AzmanJaka/E+ via Getty Images

Nano Dimension Ltd. (NNDM) is in the throes of an unsolicited takeover of Stratasys Ltd. (SSYS). Both are Israel-based companies. Both are in the expanding 3D printing business. The share prices are down over the past the last 5 years. The Seeking Alpha Quant Rating for Stratasys stands at Sell and Hold for Nano Dimension. S A warns investors, Stratasys “is at high risk of performing badly.”

In our opinion, we do not see either company as a Buy opportunity at this time for retail value investors. The upside potential is too risky shortly, despite growing revenue.

Stratasys Risk

Stratasys investors will profit from a buyout that Nano Dimension seems committed to pursuing at this time. Stratasys seems to be playing hard to get. Nano Dimension made several cash unsolicited proposals to buy out the ~85% of outstanding shares it does not yet own. Offers range from $16.50 per share, or about $3 per share higher than the current selling price, to $25, according to a reporter for the 3D Printing Industry newsletter.

But the Stratasys board holds a poison pill. In December ’23, the targeted firm adopted a shareholder rights plan, as reported by S A. In the CEO’s opening message to shareholders following the release of a flat revenue Q3 ’23 financial report in November ’23, was the immediate appointment to the board of Aris Kekedjian. The new director brings expertise in investment management and M&A; it makes us think more time is going to pass, and both companies will incur more expense as Stratasys looks for ways to fend off another proposal or demand more from Nano.

The company generated more revenue each year between 2015, ’16, ‘17 and ’18 (on average $675M) than recently: FY ‘2019 (636.1M), 2020 ($520M), 2021 ($607.2M), and for FY ’23 we are forecasting full-year revenue of $620M to $630M. The firm’s gross profit was greater in those earlier years and losses from operations were less than we anticipated for FY ’23, except FY ’20.

The share price collapsed after Stratasys rejected earlier offers. The price fell from a 52-week high near $22 to about $10 in October; part of the slide can be attributed to the invasion of Israel and the massacre by Hamas, when Israel-based stocks trading on a U. S. exchange dipped 15% to 20%. The price recovered somewhat, up a few dollars, but -4% YTD.

Despite the financial conditions, short interest is a mere 2%; we believe there are hopes for a buyout. Hedge fund interest increased in 2023 as Nano came back with proposals. 15 funds owned the stock in Q1 ’23, 17 at the end of Q2 ’23, and 19 funds owned shares in Q3 ’23. Nearly 2 dozen owned Stratasys shares between 2021 and through September ’22 when the price popped on talk of a buyout.

On the downside, Cathy Wood’s fund owns nearly a million shares and is -37% on Stratasys shares; there is a lurking possibility her fund can sell off the shares at a moment’s notice, which will drive down the share price. Or her fund can hold shares, hinting a better higher price is in the offing from Nano. But this is all a casino gamble, of which retail investors need to be wary.

Profiles

The 3D printing industry began to draw attention around 2013. We wrote in 2016 that 3D printers are revolutionizing medicine. Rambam Hospital in Israel printed and implanted a new titanium jawbone for a wounded Syrian. IAE Research cautioned in 2013 on S A to not let Wall Street’s growing infatuation lead investors to believe that 3D printing was revolutionizing manufacturing and other sectors of the economy anytime soon. Progress has been made, but the industry is developing.

Nano Dimension’s CEO told shareholders last November that using 3D printing for mass production “is still some way off from achieving full-scale mass production.” Statista estimates the global 3D printing materials market will grow from $1.53B annually in 2018 to $3.78B in the next two years. The printer market is going to grow at a CAGR rate of 24% as more industries in addition to medical and aerospace turn to 3D printing.

AI can increase the use of 3D printing. Tech analyst Tessa Axsom, writing for a 3D print company, claims its

- Applications in 3D printing led to better prints with fewer errors.

- It is expanding into new sectors rapidly used in virtually every sector of product production, consumer and military purposes, on Earth and in space.

- Efficiencies are improved.

- The design process speeds up and can produce “many iterations.”

- Material science technicians are more productive.

Stratasys Ltd. products include various high-tech printers, printing systems software and services, and consumable materials including 3D printing materials for manufacturing, tooling, and rapid prototyping.

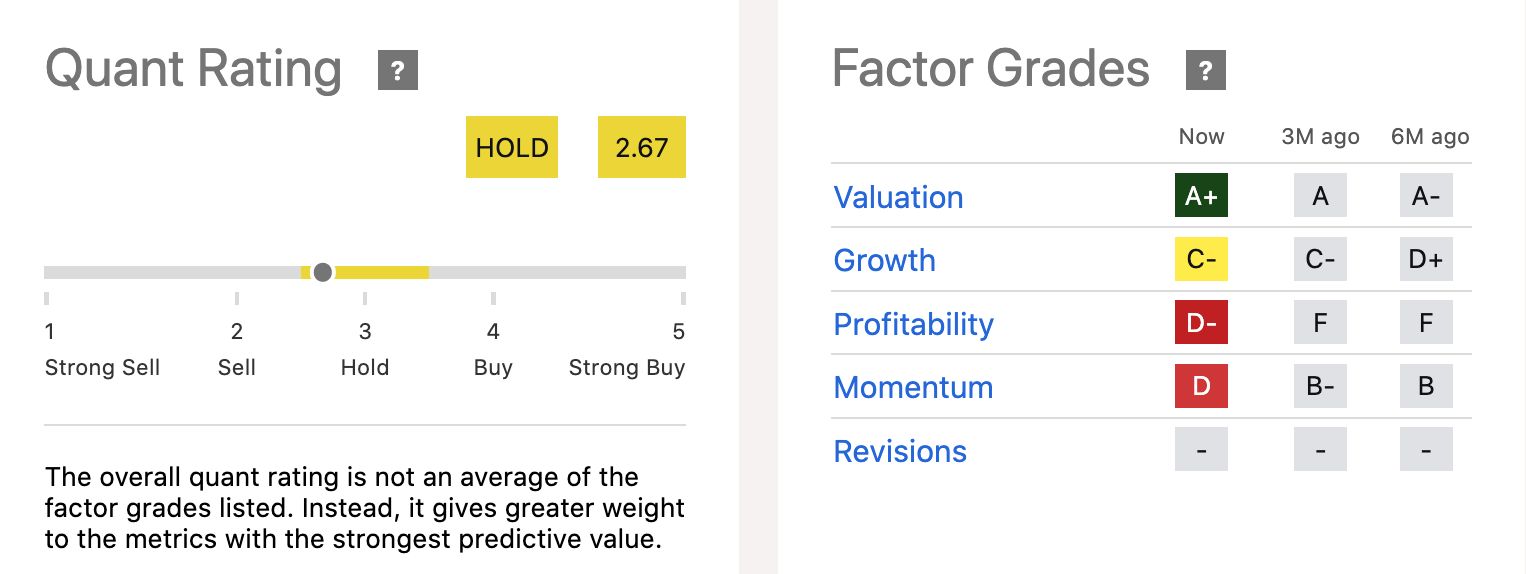

Quant Rating & Factor Grades (Seeking Alpha)

Nano Dimension Ltd. is heavily into hardware. It offers 3D printers and proprietary conductive and dielectric substances that integrate in-situ capacitors, antennas, coils, transformers, and electromechanical components. Its printers can fabricate ceramic and metal parts. The company focuses on electronics robotics and control systems. In addition, the company offers software and services.

Quant Rating & Factor Grades (Seeking Alpha)

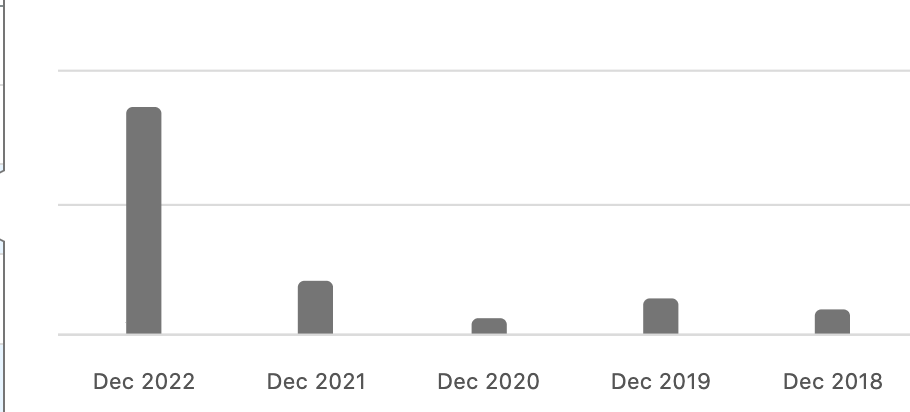

Revenue at Nano Dimensions has consistently grown from acquisitions and some organic growth. Stratasys will fit nicely into Nano’s operations, but management needs to know what Nano resources it can bring to Stratasys more than vice versa. They have not shared that yet. As an S A chart demonstrates, Nano’s revenue over the years is on the rise:

Revenue Growth (Seeking Alpha)

Gross profit went from 1.8 in 2020 to an anticipated 30.7 for 2023. We expect losses from continuing operations and negative net income will be lower, ~$140M, than in the previous two financial years. A risk to watch is the continuing cash flow from operations losses that in FY ’23 will top ($100M) versus ($92.1M) last fiscal year and ($42.6M) in FY ’21. The company has also spent +$17M on legal fees and expenses for various endeavors that management has to get under better control, in our opinion.

For transparency’s sake, we alert readers to the vision of the CEO reported in a press release for Q4 ’23. Nano needs to balance revenue growth with upping earnings:

Nano Dimension expects reported unaudited consolidated revenues of approximately $14.3 million for the fourth quarter ended December 31st, 2023, and approximately $56.2 million for the full year ended December 31st, 2023. Q4/2023 revenue is expected to grow 18% from Q4/2022, with full year 2023 revenue expected to grow 29% from full year 2022.

Nano acquired 4 companies in the last 5 years, one in particular to build its AI capabilities in the 3D printing business. Yet, it still has $872.7M in cash and equivalents on hand but expenses and losses ate away a substantial amount on hand in previous years (+$1B in ’22 and ~$1.3B in ’21).

Debt is a mere $9.58M. Adding in total receivables, we believe the company has a healthy financial outlook. We give management a high mark for the company’s liquidity and being able to pay liabilities. But while revenue ticks up, management has to pay more attention to earnings and net income, as this chart from Macroaxis.com demonstrates. The next earnings report (Q4 ’23) is expected on March 14, ’24.

Earnings & Revenue (Macroaxis.com)

Nano is in the process of reshaping the company; it cut 2 members from the board, wants to raise the gross margin to 50%, eventually repurchase $300M worth of its shares, and cut SG&A further. It appears that the current top management is in control of the company after a costly power struggle with a Canadian investment firm; those events are never good because they cost the shareholders money and divert focus from operations.

There is not much to report in the way of valuation metrics except to point out that the price to sales is 10.39 compared to the sector median of 2.9. The price to book is 0.66 to the sector median of 3.05. We do not find much gravitas in either metric as a share price influence. The market cap for Nano is $517.24M; greater concern ought to focus on the short interest at 7.6% on a stock selling at $2.20 per share that two years ago was over $15 each.

Takeaway

We believe 3D printing will exponentially grow and the smaller companies capitalizing on steady growth will double and triple in size over the next half-decade. Incorporating AI into the 3D process is a must, as AI develops. At this time, the risk/reward ratio for retail value investors in Nano Dimensions is too high to expect the share price to rise enough over the next two or three quarters.

For instance, one worrisome indicator hitting the industry is the Strong Sell Quant Rating The 3D Printing ETF (PRNT) gets from S A. Grades are all Ds and Fs. Nano Dimension’s leadership recognizes that it must keep its attention on cost containment going forward and states it is committed to “cut major expenses in overhead through consolidating facilities with acquisitions that we will do, and that will take us to the right place.”

Another acquisition is going to require a great deal lot of management attention and Nano has to decide what it can bring to Stratasys that will enhance that company’s SG&A and earnings; management has not spoken much about that, and it concerns us.

Q2 2024 Earnings Call Transcript")