kynny

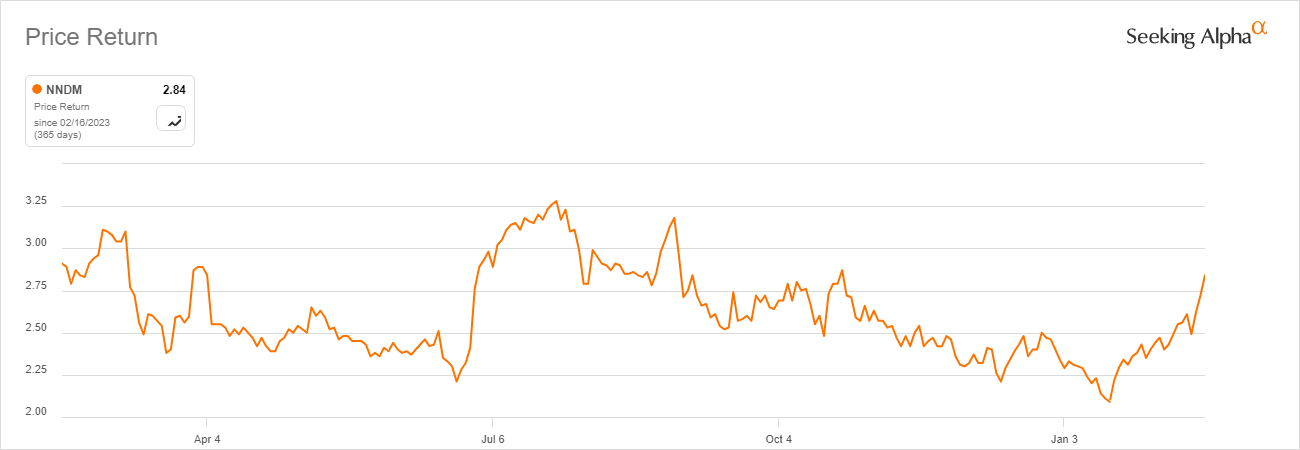

Nano Dimension (NASDAQ:NNDM) is an Israel-based provider of additive electronics, including 3D printers, the DragonFly IV being their flagship product. Over the last year, focus has shifted more onto the management of the company, their acquisition strategy, and a resulting power struggle involving activist investors. The stock has endured a significant decline since it first listed on the NASDAQ in 2016, a feature not uncommon in the 3D printing industry. Owing to the current uncertainty around the acquisition strategy, an unclear path to profitability, geopolitical concerns and other risks I have a neutral view at this price.

Seeking Alpha

Q3 2023

Nano Dimension had a relatively strong Q3, with quarterly revenue of $12.2 million, up from Q3 2022 by 22% and gross profit up by 108%. The company has a huge cash/short term investment balance of $872.7 million raised mostly through direct public offering during 2021 exceeding the current market cap by over $200 million. Management currently wants to put it to use through an acquisition strategy, a key consideration when looking at this stock which will be covered later. The R&D spend came in at $12.8 million, down from Q3 2022 but still quite large for a company Nano’s size. There was also mention of share buybacks, with the possibility of another $200 million currently under consideration.

Yoav Stern, Q3 earnings call:

On the gross margins, I spoke, but if you now go to the bottom line on this table, look at the number on the bottom. We only burned $7.7 million comparing to $20 million in the same quarter last year. This is where we are going, we are hoping next year–actually, already this quarter to cut another $30 million in our expenses, and to reach profitability at the end of the year next year. But even if we are just growing from where we are today, a run rate of 60 organically, if we do an acquisition, it will obviously change the whole formula, which is very, very exciting to us.

This means by 2025, Nano aim to become profitable through cutting an estimated $30 million in expenses this year, as well as already having reduced their workforce by 25% in Q4. Nano expects $56.2 million FY revenues, up 29% from 2022.

DeepCube

Acquired in 2021, DeepCube has been attracting attention due to the market’s current fervour for AI. Increasingly, companies that can deploy AI and reap the rewards pique my interest at least as much as companies involved in the development of AI models, because intuitively monetisation seems easier through usage in established industries to improve efficiency. Nano Dimension’s DeepCube falls into this category, using AI and deep learning to perform real time error correction and improve the speed of data analysis.

According to CEO Yoav Stern, DeepCube technology is now included in each product line. However, it’s important to separate this AI from the recent wave of AI hype, their main work up to now having little to do with the generative AI driving valuations elsewhere in the market. That may be changing somewhat though, with the company having filed two patents for LLMs performing real time data analysis of industrial machines. As management highlights below, DeepCube may provide more value to the company than was originally envisioned.

Yoav Stern, Q2 2023 earnings call:

And remember, we originally bought DeepCube for the purpose of applying the technology inside our machines and in our cloud network — cloud manufacturing network, but now it seems like DeepCube is going to become a profit center by itself and a revenue generator by itself.

How much efficiency or even revenue DeepCube will add over time is still unclear with these developments still being in their infancy but the possibility for substantial growth is promising.

Corporate Governance Woes

To say that there has been drama last year regarding Nano Dimension’s management would be an understatement. In March, there was an attempt to remove and replace the Chairman and 3 directors via special meeting called by Nano Dimension’s largest shareholder, Murchinson. The result was in favour of his removal, though the validity of the vote was disputed by Nano Dimension who stated that 90% of unaffiliated shareholders either did not participate or voted against Murchinson and filed a lawsuit declaring it’s illegality. Subsequently, the company has had a few relatively good quarters, attempted to acquire competitor Stratasys (SSYS) and voted to keep the current management.

Aside from a $17 million cost, the reason this is relevant for investors is not just because of matters relating to stability within management but because the crux of the dispute lies in the aggressive M&A style being used by management and if it is the correct way to use the massive stockpile of cash available. On balance, I think that the shareholder decision to keep the current board is a net positive for the stock as the vision is clear, if risky.

In July, Nano tried and failed to buy Stratasys with a $25 per share offer, and in December made another offer of $16.50. If history is anything to go by, it seems doubtful to go through. This all begs the question: what next? Management previously stated they intended to continue with ‘alternative’ M&A plans, but with the 3D printing industry being relatively niche, there are a limited number of likely options. Some larger publicly traded peers include 3D Systems (DDD), Desktop Metal (DM), Markforged (MKFG) and Velo3D (VLD). Companies more tangentially related to the industry but with clear synergies are also fair game as DeepCube proves, which expands the space of possibilities quite a bit.

Yoav Stern, Q3 2023:

Yes, we are looking at companies with a full line profile, above $100 million of revenue, in the areas of either electronics, additive electronics and additive manufacturing that is not electronics, and the market over the next 12 months is right ahead of us.

With this in mind, among those already mentioned Markforged and Velo 3D are only just clearing, or not quite clearing $100 million of revenue so perhaps this reduces their chances of being acquisition targets. All considered, who Nano will select next as an acquisition target remains somewhat of a black box for potential investors.

The Wider Industry

3D printing as an industry had a lot of buzz a handful of years ago and since the hype has cooled somewhat. It resembles a Gartner hype cycle in retrospect, with the technology likely now being well past the peak of inflated expectations, and therefore a more reasonable time to consider entry. There is an increasing focus on both the resilience of supply chains and decarbonisation of industrial processes globally, which should prove to be powerful catalysts for 3D printer adoption, a technology which tackles both issues.

By some projections, the 3d printing industry has a projected CAGR of 22.63% until 2028, but it could prove higher still. Yoav Stern addresses this as well as the current market dynamics below.

Yoav Stern on TAM, Q4 2022:

This market is $16 billion going according to industry reports to $205 billion in 5, 6 years. So forget 5, 6 years, let’s say, $16 billion today, let’s say, it’s going to $20 billion in a year or 2. And there is no 800-pound gorilla. There is no large company. The largest companies are two, which is Stratasys and 3D, and they are not too large for a market that’s $16 billion. They are only $0.5 million, $600 million each, give or take and they are not doing the right things in order to consolidate the market plus they are not capitalized properly. We do, and we are, and we intend to do it based on synergies and based on technologies and based on running a business that is focused on the bottom line, not on the top line.

This is the bull case for Nano Dimension in straightforward terms: the 3D printing industry is expanding quite rapidly and Nano Dimension is pursuing growth at all costs to expand with it. The cynical view might be that management is not allocating capital efficiently and the challenge from activist investors is a good thing.

Valuation

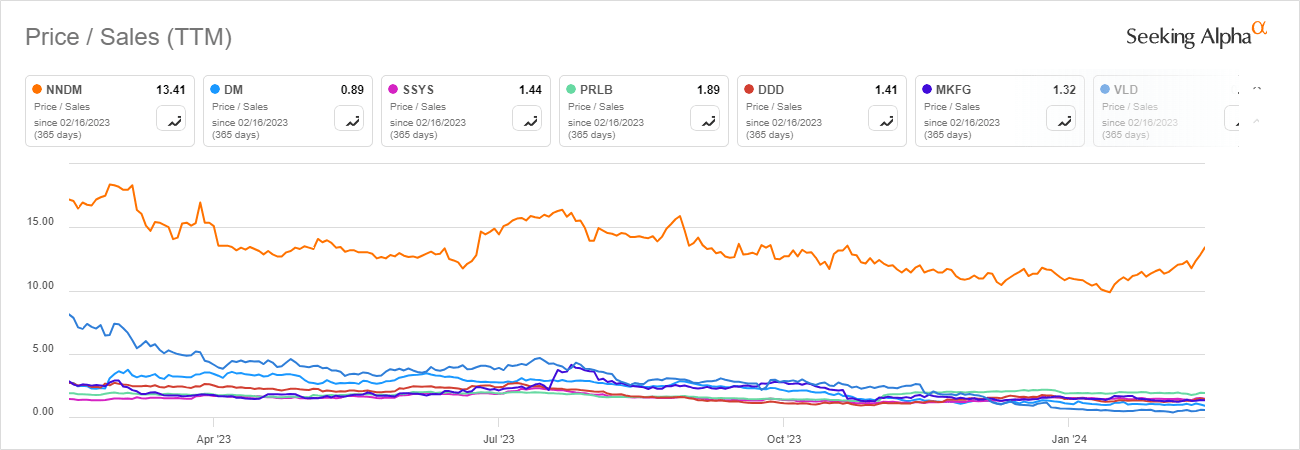

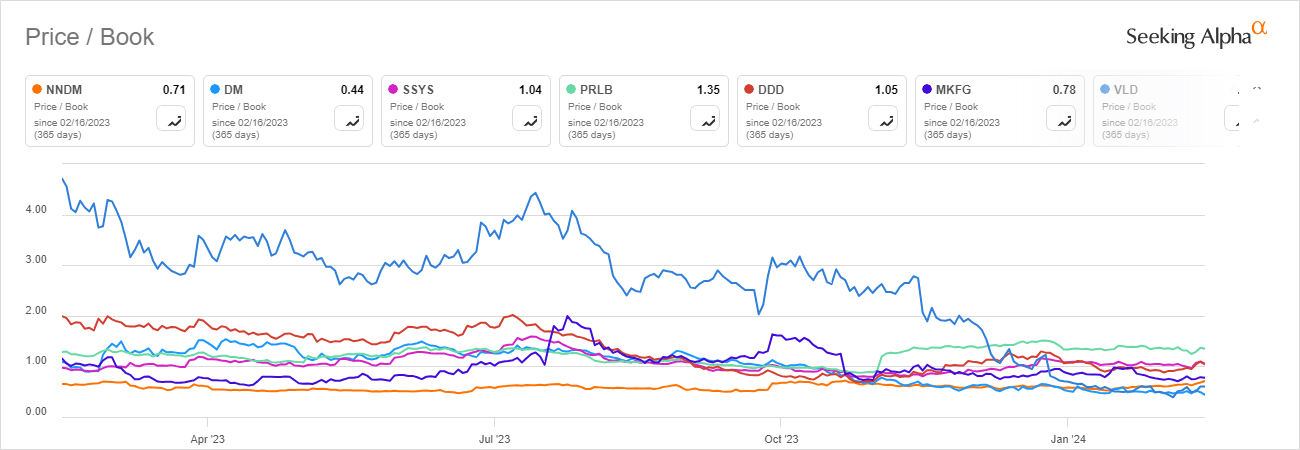

Compared to peers, Nano Dimension has a high Price/Sales ratio of 13.41 likely stemming from relatively low revenues. This might be a red flag for overvaluation but this does not take into account the company’s abnormally huge cash reserves which also gives a low Price/Book of 0.71. In other words, this is a relatively small company in terms of revenue sitting on a huge pile of cash. This underscores the importance of whether the current acquisition strategy is successful.

Seeking Alpha Seeking Alpha

Risks

The main risk is that the current acquisition strategy fails somehow, whether it be overpaying for an acquisition, or it is thwarted by activist shareholders. It is undoubtedly the main risk because the mammoth, larger than market cap cash pile is currently mostly earmarked for future acquisitions. The current cash runway may look huge, but as admitted by management, a large portion is not intended to sustain operations, but rather to fund ambitious acquisitions.

Yoav Stern, Q3 2022:

The cash that is earmarked for acquisitions in the next three to five years is between $600 million to $800 million.

Assuming these take place which will likely be the case absent Stern’s removal, the cash runway would likely be significantly diminished and give the stock a similar level of risk to other competitors. Therefore, it is misleading to view the company’s cash as a buffer given the current trajectory.

Another risk to the acquisition strategy is selection of potential targets. Any investors are in part taking a bet that this $600-$800 million is spent not only for acquisition(s) at fair value but also those with significant synergies and ability to generate organic growth. The company is also quite far away from profitability, has had a decent amount of volatility and should be seen as a speculative play.

Lastly, Nano Dimension is based in Israel so the current conflict could pose a risk to business domestically. Nano has R&D and manufacturing facilities within Israel, and recently mentioned that 15% of their employees are currently in the reserve fighting in Gaza.

Conclusion

Nano Dimension is a company with a lot of cash and an aggressive acquisition strategy. Now that Stratasys is less likely as an acquisition target, some uncertainty has been generated about where that cash will go instead. Going for it are positive quarterly results, an AI product in DeepCube that could capitalise on current trends, and an industry well poised for future trends. However, uncertainty regarding management and the current expansion at all costs strategy make further volatility in the stock likely. With the latest acquisition attempt failing investors essentially have to trust the plan and hope that the next target is chosen with prudence. The risks do not fit with my personal investing style so for now I will be staying away.

Q2 2024 Earnings Call Transcript")