Shares of Palantir Technologies (PLTR -0.53%) jumped an impressive 30% on Feb. 6 after the company released solid results for the fourth quarter of 2023 on the previous day, driven by the growing demand for its artificial intelligence (AI) software solutions.

However, Palantir was not the only company that saw its shares rise following the quarterly report. Its strong results rubbed off positively on pure-play enterprise AI software provider C3.ai (AI 6.07%), with the latter’s shares gaining almost 8% on the same day. C3.ai’s stock may have jumped following Palantir’s results because of the robust demand for AI software.

Palantir struck an impressive 103 deals last quarter that were each worth more than $1 million — a twofold jump over the year-ago period — pointing out that adoption of its Artificial Intelligence Platform (AIP) “is driving both new customer conversions and existing customer expansions.”

What’s more, Palantir’s commercial customer count jumped 44% year over year last quarter, leading to a 32% increase in commercial revenue to $284 million. There is no doubt that these metrics from Palantir indeed paint a healthy picture of the AI software market. But can C3.ai capitalize on this opportunity and deliver healthy gains like its bigger competitor? Let’s find out.

C3.ai is no Palantir, but it has plenty room to grow

Palantir made its name by building and deploying AI software platforms for use by intelligence agencies in the U.S. to help them with counter-terrorism operations.

And now, the company’s commercial business has gained solid traction. The hundreds of bootcamps that Palantir organized last year helped commercial customers understand how to integrate AI into their operations, allowing the company to land new customer accounts and gain more business from existing ones.

C3.ai, on the other hand, also provides enterprises with a software platform with which they can build and deploy AI applications. So, C3.ai and Palantir are targeting a similar market, but the latter’s experience of providing AI solutions to government agencies for a long time seems to have given it a head-start in this market.

This is evident from the fact that Palantir’s Q4 commercial revenue of $284 million is equal to the total revenue that C3.ai has generated in the past 12 months. Moreover, Palantir finished 2023 with revenue of $2.23 billion, while C3.ai’s revenue in the current fiscal year is expected to land at $306 million.

So, C3.ai has a long way to go before it can get close to Palantir, which was ranked the top provider of AI software platforms in 2021 by market research firm IDC. However, the good news for investors is the huge addressable opportunity in the enterprise AI market, which is expected to clock annual growth of 52% through 2029 and generate annual revenue of $204 billion at the end of the forecast period, according to Mordor Intelligence.

As such, there is a lot of room for C3.ai to grow in this market in the long run. The company’s growth is expected to accelerate in the coming years thanks to a switch in its business model.

Potential acceleration in growth ahead

Shares of C3.ai are down 44% since hitting a 52-week high in mid-June last year. That’s because the company’s growth has slowed down in recent quarters due to a change in its business model. C3.ai switched to a pay-as-you-go business model around a year-and-a-half ago. It was earlier following a subscription-based model, which gave it revenue visibility since C3.ai was able to lock customers into long-term contracts.

However, the switch means that customers pay for C3.ai’s enterprise AI software offerings when they use them. The company made this move to make it easier for customers to sign up for its solutions, removing the need for protracted negotiations. However, C3.ai management did point out that the transition will initially compress its margins and flatten revenue growth.

This explains why C3.ai’s revenue in fiscal 2023 (which ended in April 2023) increased just 5.6% year over year to $267 million. The good part is that C3.ai is almost at the end of the second phase of the business model transition, during which it is witnessing an improvement in deal activity and customer spending. During the next phase, which is expected to begin in a couple of quarters, C3.ai is forecasting a significant jump in revenue growth as well as an improvement in its margin profile.

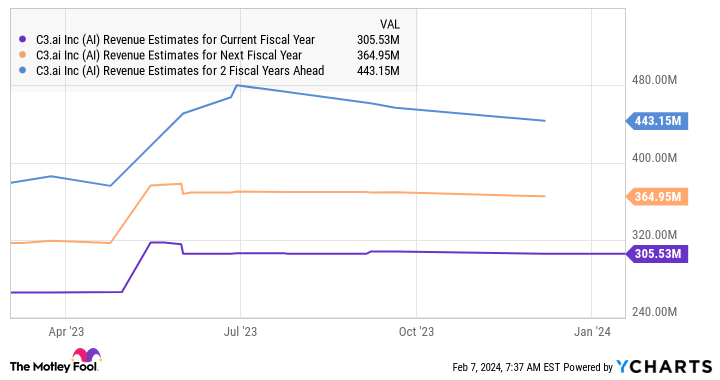

This explains why the company expects to finish fiscal 2024 with revenue of $295 million to $320 million. At the midpoint, that would translate into year-over-year growth of 15%. Even better, analysts anticipate an acceleration in its growth over the next couple of years.

AI Revenue Estimates for Current Fiscal Year data by YCharts

It is also worth noting that analysts expect C3.ai’s earnings to increase at a terrific annual rate of 50% for the next five years. Palantir, for comparison, is predicted to clock annual earnings growth of 85% for the next five years. However, Palantir stock’s 163% surge in the past year means that investors will have to pay a handsome valuation to buy it right now.

Palantir currently commands a price-to-sales ratio of 22.6, which is more than double C3.ai’s sales multiple of 10.5. It is also worth noting that Palantir’s top line is expected to grow 20% in 2024 and 2025, while the previous chart tells us that C3.ai’s revenue could also start increasing at a similar rate from its new fiscal year, which will begin in May 2024.

All this indicates that C3.ai could turn out to be a solid alternative for investors looking to buy an AI software stock right now, especially considering that Palantir’s red-hot surge has sent its valuation through the roof.

Q2 2024 Earnings Call Transcript")