The success of Netflix Inc.’s new advertising-supported tier signals significant upside to 2024 estimates for the streaming giant, Oppenheimer said Friday, as it raised its price target for the stock to $600, the highest among Wall Street analysts.

The 26% price increase from Oppenheimer’s previous price target of $475 comes after Netflix’s

NFLX,

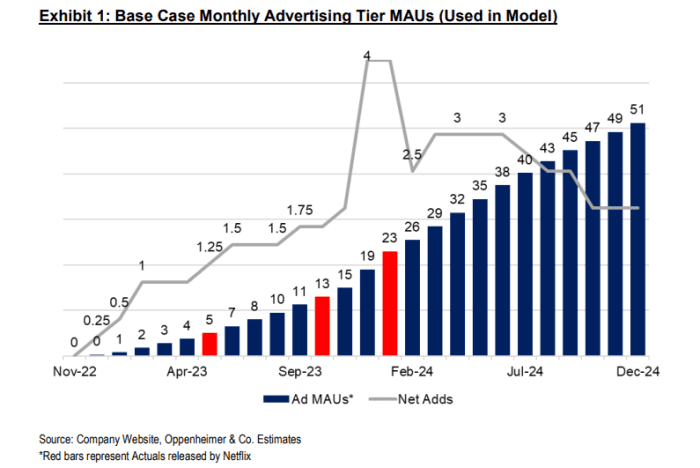

head of advertising, Amy Reinhard, said at this week’s CES consumer-technology conference in Las Vegas that monthly active users for the ad service had grown to more than 23 million, up from 15 million in November and from 5 million in May. The cheaper ad-supported tier has been available for about a year.

“Near-term, the acceleration suggests fourth-quarter net additions above guidance/Street,” analysts led by Jason Helfstein wrote in a note to clients.

The pace of growth “suggests plenty of room for [subscription] growth in 2024,” Helfstein said, as his team raised its fourth-quarter estimates for net additions to 10 million-plus from 9 million, and its 2024 estimate to 24 million-plus from 21 million-plus. The Wall Street consensus is for 9 million-plus additions in the fourth quarter and 18 million-plus for 2024.

The faster that Netflix reaches scale in advertising, the faster its ARM levels can reset higher, the analysts wrote. ARM is defined by Netflix as streaming revenue divided by the average number of streaming paid memberships divided by the number of months in a period.

Read now: This one nugget from Netflix’s viewership numbers could be a bullish sign for its ad business

Advertising has “significant” incremental margins, the analysts said, with Oppenheimer now expecting $6 billion in ad revenue in 2025. That would imply $4.8 billion in incremental Ebitda, or earnings before interest, taxes, depreciation and amortization, based on an assumption of an 80% margin. That’s well above the estimate for 2023 for Ebitda of just $7.3 million.

“This should then allow cash content spend of $19.5/$21 billion in 2025/2026 vs. $17 billion guidance, leaving ~$17.5 billion of cash after

$14.5 billion of buybacks. Either Netflix can increase their content moat, repurchase more stock or both,” the analysts wrote.

Overall, Oppenheimer is expecting Netflix to add 10 million subscribers in the fourth quarter, which is higher than the Wall Street estimate for 8.7 million.

Oppenheimer has an outperform rating on the stock, the equivalent of buy. Analysts polled by FactSet have an average overweight rating on the stock, also equal to buy, with an average stock price target of $480.20.

The stock was up 0.5% Friday and has gained 50% in the last 12 months, while the S&P 500 has gained 20%.

Read now: Here’s what’s worth streaming in January 2024: ‘Masters of the Air,’ ‘Echo,’ ‘Griselda’ and more

Q2 2024 Earnings Call Transcript")