Olivier Le Moal

Just over six weeks ago, I wrote on New Gold (NYSE:NGD), noting that while the company was set up to beat 2023 guidance, the stock was well outside of its ideal buy zone at US$1.55 after its ~80% rally. This is because the stock was back to trading at a ~$1.1 billion market cap and just shy of 4x FY2023 cash flow estimates, which was near its historical multiple (10-year average) of ~4.8x P/CF. Since then, the significant beat on its production guidance midpoint hasn’t helped the stock, with NGD suffering a ~25% drawdown which was above that of the Gold Miners Index (GDX). In this update, we’ll dig into the Q4/FY2023 results, the forward outlook, and whether NGD is offering an adequate margin of safety:

Rainy River Operations – Company Website

Q4 & FY2023 Production

New Gold released its Q4 and FY2023 results last month, reporting quarterly production of ~105,000 gold-equivalent ounces [GEOs], a ~7% increase from the year-ago period. This was helped by a much stronger quarter from its New Afton Mine (British Columbia) with production of ~40,800 GEOs (~16,500 ounces of gold and ~12.0 million pounds of copper), a significant improvement from easy year-over-year comparisons due to lower grades and throughput in Q4 2022. Meanwhile, although its Rainy River Mine (Ontario) saw lower production year-over-year, it was up against difficult comparisons with an average milled grade of 1.15 grams per tonne of gold in the year-ago period. Still, the mine put up a solid performance with ~64,300 GEOs produced, ending the year with over 10% growth at Rainy River and coming in right at the top end of its annual guidance (~9,700 ounces above the midpoint of 250,000 ounces).

New Gold – Quarterly GEO Production – Company Filings, Author’s Chart

Digging into the operations a little closer, Rainy River had a much brighter year after flooding that impacted production in 2022 and poor grade reconciliation at East Lobe that weighed on 2021 production. In fact, 2023 production was the best in years vs. three-year average production of ~237,000 GEOs (2020-2022), helped by an incremental contribution from the higher-grade Intrepid Zone (Rainy River Underground) where grades are reconciling well to date. In fact, throughput and grades were both higher year-over-year, driving a ~10% increase in output vs. its previous three-year average. That said, the best is yet to come, with much higher mining rates in the underground Main Zone where production should begin by year-end and ramp up throughout 2025. And combined with lower waste tonnes mined, we should see significantly higher production at lower unit costs.

The result? Significant free cash flow generation in 2025, once capex winds down. And while this might be a decade late relative to initial expectations relative to what Rainy River Resources (RR.TSX) initially put forth in 2013 in its Feasibility Study (~330,000 ounces at sub $800/oz all-in costs), it’s nice to see this asset finally turning the corner after what’s been a disappointing several years. And as for Q4 specifically, we saw more solid results with ~25,000 tonnes per day processed at 0.94 grams per tonne of gold, which was only down year-over-year because of the difficult comparisons. However, investors can expect a better 2024 with production of ~300,000 ounces of gold at improved unit costs vs. a $1,525/oz AISC guidance midpoint in 2023.

Rainy River Tonnes Milled, Grades & GEO Production – Company Filings, Author’s Chart

Moving over to New Afton, it was a solid year here as well, with significant improvements followed what was a tough 2022. This was evidenced by annual gold production beating the top end of guidance by a wide margin with ~67,400 ounces produced (guidance: 50,000 to 60,000 ounces in 2023), or ~62,600 ounces of gold without the benefit of ore purchases. Meanwhile, copper production also came in significantly higher at ~47.4 million pounds, above the guidance midpoint of 43 million pounds and significantly higher 31.1 million pounds last year. The significant increase in production was helped by higher grades, throughput, and recoveries, with New Gold stating that mining from the B3 Zone continues to perform “above expectations” continuing a trend of strong performance in Q3 as well.

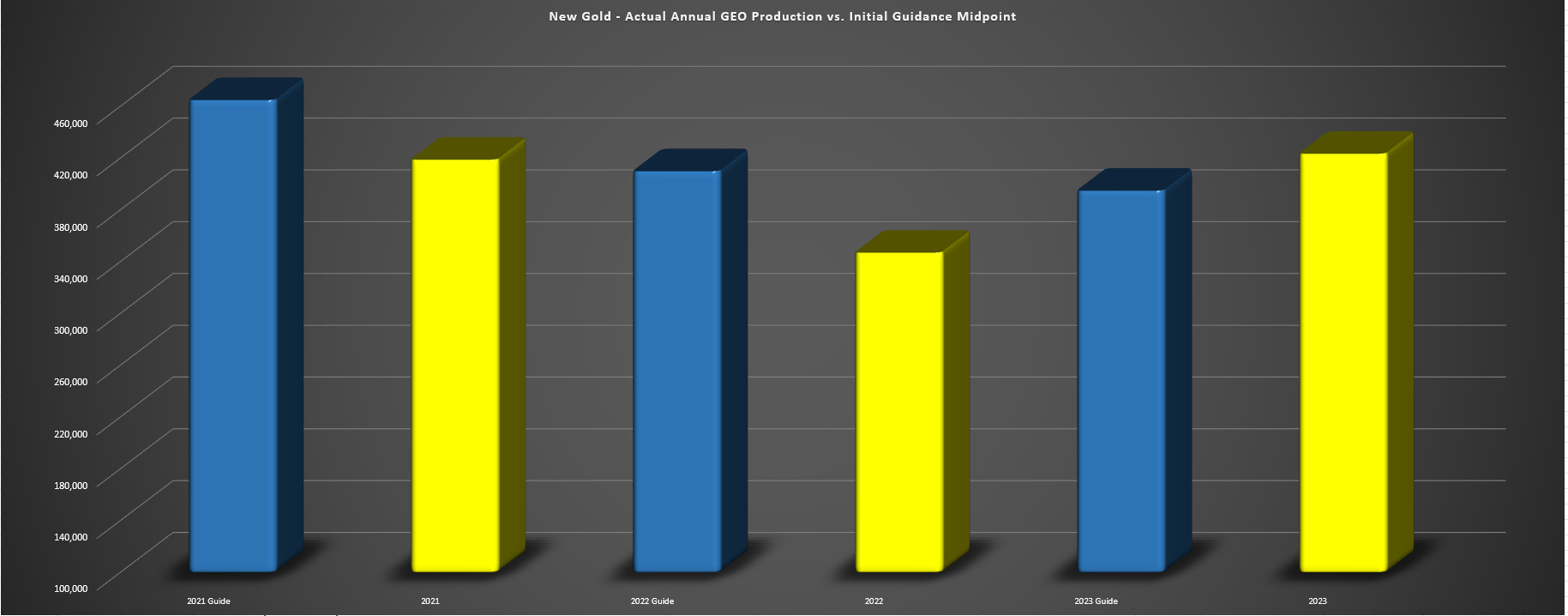

New Gold Actual Annual GEO Production vs. Initial Guidance Midpoint – Company Filings, Author’s Chart

Given the solid performance at both assets in Q4, New Gold was able to deliver miles above its initial guidance midpoint of 395,000 gold-equivalent ounces for FY2023, reporting a 7% beat with annual production of ~423,500 GEOs. This reversed a trend of over-promising and under-delivering in the prior two years, and by a significant amount with an average GEO shortfall of 50,000+ GEOs vs. its guidance midpoint in 2021 and 2022. And given the solid execution to date and over-delivery on promises under new CEO Patrick Godin (formerly Pretium Resources COO), and new COO Yohann Bouchard (formerly Yamana Gold COO), I would expect another very solid year in 2024.

This is especially true especially with much of the heavy lifting complete as the company works to reap the rewards of the more productive C-Zone (opportunity to tap into excess capacity at the New Afton plant), and a significant lift in overall grades at Rainy River Underground, similar to what OceanaGold will enjoy at Haile in South Carolina (benefiting from higher-grade Horseshoe Underground ore). Let’s dig into the 2024 and 2025 outlook:

2024/2025 Outlook

While it was certainly encouraging to see better results in 2023 after two disappointing years, I would expect another solid year in 2024 with 400,000+ GEOs in what’s a transition year for the company. This is because New Gold continues to work on developing towards the Main Zone underground at Rainy River where production should begin in Q4. Meanwhile, the company has confirmed that commercial production at the C-Zone at New Afton will also start in the second half of this year, with a plan to ramp up to full production by the end of 2025. However, even if production could dip after a very strong 2023, this will be made up and more in 2025, with annual GEO production likely to increase above 440,000 GEOs at much lower costs (sub $1,300/oz AISC). Meanwhile, although production could be down next year, I would expect positive free cash flow at current metals prices after two capital intensive years in 2022/2023.

New Gold – AISC, Realized Gold Price & AISC Margins – Company Filings, Author’s Chart

As for the cost outlook, New Gold has done a solid job keeping costs in check despite inflationary pressures, with a clear downtrend in costs following a brutal 2022 ($1,800/oz plus AISC). And while I would still expect costs above the industry average in 2024 (estimated industry average costs for 2024: ~$1,420/oz), we should see AISC below $1,480/oz, a slight improvement from 2023 levels, setting up margin expansion if gold prices can continue to hang out near $2,000/oz. That said, the real benefit will come in 2025 when Main Zone Underground and the C-Zone are both contributing at closer to full production levels, with New Gold’s AISC margins set to improve to $700/oz or better. And when combined with the potential to generate upwards of $200 million in free cash flow in 2025, I would expect a re-rating in the stock as we get closer to this inflection point if it can execute successfully.

Recent Developments

Finally, looking at recent developments, many investors have heard lots of talk about the C-Zone, but they may not realize the full impact. To put it in perspective, production is expected to increase to ~70 million pounds of copper and ~90,000 ounces of gold, which represents a 44% increase in gold production and 48% increase in copper production vs. 2023 and even higher growth vs. the 2023 guidance midpoint which New Gold easily beat. Not only will this significantly improve margins with a much higher throughput rate, but it will allow for a significant increase in free cash flow at the same time as Rainy River will also enjoy $800/oz+ AISC margins. However, New Gold remains quite optimistic about its ability to extend the mine life at New Afton, with the company noting that it should be able to increase reserves to extend the mine life past 2030.

New Afton Block Cave, Concept ML Extension Opportunities + Resource Envelope – Company Website

Looking at the above images, we can see that the C-Zone Block Cave is just below B3, but there is significant resource upside with a relatively low hurdle to adding reserves given that block caves are extremely expensive up front to develop, but then benefit from industry-leading costs once in production (New Afton’s cut-off grade is sub $30/tonne with block cave while Macassa’s cut-off grade with overhand and underhand cut & fill in Ontario is ~$300/tonne). And as the above chart highlights and New Gold has stated in past updates, there is room for potential mine life extension by increasing column height beyond 350 meters, besides the opportunity to include additional drawpoints on the eastern side of the C-Zone. Meanwhile, the company could have another block future block cave in the D Zone, and drilling at the K-Zone drilling to date has been encouraging, with intercepts like 14 meters at 0.64 grams per tonne of gold and 0.64% copper (~$95/tonne rock).

In summary, while New Afton’s mine life may be relatively short compared to other massive block caving operations like Northparkes and Ernest Henry owned by Evolution (OTCPK:CAHPF) in Australia, there looks to be considerable upside to extend this into the late 2030s and potentially the 2040s.

Valuation

Based on ~693 million fully diluted shares and a share price of US$1.31, New Gold trades at a market cap of ~$910 million, making it one of the lower capitalization ~400,000 ounce producers in Tier-1 jurisdictions. This lower valuation is partially justified by its higher costs and relatively high leverage compared to some of its mid-tier peers (~$400 million in debt) and its high cost profile currently relative to peers like Alamos Gold (AGI), Dundee Precious Metals (OTCPK:DPMLF), and Centerra (CGAU). However, New Gold trades at a far lower FY2024 cash flow multiple and its margin profile will improve materially looking out to 2025. Hence, while it may trade at a low market cap today, I would not be shocked to see it trade closer to a $1.5 billion market cap in 2025 once it starts generating significant free cash flow.

New Gold Cash Flow Multiple & Historical Multiple – FASTGraphs.com

Using what I believe to be a fair value of US$1.85 (18-month target price), I see a 41% upside from current levels for New Gold, and this assumes it trades at a conservative free cash flow multiple for a Tier-1 jurisdiction producer of just ~6.0x (FY2025 estimates). That said, I am looking for a minimum 40% discount to fair value when it comes to small-cap producers to ensure a margin of safety, and this points to an ideal buy zone for NGD of US$1.12 or lower. So, while I think any further weakness should set up a buying opportunity, I don’t see NGD in a low-risk buy zone just yet.

Summary

New Gold had a great year in 2023 under new leadership and is just a year away from a transformation that will turn it into a free cash flow machine in 2025 through 2027. Notably, the timing on this turnaround and free cash flow inflection point is certainly advantageous, with the company benefiting from much higher gold prices as it starts extracting its most valuable ore at both of its mines. And as we see margins and free cash flow improve starting in Q4 2023, I see a path to a much higher share price for patient investors and I’d expect any pullbacks below US$1.10 to provide buying opportunities.

Thanks for reading!

Q2 2024 Earnings Call Transcript")