da-kuk

When it comes to individual stocks, a lot can change in a very short window of time. Sometimes, this can be for the better. Other times, it can be for the worst. Back in late March of 2023, I wrote a very bullish article about New York Community Bancorp (NYSE:NYCB), detailing how the company’s ability to absorb certain assets from the now defunct Signature Bank represented a ‘deal of a lifetime’ for the firm’s shareholders. I ended up rating the company a ‘strong buy’ as a result. Up through January 30th of this year, things are going well. No, the stock was not outperforming the broader market like I would have anticipated. But shares did see upside, including dividends, of 18.5%. For less than a year, that’s a solid return.

In less than two days, the picture flipped on its head entirely. Shares plummeted and are now down 34.5% since the aforementioned article. This was caused by a couple of factors. For starters, management cut the common distribution from $0.17 per share each quarter to only $0.05 per share each quarter. And second, the firm reported a surprise and that loss because of a reserve build associated with certain assets. This combination of factors has stoked fears amongst the investment community that round two of the banking crisis might begin again. Digging in, I will admit that some of the data is less than ideal at this time. A continued drop in deposits, combined with high amounts of debt, don’t paint the best picture. Clearly, the company is not in the same shape that I would have hoped. But this does not mean that there does not exist an interesting opportunity. For those who don’t mind taking some risk, there could be some rather meaningful upside to capture. Because of this, for those who don’t mind said risk, I believe that a ‘buy’ rating is appropriate at this time.

Some painful developments

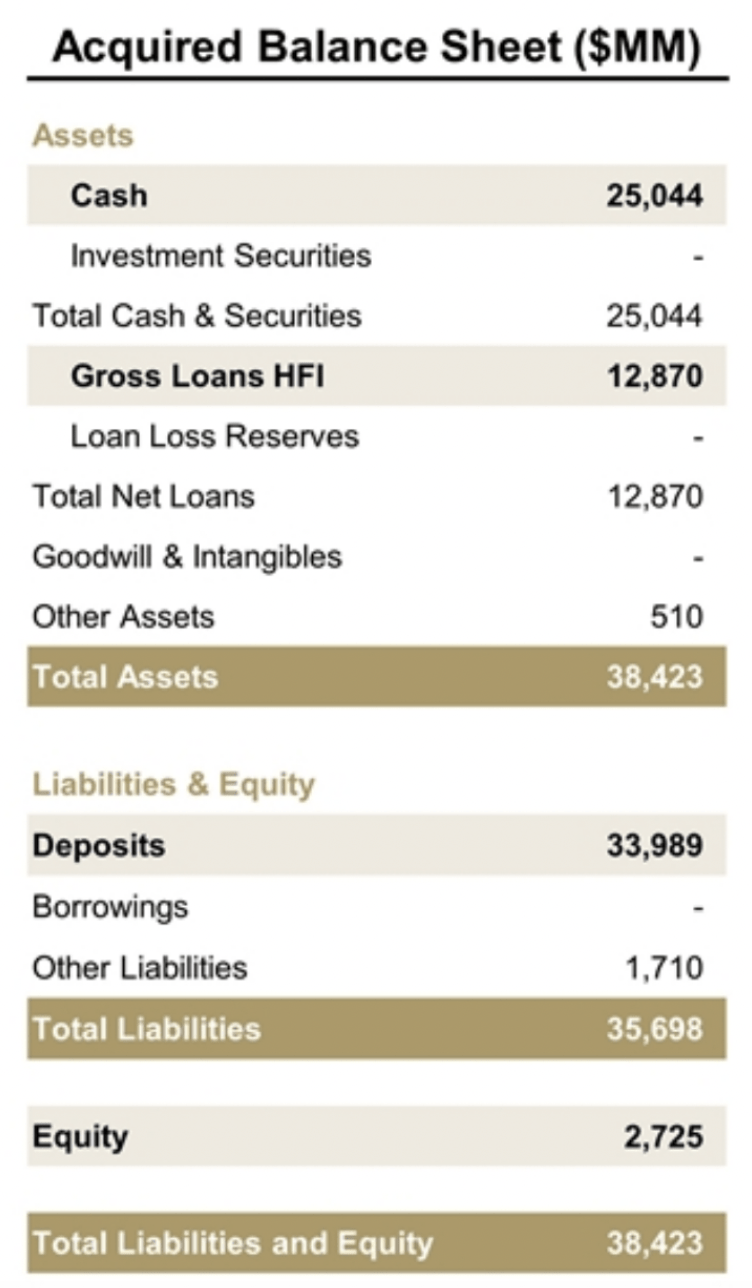

Back when Signature Bank was collapsing in 2023, one company that stepped up in an effort to add stability to the sector while simultaneously attempting to create significant value for shareholders was New York Community Bancorp. The deal that was hashed out with regulators resulted in New York Community Bancorp assuming about $25.04 billion of cash and securities, as well as $12.87 billion of gross loans, and $510 million of other assets, that were previously owned by Signature Bank. At the same time, they also had to take on $33.99 billion of deposits and $1.71 billion of other liabilities, leaving additional equity for investors of just under $2.73 billion.

NYCB and Author’s Article

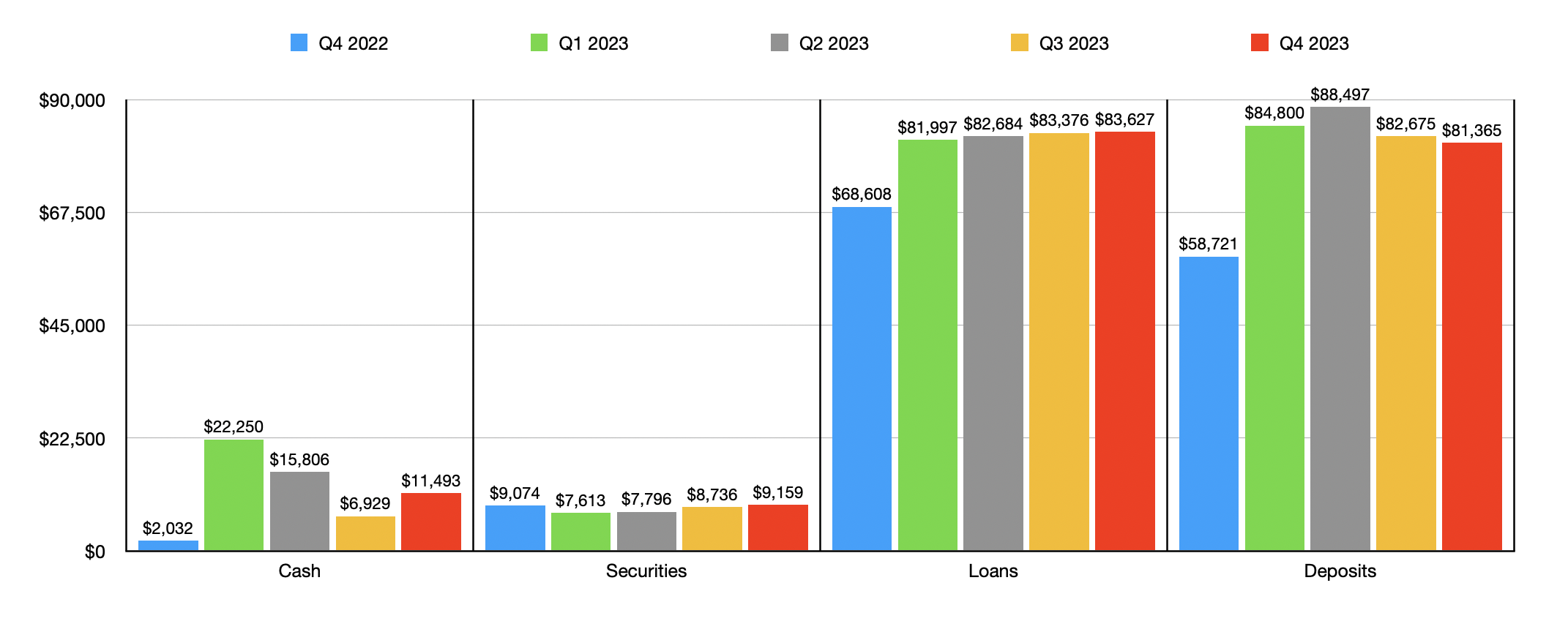

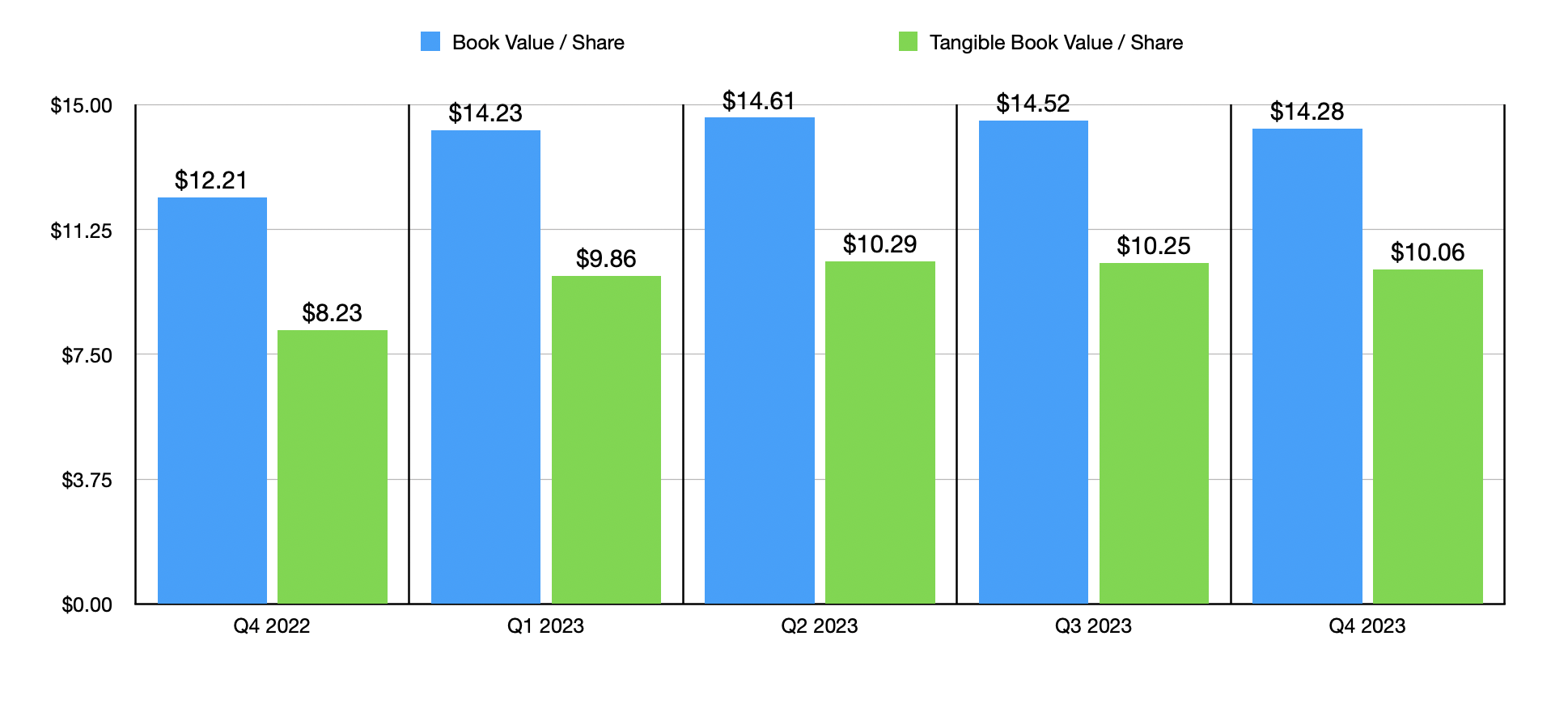

There were some other facets of the deal as well, such as New York Community Bancorp granting to the FDIC certain equity appreciation instruments that could entitle the regulator to up to $300 million that would be payable in company stock. But regardless of the costs involved, the net benefit at the time was obvious for investors. Since then, things have not gone exactly well. Though it would also be a mistake to say that they went poorly. The most obvious benefit for the company, besides the immediate increase in shareholder equity, a move that took book value per share from $12.21 to $14.23 in the course of a single quarter, was a surge in assets. The value of loans went from $68.61 billion at the end of 2022 to just shy of $82 billion in the first quarter of 2023. Cash jumped to $7.61 billion from $2.03 billion even as debt remained almost unchanged. Only the value of securities took a slight hit, dropping from $9.07 billion to $7.61 billion.

Author – SEC EDGAR Data

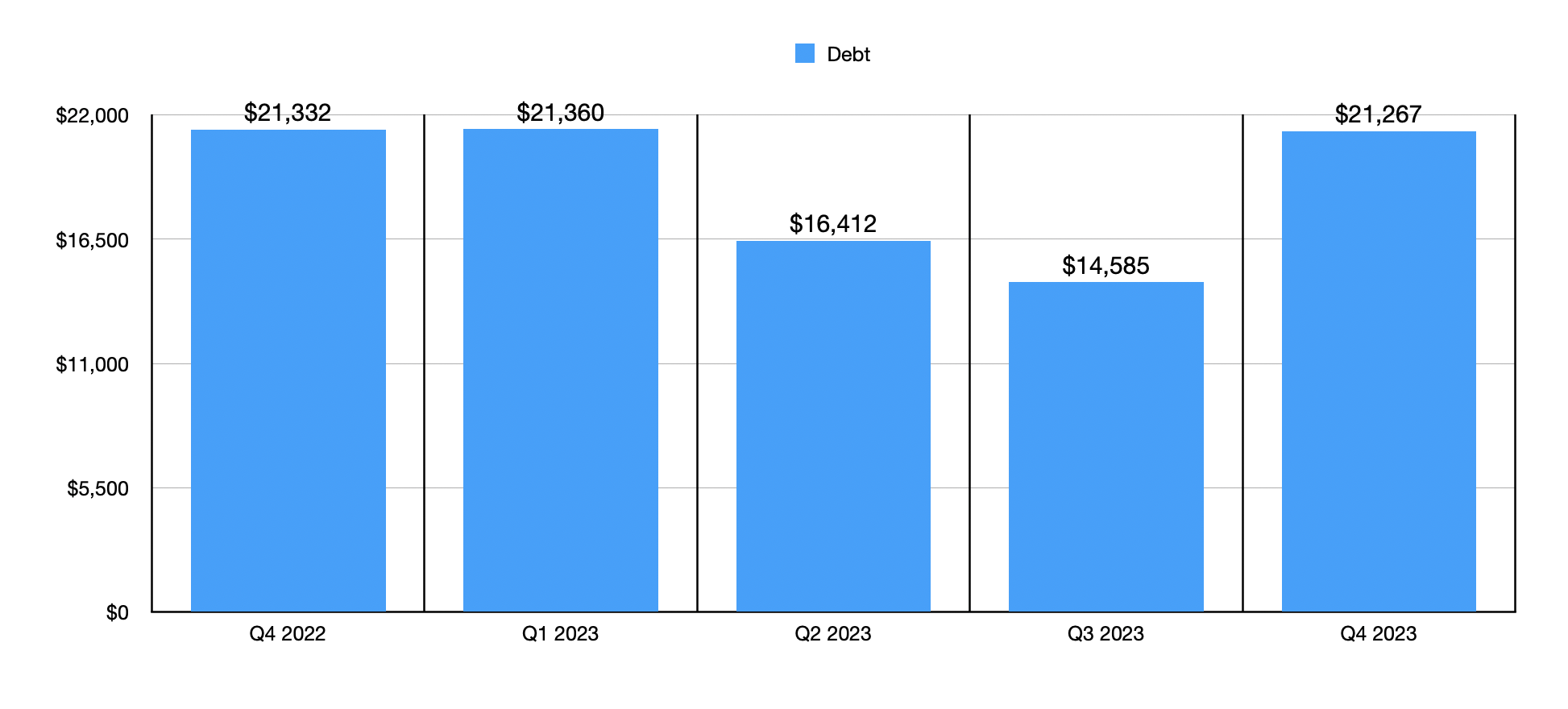

The overall growth in the company’s balance sheet included an increase in liabilities, notably in deposits. They expanded from $58.72 billion to $84.80 billion in the span of a single quarter. But even this wasn’t so bad. I say this because, as of the fourth quarter of 2023, 25% of all deposits on the company’s books are non-interest bearing. Since the end of the first quarter, there has been a lot of volatility in the company’s balance sheet. The value of loans, for instance, has continued to increase, eventually hitting $83.63 billion as of the end of the 2023 fiscal year. Securities rebounded and grew to $9.16 billion. For a time, debt was declining. By the third quarter of the year it had fallen to $14.59 billion compared to the $21.36 billion it was at two quarters earlier. But because of the desire or need to see him financially stable, management hiked up the amount of cash on hand from $6.93 billion in the third quarter of 2023 to $11.49 billion by the end of the fourth quarter. That resulted in debt rising further to $21.27 billion.

Author – SEC EDGAR Data

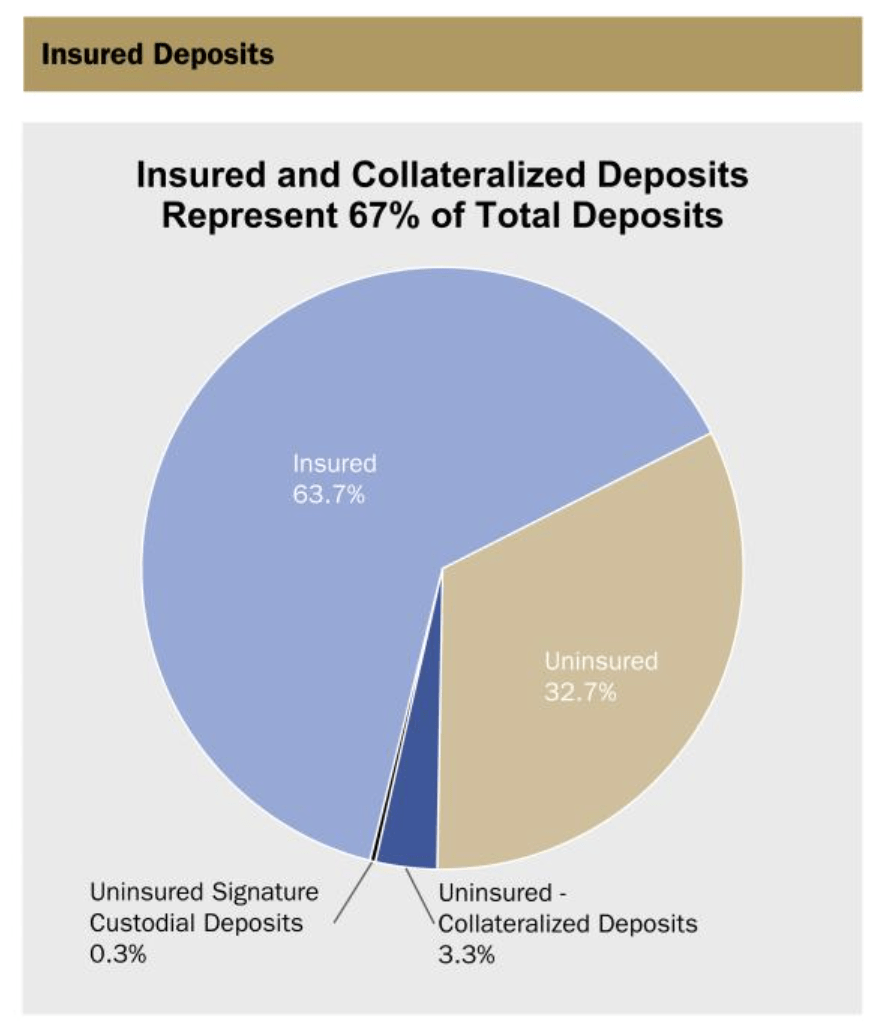

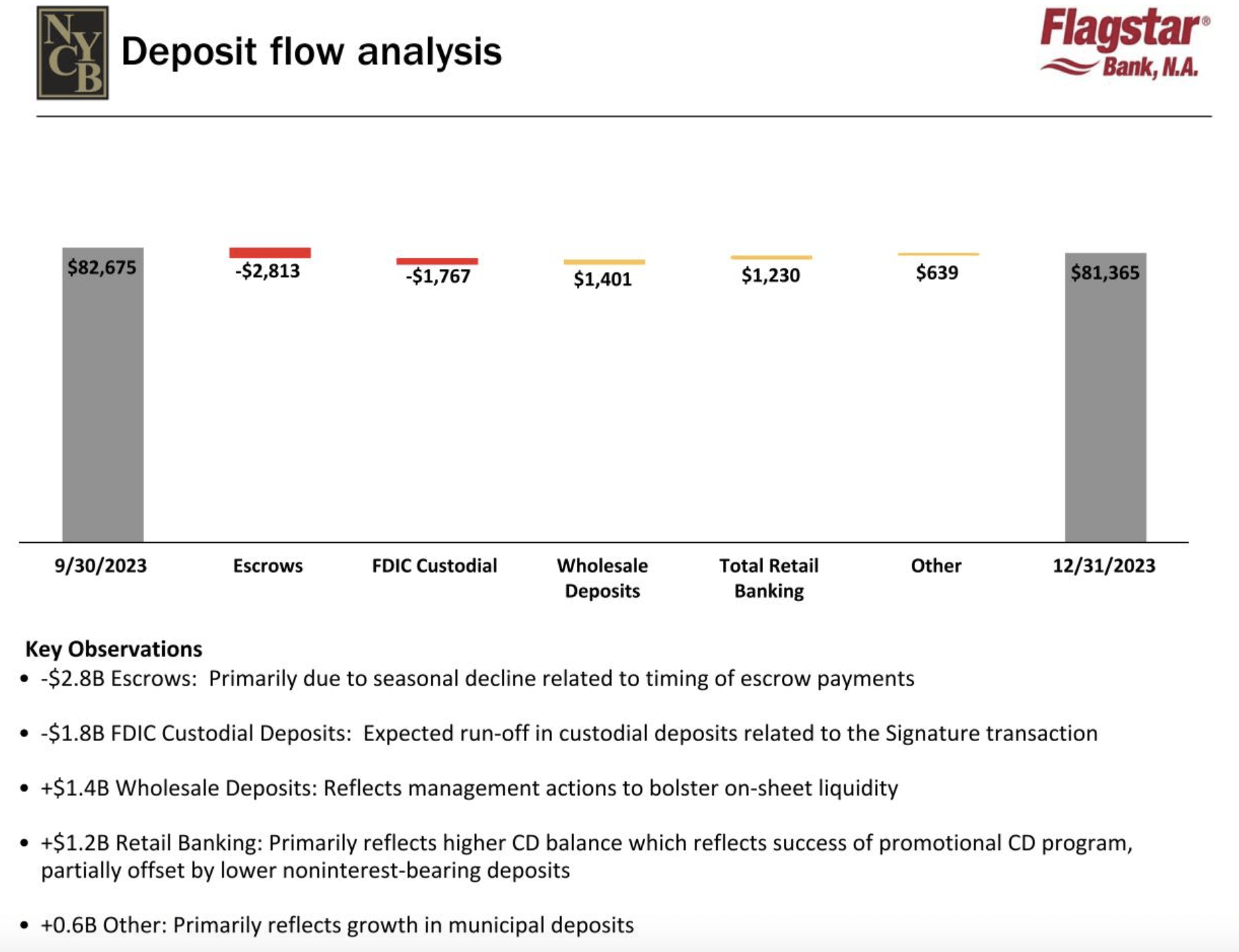

Perhaps the scariest thing for investors during the yeah past several months has been a decline in deposits. After spiking to $88.50 billion in the second quarter of 2023, they ended up dropping to $82.68 billion by the end of the third quarter. Fast forward to the final quarter of the year, and we end up with a reading of $81.36 billion. That’s a decline from the previous quarter of $1.31 billion. The good news is that this drop seems to have been driven by a decline in uninsured deposits. These went from around 38% at the end of the third quarter to 32.7% by the end of the fourth quarter.

New York Community Bancorp

Of course, any discussion regarding deposits requires some additional details. Although deposit declines are unfavorable to see, management attributed a $2.81 billion reduction to mostly seasonal declines associated with the timing of escrow payments. Beyond this, the only pain involved $1.77 billion of a reduction associated with custodial accounts involving the Signature Bank transaction. If we strip that alone out of the equation, deposits would have actually risen by $457 million. This shows that the core institution is relatively stable.

New York Community Bancorp

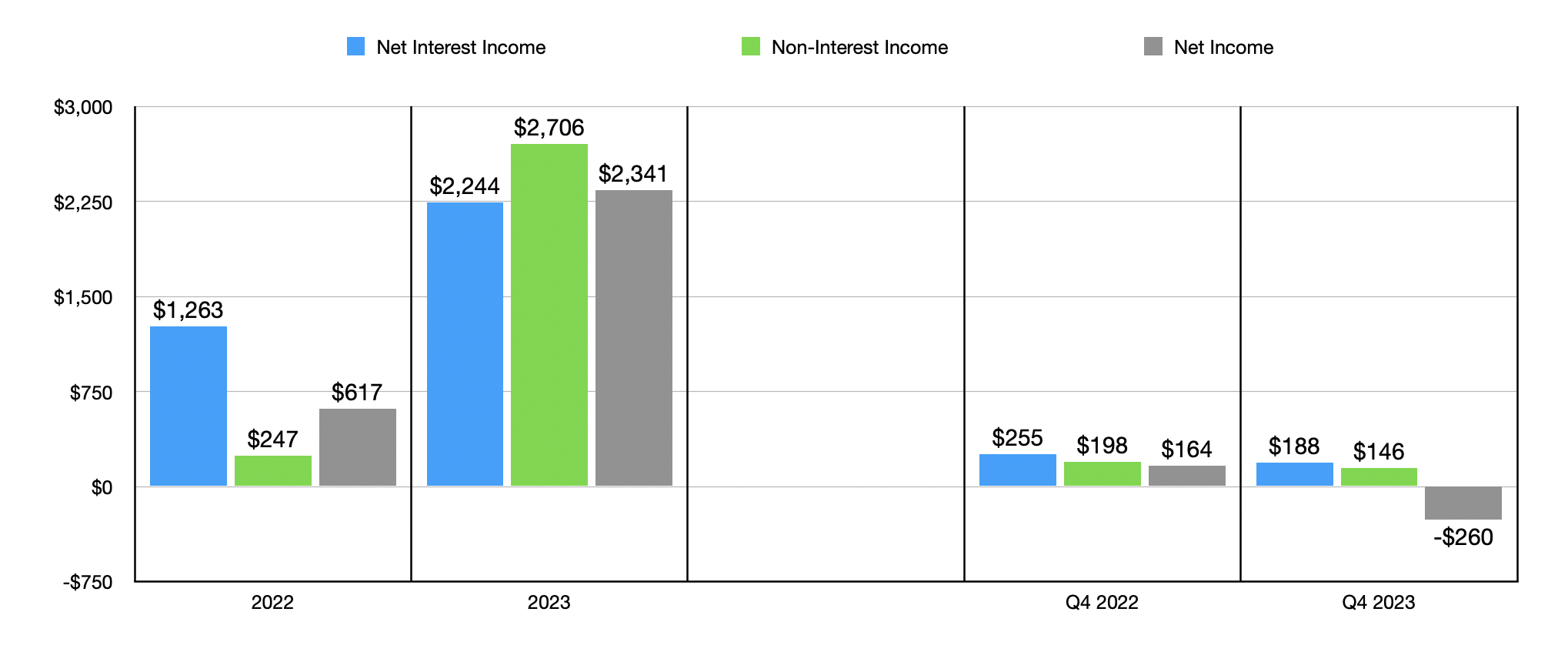

Many investors may wonder why a bank would take such a big leap in order to absorb assets and liabilities from a troubled institution. The answer is because the upside can be significant. To see what I mean, we need only look at the chart below, which shows net interest income, non-interest income, and net profits, not only for the 2022 and 2023 fiscal years, but also for the final quarter of each of those respective fiscal years. 2023 was substantially better than 2022. A larger balance sheet, combined with an increase in the company’s net interest margin from 2.35% to 2.99%, allowed revenue and profits to rise materially. Of course, there was another factor at play when we’re talking about the 2023 fiscal year results on their own. A big portion of this upside was driven by $2.15 billion in the form of a bargain purchase gain associated with the transaction. This is basically a gain that has been recognized because of the discount the company got on the assets. By comparison, for 2022, this particular gain was only $159 million and was obviously associated with a different opportunity.

Author – SEC EDGAR Data

Where investors see the pain, however, is not only in the deposit decline, but also in the final quarter results for 2023. Net interest income, non-interest income, and net profits, all took a hit year over year. In particular, the company went from generating a net profit of $164 million in the final quarter of 2022 to generating a net loss of $260 million the same time of 2023. And the largest contributor to this, by far, was a $490 million increase, year over year, associated with a provision for credit losses. This rise, according to management, was driven by multiple factors, most notably higher net charge offs. However, because of uncertainty in the office sector, some undisclosed amount associated with those assets was factored in. This is on top of some repricing risk involving the company’s multifamily portfolio and a rise in classified assets. Two loans were responsible for the better part of $185 million worth of charge offs during this window of time, so management is painting the picture as more or less isolated.

New York Community Bancorp

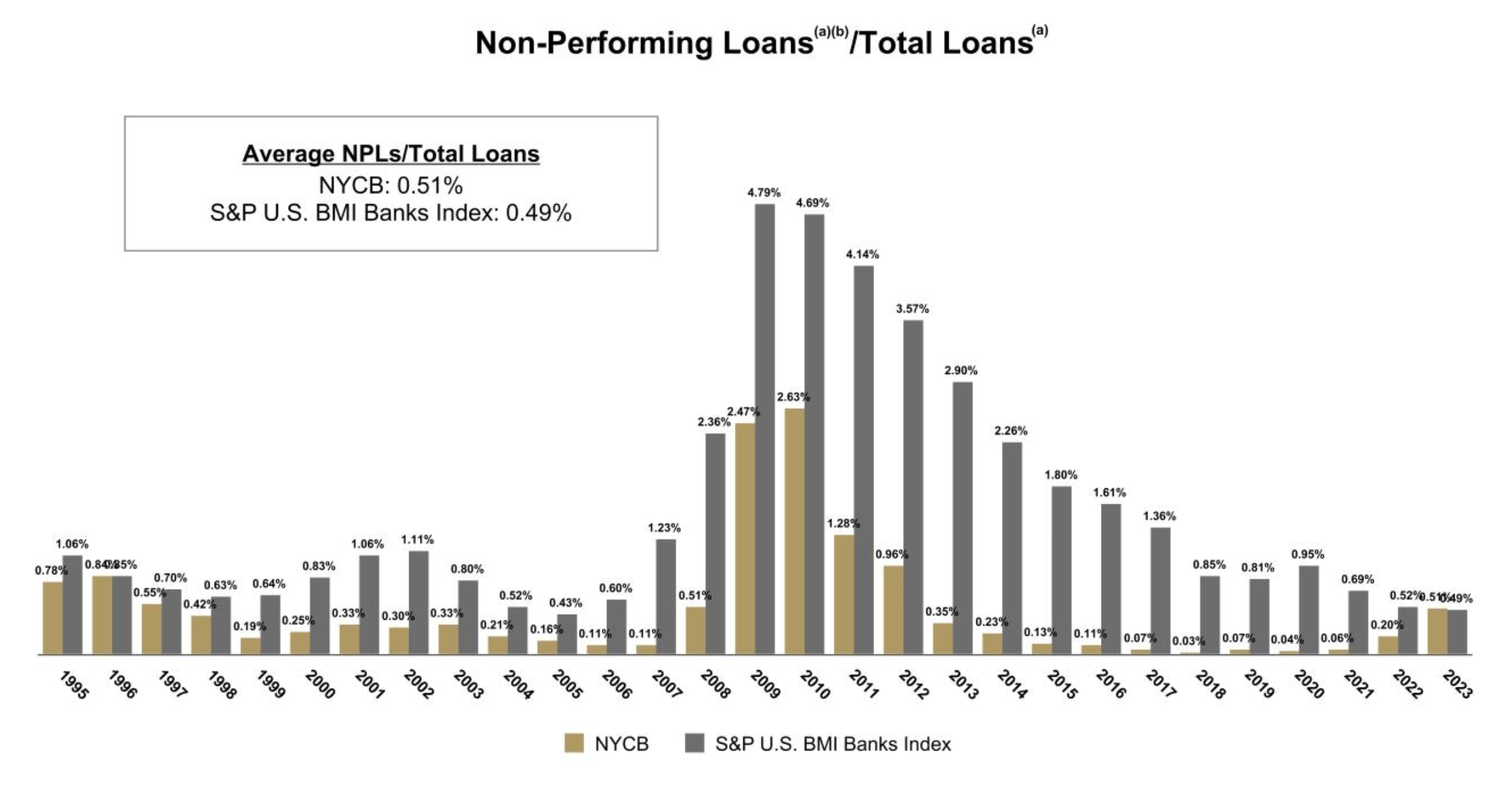

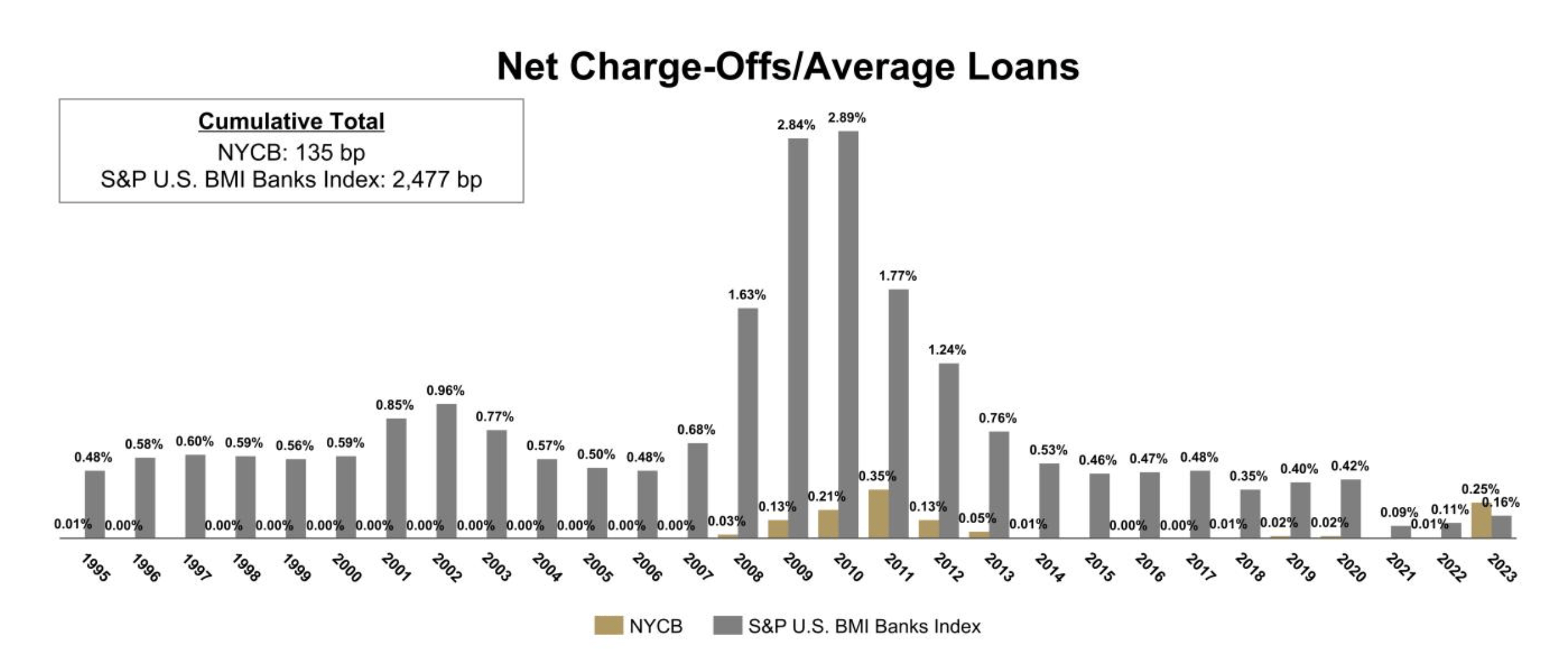

When digging a bit deeper, we do start to see that the company has been experiencing some weakness when it comes to certain assets. As you can see in the chart above, non-performing loans have recently started rising in relation to total loans. They are only just, as of the end of 2023, in line with similar institutions. But the overall trend is not great to see. A similar spike, this one coming in larger than what you would expect from similar firms, can be seen when it comes to net charge-offs as a percent of average loans.

New York Community Bancorp

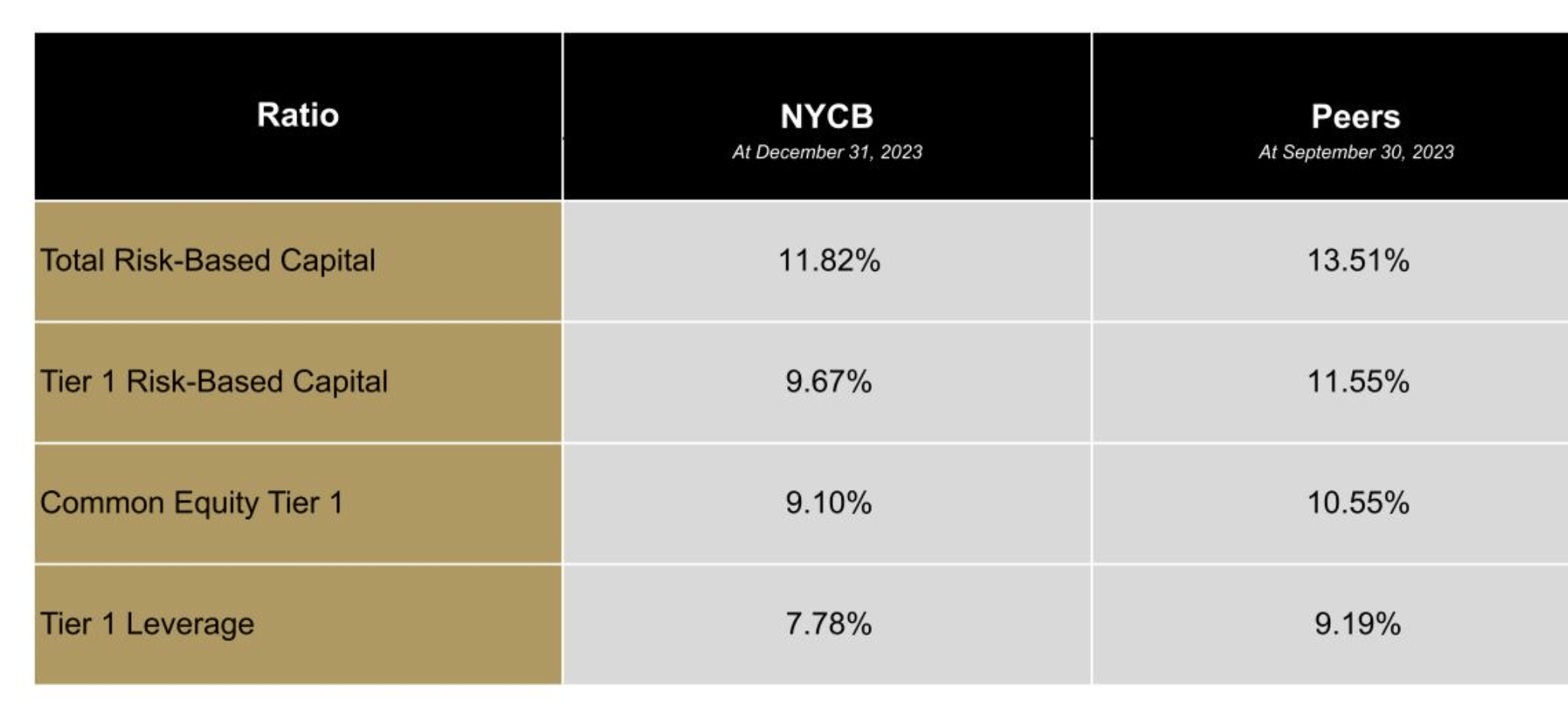

Given this provision the management took, not to mention the distribution cut, I would normally become quite cautious. Banks are relatively fragile institutions they have the potential to collapse rather quickly when sentiment turns against them. Even though this might seem like an antiquated view because of the regulatory frameworks that have been implemented over the past several decades, there are still some weak spots. The biggest is that uninsured deposits exist. As I mentioned already, about 32.7% of all deposits currently controlled by New York Community Bancorp are uninsured. Generally speaking, I like to see this number come in at 30% or lower. So we aren’t terribly far off, but it is still elevated. To put this in perspective, this translates to roughly $26.85 billion in uninsured deposits. When you factor in that the company has cash of $11.49 billion and securities of $9.16 billion, the total amount of liquidity between those two sources is about $20.65 billion. On the other hand, the institution also has debt of $21.27 billion.

New York Community Bancorp

This means that, if there were a run on the institution, there would be a chance that management might have to sell off certain assets, which could create another crisis. I don’t set the rules, but according to the data provided, it is worth noting that the company, from a regulatory capital perspective, is on solid footing. Its Tier 1 risk-based capital is lower than its peer group. However, at 9.67%, it’s still above the 6% threshold required by regulators. There’s also the fact that, at the moment, shares are trading at $5.75, which is well below the $14.28 per share of the book value that the institution has and it’s below the $10.06 per share of tangible book value. This does provide the institution a nice degree of wiggle room as things stand. And in the event that it can survive the current situation, the disparity between price and book value could justify some meaningful upside for shareholders.

Author – SEC EDGAR Data

Takeaway

Based on all the data provided, I must say that I am, in general, cautiously optimistic about New York Community Bancorp. It’s clear that the institution bears a lot more risk than it did earlier in 2023. But with that risk comes significant upside potential if all goes right. I’m not crazy about the firm’s uninsured deposit exposure, even though that is a nice improvement over where things were earlier in the year. The drop in deposits for two consecutive quarters, not to mention the elevated debt, is also discouraging. But for those who don’t mind some risk, it does seem to be a solid prospect. I have yet to make a decision on matters. However, I may very well throw a small speculative bit of money into the ring, either in the form of shares or in the form of call options. And I definitely couldn’t blame other investors for doing likewise.

Q2 2024 Earnings Call Transcript")