olrat/iStock via Getty Images

MYR Group Inc. (NASDAQ:MYRG) is a holding company of leading specialty contractors that service the electric utility infrastructure, commercial and industrial construction markets in the U.S. and Canada.

The company has two business segments, a Transmission & Distribution segment (“T&D”) and a Commercial & Industrial segment (“C&I”).

In 2023, MYR Group’s T&D segment had full year revenue of $2.09 billion and the C&I segment had revenue of $1.55 billion.

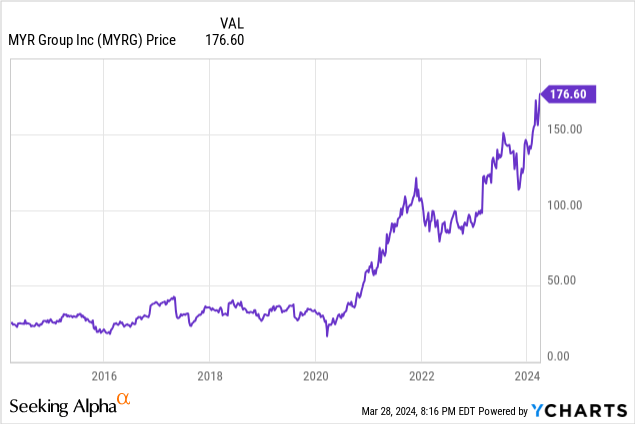

Since 2020, MYR Group’s stock price has done really well, rising from around $32.43 in the beginning of 2020 to around $176.60 as of March 28.

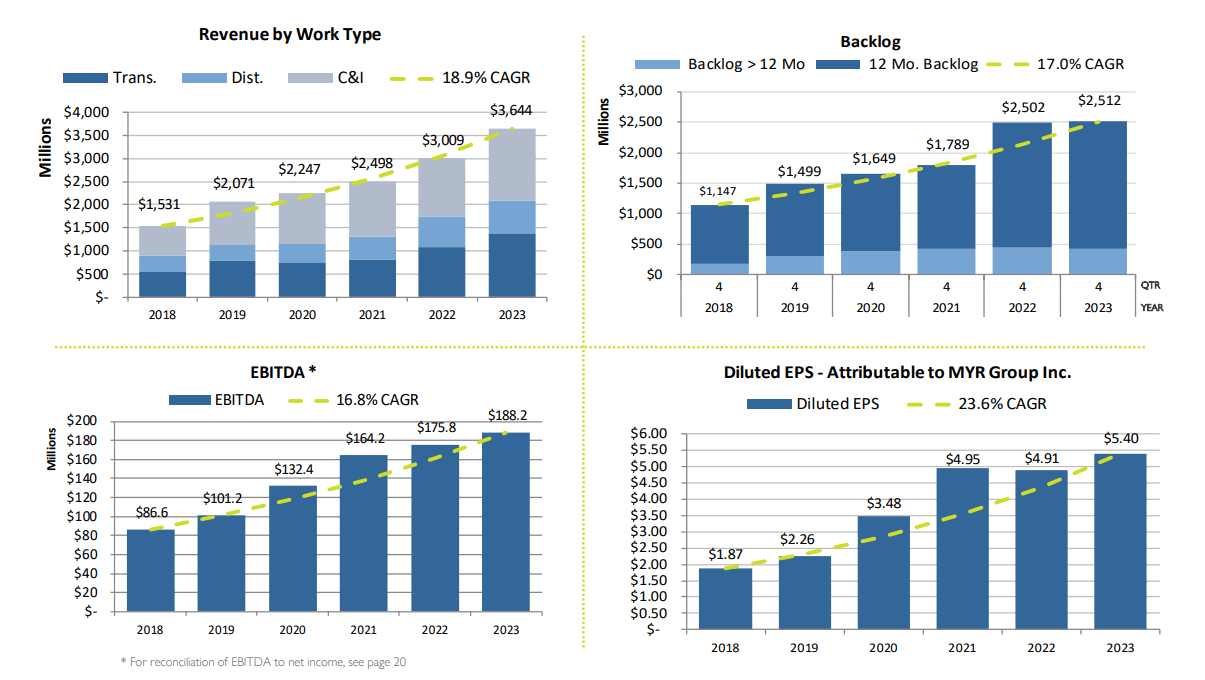

Since 2018, MYR Group’s financials have benefited from growing demand given tailwinds from the clean energy transition, and increasing investment in upgrading and improving the electric grid.

In terms of financials, MYR Group’s diluted EPS has more than doubled from $1.87 in 2018 to $5.40 in 2023. Meanwhile, revenue, EBITDA, and the company’s backlog have increased considerably since 2018 as well.

MYR Group Investor Presentation

On February 28, 2024, MYR Group reported full year 2023 results that indicated substantial demand strength and continued financial growth.

2023

In 2023, MYR Group revenue rose 21.1% year over year to $3.64 billion.

Revenue in the T&D segment rose 19.7% year over year to $2.09 billion given increases in revenue on transmission projects and distribution projects. Sales in transmission projects rose primarily related to an increase in revenue on clean energy projects.

Revenue in the C&I segment rose 23.1% year over year to $1.55 billion thanks to higher revenue related to clean energy projects in certain geographical areas.

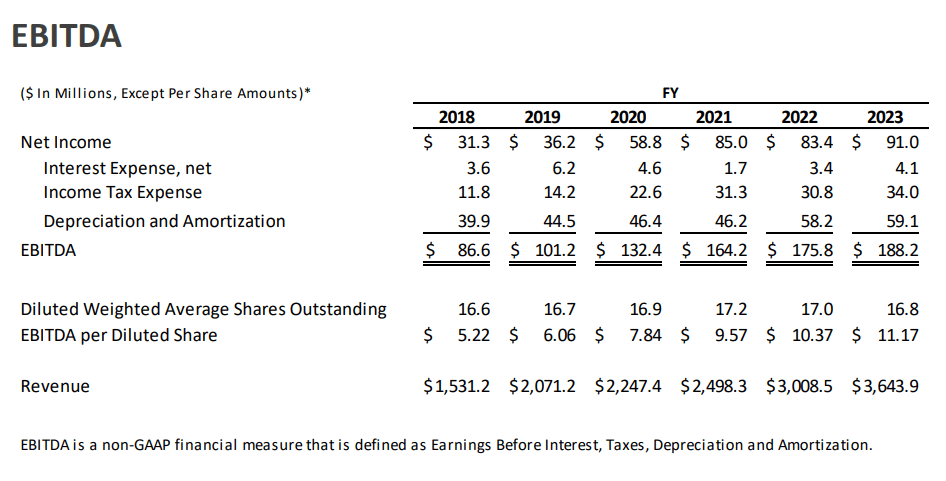

Full year EBITDA rose to $188.2 million in 2023 from $175.8 million in 2022.

MYR Group Investor Presentation

Net income for the year rose to $91 million, or $5.40 per diluted share, from $83.4 million, or $4.91 per diluted share, for the same period of 2022.

MYR Group’s backlog also increased marginally to $2.51 billion at the end of 2023, up from $2.5 billion at the end of 2022. T&D backlog was $959.6 million and C&I backlog was $1.55 billion at the end of 2023.

Furthermore, MYR Group maintained a strong balance sheet with funded debt to LTM EBITDA leverage of 0.19x as of the end of 2023. At the end of the year, MYR Group had $442 million of availability under its $490 million credit facility, giving management flexibility in terms of capital allocation decisions.

In terms of M&A, MYR Group has had a lot of organic growth in recent years and management is willing to be patient in terms of acquisition opportunities as a result.

My takeaway is that 2023 was another strong year of financial growth for MYR Group as demand continued to strengthen in the last several years.

Outlook

When it comes to outlook for 2024, CEO Rick Swartz said the following during the Q4 2023 earnings call when asked about top line trends based on the awards that the company has had,

I would still look at the high single-digit growth for the year, probably a little — weighted a little more heavy towards the second half of the year.

Swartz added,

And as we said before, this year, we really want to focus on though we don’t mind growing our top line, and we still see it coming in, in kind of that higher single-digit. We’re really going to focus on that bottom line growth, and this all takes that into account. We want to make sure that the work we’re doing and we take on is profitable going forward.

My takeaway is that 2024 might be a slower year in terms of top line growth than 2023 given demand can be lumpy from time to time. Nevertheless, management is very positive in terms of the amount of work that’s out there and I think MYR Group’s top and bottom line will continue to grow at a fairly strong rate well into the late 2020’s given how big the demand tailwinds are.

Tailwinds

MYR Group benefits from increasing electricity usage and also the clean energy transition.

In the past few decades, electricity usage in the United States and Canada has not increased much due to increasing energy efficiency.

According to the EIA, in fact, total U.S. electricity consumption rose only 6.1% in the last 10 years from 3832 terawatt-hours in 2012 to 4067 terawatt-hours in 2022.

Nevertheless that trend might change as electricity demand is expected to increase from 2.6% to 4.7% in the United States over the next five years, with potentially $630 billion in near term investment required to meet load growth according to the December 2023 report from the Clean Grid Initiative.

For the future, I think electricity usage will be considerably higher than expected given the substantial growth potential in EVs and data centers. As such, I would not be surprised if electricity demand growth were higher than the 4.7% top range that the Clean Grid Initiative predicts over the next five years.

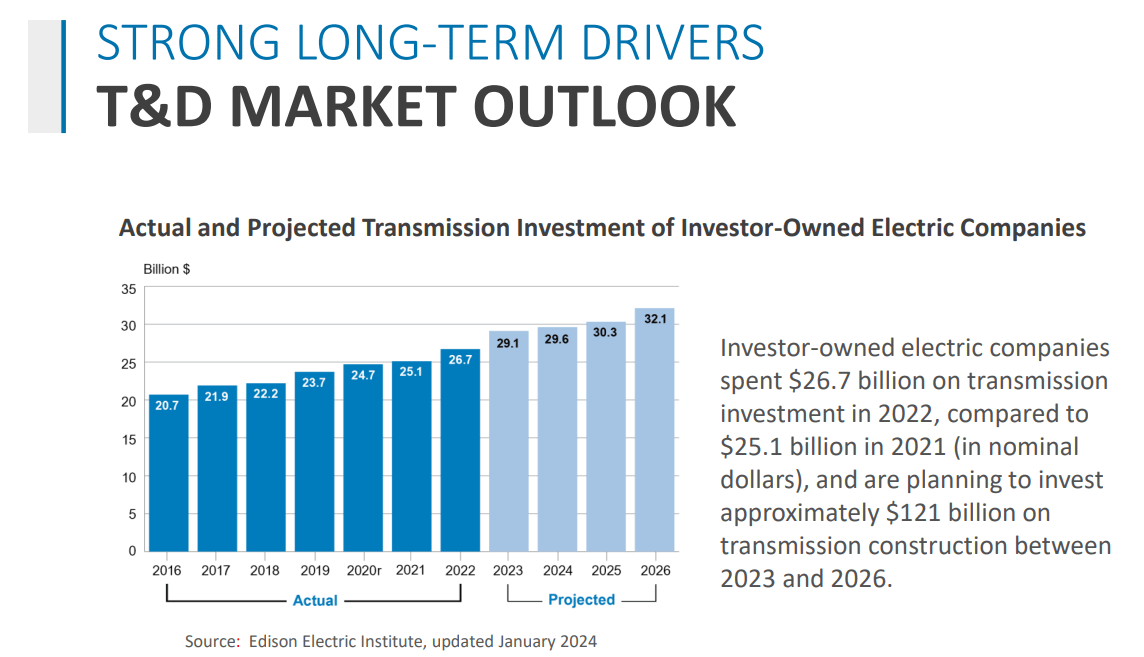

As a result of the increase in need to meet load growth, investor-owned electric companies are expected to invest $121 billion on transmission construction between 2023 and 2026, potentially helping boost demand for MYR Group’s T&D segment.

MYR Group Investor Presentation

Past 2026, there’s more demand growth potential.

According to the DOE in 2023, U.S. transmission systems need to grow significantly by around 60% by 2030 and may need to triple by 2050 to meet clean electricity demands.

If electricity consumption exceeds estimates, I would not be surprised if U.S. transmission systems need to grow even higher than 60% by 2030 as well.

In addition to private sector demand, there’s government support in helping improve and expand the grid. In particular, a powerful tailwind for demand for MYR Group’s T&D segment is the $1.2 trillion Infrastructure Investment and Jobs Act (“IIJA”) that includes $73 billion for the electric grid and energy infrastructure. According to MYR Group, combined federal spending planned for energy over the next 5 to 10 years is over $300 billion between the IIJA and the Inflation Reduction Act.

Likewise, MYR Group’s C&I segment also benefits from the Infrastructure Investment and Jobs Act, helping potentially increase demand for the segment.

Risks

MYR Group wins substantial business from competitive bidding processes. As a result, its margins could narrow if competition increases.

Weak economic conditions could cause utilities and other customers to postpone some capital programs which might decrease demand for MYR Group.

MYR Group could make a bad acquisition.

If demand weakens for MYR Group, its financials could underperform.

My Take

In terms of expectations as of March 28, analysts expect MYR Group’s earnings per share to continue to increase in the future from the $5.40 per share it earned in 2023.

Specifically, analysts on average expect MYR Group’s EPS to rise to $6.44 in 2024, $7.97 in 2025, and $10.75 in 2026, giving the stock a forward PE ratio of 27.23 for 2024, 21.98 for 2025, and 16.30 for 2026.

Seeking Alpha

In terms of its valuation, MYR Group has a 5 year average forward PE ratio of 18.53 while the sector median for forward PE ratio is 19.03.

From the 5 year average forward PE perspective, MYR Group’s valuation doesn’t become attractive until 2026.

Furthermore, I don’t think the company deserves a valuation of over 20 in terms of forward PE ratio in a normal growth environment given MYR Group has to competitively bid for a substantial percentage of its projects and the company works with relatively low profit margins.

With that said, it’s my view that MYR Group has substantial demand tailwinds that could last multiple years that will help the company meet or exceed its 2025 and 2026 estimates. Given management has guided for softer top line revenue growth in 2024, I am more cautious about 2024, but I think there’s a decent chance the company will still meet EPS estimates for the year.

In terms of demand tailwinds, I think there’s enough visibility and growth potential in the medium to long term for MYR Group to trade for 19x 2026 EPS estimates, so I have a price target of $204.25 per share. I think the stock could achieve that price in a year or two as demand continues to strengthen given the company’s tailwinds.

As such, I rate MYR Group a ‘Buy’ and I would own it in a diversified portfolio that includes the Magnificent Seven. With that said, I don’t think MYR Group is an ‘Overweight’ as the company isn’t a dominant company with numerous competitive advantages.

For the future, I would follow earnings reports and see if MYR Group’s revenue, EBITDA, EPS, and backlog are growing.

Furthermore, I would follow electricity usage trends. If electricity consumption growth exceeds expectations by a substantial margin, I think there’s potential for even more demand for grid upgrades and maintenance.

Q2 2024 Earnings Call Transcript")