damircudic

One of the most attractive players in the banking sector that I’ve seen this year has got to be Metropolitan Bank Holding Corp. (NYSE:MCB). With a market capitalization of $407.2 million as of this writing, the institution is small enough to fly under the radar of most investors. Despite the company experiencing a bit of pain from a profitability perspective this year, the overall financial performance of the business in recent years has been solid and management continues to be successful in growing the enterprise. Add on top of this how cheap shares are and I do believe that the bank makes for a ‘strong buy’ prospect at this time.

A great opportunity to bank on

According to the management team at Metropolitan Bank Holding Corp, the institution operates as a bank holding company that’s based out of New York City. At present, the company has six different banking centers, four of which are located in Manhattan. Another is located in Brooklyn, while the last is located in Long Island. The firm also leases a property in Florida that it utilizes as a loan production office, as well as another property in New Jersey for administrative functions. Additional office space for one of its units is located in Kentucky.

Operationally speaking, Metropolitan Bank Holding Corp engages in a wide variety of traditional regional banking activities. Just admire any commercial bank, the firm accepts deposits from its clients. It then lends these deposits out in a variety of manners. Examples of specific products it offers include commercial real estate loans, mortgages for multifamily properties, construction loans, commercial and industrial loans, and more. It also has a Global Payments Business through which it administers domestic and international digital payment solutions on behalf of financial technology clients while also serving as an issuing bank for third-party debit card programs nationally. Up until this year, the company also engaged in the digital currency space, which many know as the crypto asset market. In addition to all of this, the institution also provides corporate cash management deposit accounts. These are accounts that belong to clients that have possession of or control over large deposits, with examples of these clients being property management companies, title companies, and bankruptcy trustees.

Author – SEC EDGAR Data

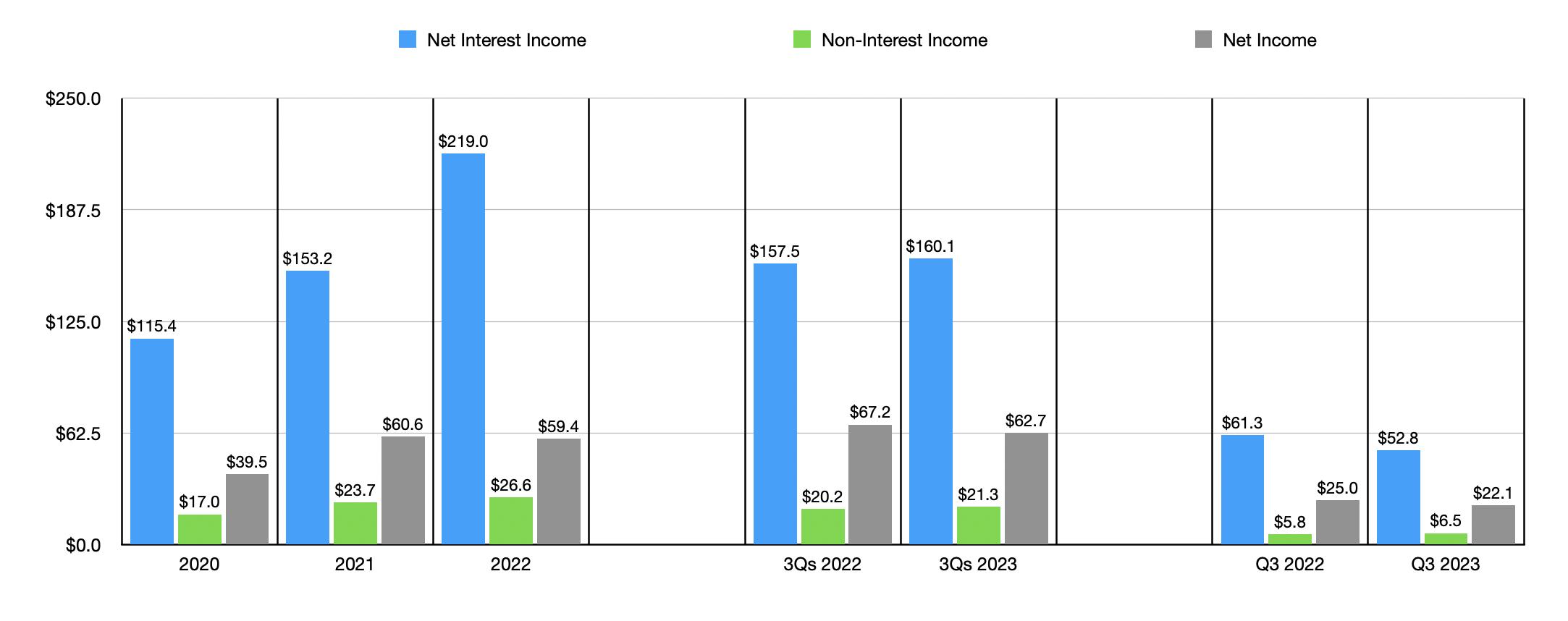

Over the past few years, management has done quite well to grow the company’s top line. Net interest income grew from $115.4 million in 2020 to $219 million in 2022. Over the same window of time, non-interest income expanded from $17 million to $26.6 million, while net profits managed to grow from $39.5 million to $59.4 million. Financial performance this year has been somewhat hampered. For the first nine months of this year, net interest income came in at $160.1 million. That’s only marginally higher than the $157.5 million reported one year earlier. Non-interest income inched up only slightly from $20.2 million to $21.3 million. Unfortunately, none of this stopped net profits from pulling back marginally from $67.2 million to $62.7 million. Higher expenses, such as a sizable boost in professional fees, larger FDIC assessments, and changes in regulatory settlement reserves, were largely responsible for this bottom line pain.

Author – SEC EDGAR Data

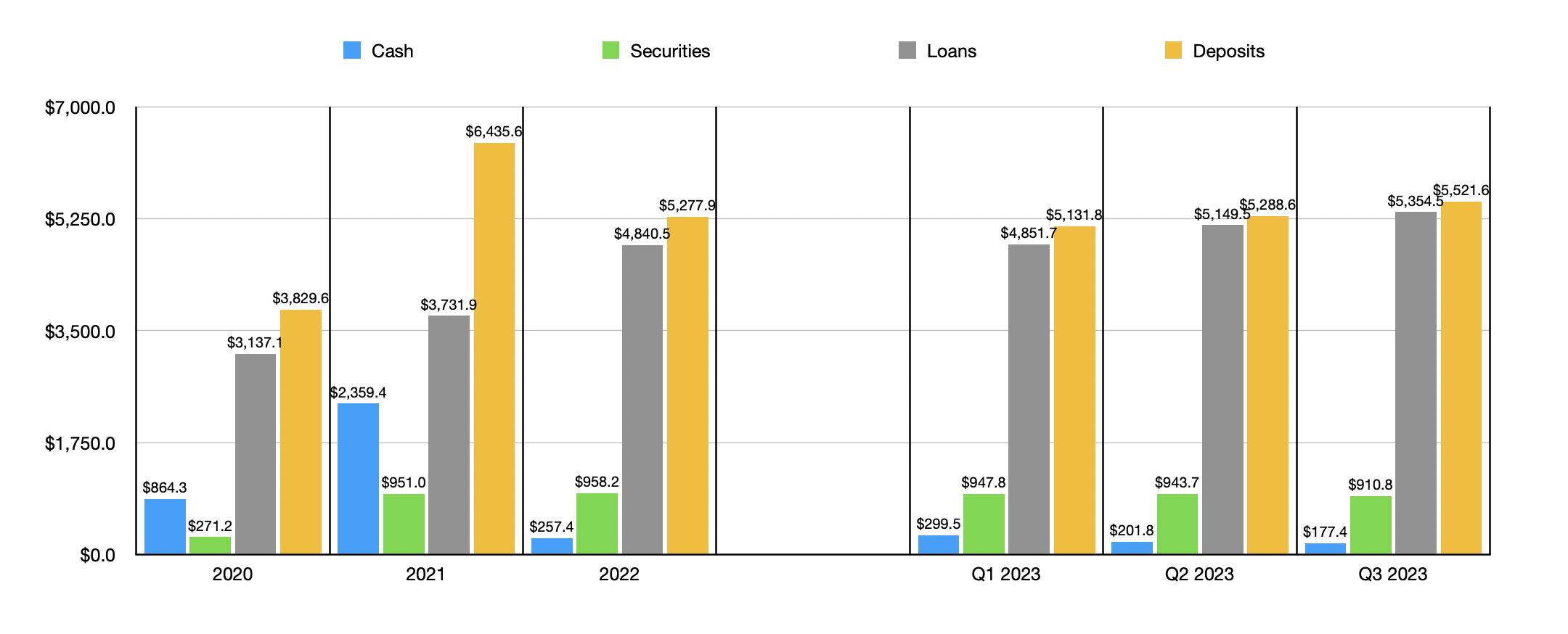

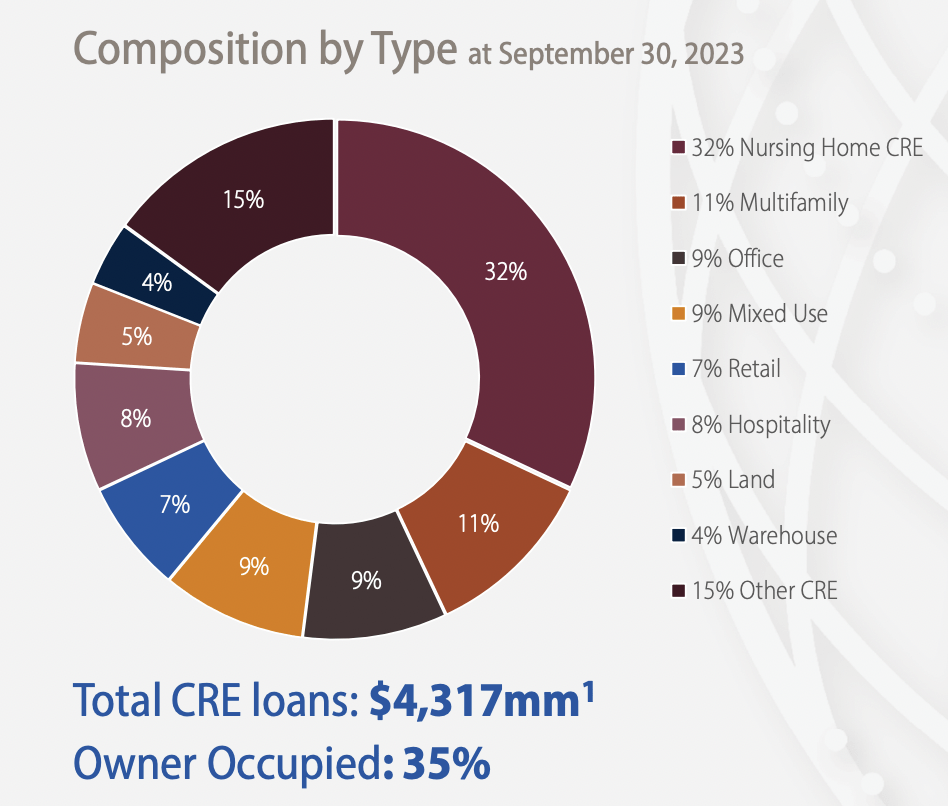

The overall growth in both the top and bottom lines for the institution was made possible by continued expansion of the company’s assets. The value of loans on its books, for instance, grew from $3.14 billion in 2020 to $4.84 billion in 2022. The company continued to see growth after this, with the value of loans eventually hitting $5.35 billion by the end of the third quarter of this year. One thing that I know that investors have been worried about when it comes to loan exposure is the amount of a bank’s portfolio that’s dedicated to office assets. The vast majority of the company’s loans, about $4.32 billion in all, are dedicated to commercial real estate. But only about 9% of that, or 7% of total loans, involve office assets. It is true that another 9% of commercial real estate loans, by value, involve mixed-use properties. So there could be some additional exposure there. But mixed-use properties do tend to be safer than assets that are specifically office oriented.

Metropolitan Bank Holding Corp

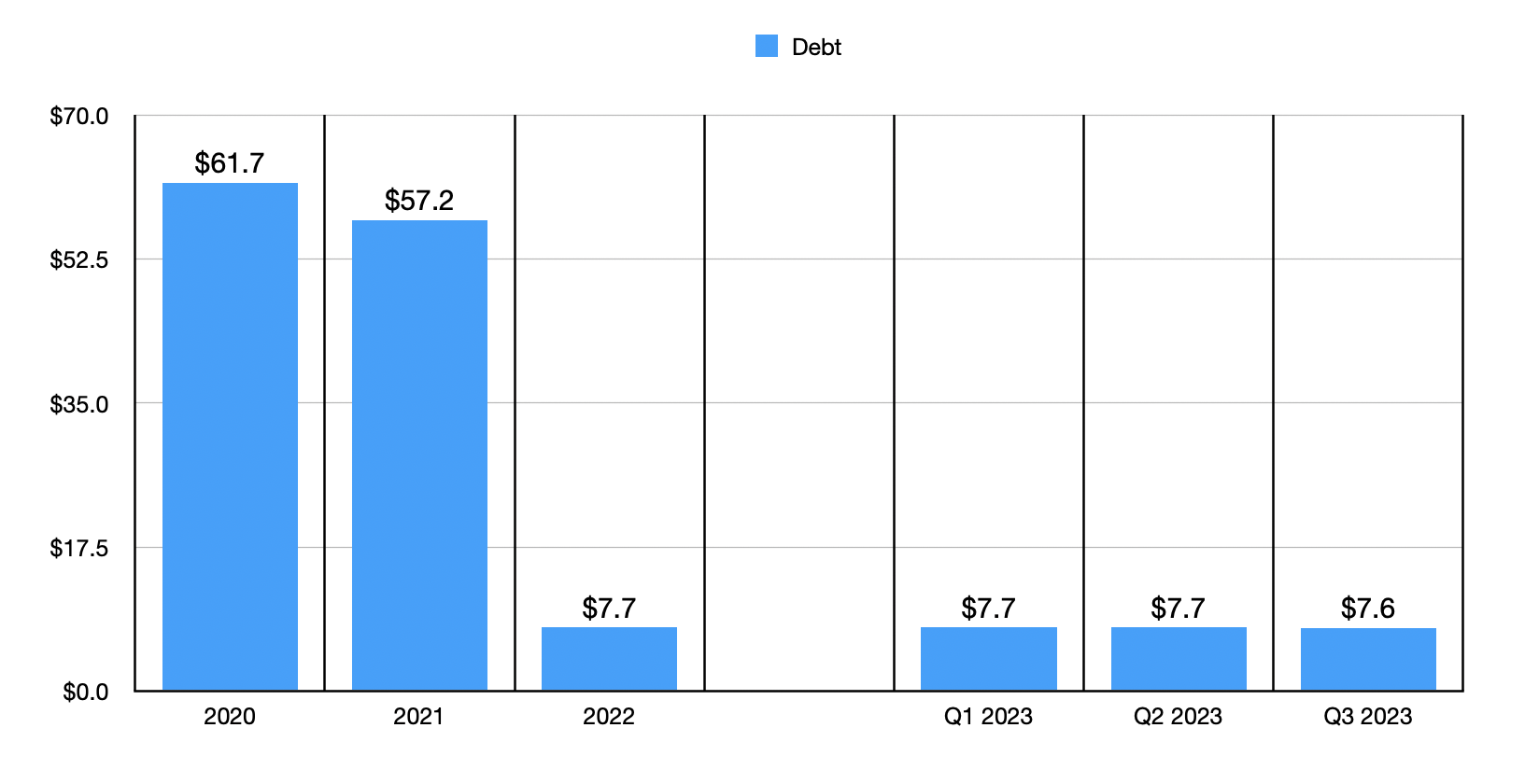

This is not to say that everything has been great from an asset perspective. Since 2021, the bank has seen a rather significant refuse in the value of cash and cash equivalents on its books, with the metric dropping from $2.36 billion to only $177.4 million. On the other hand, at least the value of securities has been stable, fluctuating in the $900 million range from the end of 2021 through the present day. The good news is that, even though cash has decreased, the value of debt on the books has remained incredibly low. As of the end of the most recent quarter, the bank had only $7.6 million in the form of debt. That means there is very little in the way of risk for shareholders on this front.

Author – SEC EDGAR Data

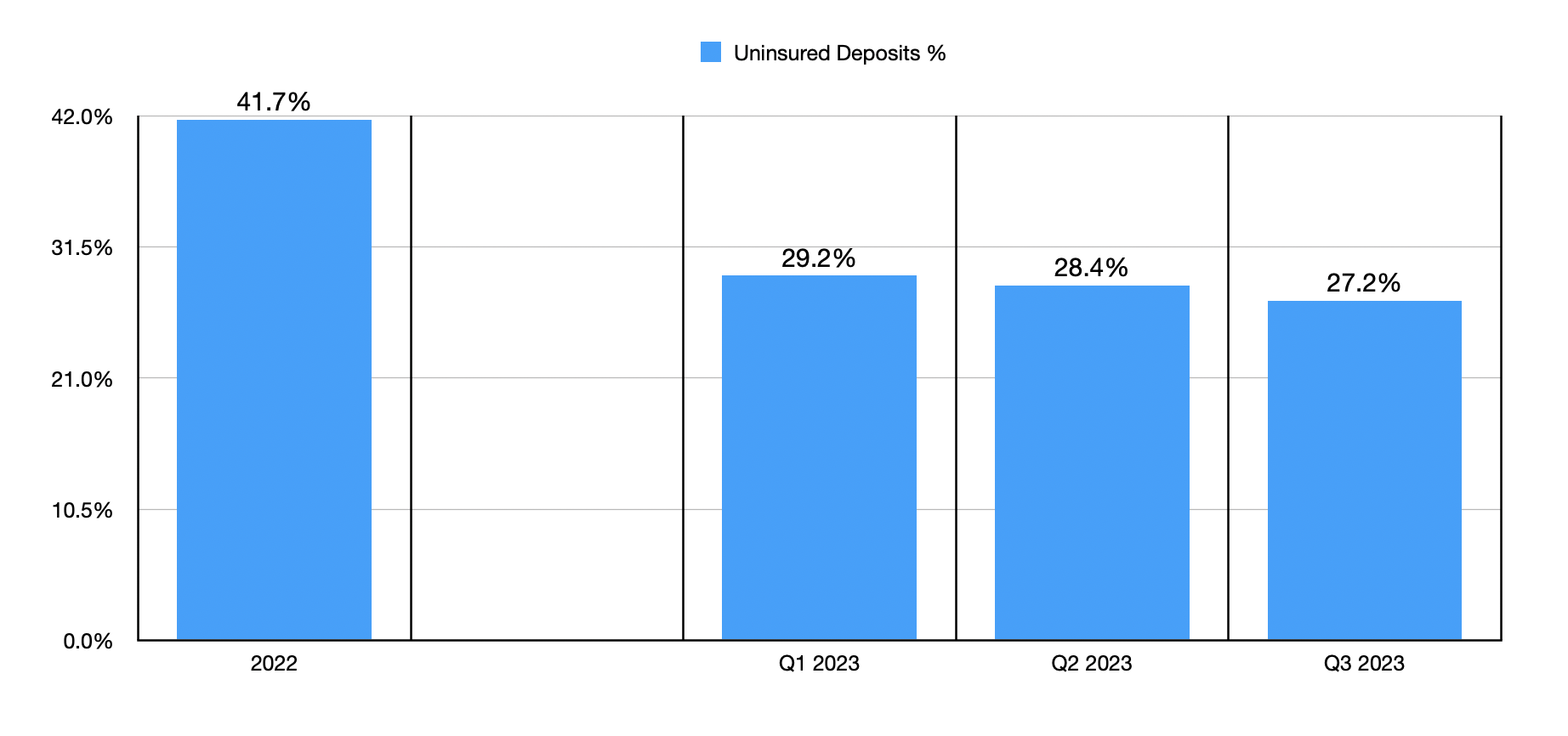

The growth in the value of loans that the institution has was made possible by continued growth in deposits. These jumped from $3.83 billion in 2020 to $5.28 billion in 2022. It is worth noting that the 2022 reading is lower than the $6.44 billion reported at the end of 2021. However, ever since dropping, the value of deposits has only grown. By the end of the most recent quarter, deposits had expanded advance to $5.52 billion. That’s $233 million higher than what the bank reported one quarter earlier and it is 4.6%, or $243.7 million, above what the business ended the 2022 fiscal year at. Honestly, I find this continued boost fascinating. After all, according to management, the company reported a $488.9 million decrease in deposits this year associated with its decision to exit the cryptocurrency space. So to see growth continue even after losing such a sizable portion of deposits should be bullish. It’s also worth noting that the bank went from having 41.7% of its deposits classified as uninsured at the end of last year to 27.2% today. That’s a bit below the 30% threshold that I see as important.

Author – SEC EDGAR Data

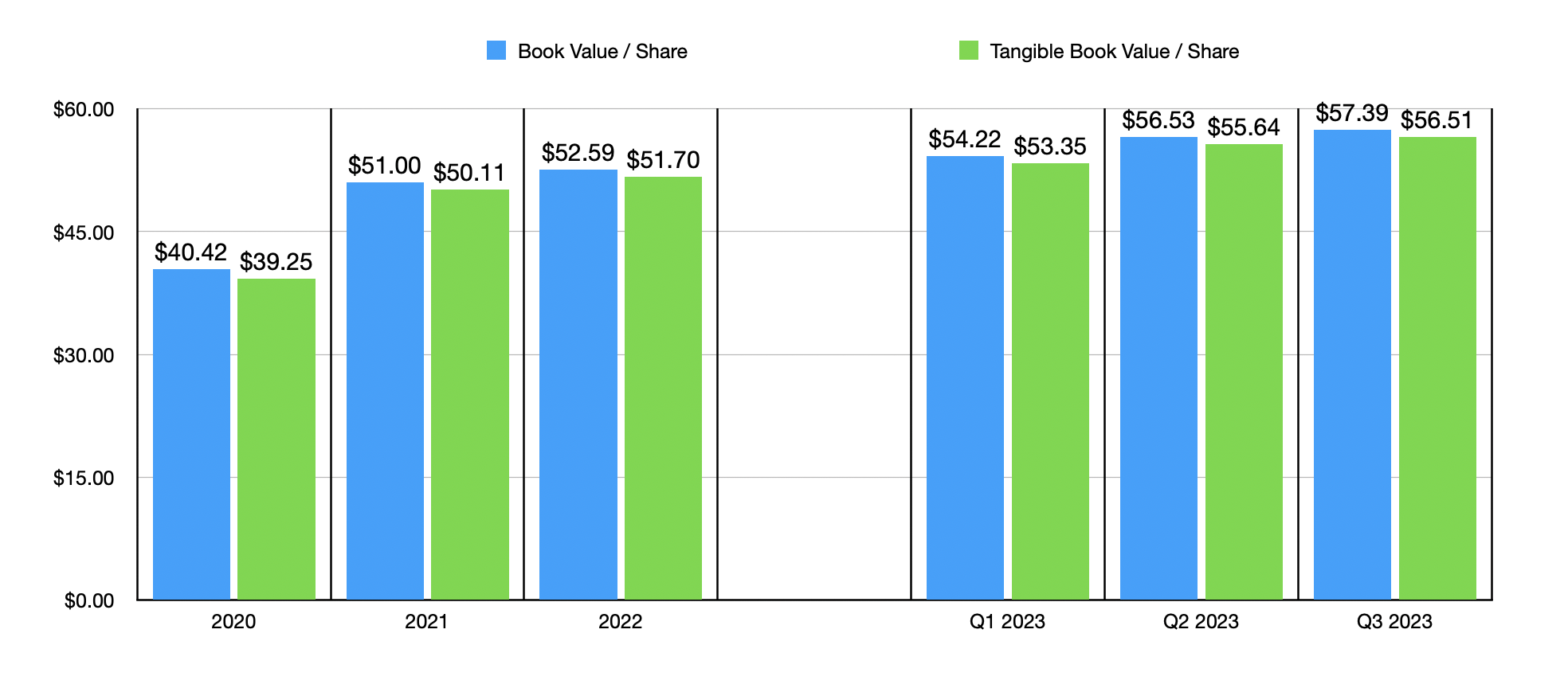

In terms of valuing the bank, it’s worth noting that, using data from last year, shares are trading at a price to earnings multiple of only 6.9. While not the cheapest that I have seen, it is very cheap, with most banks trading between a multiple of 6 and 11. The institution is also trading at 65.2% of its book value and at 66.2% of its tangible book value. Both of these are significantly lower than with the vast majority of banks trading much closer to their book values on a per-share basis.

Author – SEC EDGAR Data

Takeaway

Based on the data available, I would argue that Metropolitan Bank Holding Corp. is most certainly an appealing prospect. While I don’t admire seeing bottom line weakness this year, and it would be nice to see the cash on its books boost, pretty much everything else about the institution is very appealing to me. Given these factors, particularly how cheap shares are, I would argue that Metropolitan Bank Holding Corp. is definitely worthy of a ‘strong buy’ rating at this time.

Q2 2024 Earnings Call Transcript")