Mastercard (NYSE: MA) and Visa (NYSE: V) have an effective oligopoly in the payment processing space. That’s a good thing for their businesses in some ways, and a bad thing in others. But the good largely outweighs the bad, which helps explain Mastercard’s 500%-plus share-price gain over the past decade. Nevertheless, the buy, sell, or hold decision on Mastercard stock isn’t exactly an easy one.

Buy Mastercard?

To start with the positives, Mastercard’s industry position is strong. While Visa is actually a bigger company, that doesn’t change the fact that Mastercard is a giant that would be hard for a smaller competitor to displace or replace. As card-based payments grow, so, too, does Mastercard’s business. There’s no particular reason to believe that the upward trend in the payment processing industry is going to come to a sudden halt.

Image source: Getty Images.

If you are a growth-minded investor, that is a compelling storyline and one you might want to jump on. In addition to that, Mastercard has raised its dividend annually for 12 years. The annualized dividend growth rate over the past decade was a heady 23%. More recent boosts have come in at around half that level, but even that is still a huge expansion rate. So if you are a growth-and-income or dividend growth investor, you might find this stock appealing, too. But hold on a second before you run out to buy it…

Hold Mastercard?

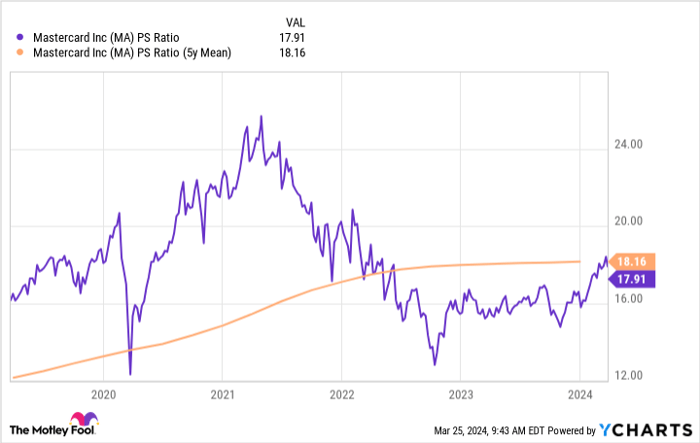

Here’s where things get a little more interesting. Mastercard’s price-to-sales ratio is around 18.2 today versus a five-year average of 18.1 or so. Its price-to-earnings ratio is 40.9 versus a longer-term average of 40.7. The company’s price-to-cash-flow ratio is 32.9 compared to 32.8. And the price-to-book-value ratio is 65 versus the longer-term average of 55 or so.

MA PS Ratio data by YCharts

In fairness, the only metric that is significantly out of line with the five-year average is the price-to-book-value ratio. But all of the other traditional valuation measures are clearly indicating that the stock is, at the very least, fully valued.

The dividend yield is around 0.5%, which isn’t terribly compelling. And that is middle of the road-ish, historically speaking. So the stock looks fully valued and that might lead some investors to hit the pause button on buying it. But while Mastercard’s valuation isn’t especially attractive, it is perhaps not bad enough to those who own it to sell out of the stock. Thus, sitting pat might make the most sense if you own it.

Sell Mastercard?

If you are a value investor or an investor trying to maximize the income your portfolio generates, you’ll probably want to stay away from Mastercard today. If you have owned it for a number of years and benefited from the massive share-price advance, it wouldn’t be unrealistic to consider locking in some of the gains (even if you don’t close out the entire position).

But there’s another not-so-minor factor to consider here. Mastercard and Visa frequently find themselves battling with customers and regulators thanks to their dominance in the payment processing space. It is hard to track such disputes and they can result in large fines and potentially material changes in the business environment. For more conservative investors, such risks, which the company really can’t discuss in any detail while they are ongoing, might be enough of a reason to avoid Mastercard (and Visa, for that matter). It might also be enough to convince an investor with a big gain to take a profit and move on to a less exciting — and perhaps more attractively valued — stock.

Few easy answers with Mastercard

Mastercard is not a screaming buy, but also isn’t an obvious sell. Sure, there are some investors who will hate it, like dividend investors, but there are also some that might appreciate it, like growth-and-income types. All told, if you own Mastercard, it probably makes sense to keep it. If you don’t own it, you would probably do well to put it on your wish list.

Should you invest $1,000 in Mastercard right now?

Before you buy stock in Mastercard, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Mastercard wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Mastercard and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")