Grace Cary/Moment via Getty Images

Investment overview

FYI: I wrote about Meritage Homes Corporation (NYSE:MTH) previously with a buy rating as I thought the business was well placed to meet the home undersupply situation in the US, especially with its ability to provide incentives to capture demand. I stay buy-rated for MTH as the demand outlook remains very strong, with orders growing 60% in 4Q23 and visibility going as far as 6 months out. Importantly, I think MTH has a chance to beat its guidance as management is not pricing in any rate cut.

4Q23 earnings results

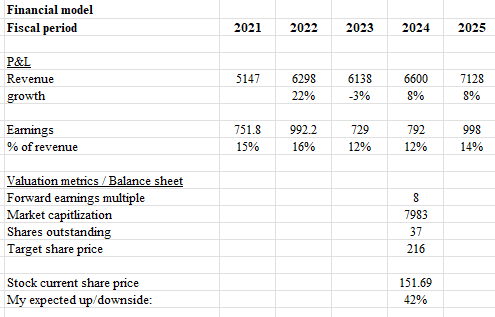

MTH reported total revenue of $1.65 billion for 4Q23, ending the year with a total revenue of $6.138 billion (include financial services revenue), implying y/y growth of -17% and -2.4%, respectively, which was better than I had expected on a full-year basis. Down the income statement, MTH reported 4Q23 gross profit of $439 million, implying a margin of 26.5%, a 30bps improvement vs. 4Q22. However, a higher operating cost structure led to a decrease in EBITDA margin by around 200bps, from 18.1% in 4Q22 to 16.1% in 4Q23. That said, all these were well within my expectations, as the 4Q23/FY23 net margin came in at 12%, in line with my model expectation. In terms of EPS, MTH reported 4Q EPS of $5.38 (diluted basis), which was an outperformance vs. consensus of $5.15.

Demand outlook remains visible and strong

MTH’s year-over-year revenue decline was primarily due to the high base seen in FY22 due to the distortion caused by the pandemic. Hence, revenue is not a good indicator of growth momentum. What investors should pay attention to is unit order growth. In 4Q23, MTH reported 60% growth in order, which is an extremely strong performance, led by Texas up 72%, while the West and East were up 56% and 52%, respectively. When combined with the community count declining by 1% vs. last year, this implies an absorption growth of 64% vs. last year. This is a massive step up from the 51% absorption decline seen in 4Q22. This translates to an absorption month of 3.6, near the midpoint of the management target of 3 to 4 months. My thesis that the home undersupply situation will drive home buyers to purchase new construction is playing nicely, and this theme should continue to benefit MTH for the foreseeable future. For reference, entry-level buyers continue to account for 88% of orders this quarter. In terms of visibility, management noted they have 6 months of supply on the ground, which is the high end of the 4-6 month target range. Given that demand is not a concern here, I believe this supply on the ground should translate easily to bookings and revenue, which means MTH effectively has six months of revenue visibility already. This should also ease some investors’ concern that MTH is facing a lack of community count growth (4Q23 ended with 270 communities vs. 4Q22 of 271).

Another important thing to note is that MTH continues to focus on affordability, as can be seen from FY23 orders ARPU performance, which fell by 4%. Pricing is a very important attribute in the current home purchase decision-process because of the high mortgage rates. By keeping prices as affordable as possible, this ensures MTH can continue to convert supply to demand; this can be seen in the surge in conversion ratio (closings/backlog) to >100% in 4Q23.

Good chance for guidance beat

In my opinion, a big part of why MTH share price fell after the strong demand outlook is because management guided for gross margin to decelerate in FY24, which essentially implies earnings to be negatively impacted as well. Specifically, management guided gross margin to be in the range of 23% to 23.5%, a big decline on a year-over-year basis at the midpoint. The primary reason for this decline was that higher land costs are going to surface in the P&L, offsetting the benefits of lower incentives, and importantly, operating conditions hold in line with late 2023. The latter is important to note because this means that management is not incorporating any rate cuts, and the Fed has signaled that they still expect three cuts in 2024, suggesting potential upside from here. The initial phases of the rate cut will be very favorable to MTH because existing home owners will still remain wary about the rate outlook. My logic is that it takes time to sell the house, and if by the time the house is sold and rates are higher, they will be on the hook for higher refinancing costs. Hence, the existing home supply will not see a major shift. However, for home buyers, the decline in rate will almost immediately be reflected in mortgage rates, making it cheaper for them to purchase homes (which MTH benefits). In this case, MTH can afford to further reduce incentives as the cost of a home purchase is cheaper due to rates (the benefit of reducing incentives outweighs the increase in land costs).

Also, from a historical perspective, management tends to under-guide. If we look at all the EPS guides that MTH has provided (2/3/4Q15, 2/3Q16, 3Q20, 3Q21, 3/4Q22, and 2/3/4Q23), they have managed to beat their guidance by 13% on average. We could see a similar situation for FY24.

Balance sheet remains strong

MTH continues to have a strong balance sheet, ending the year with a net debt of ~$100, giving it ample flexibility to lever up the balance sheet when needed. Note that most of the debt is in cash ($921 million), which means MTH has readily available cash on hand to be deployed. Having cash is crucial today as MTH growth is capital-intensive; MTH needs enough dry powder to acquire land for development. This is evident in 4Q23 when MTH allocated $654 million, an increase of 86%, towards land acquisition and development.

Valuation

May Investing Ideas

Based on my research and analysis, my expected target price for MTH is $216.

- I expect revenue to grow faster than I previously expected after seeing the strength in order growth and also pricing the reality of a rate cut in 2024, which should drive further demand. Management guidance for FY24 revenue is $6 billion, but according to its guidance history, it tends to beat guidance by 10%; hence, I am assuming $6.6 billion. This growth momentum should follow through into FY25, given that the home supply situation is not going to go away anytime soon.

- For earnings, I have tamed down my margin expansion expectation for FY24 to reflect management’s FY24 guidance. I assumed the high end of the guide, as I expect the upcoming rate cut to outweigh the impact of the higher land cost. However, my expectation for FY25 remains the same, as incremental sales should drive operating leverage

- My valuation expectation stays at 8x forward earnings, as this is the mid-cycle multiple that MTH historically trades. That said, there is a case to be argued here that valuation could go higher as the market starts to price in the impact of a rate cut.

Risk

Gross margin deterioration could be due to other unknown factors that might be structural to the business. If gross margin continues to decline from here, it could outweigh other positive margin drivers, leading to a flatter net margin for the near term, thereby impacting earnings growth.

Conclusion

I remain buy rated for MTH. The 60% growth in orders during 4Q23 is strongly evident that the demand trend is still very strong. Coupled with MTH’s focus on affordability, I expect MTH to easily convert supply to demand in this high mortgage rates environment. Despite management’s cautious gross margin guidance for FY24, potential rate cuts in 2024 could be a catalyst for guidance beat as the cost of home purchase decreases (lower mortgage rates).

Q2 2024 Earnings Call Transcript")