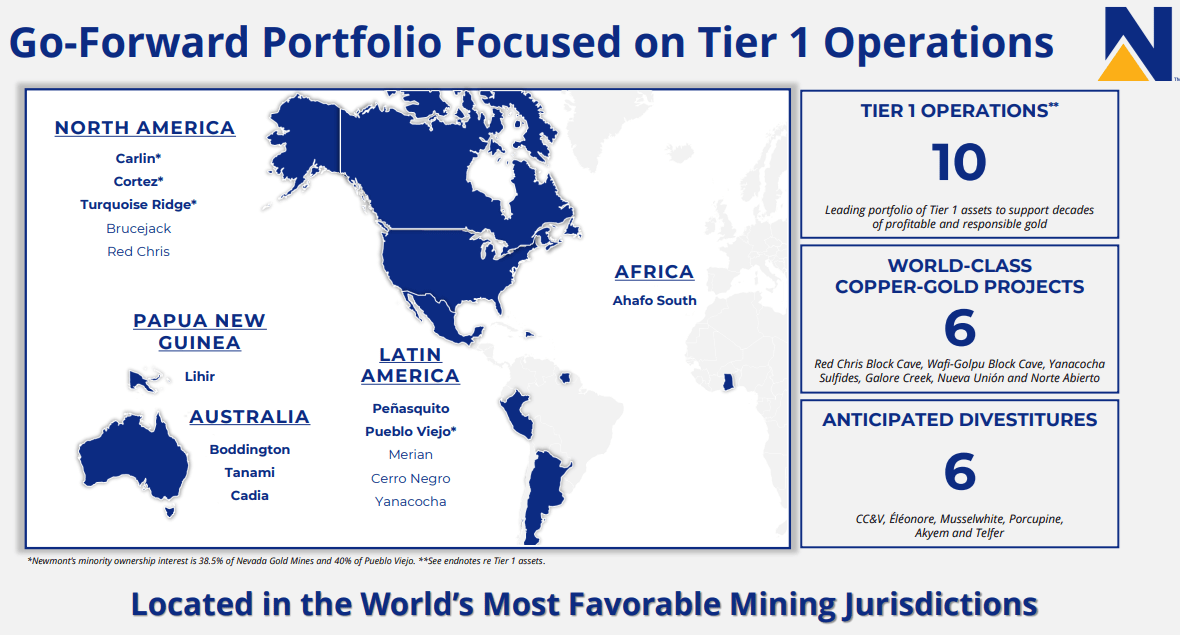

#3. They Have The Most Impressive Gold Mining Portfolio In The World

With their planned sale of six tier-two assets in the near future, NEM’s pro-forma portfolio will consist of 10 tier-one gold mines along with six high-quality copper mines.

NEM Portfolio (Investor Presentation)

Moreover, these mines will be almost entirely concentrated in low-risk mining jurisdictions with a mere 6% of its gold reserves and none of its copper reserves being located in Africa. Of equal importance, nearly two-thirds of its gold and copper reserves will be located in North America, Australia, or Papua New Guinea. When combined with its scale and balance sheet strength, NEM will have one of the lowest risk profiles in the mining industry.

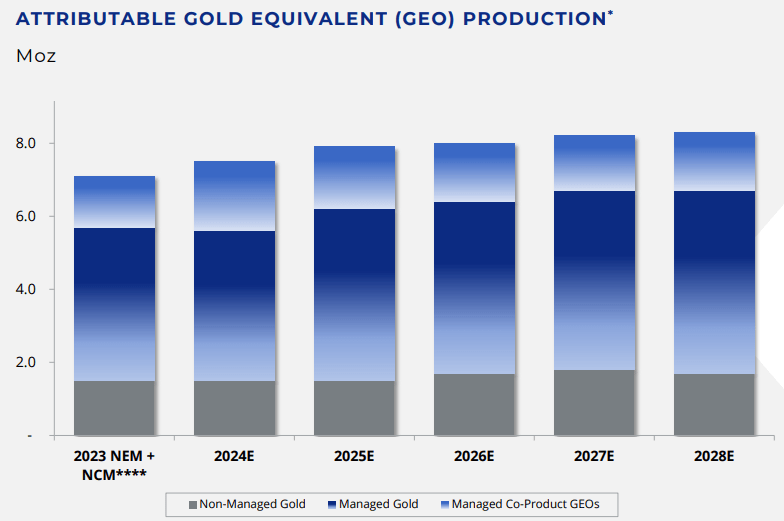

#4. Operational And Free Cash Flow Improvements Coming Up

On top of its enhanced risk profile, operating efficiency and productivity improvements appear highly likely in NEM’s future, as its Gold Equivalent Ounce production in its tier-one portfolio is expected to increase meaningfully in the coming years:

NEM Production Profile (Investor Presentation)

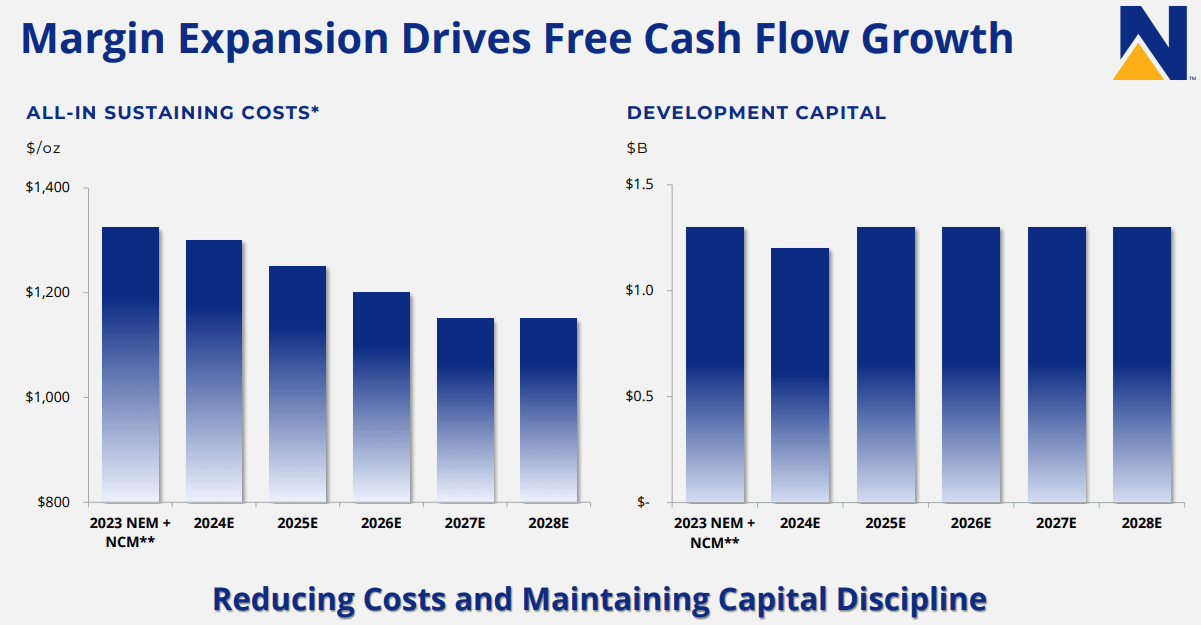

Moreover, due to its anticipated synergies, improved asset quality, and other investments in efficiency improvements, NEM’s all-in sustaining costs are expected to fall meaningfully while its development capital spending should remain quite stable, likely leading to expanding margins for the company on a gold price neutral basis:

NEM Efficiency Improvements (Investor Presentation)

#5. Very Bullish Outlook For Gold And Copper

That being said, we expect gold and copper prices to soar in the coming years. As we detailed in a recent article, gold will likely continue its recent strong performance due to:

- The Federal Reserve ending its rate-hiking cycle and beginning to cut rates

- Continued strong central bank buying of gold

- Soaring geopolitical risks and tensions

- A likely weakening of the economy

- A reversion to the mean of its valuation relative to the stock market

- The continued decline of the U.S. Dollar

Copper, meanwhile, should perform well because:

- Demand is soaring due to the green energy transition

- The value of the U.S. Dollar is expected to continue to decline

- Production is suffering from mining disruptions and is unlikely to be able to meet demand for the foreseeable future

#6. NEM Stock Is Very Undervalued And Is Set To Buy Back Stock Aggressively

Last, but not least, NEM stock looks very undervalued right now, as its CEO recently emphasized. With a $1 billion stock buyback recently announced, it appears that management is ready to put its money where its mouth is.

Moreover, the stock is trading in-line with its NAV right now despite historically trading at a 30% premium to its NAV, implying ~30% near-term upside for the stock. If gold and copper prices continue to rise, however, it will enjoy even further upside.

NEM Stock Risks

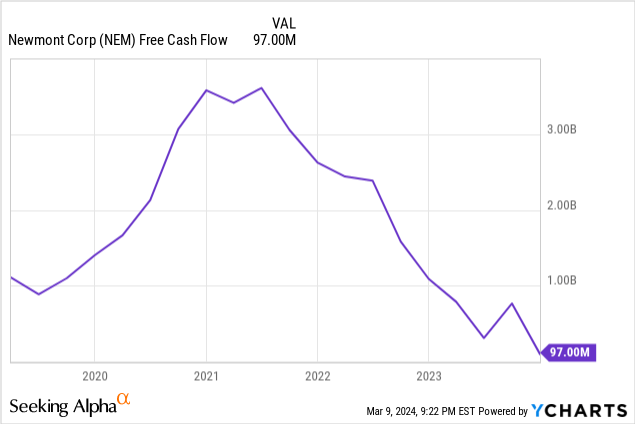

That being said, no stock is risk-free and NEM certainly has a past that is likely leaving many investors in “show me” mode. In addition to its steep stock price underperformance, NEM’s management recently cut its dividend, likely destroyed per share intrinsic value through the Newcrest acquisition, and generated shockingly little free cash flow last year relative to its total production capacity.

Moreover, it is having to digest a major acquisition and also faces some execution risk as it seeks to sell six tier two assets and get decent value for them. As gold analyst John Ing pointed out:

Sometimes with these acquisitions, you buy other people’s problems…I just wonder whether this is going to work out longer term…When you get to a certain size, they’ll have something like 21 mines in about 10 jurisdictions, and that’s a lot to manage.

Investor Takeaway

NEM indeed looks like a generational buying opportunity right now and – while the company will need to prove to the market that it can handle its new and improved portfolio, get attractive pricing for its non-core assets that it is selling, and effectively harvest its projected synergies – its strong balance sheet, world-class portfolio of assets, improving operational and production profile, and bullish outlook for gold and copper prices combine with its significantly discounted stock price to make it appear poised to deliver substantial total return outperformance in the years to come. As a result, it is one of my largest positions at the moment and I rate it a Strong Buy.

Q2 2024 Earnings Call Transcript")