Brandon Bell/Getty Images News

The hotel industry plunged into its rock-bottom at the height of the pandemic. But three years later, the picture has completely changed. It has already regained its footing and is poised to accomplish pre-pandemic levels. It does not show a possibility of a slowdown amid macroeconomic volatility. Thanks to the resilient travel spending and changing work landscape that allow more people to make domestic and international trips.

Marriott International, Inc. (NASDAQ:MAR) enjoys a favorable tourism trend. It shows stable top-line growth and decent liquidity as it expands and builds more properties. Also, it has a solid market positioning with its huge operating capacity and efficiency. Even better, the stock has paid off over the years having the best returns since the Great Recession. It outperformed its close peers admire Hilton (HLT) and Hyatt (H). The current price also makes the stock an excellent buy.

3Q23 Performance

Marriott has already escaped the pandemic quicksand and remained a hotel giant. And today, it continues to dominate the market with its impressive top-line growth and sustained expansion. Thanks to revenge travel and the company’s prudent asset management.

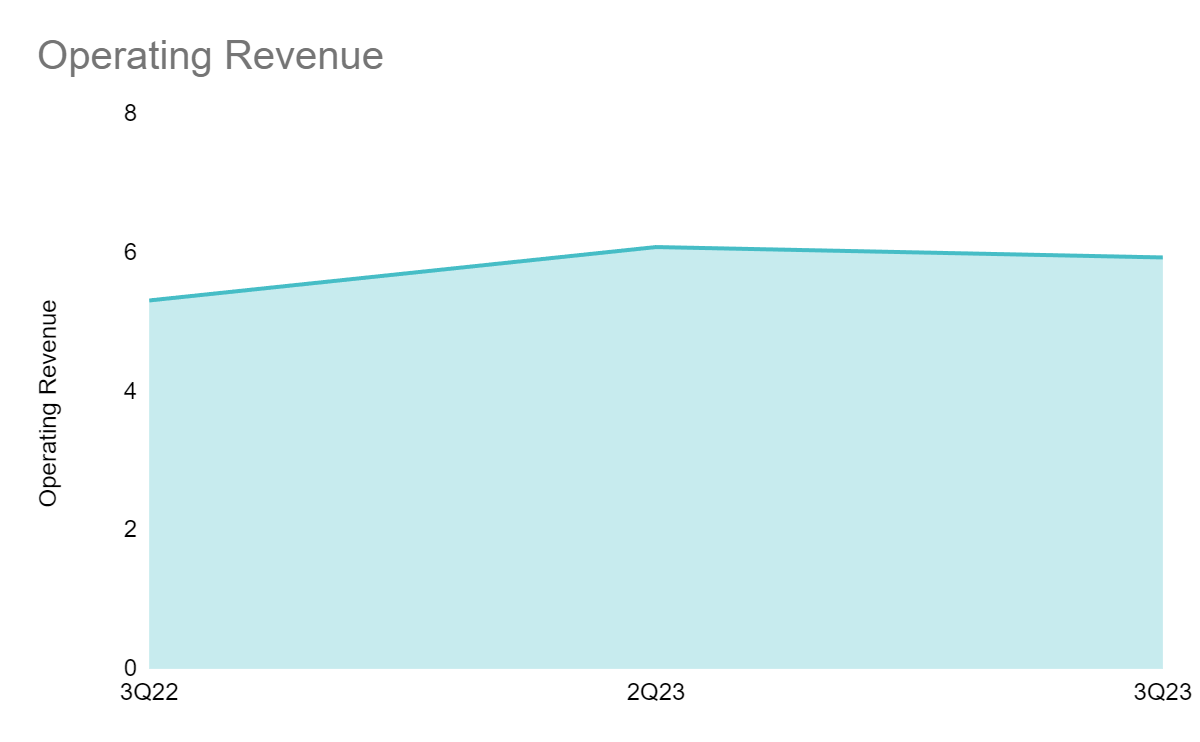

The total operating revenue for the third quarter reached $5.93B, a 12% YoY boost. QoQ growth inched down by 2.4%, which we can credit to the inflation uptick from July to September. This can be observed mainly in its US and Canadian markets. Yet, the opposite can be seen in its international market, particularly in Asia Pacific. In fact, its RevPAR in the region rose by 22%, driven by the sustained boost in the number of properties and occupancy and room rates. In only a year, the total number of its rooms worldwide increased by more than 70,000, bringing the total to 1,581,002. The boost was much higher than of its close peers namely Hilton and Hyatt. We will make a comprehensive comparison of these lodging companies in the next section. With its huge market presence and solid brand recognition, it has expanded its customer base domestically and internationally.

Operating Revenue (MAR 3Q Earnings Report)

Given this, discretionary spending, particularly on tourism, has been resilient. This was mainly driven by external factors other than the pent-up travel demand. Prudent economic policies, stable labor market conditions, and digital transformation were some factors.

First, macroeconomic improvements in the labor market have been visible. These have helped a lot of people withstand inflationary pressures. For instance, the unemployment rate in the US had an uptick in recent months. Yet, we can see it was primarily driven by the higher number of people entering and reentering the labor force. Most importantly, the average hourly wage in the US has risen continuously since its recovery from the pandemic. This helped many people with purchasing power, especially non-essential items and services. This fueled their desire to travel after being locked in homes for about a year.

Second, the labor market transformation has been very favorable for the tourism sector. The prevalence of remote work flexibility in businesses helped employees boost their travel frequency. Since 2022, its impact on the travel landscape has been evident. It increased hotel occupancy rates and improved flexibility with hotel booking rates. It was especially helpful for Marriott since its business model is mainly fee-based. It’s easier for MAR to adjust rates to demand and macroeconomic changes in contrast than a lease-based model. In a investigate, over half of American travelers spend more on travel than they did in the previous year. Regarding frequency, over 80% are traveling more often today than they did in 2022. Pandemic-driven revenge travel remains an essential factor since 29% of the respondents agree that their travel plans today are related to delays in the past three years. Another investigate reveals that 40.7% of full-time employees are working either remotely or hybrid. Unsurprisingly, the estimated number of Americans working remotely may accomplish 32.6 million by 2025. Hence, more and more people may preserve or boost their travel spending and frequency.

Third, cost pressures have started to ease as inflation decelerated to 3-4% from 9.1%. This reflects the successful action of The Fed to cushion the blow. While higher interest rates discouraged borrowings and investments, personal loans remained unfazed. More households used credit cards for their essential and non-essential spending admire leisure travel. And as the Fed Rate Hike Pause continues this holiday season, travel continues to boom. Hotels admire Marriott are once again encouraged to boost their capacity to accommodate more guests.

Given all these, Marriott is taking advantage of all market opportunities. As of 3Q23, its occupancy rate was already 72.1% compared to 68.9% in 3Q22. It was still much lower than in 3Q19 with 76.0% since the economy has yet to stabilize amid recession woes. The continued expansion of Marriott also contributed to the wide gap. With the continued travel uptrend and increased property construction of MAR, it is poised to fully recover by 2025. It still has a lot of growth drivers, which we will converse thoroughly in the succeeding parts.

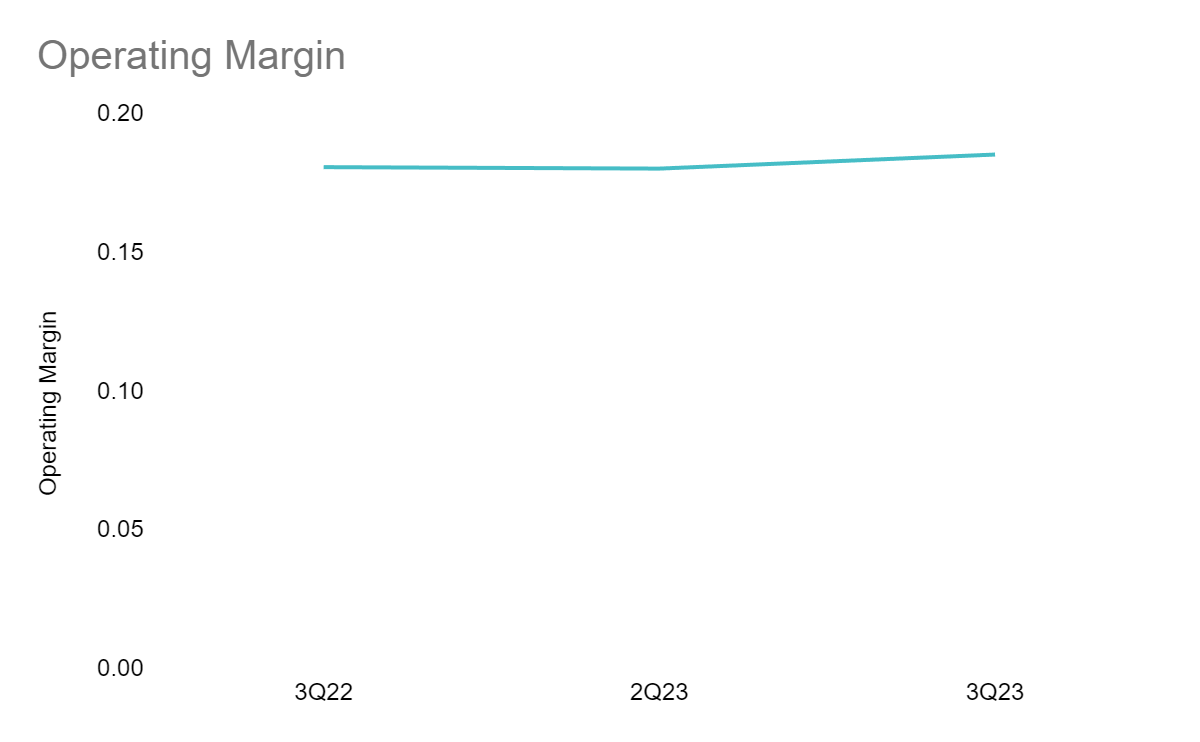

Even better, it kept costs and expenses reasonable relative to the continued expansion. MAR showed increased efficiency with easing cost pressures as it expanded. Its prudent and competitive hotel rates helped it cover and outweigh costs and expenses. Also, the slowing inflation helped it supervise variable costs better. In turn, the operating margin remained stable with a slight boost from 18.1% in 3Q22 and 18.0% in 2Q23 to 18.5% in 3Q23. Indeed, MAR enjoys solid top-line growth. As MAR increases its hotels and rooms, it has more upside in 4Q22 and the whole of FY24.

Operating Margin (MAR 3Q Earnings Report)

What Makes MAR So Solid

MAR has endured the blows of the pandemic recession, exacerbated by zero-tolerance restrictions. But over the next three years, it has regained its footing. Although it hasn’t reached pre-pandemic levels, the consistent uptrend is remarkable. It’s no surprise it is poised to complete its recovery in about a year or two. The important thing is that it continues to create high revenues while keeping costs and expenses manageable. This is an essential credit amid the still elevated prices and interest rates. These are some of the things I consider to say Marriott is a solid company.

Business Model

Cost reimbursements comprise 74% of Marriott’s total revenue, showing it uses a managed-based model. But in reality, the majority of its business runs a fee-based model. Over 70% of revenues are from base management, franchise, and incentive fees. To hinder confusion, you may read here to better grasp how cost reimbursement works for MAR. Cost reimbursement tends to understate MAR’s operating income. But it also gives a clearer picture of Marriott’s revenue generation from its franchisees, lessees, and customers and how it allocates it to employees.

I admire its fee-based model since this is very favorable for the company at this point. Tourism is booming. Revenge travel is resilient. More people are planning to travel next year. It is also flexible to macroeconomic and market changes. Since many of its hotels are under its management, it can easily adjust rates to market demand. Also, it is safeguard even during economic downturns since franchise fees are constant payments to MAR. It may vary depending on the revenue generated by its franchisees. This gives it an edge over many of its peers, primarily Hyatt. The latter has a greater concentration on lease revenues, which are relatively inflexible than fee revenues.

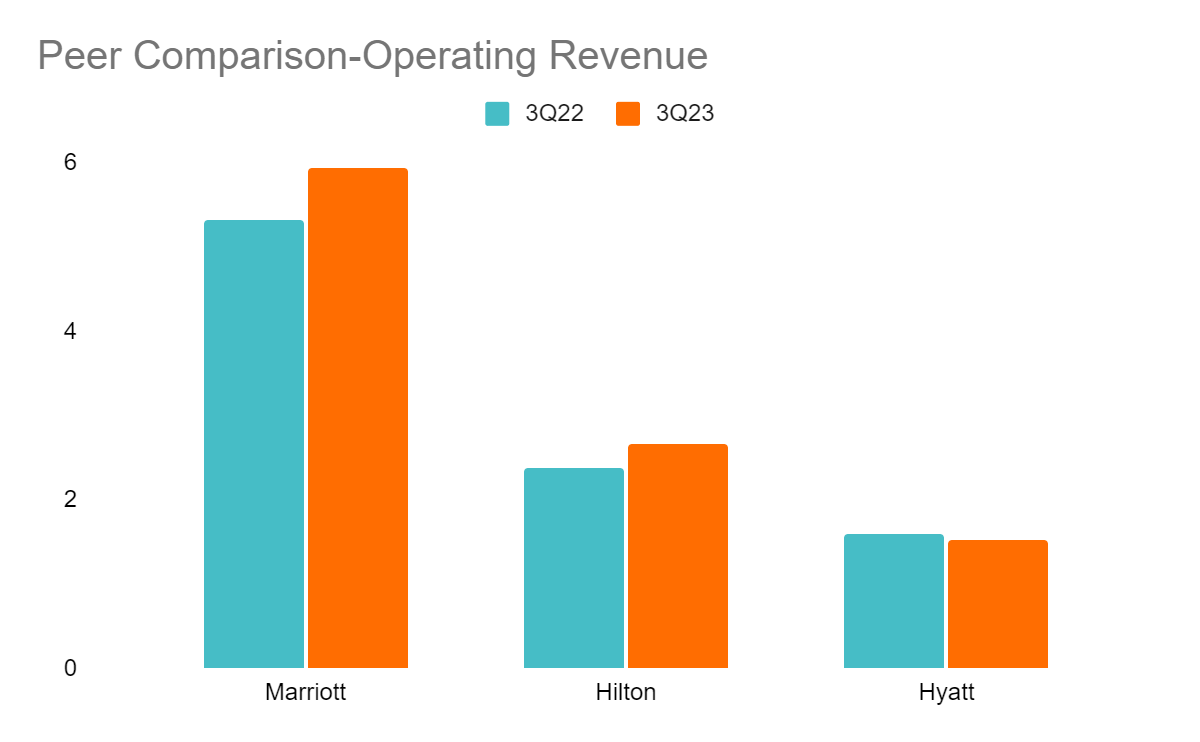

Meanwhile, Hilton also concentrates more on fees than leases. But if we get the percentage of their respective leases to revenues, MAR has only 6% while HLT has 13%. With that, MAR has more flexible revenue streams. We can see how advantageous a fee-based model is in their operating revenue. Both MAR and HLT had double-digit revenue growth in 3Q23, while Hyatt decreased by 5%. Hilton has a higher revenue boost of 12.7% versus MAR with 11.7%. Nonetheless, their actual revenue gap continued to widen. In 3Q22, MAR’s revenue was higher by $2.94B. In 3Q23, it rose to $3.26B. Indeed, MAR continues to dominate the hotel industry.

Peer Comparison-Operating Revenue (Earnings Report)

Solid Market Positioning

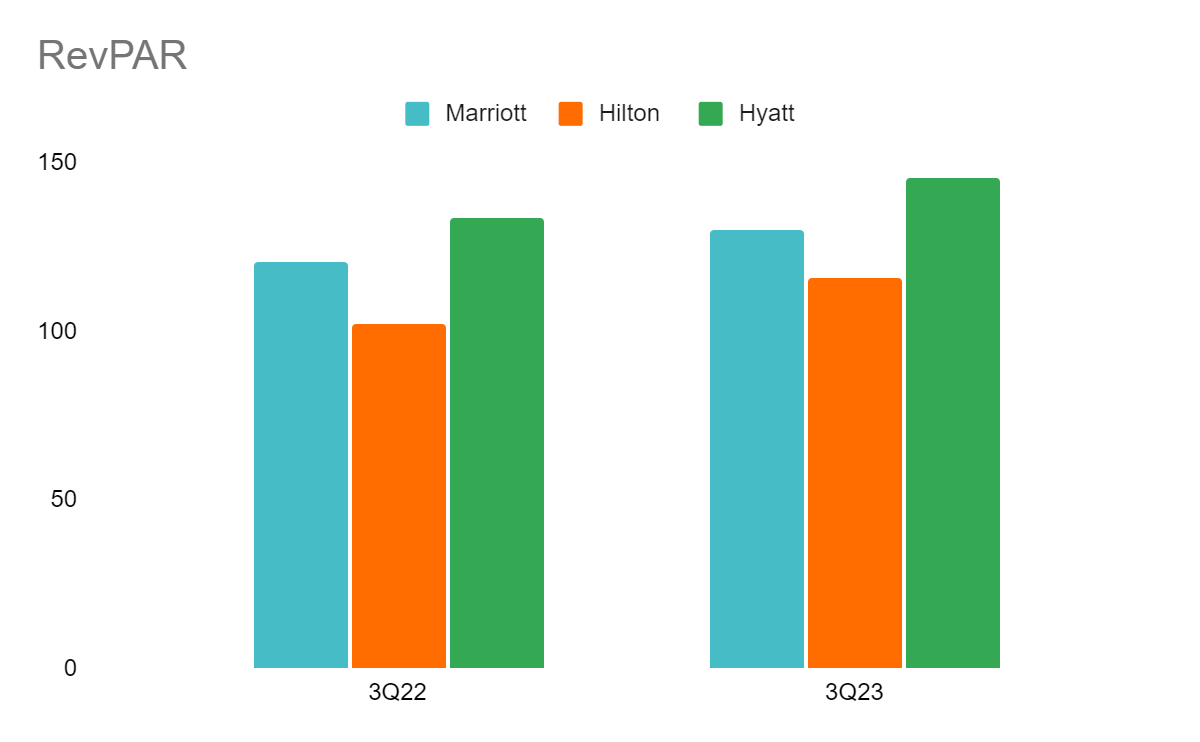

Marriott remains a formidable hotel with its fee-based model. But what makes it a durable giant is its sustained expansion and solid brand recognition. Its prudent pricing strategy on room rates allows it to vie even with smaller peers. We can see it in its impressive RevPAR growth. Its domestic growth was a bit slower than expected, but it rose by over 20% in Asia Pacific. It amounted to $129.73 and was higher than HLT with $121.37. Yet, both were much lower than H with $194, driven by its average daily rate. Even so, we must recollect that the difference in the available rooms between MAR and H is still over one million.

RevPAR (3Q Report)

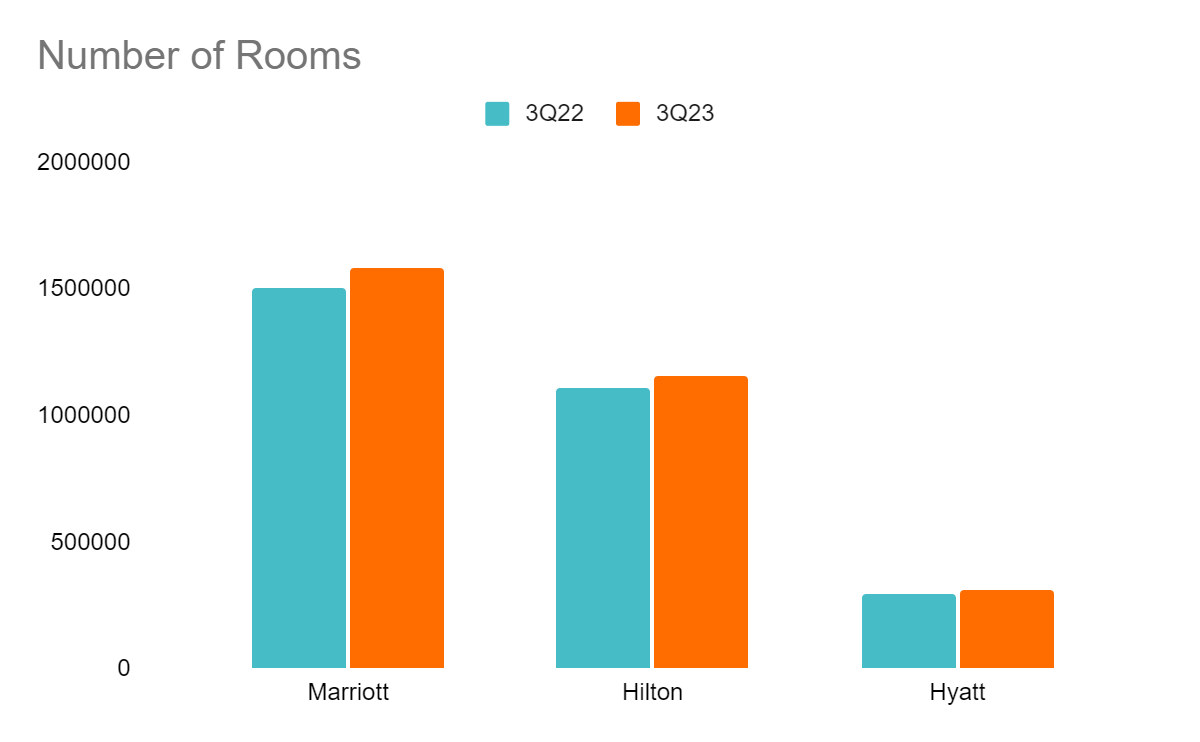

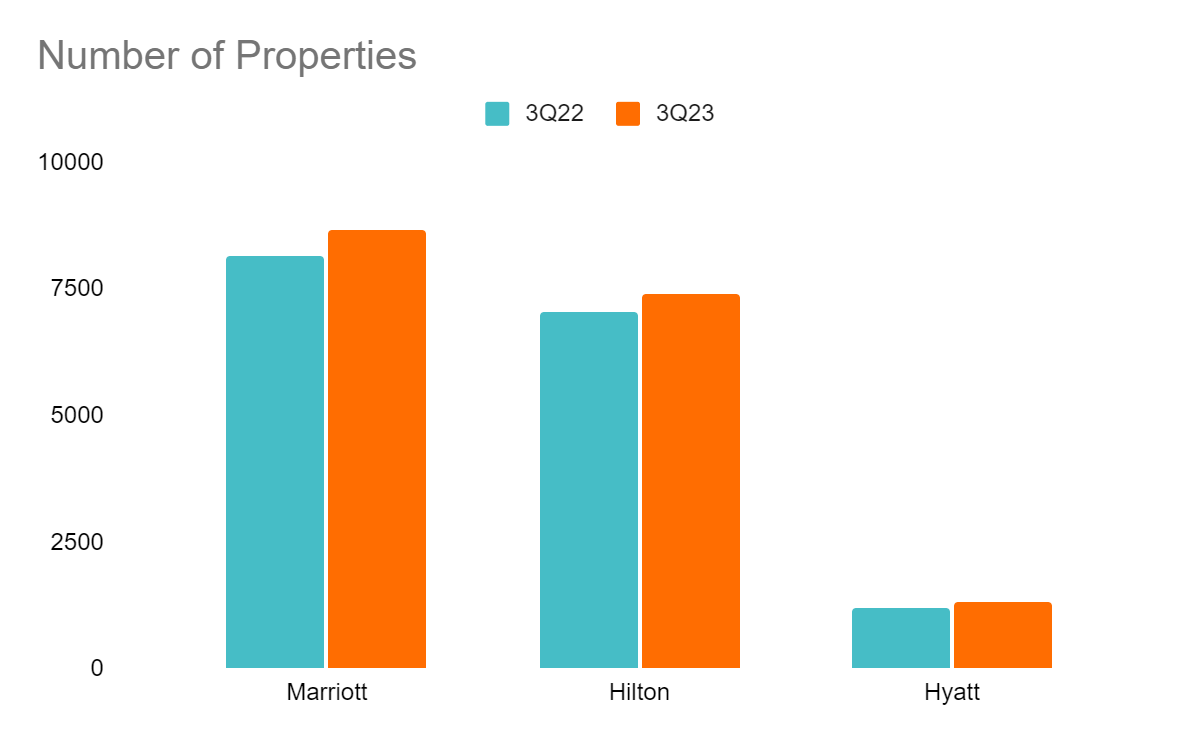

What makes MAR much ahead of the competition is its swift and sustained yet prudent expansion. It is a driving force toward growth as tourism recovers and returns to pre-pandemic levels. With the prevalent remote work setup, many employees can now go on vacation despite their busy schedules. MAR is ready after opening 73,652 new rooms. The total number of 1,581,002 is much higher than Hilton, with 1,159,783 (opened 48,636 new rooms), and Hyatt with 313,257 (18,369 new rooms). Its total properties are now 8,675 (built 503 new properties) versus HLT with 7,399 (built 338 new properties) and H with 1,310 (built 99 new properties). Hence, MAR has a much larger capacity to accommodate guests all over the world and create more revenues.

Number of Rooms (3Q Report)

Number of Properties (3Q Report)

Excess Liquidity

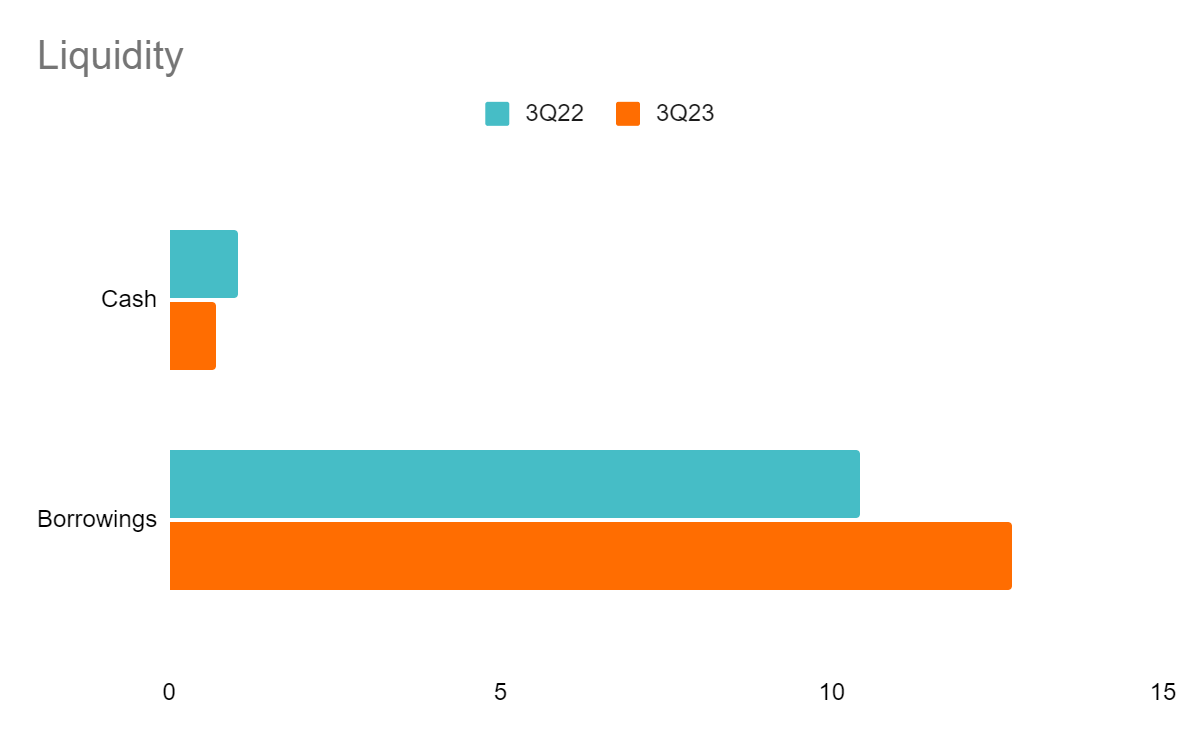

Marriott is a capital-intensive company, so liquidity is a crucial aspect to consider. Cash and borrowings substantially increased from 3Q22 to 3Q23. It can be discouraging at this point. Yet, we can credit it to its increased spending and leverage to cover its expansion. Also, interest rates are still elevated. On a lighter note, its EBITDA rose by almost 30%, showing that its expansion had been fruitful. With that, its Net Debt/EBITDA decreased from 2.67x to 2.64x, both lower than the maximum of 3.5x-4.0x. This shows the company is earning enough to cover borrowings in a short period.

Liquidity (MAR 3Q Earnings Report)

High Stock Price Returns

Over the years, the stock market has been through crests and troughs, and MAR is no exception. Despite this, MAR and the whole S&P 500 (SPX) showed resilience as the economy recovered. Even better, MAR has shown double-digit and better-than-market-average stock price returns. I compared the ten-year historical prices of MAR to HLT, H, and SPX. I assessed their performance using their actual returns and volatility using the Sharpe Ratio, Treynor Ratio, and Jensen’s Alpha.

By weighing their risks and returns, the three hotel stocks have outperformed the SPX. Even better, MAR remains the most solid stock with its impressive performance. As you can notice, MAR, HLT, and H have a negative Treynor Ratio due to negative beta. Their slope relative to the SPX is negative, so we can’t carry out which is the best stock among them. That is why I also used Jensen’s Alpha and proved that MAR was the best stock among the three hotels.

Some Growth Drivers

Hotels and other lodging properties have been experiencing a boom in the past three months. Despite the initial worries about recession, travel spending remains resilient. Primary growth drivers are the pent-up demand for travel fueled by hybrid work prevalence and credit card accessibility. Marriott enjoys this trend with its impeccable revenue growth. These drivers can help the company uphold its growth and expansion.

Winter Travel Demand and Decreasing Oil Prices

Winter travel expectations are still rosy even if the Summer and Autumn hype have already ebbed. The extremely cold weather does not seem to stop people globally from traveling this Winter. Various studies show that revenge travel is here to stay. One shows 83% of Americans planning to take at least one trip by the end of this year.

Another noticeable trend is that air travel is increasing faster than land travel. We can credit it to the decreasing fuel prices, which help stabilize airfares. Right now, the number of domestic travelers is seen to be up by 2.2% from December 23 to January 1. More specifically, the number of people traveling by air this holiday season will accomplish 115.2 million. While it is still lower than the 2019 peak of 119 million, recovery is now within accomplish.

In addition, the demand for RVs has decreased after RV prices skyrocketed. For a while, people have chosen campsites and domestic destinations to cope with inflation. But as inflation decelerated and the RV prices became less appealing, more travelers turned to other destinations. This is an opportunity for hotels as they also vie with RVs, which serve both for driving and lodging.

Artificial Intelligence to improve Efficiency and Customer Engagement

And now, artificial intelligence (AI) is becoming the crown jewel of many companies across different sectors. Even hotels are already seeing how AI can boost digital strategy, better system integration, improve efficiency to reduce costs, and accomplish out to more customers through social media and its more responsive web design. Marriott also embraces AI to personalize customer encounter. For instance, it has extended to social media using organic and paid social content to create potential customers. Collecting relevant email addresses and leveraging analytics are also part of it. AI can customize recommendations and offer more targeted services based on consumer behavior. It is often partnered with ChatGPT for better customer service and interaction.

More interestingly, Marriott uses AI algorithms to adjust room prices dynamically based on market demand and supply to boost revenues and occupancy rates. It helps the company keep room rates competitive while keeping its demand. MAR also uses AI to adjust staffing levels and assignments based on business needs.

Interest Rate Hike Pause

As inflation stabilizes again, the Fed has kept policy rates unchanged again. Given this, it is easier for people and businesses to pay their borrowings and attract investments. It is more crucial for MAR, given the high capital intensity. This can help the company keep or even boost its liquidity level. Also, people will be more confident about using their credit cards for non-essential spending admire travel amid holiday spending splurge.

Risk

Potential Inflation boost

Inflation has continuously decelerated from its 9.1% peak in June 2022. Despite this, policymakers are keen on the possibility of an inflation boost. Holiday spending splurges may drive this and may affect fuel prices. Also, fuel prices may be affected by the Winter demand. They must also keep watch of the Israel-Palestine War as the OPEC oil cuts remain a concern. If it persists, fuel prices may rebound and impact transportation and airfares. Although revenge travel remains solid, this may affect travel spending.

Vacation Rentals

Airbnb rooms are the primary competitors of the hotel industry. They cater to many backpackers and those who wish to lodge at a more manageable price. They can be predatory and work against hotels. Thankfully, MAR appears to be ahead of the competition as it has already started offering private home rentals in 2019. It is crucial to combine this niche to ensure the company can keep customer base.

Stock Price

The stock price of Marriott has increased over the years. Despite the sudden drop due to the pandemic and inflationary headwinds in 2022, the stock kept rebounding. It has stayed in an uptrend allowing investors to create returns. At $221.24, it has already risen by 43% in only a year. Investors may see the price a bit high to make a buy position. Yet, MAR still shows promising upside potential. These are supported by the key drivers and the impressive aspects discussed in the previous section. MAR still has room to enlarge and create more returns to uphold the stock price boost.

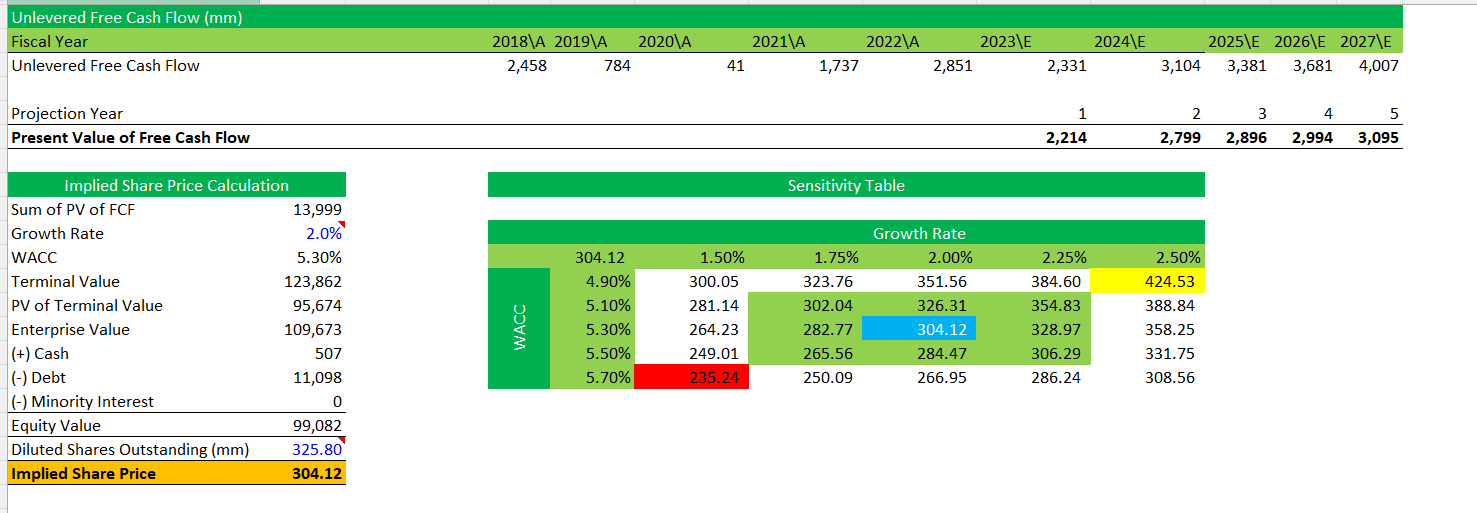

Its PE Ratio of 23.44x is also much cheaper than that of HLT at 35.79x and H at 28.98x. With that, MAR is still trading at a more reasonable price relative to its earnings. And to better appraise the stock price of Marriott, I used the DCF Model since MAR is capital-intensive. The DCF Model is a better method to scrutinize the intrinsic value of the company. I derived the growth rate in line with the target inflation of the US Fed. Also, I expect MAR’s revenue growth to standardize in the next five years. The double-digit growth shows MAR is still in its recovery phase toward pre-pandemic highs. Meanwhile, I derived the WACC by getting the debt and equity components using the Capital Asset Pricing Model.

DCF Model (Author Estimation)

The screenshot shows how I got the target price of $304.12. I also made a sensitivity table to show how the price will vary with the growth rate and WACC. We can see that the stock price remains undervalued regardless of the percentage. The target price shows that the upside potential of the stock price is still high by 36%, so MAR is still an excellent buy.

Key Takeaways

Marriott International, Inc. remains a formidable figure in the hotel industry. With its massive size and sustained expansion, it caters to a wide range of customers based on their preferences and capacity. It also maintains adequate liquidity to cover its business operations, dividends, and borrowings. Also, it has enticing growth drivers, which may allow MAR to create more revenues. Travel is still on its way to pre-pandemic peak, and its current trajectory shows MAR will accomplish it in no time. Even better, the stock price remains bullish and has many upside drivers. That is why I still suggest Marriott as a great buy.

Q2 2024 Earnings Call Transcript")