Bloomberg/Bloomberg via Getty Images

Thesis Summary

MicroStrategy (NASDAQ:MSTR) has rallied over 50% in the last week, fueled by a significant move in Bitcoin and bold statements from Michael Saylor, who is going all-in on Bitcoin.

The company will double its efforts in the Bitcoin space, which could be a great move if, as I expect, the price keeps improving.

Nonetheless, the question is if this is the best vehicle to invest in Bitcoin. Given the large amount of shorting and the potential for more “Bitcoin development”, I have no doubt that this stock can trade at a premium. By my calculations, it already does.

At this level, I would simply advise holding the stock. If we get another Bitcoin sell-off, and this is amplified in MSTR, then that would certainly be an interesting point to add.

Latest Earnings

MSTR reported earnings last week, which sent the stock much higher, aided by a move higher in Bitcoin.

While the company beat on EPS, revenue came in below expectations. Most of the investor presentation, though, focused on the company’s BTC holdings and its strategy moving forward.

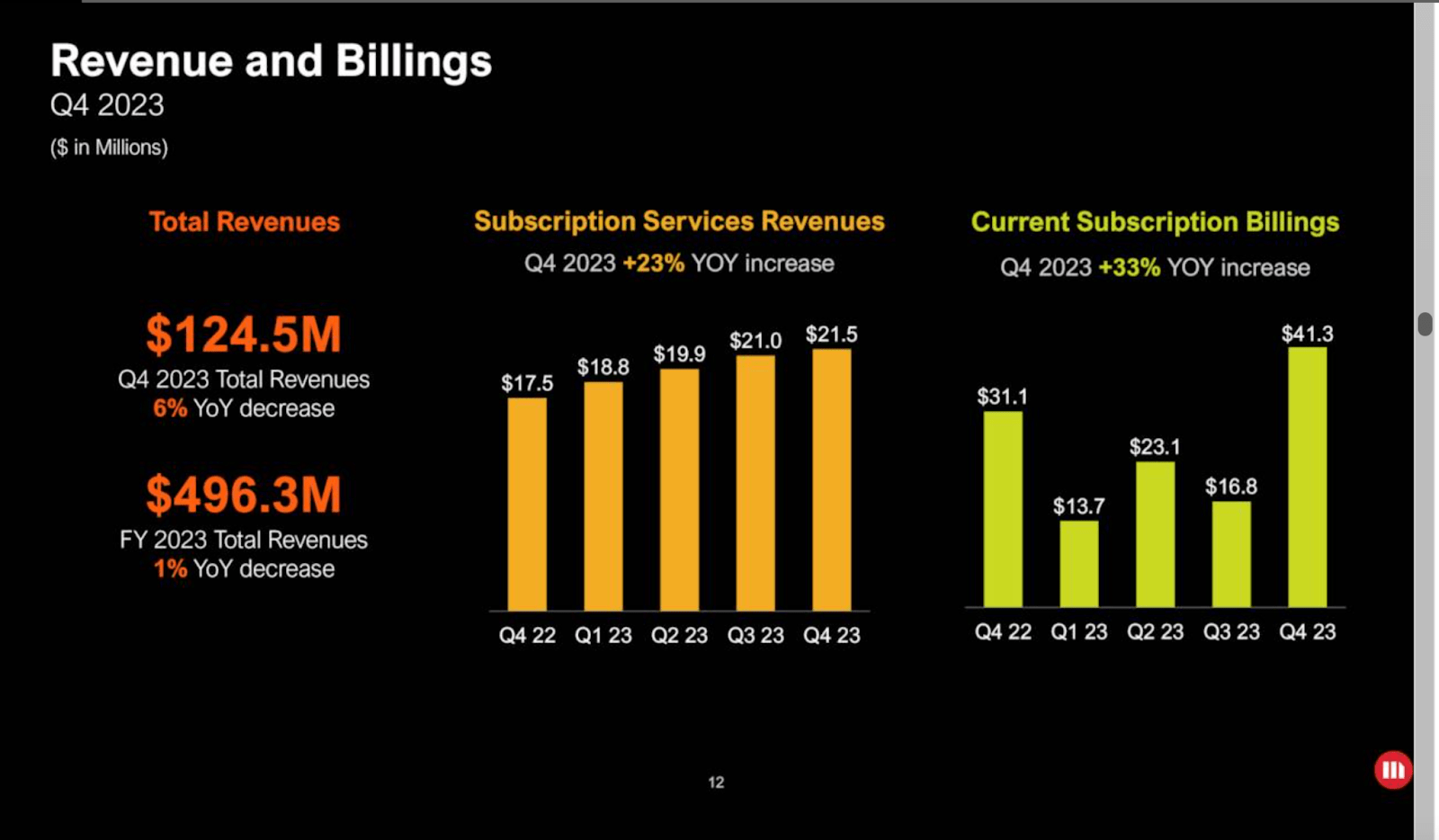

Revenue and Billing (Investor slides)

For the time being, though, the company still makes its revenues from its Business Intelligence solutions, which are actually still quite popular. Subscription services increased by 23% YoY, with billings up 33%.

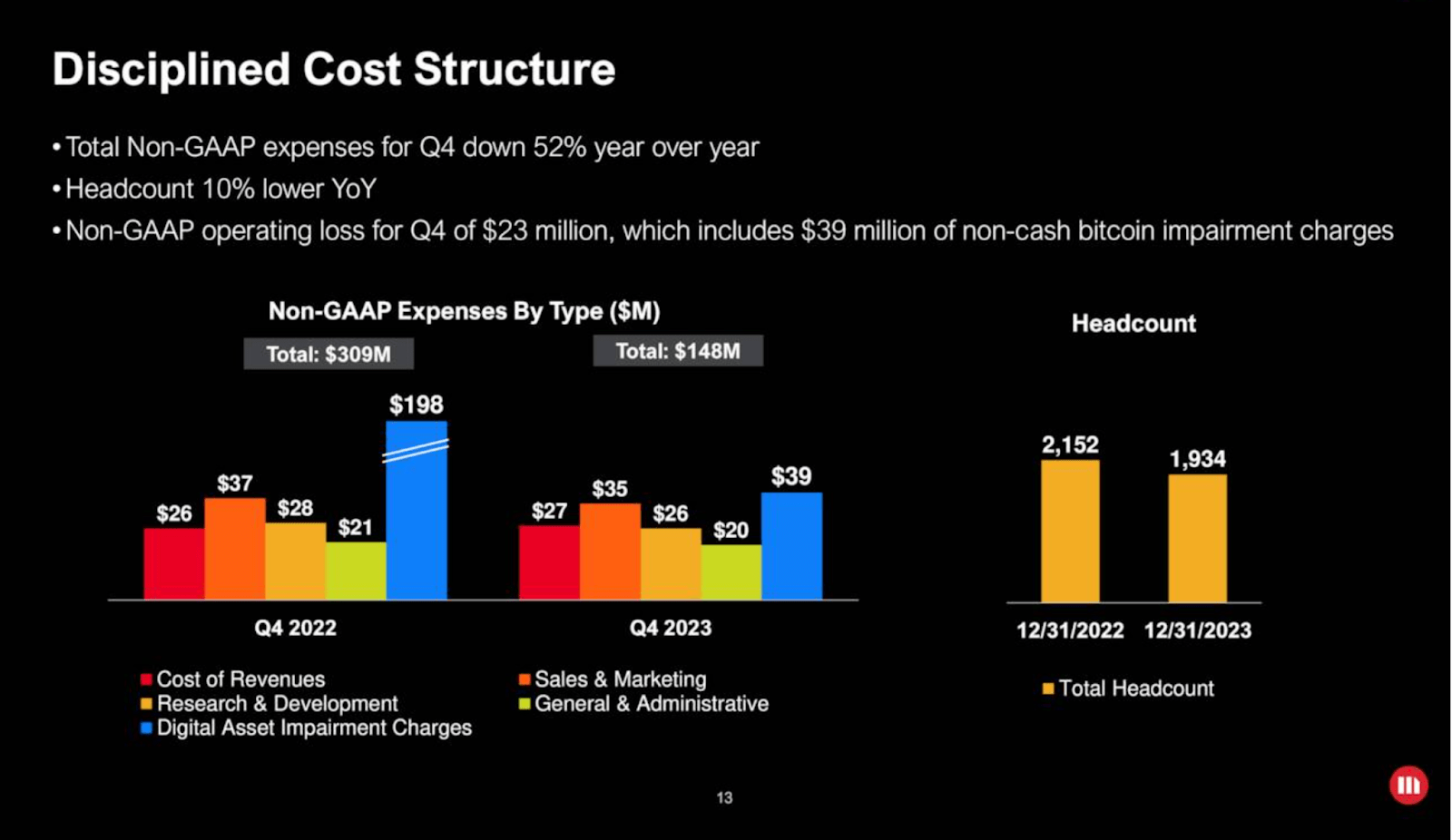

On another encouraging business note, the company has done well to significantly reduce their expenses in 2023.

Costs structure (Investor slides)

Of course, the biggest contributor to the “increased operational performance” was the large reduction in Digital Asset Impairment charges.”

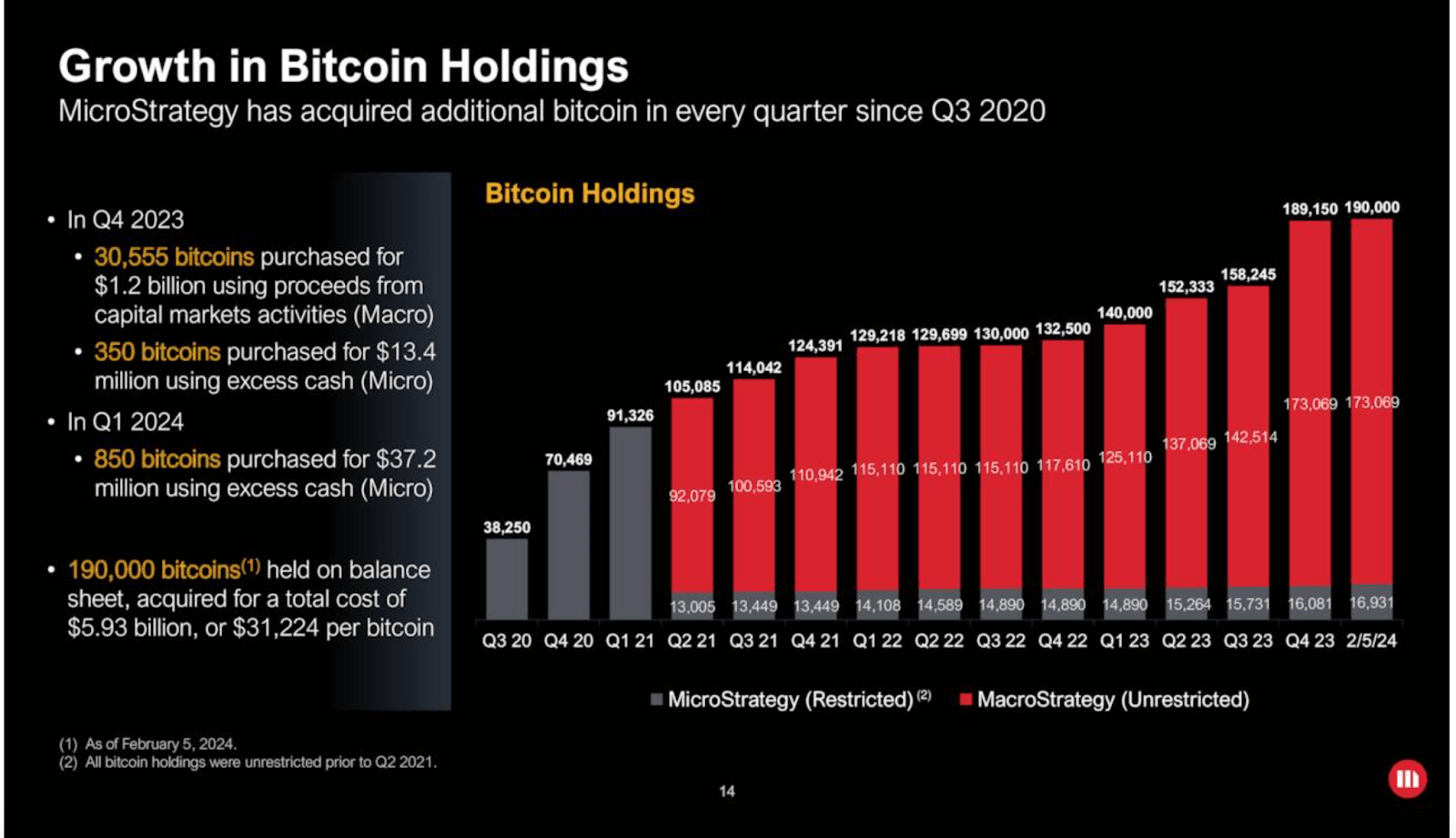

MSTR is the second-largest public holder of Bitcoin, right behind Greyscale (GBTC).

BTC Holdings (Investor slides)

The company has continued to add aggressively to their BTC holdings. Which now sits at 190,000.

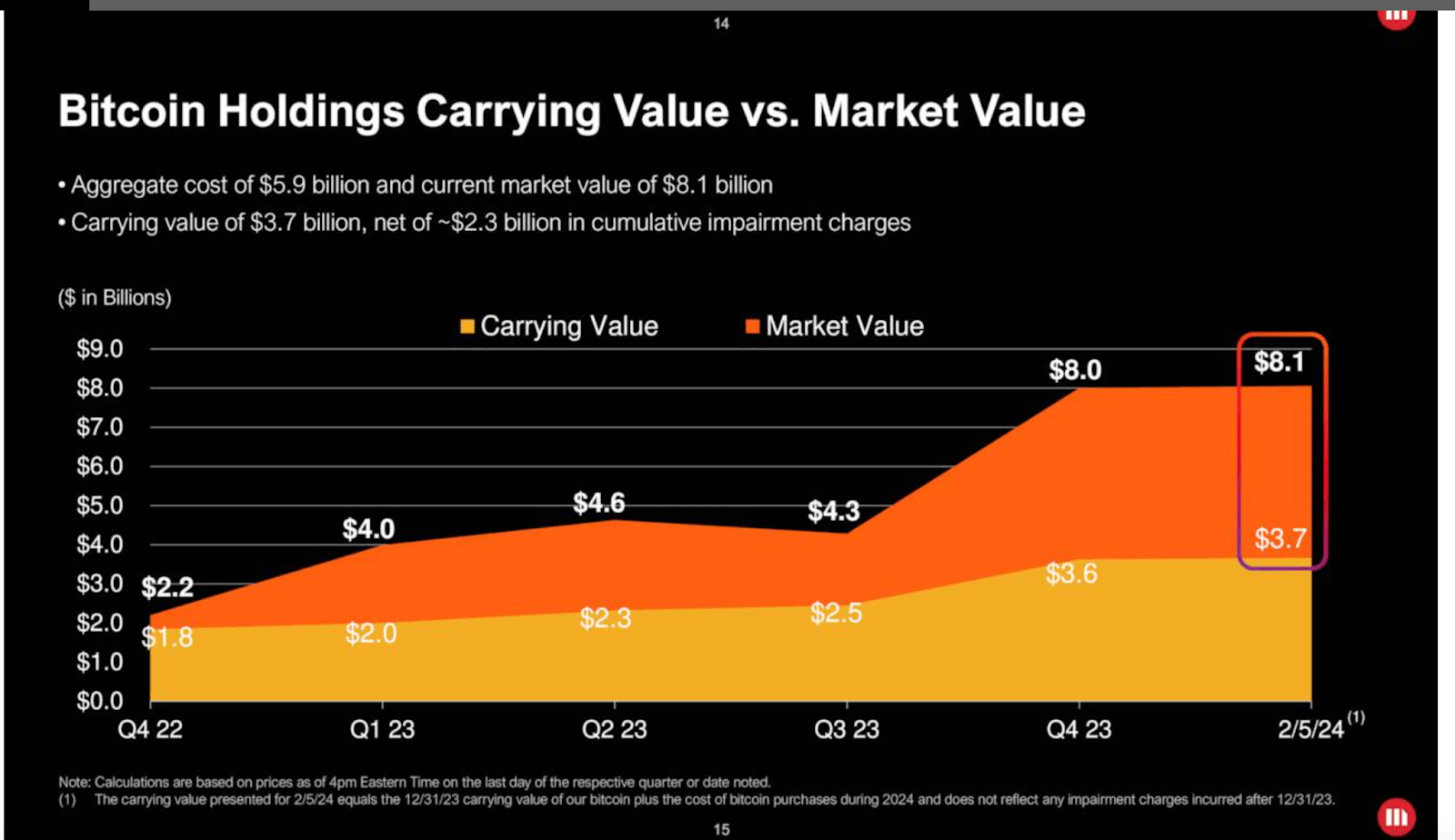

BTC value (Investor slides)

With Bitcoin now close to $50,000, MSTR has hit $3.5 billion in unrealized profit.

Michael Saylor has decided to double down on Bitcoin, having achieved such great success with their current Bitcoin strategy.

Saylor Is All In

During the latest earnings call, Saylor made it very clear that this is a Bitcoin-centric company.

“We view ourselves as a Bitcoin development company. That means that we’re going to do everything we can to grow the Bitcoin network.”

Source: Saylor, Earnings Call

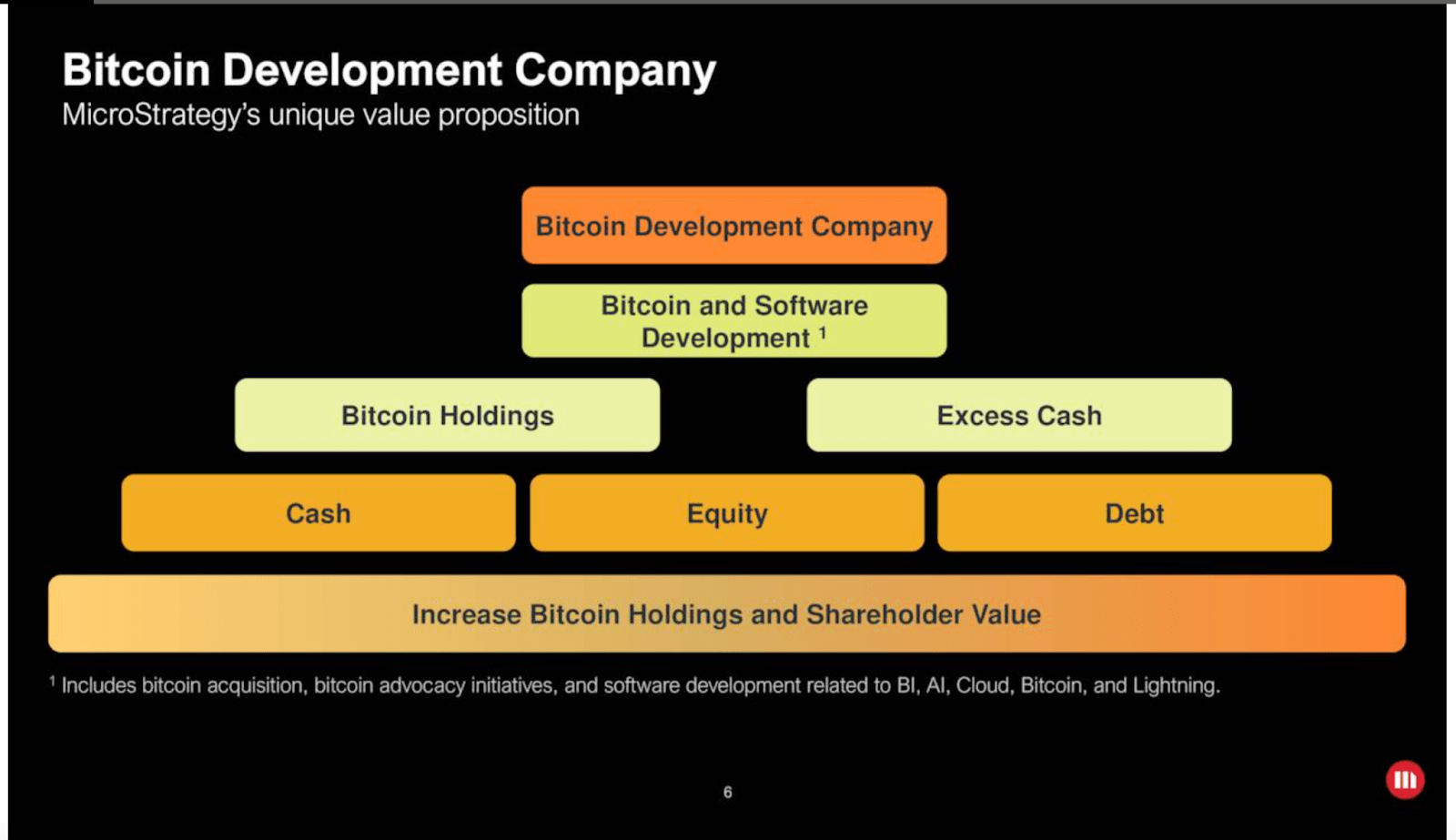

This idea was also reinforced in the earnings presentation, But what does Saylor mean exactly?

Bitcoin development company (Investor slides)

We have active control of our capital structure and we can do things operating companies can do that trust companies like spot BTC ETF they can’t do. And that’s a wide range of things, and one of those things is we can develop software,

Source: Saylor, Earnings Call

It’s still unclear what this software could look like, but it does make sense on the surface. Once upon a time, MSTR was a software company, and there’s certainly room for this expertise to be taken to the Bitcoin blockchain.

The other big part of the plan is, of course, accumulating more Bitcoin.

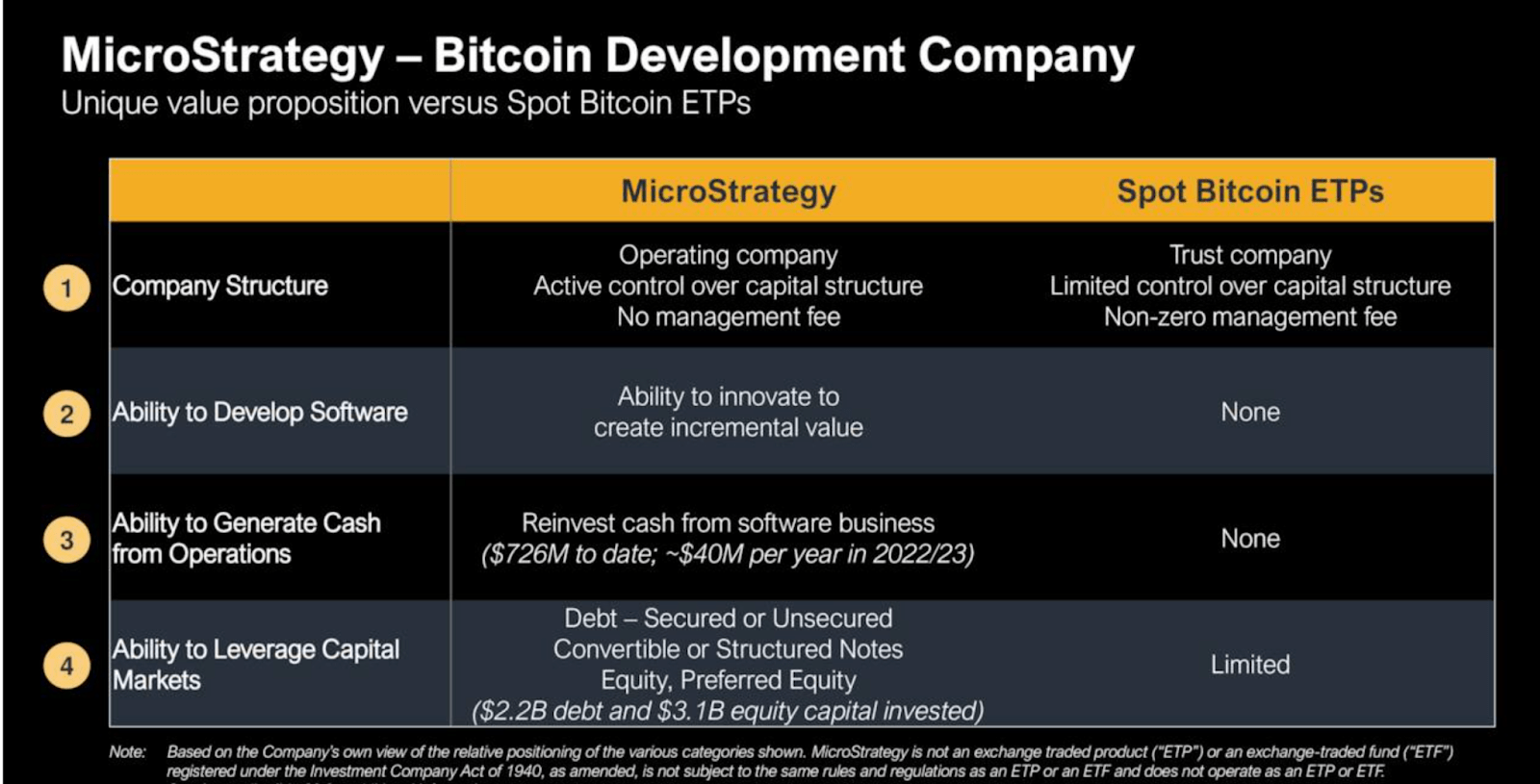

MSTR vs ETFs (Investor slides)

Granted, MSTR does have certain advantages over the ETFs. Namely, MSTR can dilute its shares or acquire more debt in order to buy more Bitcoin. If done right, this should be quite accretive to shareholder value,

Is MSTR still worth a buy?

On the surface, I like MSTR as a Bitcoin proxy, but following the last rally, it certainly seems like the stock has come close to fair value.

At $50K, MSTR’s Bitcoin holdings are now worth close to $9.5 billion. Based on some estimates, the software part of the business could be worth close to $3.3 billion.

That puts the MSTR’s fair value market cap at $12.8 billion, and its actual market cap actually stands at $12 billion right now following the recent surge. But there’s also around $2 billion in long-term debt, so the actual value is closer to $10.8 billion

Arguably, more than the company’s fair value is priced in here, which does make sense if we imagine investors are also accounting for future developments.

Firstly, one might expect MSTR to develop some income streams from Bitcoin development and related software. This is still a very speculative assumption, and the initial impact won’t be large, but it’s worth considering.

More importantly, though, I’d expect MSTR to continue accumulating Bitcoin, which it can do by increasing its debt or even diluting its shares.

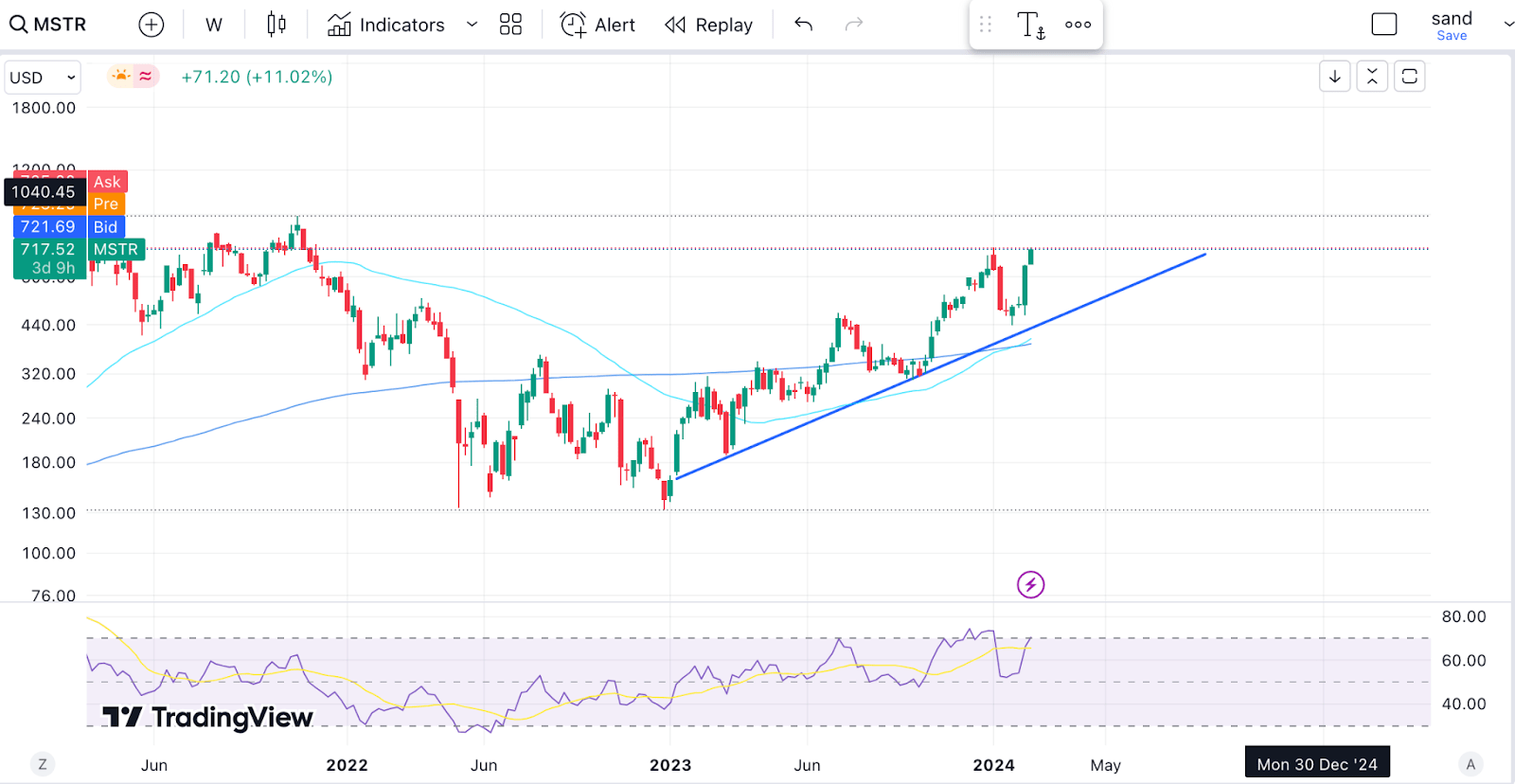

Technical Analysis

MSTR TA (Author’s work)

Technically speaking, we have some strong momentum building here. The 50-week MA just crossed over the 200, and MSTR did manage to make a higher high.

However, the RSI is nearing overbought and has so far given us a bearish divergence. I would change my neutral rating to a buy, if/when MSTR re-tests the trendline or its 50-week MA, both of which sit close to $400.

At this price, the market cap would be close to $7.5 billion, meaning MSTR would once again be undervalued in terms of its software business plus Bitcoin value at today’s price of around $50,000.

Risks

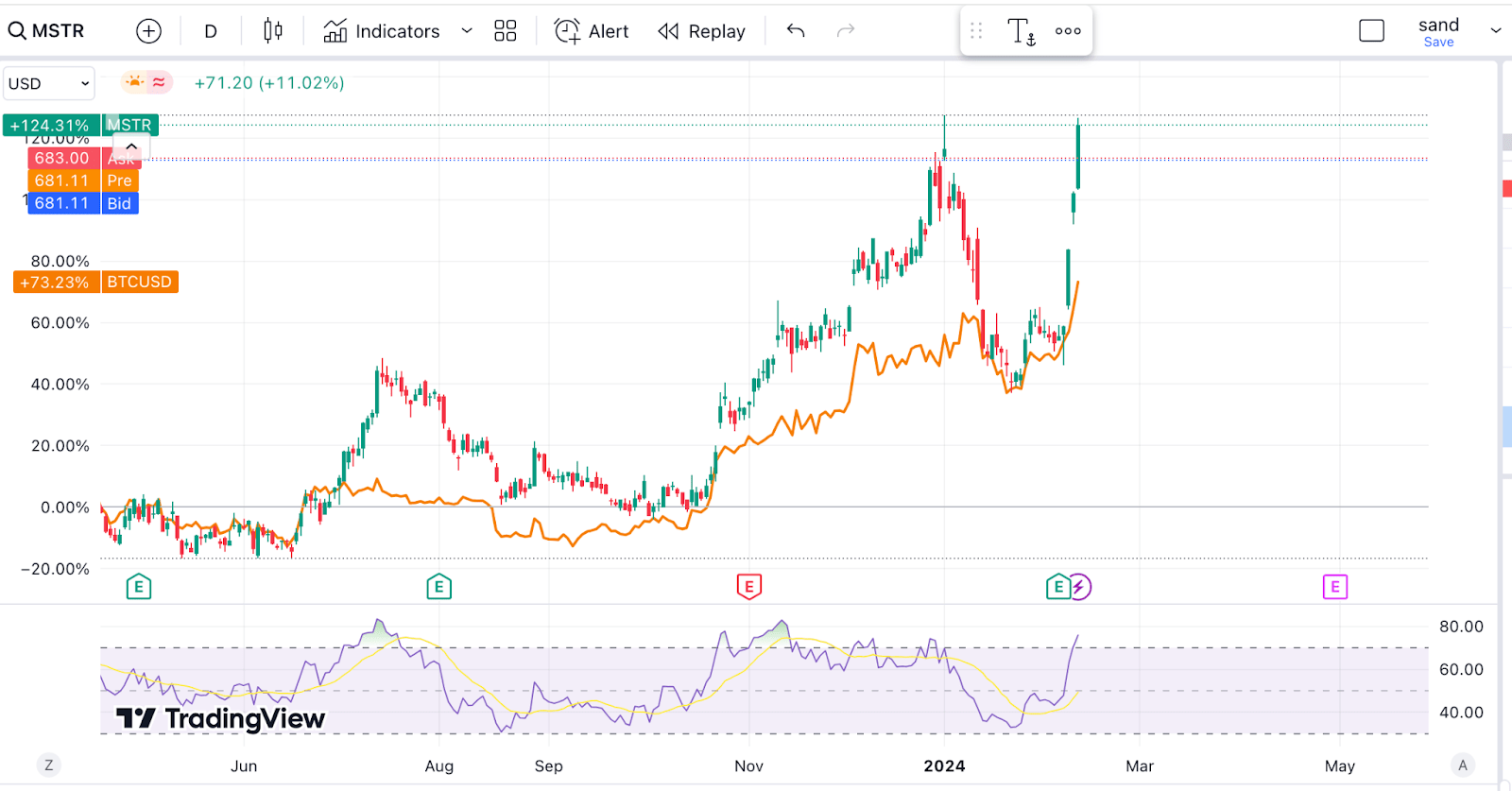

The upside potential is considerable, but it is closely tied to Bitcoin.

MSTR vs BTC (TV)

MSTR has been trading like a leveraged Bitcoin play over the last year, and I’d expect this to continue. However, it is important to note that this will be fueled by speculation and perhaps a short-squeeze rally.

From a fundamental perspective, the company isn’t worth this much. Valuing it beyond these levels relies on the hope that Michael Saylor and the company can do something beyond keep accumulating Bitcoin, but this is a very big if at this moment.

In fact, it is also a possibility, that in a valiant effort to push Bitcoin adoption forward, the company might actually sacrifice a lot of investment and revenue into developing software that, while useful, may not be very profitable to shareholders.

Takeaway

All in all, MSTR could be a compelling investment for BTC bulls, but there’s a high degree of volatility. At this price, I don’t think returns will be that much higher than Bitcoin, but if we get another big sell-off, I’ll be looking to potentially add.

Q2 2024 Earnings Call Transcript")