Erdark/E+ via Getty Images

Mobile-Health Network Solutions Aims For U.S. IPO

Mobile-Health Network Solutions (MNDR) has filed to raise $10.125 million in an IPO of its Class A ordinary shares, according to an SEC F-1 registration statement.

Mobile-Health provides a telehealth platform and related services to healthcare system participants in Singapore.

Given the numerous risks involved, the firm’s mediocre growth rate from a small revenue base, recent swing to operating loss and cash burn and very high valuation assumptions, my outlook on the Mobile-Health Network Solutions IPO is to Sell (Avoid).

What Does Mobile-health Do?

Singapore-based Mobile-Health Network Solutions was founded to develop a mobile and website-enabled telehealth platform to facilitate patient-provider interactions via teleconference in Singapore.

Management is led by co-founder, co-CEO Siaw Tung Yeng, M.D., who has been with the firm since its inception in 2016 and was previously chief information officer and regional medical director of Healthway Medical Group and has also been a clinical lecturer for the Yong Loo Lin School of Medicine, National University of Singapore.

The company’s primary software and service offerings include the following:

-

Website

-

Mobile app

-

Electronics medical certificates

-

Medication delivery

-

In-person clinic

-

Corporate healthcare and wellness services

-

Other services.

As of June 30, 2023, Mobile-Health Network Solutions has booked total fair market value investment of $14.5 million from investors.

The firm seeks to integrate its platform into the operations of healthcare providers, physicians and other healthcare professionals in Singapore and ultimately beyond.

MNDR also makes its mobile app available to patients. The use of its system grew strongly through the COVID-19 pandemic era.

Selling, G&A expenses as a percentage of total revenue have risen sharply as revenues have increased somewhat, as the figures below indicate:

|

Selling, G&A |

Expenses vs. Revenue |

|

Period |

Percentage |

|

FYE June 30, 2023 |

24.1% |

|

FYE June 30, 2022 |

8.8% |

(Source – SEC.)

The Selling, G&A efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Selling, G&A expense, was 0.5x in the most recent reporting period. (Source – SEC.)

MNDR’s most recent calculation was negative (29%) as of June 30, 2023, so the firm has performed poorly in this regard, per the table below:

|

Rule of 40 |

Calculation |

|

Recent Rev. Growth % |

13% |

|

Operating Margin |

-42% |

|

Total |

-29% |

(Source – SEC.)

What Is Mobile-health’s Market?

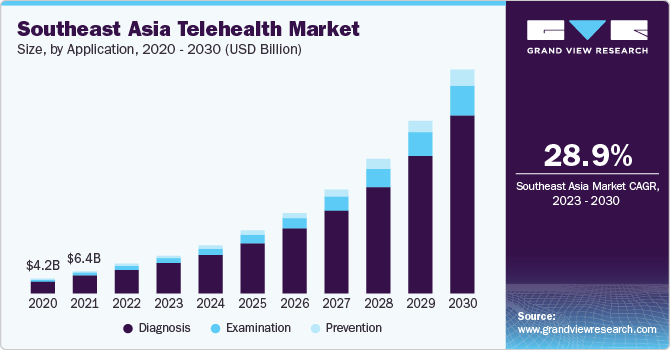

According to a 2023 market research report by Grand View Research, the market for telehealth services in Southeast Asia was an estimated $8.5 billion in 2022 and is forecast to reach $64.8 billion by 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of a very high 28.9% from 2023 to 2030.

The main expected reasons for this expected growth are a growing penetration of smartphone and tablet usage and increasing awareness by consumers of the “importance of monitoring health and fitness to control the incidence of chronic ailments.”

Also, the chart below illustrates the historical and projected growth trajectory of the Southeast Asia Telehealth Market by service application from 2020 to 2030:

Grand View Research

Major competitive or other industry participants include the following:

-

HALODOC

-

HEYDOC INTERNATIONAL SDN. BHD.

-

Grab

-

MyDoc Pte. Ltd.

-

Doctor Anywhere Pte Ltd.

-

Teleme

-

GOOD DOCTOR TECHNOLOGY (SINGAPORE) PTE. LTD.

-

DoctorOnCall

-

Alodokter

-

ClicknCare.

Mobile-Health Network Solutions Recent Financial Results

The company’s recent financial results can be summarized as follows:

-

Growing top line revenue from a small base

-

Reduced gross profit and lower gross margin

-

A swing to operating loss and cash used in operations.

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

FYE June 30, 2023 |

$7,874,886 |

12.7% |

|

FYE June 30, 2022 |

$6,988,849 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

FYE June 30, 2023 |

$1,094,994 |

-43.4% |

|

FYE June 30, 2022 |

$1,935,106 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

% Variance vs. Prior |

|

FYE June 30, 2023 |

13.90% |

-49.8% |

|

FYE June 30, 2022 |

27.69% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

FYE June 30, 2023 |

$ (3,288,700) |

-41.8% |

|

FYE June 30, 2022 |

$193,662 |

2.8% |

|

Comprehensive Income (Loss) |

||

|

Period |

Comprehensive Income (Loss) |

Net Margin |

|

FYE June 30, 2023 |

$(2,817,098) |

-35.8% |

|

FYE June 30, 2022 |

$(21,736) |

-0.3% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

FYE June 30, 2023 |

$(2,248,626) |

|

|

FYE June 30, 2022 |

$975,656 |

|

(Source – SEC.)

As of June 30, 2023, Mobile-Health had $2.2 million in cash and $2.3 million in total liabilities.

Free cash flow during the twelve months ending June 30, 2023, was negative ($2.4 million).

Mobile-Health Network Solutions’ IPO Details

Mobile-Health intends to raise $10.125 million in gross proceeds from an IPO of its Class A ordinary shares, offering 2.25 million shares at a proposed midpoint price of $4.50 per share.

No existing shareholders have indicated an interest in purchasing shares at the IPO price.

The company is also registering for sale by existing shareholders approximately 3.1 million additional shares.

Should these shares be registered and sold within a short time frame, the effect on the stock price could be quite negative.

Assuming a successful IPO, the company’s enterprise value at IPO would approximate $165.5 million, excluding the effects of underwriter over-allotment options.

The float to outstanding shares ratio (excluding underwriter over-allotments) will be approximately 6.62%, making the stock a ‘low-float’ stock subject to the potential for increased volatility post-IPO.

Management says it will use the net proceeds from the IPO as follows:

approximately 20% for product development to expand the functionality and value of our core technology platform;

approximately 25% for development and expansion of business and operations;

approximately 30% for potential merger and acquisitions although we have no commitments with respect to any such acquisitions at this time; and

approximately 25% for general corporate purposes, including working capital, operating expenses and capital expenditures.

(Source – SEC.)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, leadership said the company is not presently subject to material legal proceedings.

The sole listed bookrunner of the IPO is Network 1 Financial Securities.

Valuation Metrics For Mobile-Health

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure (TTM) |

Amount |

|

Market Capitalization at IPO |

$153,000,000 |

|

Enterprise Value |

$165,512,211 |

|

Price / Sales |

19.43 |

|

EV / Revenue |

21.02 |

|

EV / EBITDA |

151.15 |

|

Earnings Per Share |

-$0.10 |

|

Operating Margin |

13.90% |

|

Net Margin |

-41.76% |

|

Float To Outstanding Shares Ratio |

6.62% |

|

Proposed IPO Midpoint Price per Share |

$4.50 |

|

Capital Expenditures |

-$186,001 |

|

Free Cash Flow Yield Per Share |

-0.12% |

|

Debt / EBITDA Multiple |

11.43 |

|

CapEx Ratio |

0.00 |

|

Revenue Growth Rate |

12.68% |

(Source – SEC.)

Mobile-Health Has Turned To Operating Loss On Reduced Efficiency

MNDR is seeking U.S. public capital market investment to fund its operational and expansion capital needs.

The company’s financials have generated higher top line revenue from a small base, lower gross profit and gross margin and most recently an operating loss and cash used in operations.

Free cash flow for the twelve months ending June 30, 2023, was negative ($2.4 million).

Selling, G&A expenses as a percentage of total revenue have increased substantially as revenue has grown from a low base; its Selling, G&A efficiency multiple was .05x in the most recent fiscal year.

The firm currently plans to pay no dividends and to keep most or all of future earnings, if any, for its business operations and expansion efforts.

MNDR’s recent capital spending history indicates it has continued to spend on capital expenditures despite negative operating cash flow.

The company’s Rule of 40 results have been highly negative, with moderate revenue growth dragged down by high operating losses contributing to a negative figure for this metric.

The market opportunity for providing telehealth services, which the company sells into, is moderately large but expected to grow at a high rate of growth in the coming years and providers and patients alike adopt more efficient modes of service delivery.

MNDR is also choosing to be considered an ‘emerging growth company’ and is a “foreign private issuer,” both of which mean that management can choose to disclose substantially less information to shareholders.

Many such company stocks have performed negatively after their IPO.

Risks to the company’s outlook as a public company include its small size and scope of operations within Singapore and lack of proven expertise in expanding to other markets.

Existing cash runway is less than one year’s free cash burn, so the firm will run out of money without a quick infusion of cash.

Management is seeking an Enterprise Value/Revenue multiple of approximately 21x on only modest topline revenue growth from a small base and on a swing to operating losses and cash burn.

Given the risks involved, its relatively slow growth rate from a small revenue base, swing to operating loss and cash burn and unreasonably high valuation expectations, my outlook on the IPO is to Sell (Avoid).

Expected IPO Pricing Date: To be announced.

Q2 2024 Earnings Call Transcript")