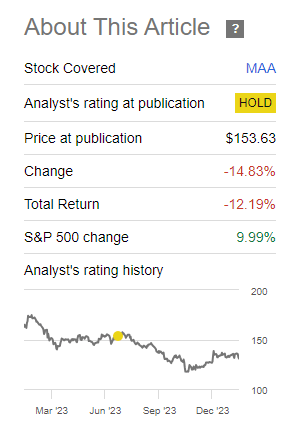

In the relatively recent past, we had suggested that Mid-America (NYSE:MAA) would be an attractive security at a slightly lower price point.

Seeking Alpha

Within that article, we specifically identified $140 as the price we would drool just a little bit. That was not too long back and the stock went significantly lower over that timeframe. It breached that $140 and hit a low of $115.56.

Seeking Alpha

We did not buy. We go over some of our latest thoughts on this and tell you why we hesitated and what we would look for today.

Company Performance

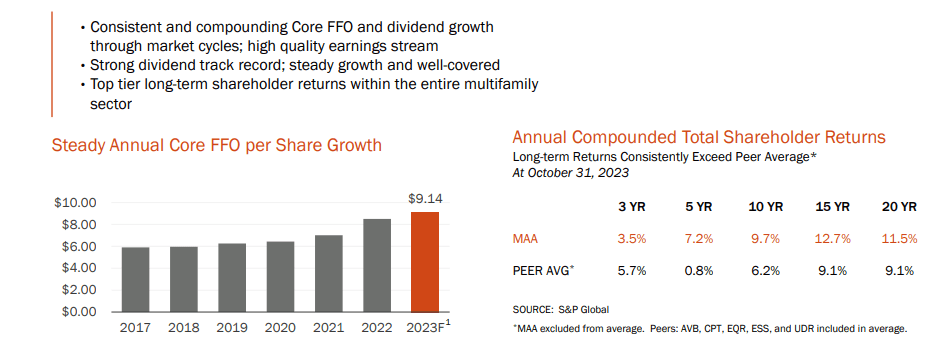

MAA has been a great steward for shareholder capital and you can see that by its investing choices over the last two decades.

MAA Q3-2023 Presentation

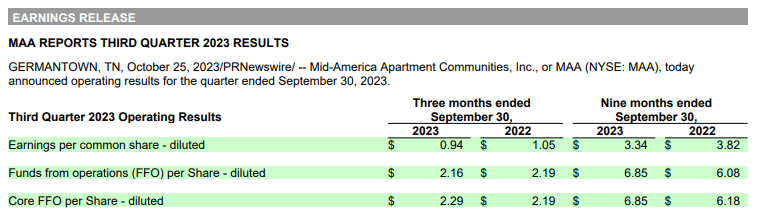

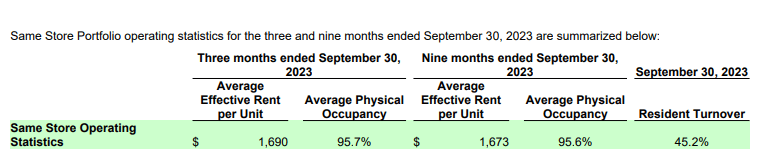

The latest quarter was no different and funds from operations (FFO) climbed by about 4.56% year over year to $2.29 per share.

MAA Q3-2023 Presentation

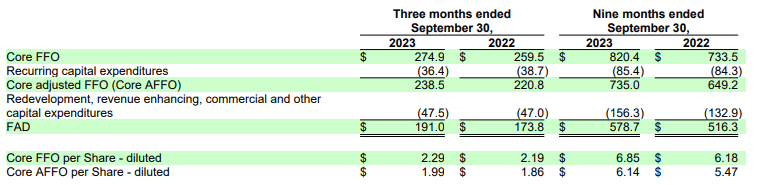

The adjusted FFO (AFFO) (which subtracts out recurring capital expenditures) also moved up at a similar clip.

MAA Q3-2023 Presentation

If you were looking for any major red flags in its occupancy or rent levels you did not get it in this quarter.

MAA Q3-2023 Presentation

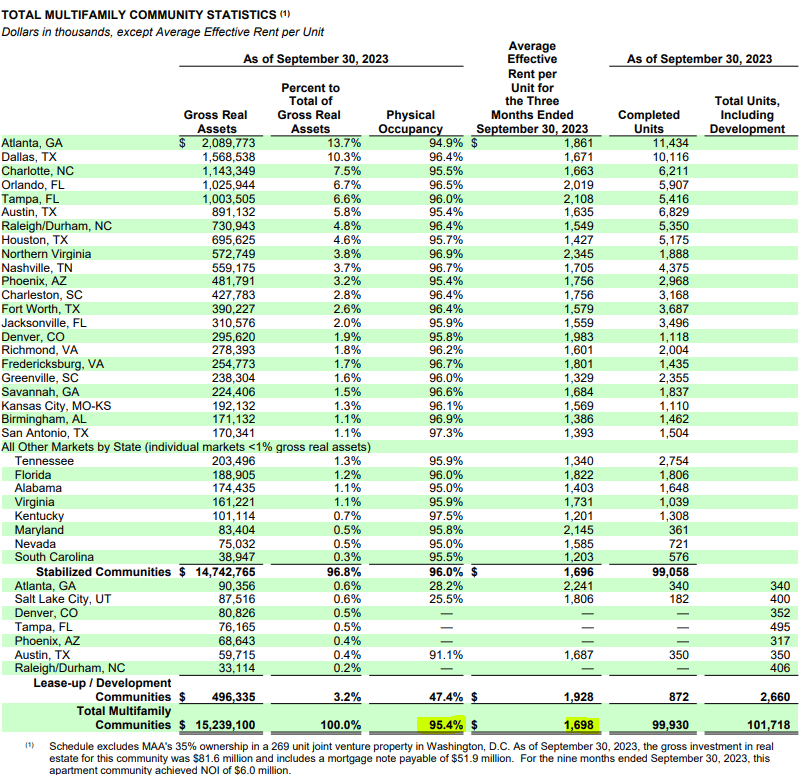

On an individual city level, you could see that there were no real soft spots.

MAA Q3-2023 Presentation

We actually went back and compared this to the last several quarters and there were no real weaknesses. So what’s the stopping point?

Supply

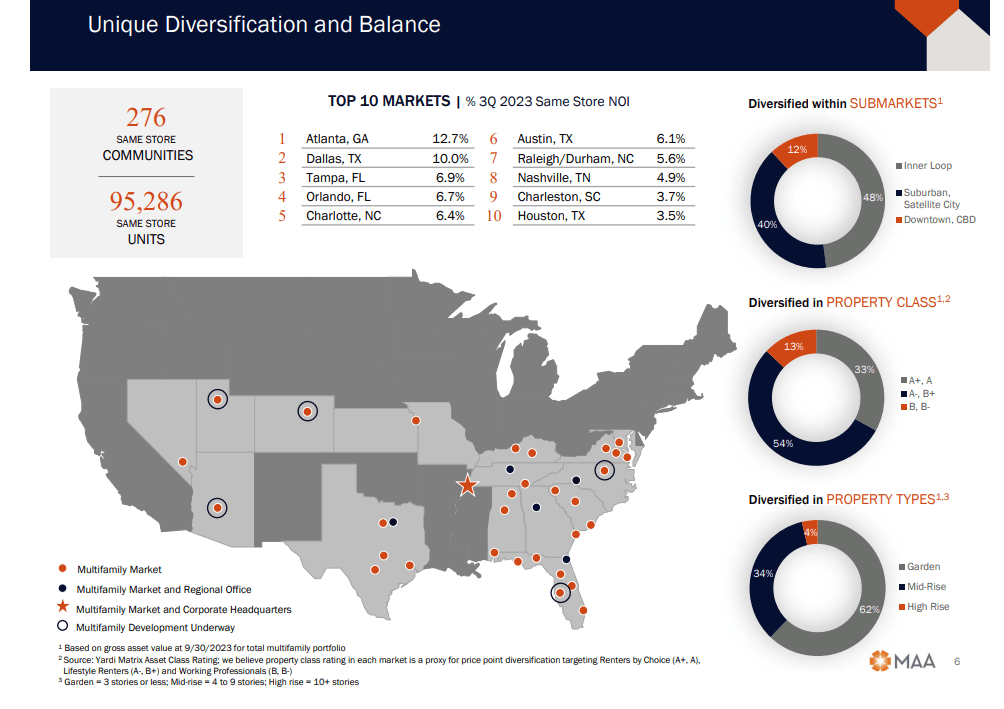

Well, there is one sort of soft spot and that is the sun-belt exposure. Below (and in the city breakdown above as well), we can see where MAA gets most of its money.

MAA Q3-2023 Presentation

While MAA has held its vacancy levels in check, the same really cannot be said for what is currently happening across those cities. We looked at all of those and the stories are surprisingly similar. We are going to next post some recent statistics on a few of those, but keep in mind this really applies across the board. First up is Dallas.

Overall vacancy for apartments built in the downtown Dallas area since 2019 is at 9.9%. In downtown Fort Worth, vacancies in the newest units are almost 17%, Partners Real Estate estimates.

Vacancy rates in the newest suburban D-FW rental units are less than 9%, according to the study. “Most of the properties in the suburbs delivered during the same time period have performed much more strongly,” the analysts said.

One factor could be the slow return to office in city centers following COVID’s work-at-home shift. About 60% of Dallas-area office employees are back in the workplace as of the latest estimates.

But higher apartment vacancies downtown probably have as much to do with construction.

There’s been ample demand for apartments in the urban cores of Dallas and Fort Worth, but even more supply,” said Jay Parsons, chief economist at Richardson-based RealPage. “Apartment vacancy in both was less than 5% early last year before it started climbing.”

There is a lot of regular supply coming on, but it gets worse for landlords. There is another stealth source of new supply coming from office conversions.

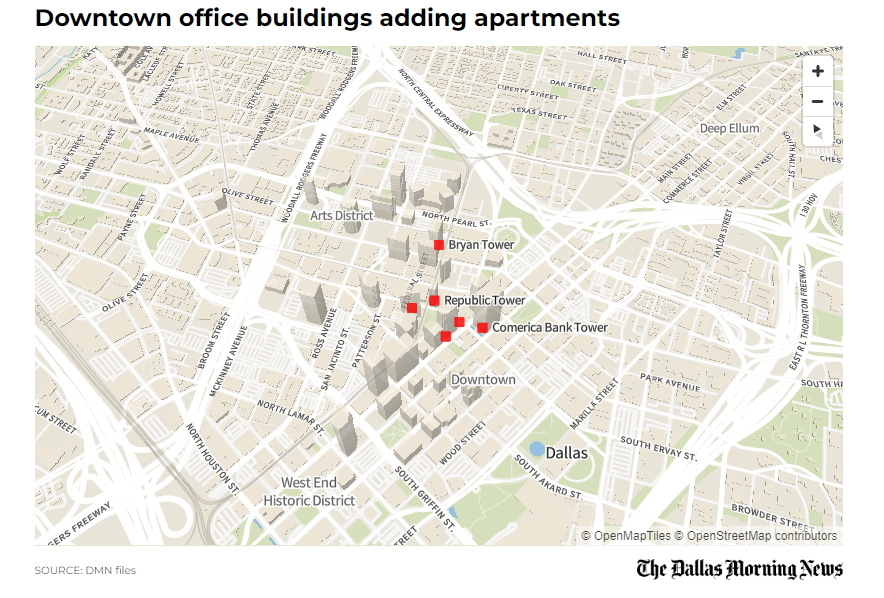

The 211 N. Ervay building is a bright spot on the Dallas skyline.

The last survivor of a generation of downtown offices that once sported colorful exteriors, the 65-year-old high-rise is covered in azure and aquamarine panels.

But the building’s flashy 1950s look is a big plus for new owner Kenny Wolfe.

I’m a midcentury modern fan,” said Wolfe, whose firm plans to convert the 187,000-square-foot tower into 238 rental units.

Dallas News

The Ervay Street office is one of a handful of downtown buildings being revamped into residential.

Source: Dallas News

That is a lot of new supply to absorb in a market with high vacancy rates. That holds true even when accounting for a low housing inventory and immigration trends. Nashville, Tennessee, is looking even worse.

Nashville has more than 16,000 vacant apartment units, and that figure could drastically increase in the next couple of years, given that another 18,000 units are in the pipeline, the Nashville Business Journal reported, citing data from CoStar.

The multifamily vacancy rate in Nashville is nearing 11 percent, which is considerably higher than the national average, said Michael Cobb, CoStar Group’s Nashville director of market analytics.

“Last year saw 7,200 units absorbed. Let’s couple that figure with the arrival of another 9,000 units this year and another 8,000 units in 2025. Even if [absorption] continues at this rate, we’re still not going to get anywhere near being full,” Cobb told the outlet.

Atlanta, Georgia might be the worst of three and is MAA’s largest exposure.

Yet the new supply pipeline currently includes more than 850 multifamily projects. Some of the projects in planning may fall out of the pipeline given the current state of Atlanta’s apartment performance, but even looking at only projects currently under construction, nearly 38,000 units will be added to Atlanta’s apartment stock in the coming years.

Most of the existing construction is concentrated in the Downtown and Midtown areas as well as the northern suburbs. When adding in planned projects, the pipeline expands to the south and east, especially along the I-75 and I-20 corridors.

There is some hope for a moderating pipeline, as the number of units being cancelled has steadily increased through the summer, but even if a small portion of the planned units come to fruition, Atlanta’s downcycle may be extended.

Atlanta apartment performance will regain its strength at some point, however as the national supply wave continues Atlanta remains at the eye of the storm. It may take years to absorb the new deliveries before demand and supply return to equilibrium.

Source: Radix

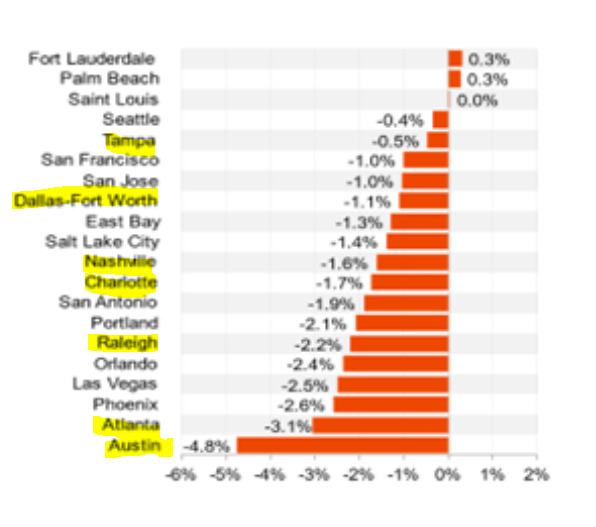

The year over year rent growth overall in some of these cities is now deep into negative territory.

Co-Star Group

These all are Q3-2023 numbers with labor markets on the strong side and a lot of supply still waiting in the wings. Over the next 12 months, we see more pain for these markets and if that is coupled with a highly probable recession, things might get dicey for even the relatively resilient MAA.

Verdict

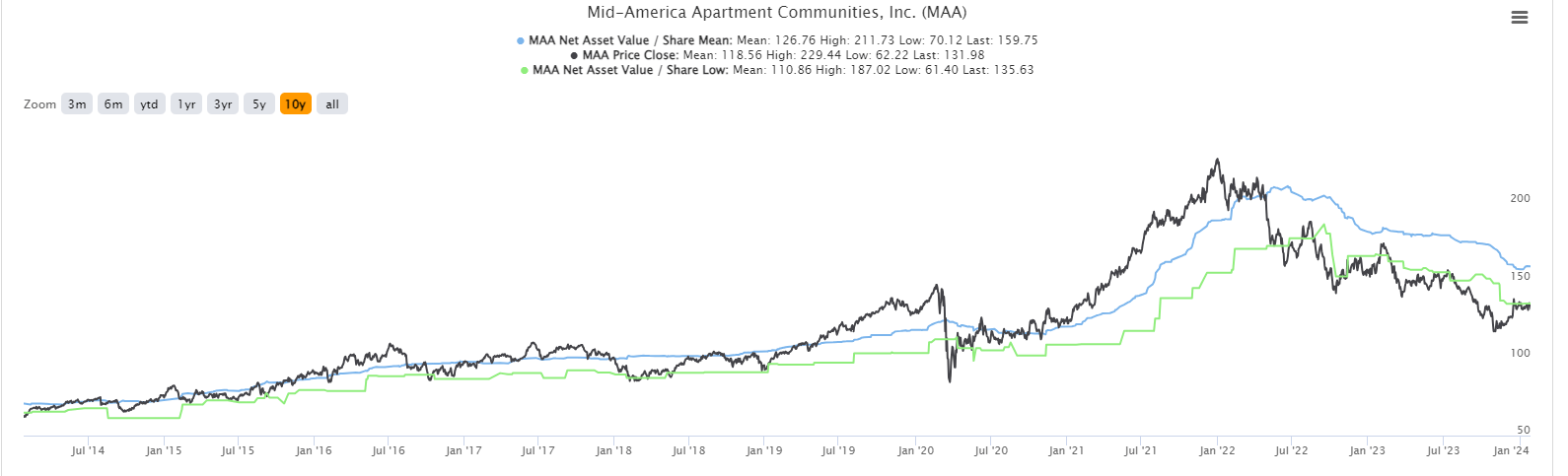

MAA’s superior balance sheet (one of the 8 REITs with an “A” rating) and exceptional management have done the job of navigating the first wave of supply. But challenges remain over the next 12-24 months. The mean analyst NAV estimate (blue line below) peaked a little over $200 and has been moving lower slowly.

TIKR

The lowest estimate on the street today is for $135.63, a number that we think is actually close to the real NAV. You can see that over the last 18 months, the stock price has generally been cheap relative to the estimated NAV, but that estimated NAV (and your margin of safety) has eroded. It is quite fascinating that this is the degree of NAV drop for one of the least leveraged apartment REITs out there. So far the FFO down revisions have been fairly modest.

Seeking Alpha

But we think there will be more pain in that area and we expect 2025 estimates to ultimately move well below $9.00 per share. This does not make MAA a bad choice for longer-term investors. It just means that there are risks here and those risks could really ramp up in a recession. As MAA approached its lows, we were tempted but there are also other REITs that we see with a wider margin of safety and fewer supply issues. We favored those instead. MAA remains an interesting long-term prospect and we might still end up buying it. The covered calls present even better choices for the risk-averse investor. But we remain on hold for now.

Mid-America Apartment Communities, Inc. PFD SER I (MAA.PR.I)

Shockingly as MAA has become cheaper, MAA.PI has been priced to even more ridiculous levels. This high-yielding preferred share has a call date in October 2026. Despite its large coupon of 8.5% the relatively near call date means that is for losers only. The yield to maturity is lower than the 3-year Treasury and by a good margin.

Q2 2024 Earnings Call Transcript")