Dragon Claws

Investment Thesis

Modiv Industrial (NYSE:MDV) is a real estate investment trust that operates, acquires, and leases commercial real estate properties. It has recently reported a decent quarter and I believe it can maintain this performance in the future as a result of industry tailwinds and its continued focus on acquisitions.

About MDV

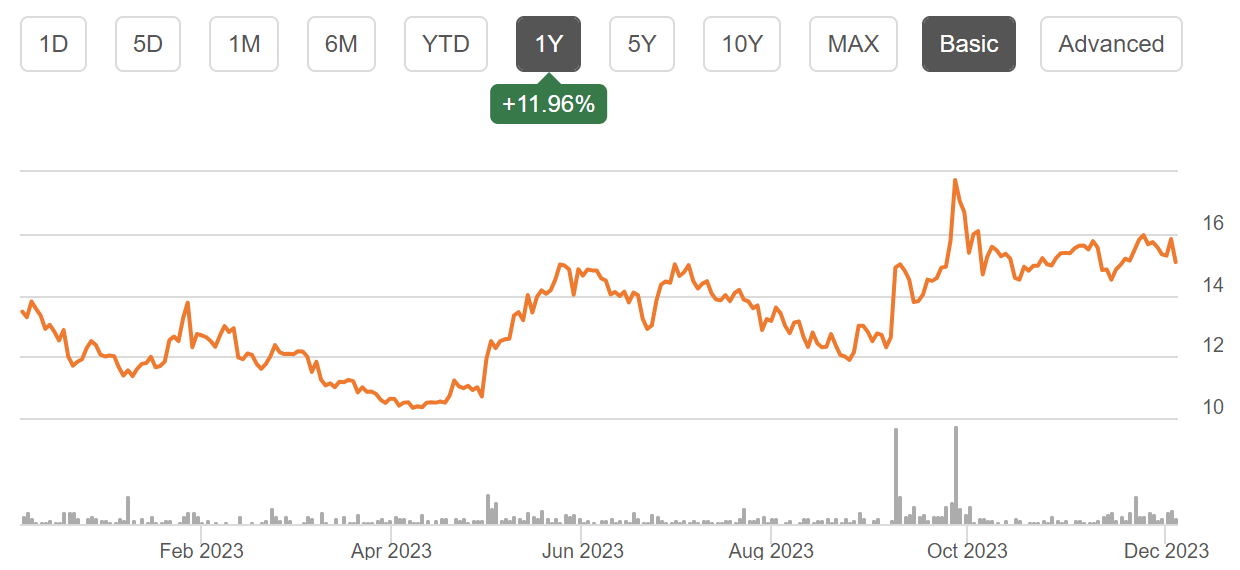

Share Price History of MDV (Seeking Alpha)

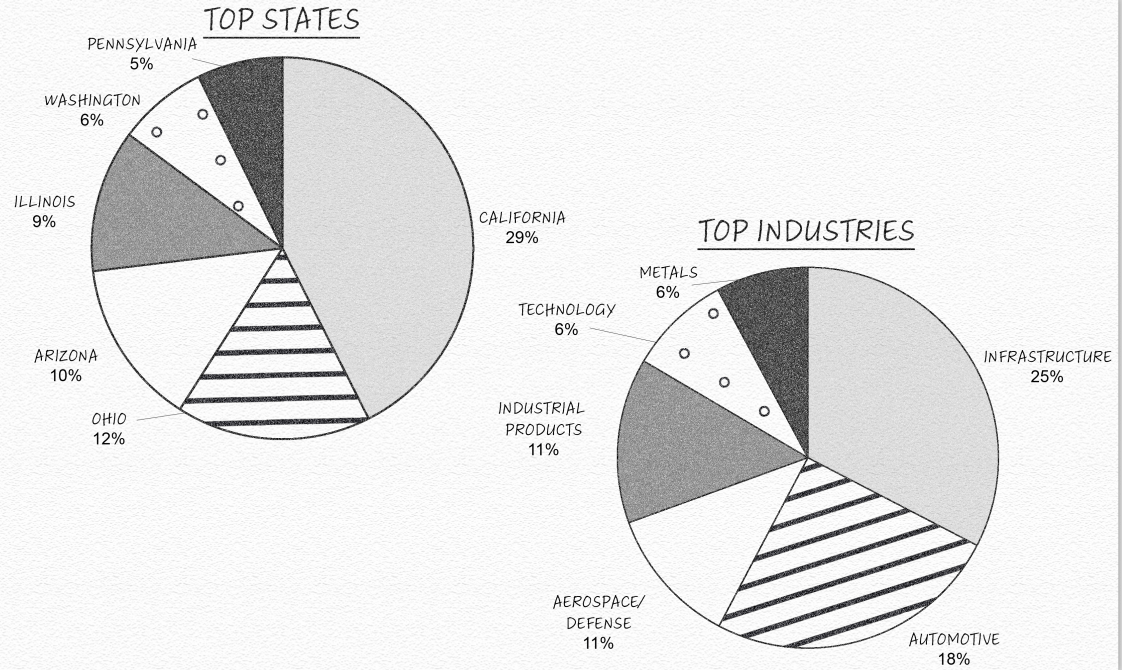

MDV is a real estate investment trust which has been internally managed since 2019. The company mainly deals in owning, managing, acquiring, and leasing commercial real estate in major states such as California, Arizona, Ohio, Washington, and Illinois. Its main objective is to build portfolio of income-producing commercial real estate investments in industrial manufacturing sites around the US, with a focus on corporate credit, geographical location, industry, and length of lease. The company has returned 19.59% (Price return:11.96% & dividend yield:7.63% compared to current share price) to its investors in the last one year. The company’s investment in land represents 22.7% of its total investments in real estate property while investment in Buildings is 72.1% of MDV’s total investments in real estate property. The remaining 5.2% of the company’s total investments in real estate property comprises equipment & tenant origination. It has leased its space to 30 distinct commercial tenants operating in 17 different sectors. MDV’s major tenants include Lindsay, Trophy of Carson, Valtir, AvAir, Cummins, Northrop Grumman, Taylor Farms Food, Fujifilm Dimatix, and Costco Wholesale. Its portfolio includes industries such as Infrastructure, Automotive, Industrial Products, Technology, Aerospace/Defense, and Infrastructure.

Portfolio by Region and Industry (Investor Presentation: Slide No: 10)

Financials

The real estate industry experienced a downturn due to rising interest rates, leading to lower demand for properties. However, the scenarios for industrial manufacturing properties are contradictory. The trends in this sector have remained positive for longer time due to COVID-19 Pandemic and geopolitical issues which have increased the prominence of onshore manufacturing in the U.S. The need to ensure the supply chain has significantly boosted demand for manufacturing spaces. At year’s end in 2022, the market for 3.8 billion square feet of manufacturing space had a record-low 3.4% availability rate following an annual absorption of 53.8 million square feet, which was the highest since 2016. As per the National Association for Industrial and Office Properties, It is predicted that absorption will total around 205 million square feet for the full year 2024 and 111 million square feet for the first half of 2025. I believe these tailwinds present great opportunities for companies operating in the industrial real estate sector as they can enhance the demand for industrial real estate and occupancy rate. As per my analysis, MDV is strongly and strategically positioned to cater to the growing demand as it is continuously focused on acquiring properties targeting the top-performing industries in geographically well-positioned states. Recently, in the third quarter, it acquired two industrial properties, and observing its current revenue growth, continued expansion of the portfolio, and healthy cash flows, I believe it can make the most of this opportunity and acquire more industrial properties in the Infrastructure, Automotive, and Defense sector which can potentially enhance its profitability in the future. In addition, as the company is a microcap, its revenue is significantly boosted by each acquisition, unlike large-cap REITs that must purchase billions of dollars’ worth of real estate annually to get the same result. It also has one of the longest-duration portfolios, with a weighted average lease term of more than 14 years which provides a reduced vacancy risk and more stability which I think makes it a competitive player in the real estate market.

The company has reported its quarterly results. It reported a revenue of $12.50 million, up 21.32% compared to $10.30 million in Q3FY22. The 12 industrial manufacturing acquisitions it executed in the first nine months of 2023 and the 14 noncore property disposals in August of the same year had a significant influence on this rise in revenue. The company has managed to exceed the market’s revenue consensus by $0.46 million or 3.68%. MDV has reported an AFFO of $3.7 million which is a 19% growth compared to $3.1 million in same period of the previous year. It reported a net loss of $6.45 million, compared to net income of $3.0 million in the year-ago quarter. This refuse was mainly caused due to a $7.80 million one-time catch-up adjustment for non-cash stock compensation expenses. It reported a diluted net loss per share of $0.99. MDV reported $5.64 million in liquidity and debt comprised of $250 million of outstanding borrowings on its $400 million credit facility and $34 million in mortgages. The company has net debt of $287.6 million with a net debt/adjusted EBITDA ratio of 6.7x (a slight decrease compared to 6.8x in Q3FY22).

The company performed well in the third quarter and managed to accomplish healthy revenue growth. It is observed that the firm is highly focused on acquisitions of properties in top-performing industries, which has significantly helped it to grow. I believe the company can maintain its growth levels in the coming quarters as a result of robust and continued demand for manufacturing space and its strong liquidity positioning as well as attractive portfolio dynamics which can help it to align with its plans to enlarge in the industrial space market and accomplish long-term growth. The company has 9-month reported an FFO per share of $1.03 and with the help of a new acquisition, I think it’s safer to say it can reach an FFO per share of $1.15 in FY2023. The company is continuously disposing of assets that do not synergize with MDV’s asset portfolio. After considering the addition of the assets that fit the long-term vision of the company and solid demand for manufacturing spaces, I think we can safely assume that MDV’s FFO per share can exceed FY2023’s FFO per share. Therefore, I believe FY2024’s FFO per share might be in the range of $1.65 to $1.78. To keep my estimates conservative, I am taking a mean of my forecasted range which gives the FFO per share of $1.72.

Dividend Yield

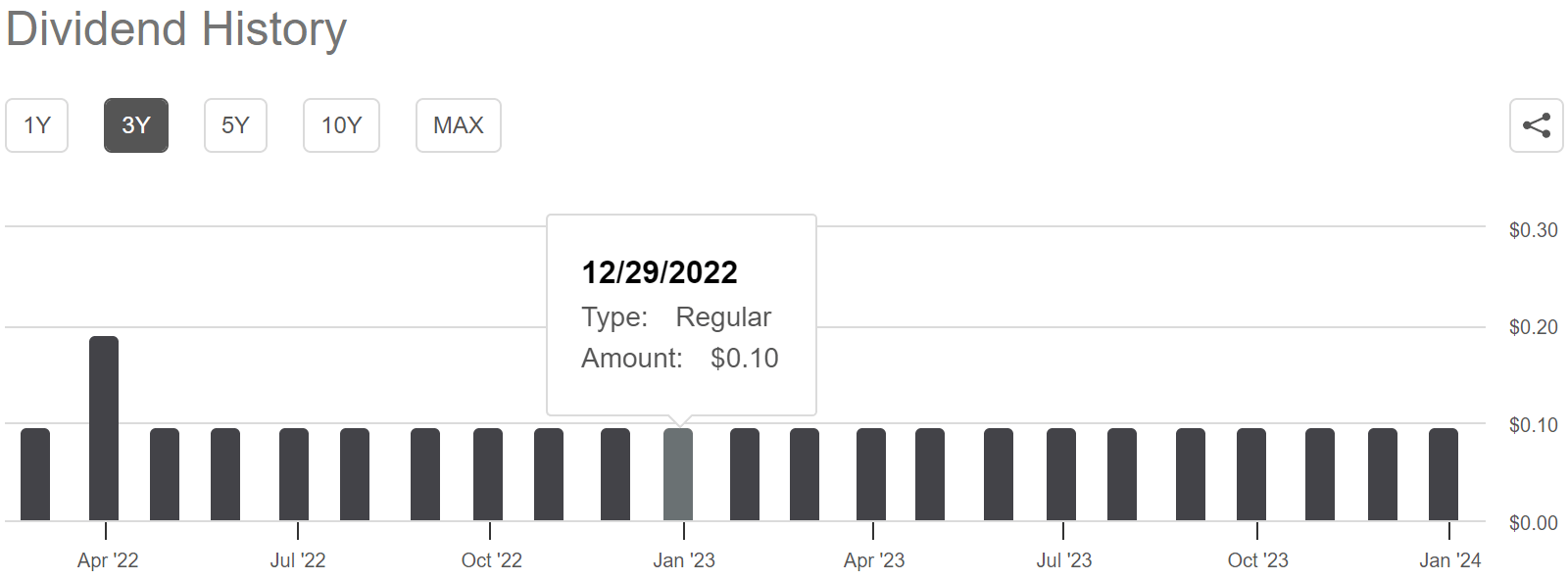

Dividend Payment History of MDV (Seeking Alpha)

The company has been consistently paying monthly dividends since the previous year which signals its significant growth. In FY2023, the company paid monthly cash dividends of $0.09583 each month, which makes the annual dividend $1.14996, representing a dividend yield of 7.63% compared to the current share price. The company has big companies such as Cummins, Northrop Grumman, Taylor Farms Food, Fujifilm Dimatix, and Costco Wholesale as its tenants which provides safety for the dividend. Even though this REIT is small, it still has high level of diversification throughout its portfolio. However, defaulting of any top tenants can put the dividend payment at risk as top six tenants comprise 43% of the company’s rental income. Looking at the top tenants and diversified portfolio, I think the company’s dividend payment is safe in the long term. The company has $5.6 million in cash & cash equivalents and $11.2 million in tenant receivables, which supports the consistent dividend payment in the long term. MDV’s dividend yield of 7.63% is significantly higher compared to the sector median dividend yield of 4.86%. This appealing yield makes the company an attractive stock, especially for risk-averse and retired investors who are seeking passive income along with capital appreciation.

What is the Main Risk Faced by MDV?

Dependency on Top Six Clients:

The company earns 43% of its total rental income from Trophy of Carson (12%), Lindsay (11%), Costco Wholesale (7%), 3M (6%), and AvAir (7%). If any of these clients defaults in the coming period it can significantly affect the company’s rental income and dividend payment capacity of the company. Another effect of the defaulting of any of these clients is it can hinder the company’s ability to repay the existing loan and borrow loans for acquisitions of new properties to make the portfolio diversified and synergized.

Interest Rate:

Before investing in dividend-paying REIT, the investors differentiate the dividend yield with the current interest rate in the market. Currently, interest rates in the market are rising to counter the rising inflation in the market. If the interest rates continue to enhance in the coming period, it can pull away the investors of REIT as they can earn stable and less risky income from other asset classes appreciate government bonds. The rising interest rate can also enhance the company’s financing cost and reduce the company’s dividend distribution ability.

Refinancing:

The company faces the risk associated with refinancing. A significant rise in inflation levels has fueled the rise in the interest rates which has ultimately increased the cost of financing for the company. If the interest rates surge, it can negatively affect the company’s operations due to high finance costs and may contract its profit margins. The increased interest rates can also negatively impact the asset valuation which can advance guide to a reduction in net income.

Valuation

The company has reported strong revenue growth and I believe it can maintain this performance in the future as a result of industry tailwinds and its continued focus on acquisitions which can help it to enhance its lease income and enlarge its profit margins. Taking into account everything mentioned above, I am projecting FFO per share of $1.72 for FY2024, resulting in forward P/FFO ratio of 8.57x. We can safely say that MDV is undervalued after comparing its forward P/FFO ratio of 8.57x with sector median of 12.74x. I believe the company might grow in the coming quarters as a result of positive demand in the industry and its alignment with its expansion of portfolio which can push MDV to trade near its sector median. However, high interest rates can enhance the financial cost and hinder the company’s ability to acquire new property to diversify & synergize portfolio of the company which can force MDV to trade below its sector median. After considering the headwind of high interest rates, I think am predicting that the company might trade at a lower P/FFO ratio than its sector median. Therefore, I assess the company might trade at a P/FFO ratio of 10.5x in FY2024. If we multiply 10.5x (estimated P/FFO) with $1.72 (estimated P/FFO) we will get the target price of $18.06, which is a 22.5% upside compared to the current share price of $14.74.

Conclusion

The company is mainly focused on acquiring industrial manufacturing properties, targeting the top-performing industries. It has reported healthy growth in revenues and I believe it can maintain its upside in the future as a result of robust demand for industrial space in the U.S. and its continued focus on strategic acquisitions which can enhance its revenues and profitability in the future and also help it to maintain its high dividend yield. MDV’s tenant list and solid dividend yield in the last two years supports consistent and safe dividend payment in the future. However, the company is exposed to risk of rising interest rates which can contract its profit margins. The stock is currently undervalued and investors can expect decent 30.13% total return (price return: 22.5% and dividend yield: 7.63%) from the present share price levels as a result of its industry tailwinds and its plans for strategic acquisitions. Considering all the factors, I assign a buy rating to MDV.

Q2 2024 Earnings Call Transcript")