PJ66431470/iStock via Getty Images

My thesis

Microchip (NASDAQ:MCHP) owns a solid portfolio combining Microcontrollers, Analogs, programmable processors, and software solutions. This complete offering allows for integrated and tailor-made solutions. While the acquisition of Microsemi in 2018 was necessary, it increased Microchip’s leverage position significantly with an ND/EBITDA reaching 5x in 2019. Despite a solid cash-flow generation, it took years to reduce such debt burden.

We are currently reaching the tipping point: the leverage ratio went below 1.5X allowing for a large and recurrent distribution to shareholders. In this report, I will analyze the business model, discuss the most recent results, and provide a valuation assessment of the MCHP stock. While the investment case is solid, weak cyclical trends and a tight valuation make me wait for a better entry point. I rate the stock as a HOLD.

Investment overview

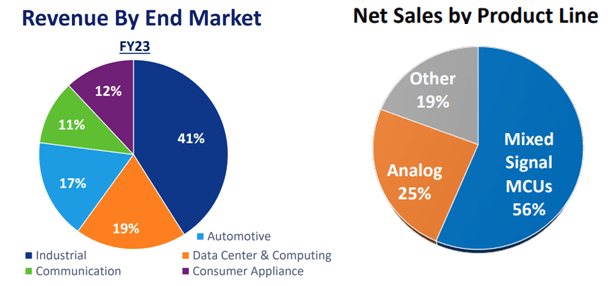

Microchip is a US-based semiconductor company created in 1989, designing and producing Microcontrollers (MCUs), Analogs, programmable processors (FPGAs), hard drive controllers, radiofrequency chip devices, and other applications. It focuses on providing Total System Solutions (TSS) for its customers: from a complete set of hardware to software and services. As such, it aims to outgrow its industry thanks to its increase in average revenue per client. It leverages its large-scale portfolio of more than 250,000 devices. Its client pool is well diversified, with above 120,000 accounts. Microchip ended last FY2023 with record revenues of $8.4 billion but has since then entered into a cyclical correction as we will discuss later on.

Microchip

The firm produces 40% of its wafers in-house, mostly older technologies while relying on external foundries to produce the rest. On top of that, it owns packaging and testing facilities. We can say it has relatively good control over its supply chain. To improve its relations with its clients and lower its business cyclicality, the firm set up 2011 a Preferred Supply Program. The PSP is helping its customers to secure inventory, by placing 12 months in advance non-cancelable orders and adding a deposit. As a consequence of the recent economic slowdown, impacting the firm’s results and creating elevated levels of inventories, Microchip decided to halt this program. The firm will have the ability to restore if the activity were to rebound.

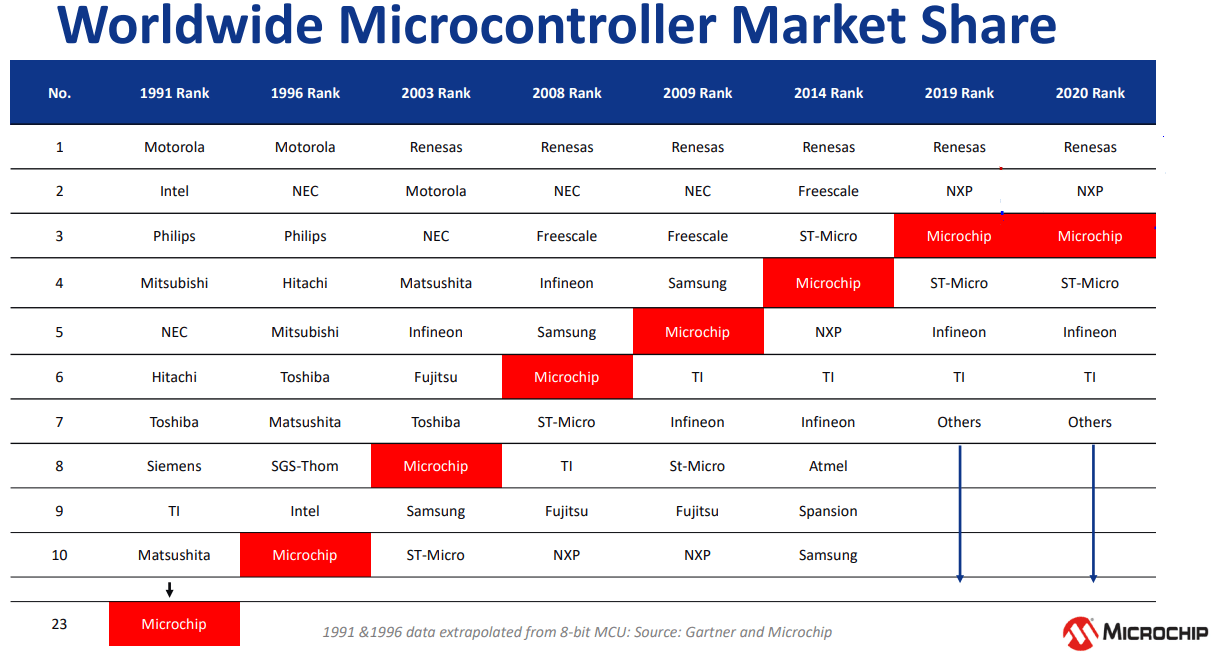

Microchip became a powerhouse by acquiring several companies. The most notable ones were the takeover of Atmel in 2016 for $3.6 billion and Microsemi for $10 billion in 2018. Atmel strengthened its portfolio in RF chips, Analogs, and memory devices, while the latter helped to increase its scale in MCUs by adding new segments such as FPGAs and storage/networking chips. Via organic growth and inorganic consolidation, the firm went from the top 10 positions in Microcontrollers to the top starting in 2020.

However, its MCU portfolio is not at the highest end of the spectrum and still importantly relies on manufactured 8 and 16-bit structures. In comparison, NXP (NXPI), STMicroelectronics (STM), and Infineon (OTCQX:IFNNY) have a more dominant position in the most advanced 32-bit chips. Microchip is gradually changing that situation by investing in 32-Bits and has already made good progress. Indeed, while in 2021 only one-fourth of its MCU portfolio was related to this latest technology, this rose to 50% in 2023.

Microchip

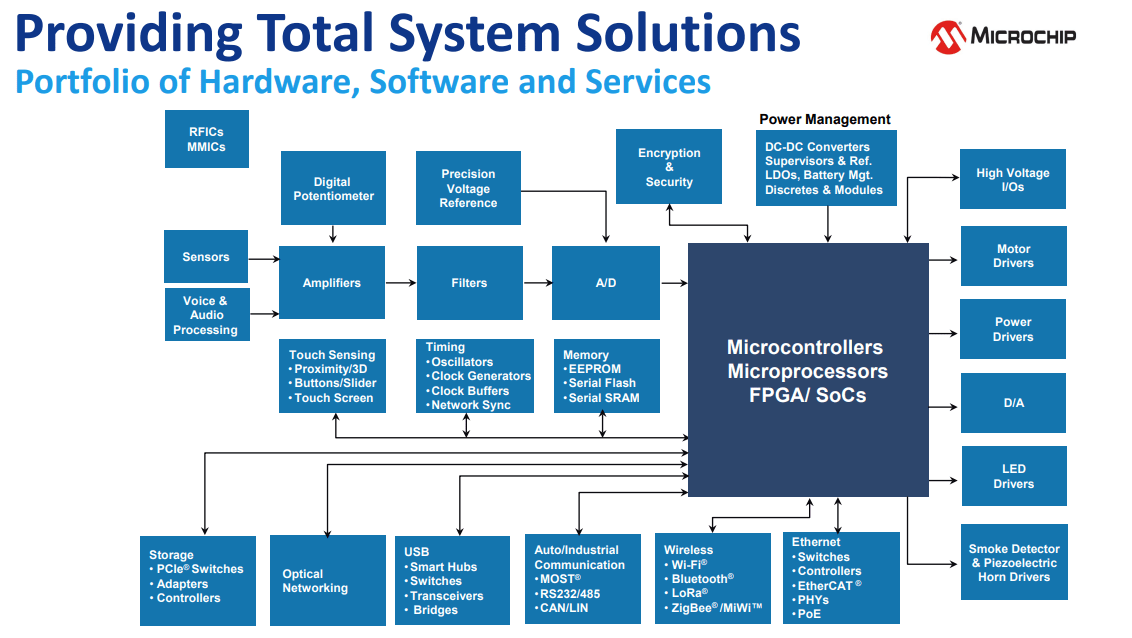

Microchip’s TSS can be mapped in the picture below. It provides a one-stop shop for its clients and translates into a solid switching cost. As a result of elevated cross-selling, the firm’s margins and cash flow conversion are high. Indeed, Microchip can generate higher revenue per client while keeping its SG&A expenses under control.

Microchip

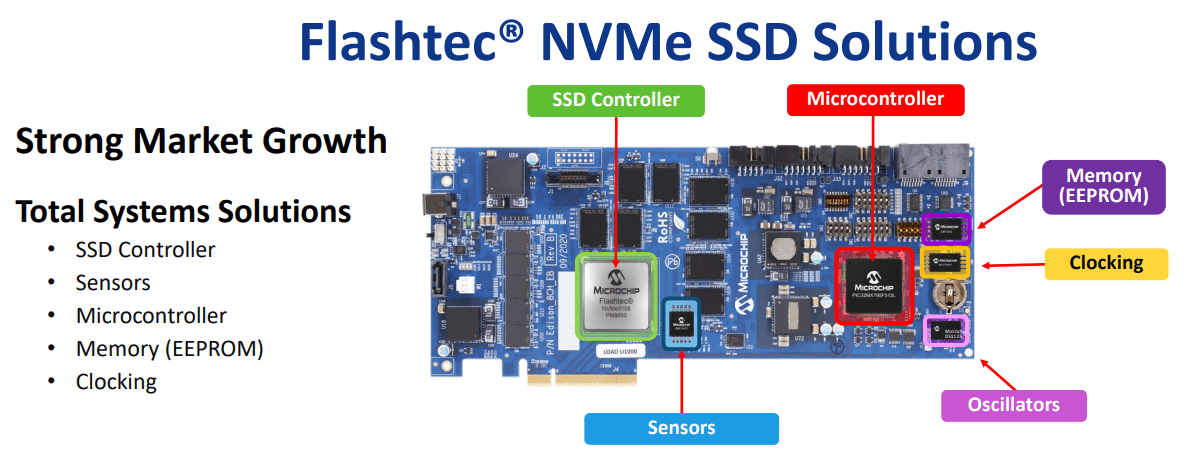

If we take one concrete example of a solution for an SSD storage drive, we see that Microchip provides a set of chips, from the controller, and MCU to sensors. Drive controllers find the location where the requested data is stored, read the data, and transfer it to the server. Such solutions are part of the data center and computing segment. In that segment, Microchip is in a quasi-duopoly, with Marvell (MRVL) as the main competitor.

Microchip

In automotive, the firm ranks number one with touch screens and buttons. Considering higher value items, it also provides chips for ADAS and infotainment where it can place its microcontrollers. Finally, it provides full solutions for EV chargers including MCU, SiC diodes, touch screen controllers, or energy metering.

Recent quarterly trends

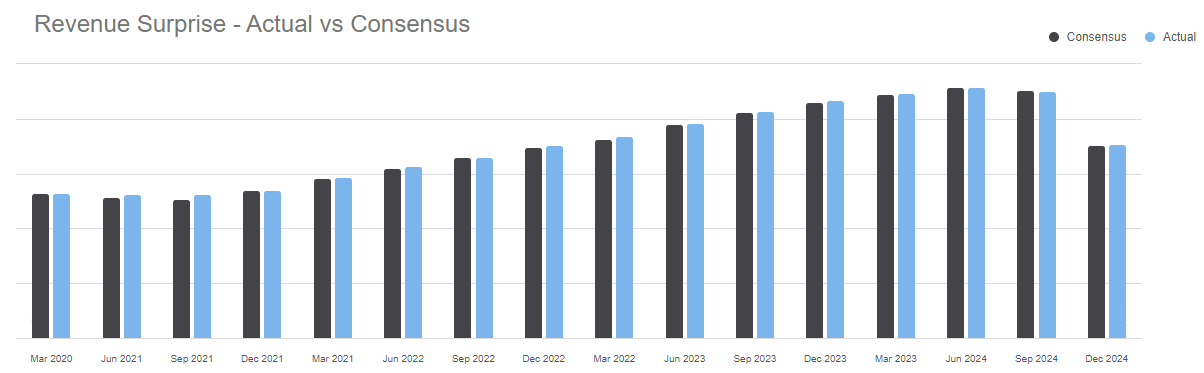

Microchip just published its Q3 FY2024 results on February 1, 2024. Revenues fell off a cliff, down 22% QoQ to $1.77 billion and down 19% YoY, while non-GAAP gross margins stood well at 63.8%. Inventory remained elevated, above $1.3 billion for the fourth consecutive quarter. Days of inventories reached 185 and increased by 10% from the last quarter. In the conference call, the company stated “We were not able to make as much progress as we would have liked“. All segments apart from defense and aerospace suffered a correction.

Seeking Alpha

What was notable in management’s comment was that its end markets were much weaker than expected around all regions. It stated that: “many customers implemented extended shutdown in December” and that Microchip was “able to push out or cancel backlog” to help customers better handle their inventory levels. The management added that such a situation was the result of a just-in-case policy set in place post-COVID disruptions, replacing just-in-time inventory management. Also, overly optimistic views of business CEOs during 2023, expecting strong economic growth would continue in 2024.

Microchip reacted to such a difficult situation by lowering utilization rates of its factories around the world and implementing cost-cutting measures such as wage cuts around all its organizations. The next and fourth quarter of FY2024 should continue to fall, with revenues seen close to $1.3 billion implying a minus 27% decline while gross margin should resist close to 60% thanks to factory optimization. The firm CEO concluded by saying: ” We don’t know how and when the upcycle will play out“. As a consequence, no guidance beyond the next quarter was given. The only positive point in my opinion was the indication of the revenue decline) is mainly volume-related due to under-shipping and not price-driven as the management said: “pricing is stable“.

What valuation can we expect?

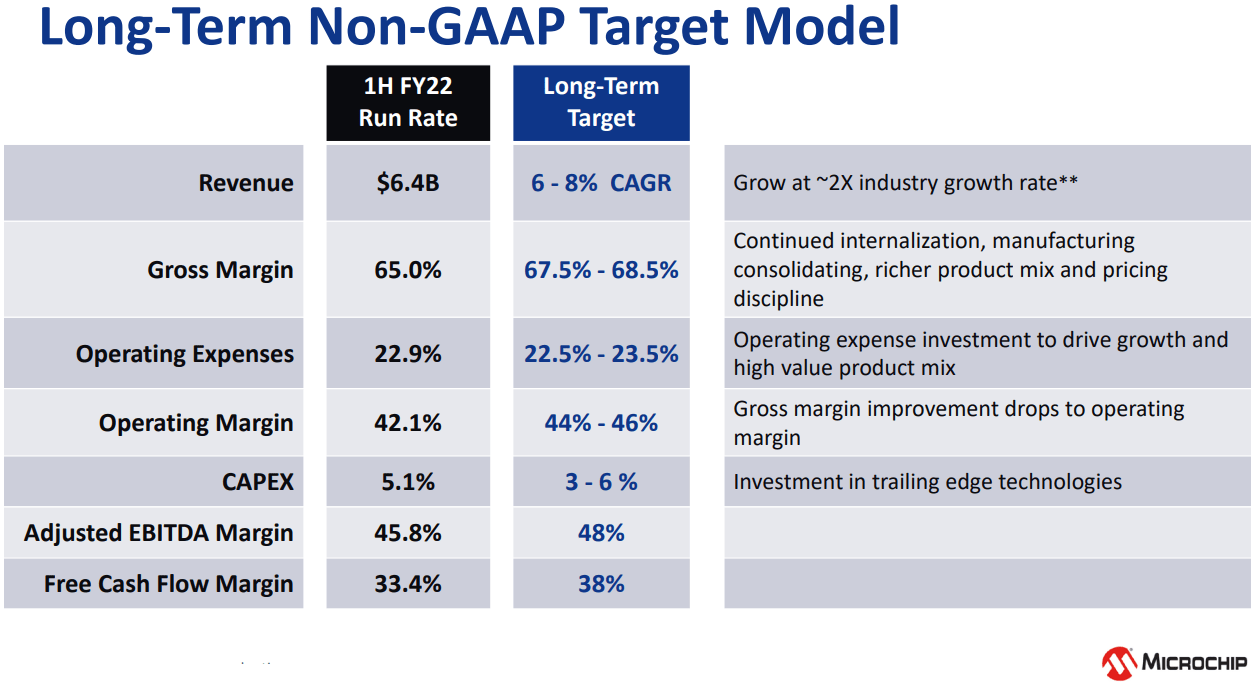

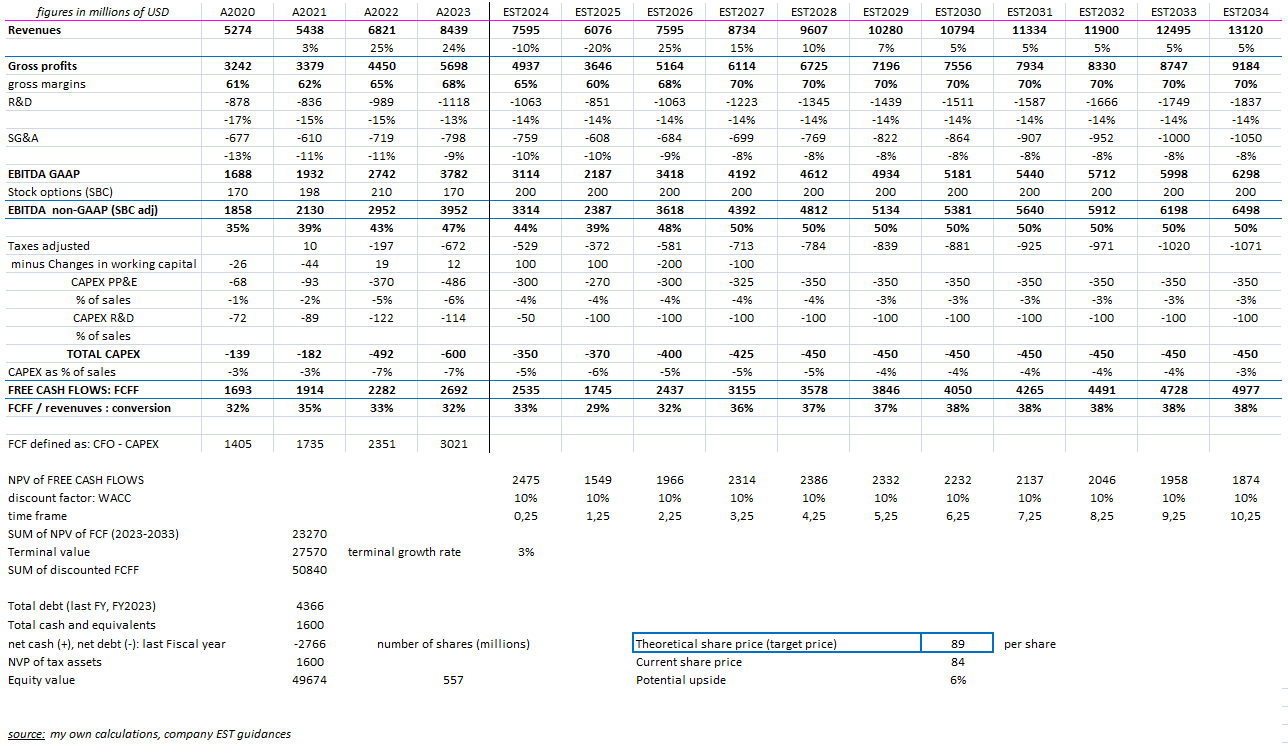

During the 2021 Investor Day, Microchip set a long-term target model. I took into account some of its hypotheses in my following DCF model.

Microchip

As revenue growth started a cyclical correction last quarter (Q3 FY24), a big part of the downturn will be felt in FY2025 (end Match 2025). I, therefore, model Microchip will hit the bottom during the next fiscal year. The rebound could be quick and large hereafter as has been the case historically in Industrial MCUs. In the medium-term (FY2028-2034), I see a CAGR of 6%, at the bottom of the range of the Long-term model provided by the management.

Microchip Total System Solutions help stabilize the firm margins, even during a downturn as we witnessed in the latest quarterly result. As a consequence, I don’t see gross margins to compress below 60% despite the expected revenue decline. It is impressive that pricing is stable despite an ongoing volume correction. This could be the new normal, post-supply-chain disruption.

When macro trends improve, I believe the operating margin could hit 50%, higher than the 2021 management estimates. Indeed, semiconductor companies (MCU and Analogs peers) have seen a clear sustainable progression of their operating leverage.

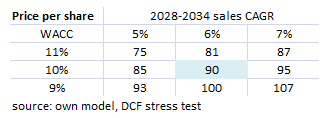

FY2024 CAPEX is expected to reach $305 million and it was said during the last conference call that the FY2025 spending level should be lower. My model uses a 4.5% CAPEX/sales ratio for the medium term. All-in-all, the FCF conversion I obtained mid-term is close to 38%. Using a WACC of 10% and my estimates, I do find the stock is broadly fairly valued.

own calculations

To give more perspective, I implemented a sensitivity analysis, varying medium-term (2027-2034) growth rate and the discount rate:

own calculations

Balance sheet analysis

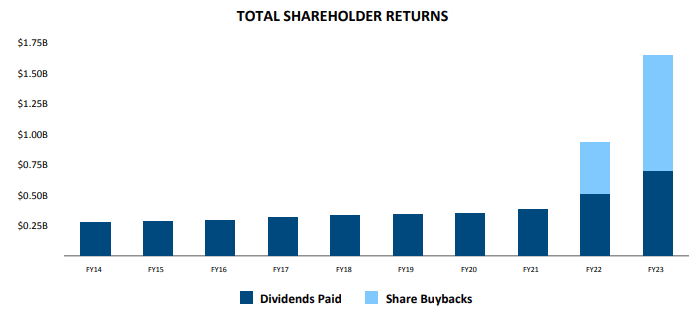

During the last quarter, the ND/EBITDA declined to 1.3X allowing the firm to further increase its cash distribution to shareholders to 82.5% for the next quarter and go to 100% by March 2025. This commitment is valid unless the leverage ratio rises above 1.5x. During the nine months of FY2024, the firm distributed $1.3 billion cash to shareholders, roughly half dividend and half buybacks. I expect the total annual cash yield to reach $1.8 billion for FY2024 leading to a yield of 4% over the market cap.

Microchip

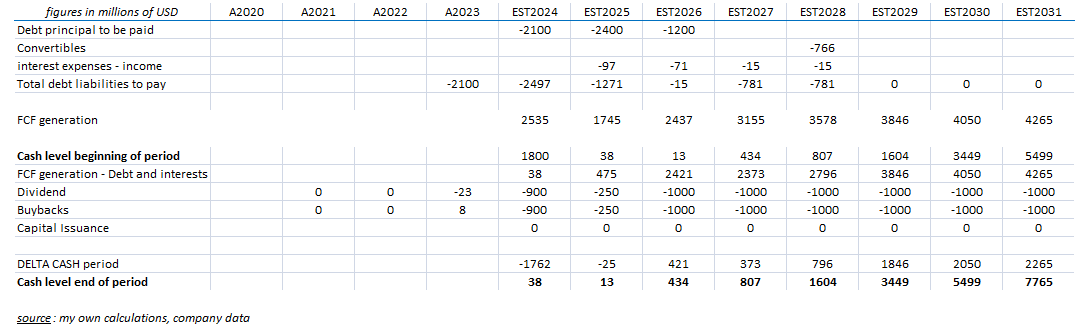

Concerning FY2025 (ending March 2025): my calculations show that cash distribution will be modest in amount as the FCF should be compressed and the firm has to repay $2.4 billion of bonds maturing during CY2025. However, starting FY2026 and beyond, Microchip could manage to distribute more than $2 billion cash payout, equivalent to a yield close to 5% which I find appealing.

own calculations

Technical analysis

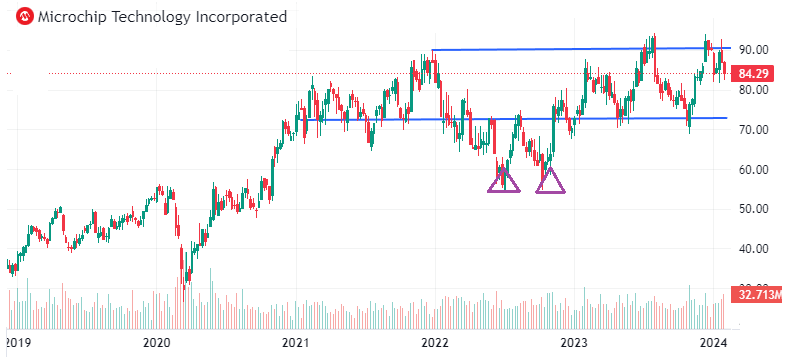

The stock rebounded strongly from mid-2022 lows via a double bottom at $55/share and then gradually reached recent highs close to $90/share. The ongoing cyclical correction of Microchip ends markets, with no clear rebound seen by the management in the near term, is not coherent with all-time high price levels. Given the weak Q3 and guidance, the stock deserves a correction. I would wait at the bottom of the upper range, looking at the support near $70-75/share, for a better entry point.

Seeking Alpha

Risks and opportunities

The main risk is see is related to the fact Microchip is competing with bigger companies in three of its markets. In microcontroller MCUs, it is NR4 with 14% market share after STMicroelectronics, Renesas (OTCPK:RNECF), and NXP. Within Analog, it is a relatively small player if we compare it with Texas Instruments (TXN) and Analog Devices (ADI). Finally, in FPGA processors, I estimate its revenues are now close to $500m as it generated close to $400m annually in 2021. This is much smaller than Xilinx from (AMD) and Altera from (Intel).

Another secondary risk comes from the fact its industrial segment is quite large, close to 40% of its sales, and is subject to high swings. Therefore, the P/E ratio has to discount such cyclicality.

Conclusion

Fundamentally, it would be the time to buy the stock Microchip management has built a company having a complete portfolio of semiconductors, software, and services, serving as a full solution for its clients. In the meantime, the debt level is now under control while the solid FCF generation allows for increasing cash distribution. Still, it is difficult to ignore the current cyclical downturn of its end markets, and the management just said no clear rebound is foreseen. It would be more rational to wait a bit more before adding to the stock. I rate the investment as a Hold.

Q2 2024 Earnings Call Transcript")