Isaac Lee/iStock Editorial via Getty Images

Stock Snapshot

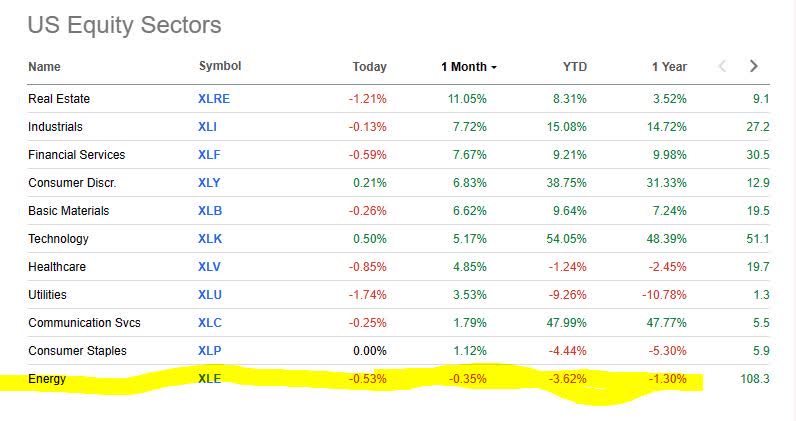

I want to highlight a tool called key market data on Seeking Alpha, which can tell me the performance of various sectors. In today’s research article, I will focus on a stock in the energy sector, which as of late has seen a slump on a year-to-date basis:

Marathon Oil – sector performance (Seeking Alpha)

As a segue into today’s research note, it is relevant to cite that oil prices have seen headwinds lately. Here is what financial portal Mint had to say this week:

Brent crude and US crude futures finished at a small loss following a see-saw session, in which prices fell more than $1 a barrel at one point on Friday, December 15, as traders tried to reconcile mixed signals for oil demand in the coming year.

With that said, my focus stock today is Houston-based Marathon Oil (NYSE:MRO), who also saw its share price drop recently.

Some quick facts about this company are that it trades on the NYSE, calls itself an independent exploration and production company, and has a 50% oil and 50% gas/NGL production mix.

The question I want to answer is whether it is time to scoop up oil stocks right now?

Scoring Matrix

This article uses a 9-point scoring matrix that holistically considers multiple angles of the stock, with an emphasis on dividend-income potential for investors and fundamental trends from the key accounting statements such as the balance sheet and income statements, as well as a future-looking outlook on this stock.

I continue to evaluate this methodology in my own portfolio, on stocks I don’t cover here, and it is my standard for building a long-term dividend-income portfolio that grows each year. So, I personally have a capital stake in this approach being successful.

Today’s Rating

Marathon Oil – score matrix (author analysis)

Based on the score total in the score matrix above, this stock is getting a rating of buy.

Compared to the consensus rating on Seeking Alpha, which seems bullish, I am going to agree with the bullish sentiment shown below:

Marathon Oil – rating consensus (Seeking Alpha)

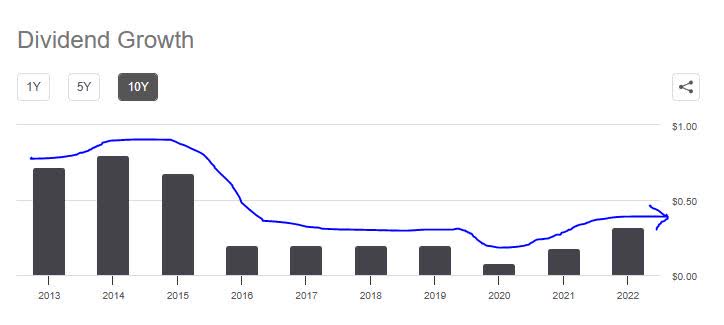

Dividend Income Growth

This section uses dividend growth data to explores the 10 year dividend income growth for a hypothetical investor owning 100 shares, to execute whether this stock is a great dividend income opportunity.

Marathon Oil – 10 year dividend growth (Seeking Alpha)

Using the chart above, if we bought 100 shares in 2013 we would have seen an annual dividend of $0.72 ($72 annual dividend income). By 2022, however, it would have dropped to an annual dividend of $0.32 ($32 income), for a 10-year refuse of 56%.

We can see from the dividend history that the 2023 levels are $0.41 annual dividend, a 28% growth from 2022. If it continues to grow at this pace of $0.08/year, it will take around 8 years just to get to the 2013 dividend level.

In this category, I will call it a hold, because although the company is showing dividend growth again, it is essentially just making up for the refuse in the last decade.

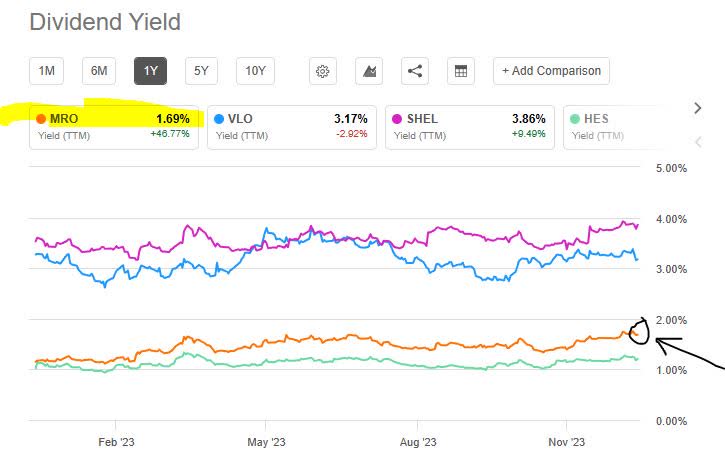

Dividend Yield vs Peers

This section uses dividend yield data to contrast the trailing dividend yield vs 2 or 3 similar peers in the same sector, to execute if this stock presents the most competitive dividend yield on capital invested.

Marathon Oil – div yield vs peers (Seeking Alpha)

In the chart above, I am comparing my focus stock Marathon vs three large peers in the oil and gas sector. These include Valero Energy (VLO), Shell (SHEL), and Hess (HES). Some of my readers may recollect those “Hess truck” toy commercials back in the 1990s on TV, around the holiday season, so I may as well include that stock here to be seasonally relevant.

In this peer group, Shell leads the pack with a trailing dividend yield of 3.86%, with Hess coming last. Marathon is next to last at 1.69% yield (1.81% forward yield).

In this category, I would not call it a great buy at this yield below 2% if I can get a much better one in this sector as the evidence shows, and a payout of $0.11/share is not much to write home about, considering the size and scope of this company. So, I call this a hold.

Revenue Growth

This section explores this company’s revenue growth trends over the last year, using data from the income statement.

What we can learn from this data point is that in Q3 results the firm saw total revenue of $1.77B, vs $2.00B in Sept 2022, a 13% YoY refuse.

Although the company did not really specific the drivers of the YoY revenue refuse, looking forward towards 2024 they had lots of positive sentiment in their Q3 presentation and earnings release.

According to CEO Lee Tillman in the presentation:

Looking ahead to 2024…our commitment to our Framework for Success remains steadfast. We’ll continue to prioritize strong corporate returns on every dollar we invest while striving to deliver peer-leading free cash flow generation, return of capital to shareholders, and per-share growth.

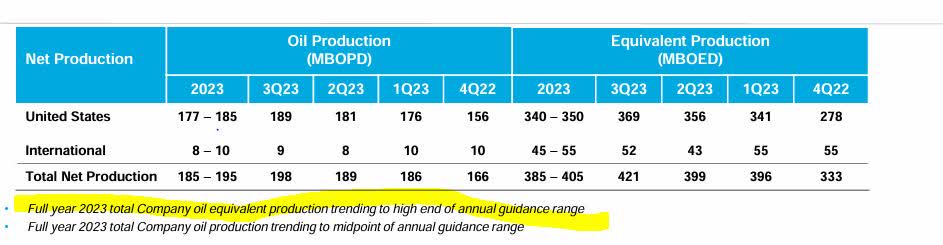

We can also see evidence that oil production has grown and remains strong going into Q4:

Marathon Oil – net production (company Q3 results)

Also notable to cite that might boost the top line is that the company “signed TTF-linked LNG sales agreement expected to drive significant 2024 E.G. financial uplift.”

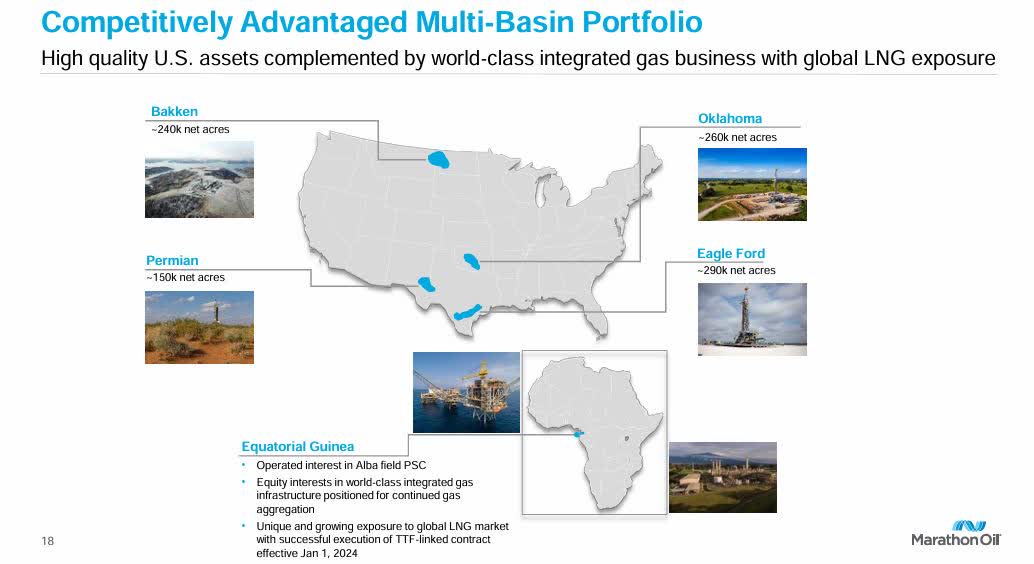

The company also has a diversified exposure across multiple wells in multiple geographic areas in both America and Africa:

Marathon Oil – diversification (company q3 results)

In this category I would call it a hold on the basis of declining revenue numbers offset by strong production outlooks and well diversification.

Earnings Growth

This section explores this company’s earnings (net income) growth trends over the last year, also using data from the income statement.

In this data point, we can see that earnings/net income was down to $453MM in Q3, vs $817MM in Sept 2022, an 80% YoY refuse.

One driver of increasing costs I found is increasing interest expense, which went up to $94MM in Q3 vs $52MM in FY2022Q2.

Operating expenses jumped up only slightly on a YoY basis, going from $703MM to $782MM.

I will call it a hold here too because of declining earnings figures along with rising interest costs, in a high interest rate environment. However, with Fed rate cuts potentially coming in 2024, that could benefit their bottom line if that eventually materializes, so I believe that should boost earnings in 2024.

Equity Positive Growth

This section explores this company’s equity (book value) growth trends over the last year, using data from the balance sheet.

From this data point, we can gather some better news such as that equity grew to $8.69B in Q3 vs $6.67B in Sept 2022, a +30% YoY growth.

This is despite the rise in long-term debt and total liabilities. A driver of this result seems to be YoY growth in total assets, particularly a $3B enhance to property/plant/equipment.

This category is a buy, on the basis of positive equity growth. Also, evidence of capital strength of this company shows: “shareholder distributions through the first three quarters of 2023 include $1,121 million of share repurchases and $186 million in base dividends.

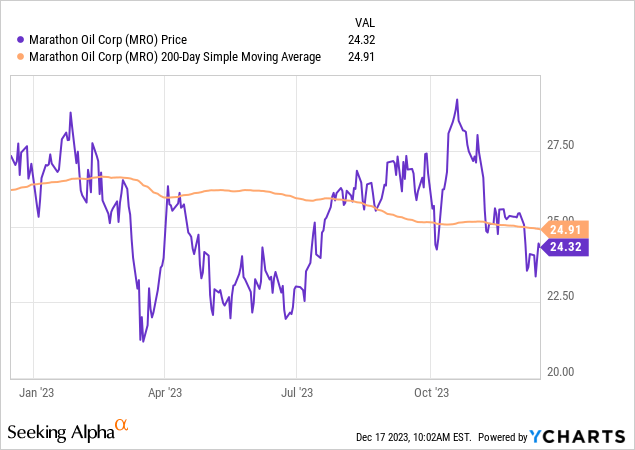

Share Price vs Moving Average

This section uses the YCharts tool to examine the current share price compared to the 200-day simple moving average, to infer if it currently presents a buy, hold, or sell opportunity. The 200-day SMA is my standard long-term trend indicator I prefer for its simplicity and smoothing out the price movement.

At first glance, the share price of $24.32 (Friday’s market close) is trading around 2.3% below the 200-day SMA.

I will call this a buy and here is why I think it presents a dip opportunity. It is severely down from its autumn highs that were trending around $28, which I think is driven by bearishness in the energy sector as I already mentioned.

Although it is a not a great dividend yield opportunity right now, and revenue as well as earnings have been sluggish, I think that this bearishness in the energy sector could be an opportunity to pick up some shares in an established energy-sector stock appreciate this, with a strategy of oil prices going up in 2024 and pushing these shares up.

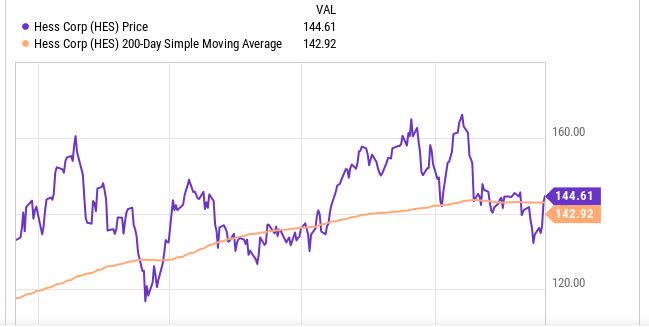

Consider that its peer Hess is also trending around its moving average right now, after its recent dip:

Hess – YCharts (Seeking Alpha)

Valuation: Price-to-Earnings

This section uses valuation data to examine the forward P/E ratio and whether it presents an undervaluation opportunity or appears overvalued.

What this data story tells us is that the forward P/E ratio is 9.02 right now, around 13% below the sector average.

Tying this multiple of 9x earnings back to the financials and share price already talked about, seems the data shows a highly bearish share price but also sluggish earnings. I think this multiple is justified and presents a buy opportunity because even though earnings saw declines so did the share price, which is trending below its long-term moving average.

advance, if interest expenses come down in 2024 and earnings boost, that could furnish a boost to the earnings side of this multiple.

Valuation: Price-to-Book Value

This section uses valuation data to examine the forward P/B ratio and whether it presents an undervaluation opportunity or appears overvalued.

The data shows a forward P/B ratio of 1.29, or +21% below the sector average.

Tying back to the equity discussion, and share price, I would call it a buy at this multiple of 1.29x because while the share price showed bearishness the equity has improved, so for a cheaper share price I am getting a company with improved book value.

Risk Analysis

This section identifies a key risk to consider about this company and what its probability and impact could be to the business.

The risk I want to briefly converse is oil prices and potential impact to this company and shares.

A USA Today article on Dec. 16th is calling for lower gas prices in 2024:

Experts hope for even more stability in 2024, with fuel prices starting lower and staying lower than in 2023.

However, they went to describe this not as a major slump to the industry but rather a return to normalcy after recent years:

Pump prices fell dramatically in pandemic-plagued 2020, recovered in 2021 and spiked dramatically amid the Ukraine invasion and runaway inflation of 2022.

By comparison, 2023 has unfolded somewhat more predictably at the pump, despite lingering inflation and war in the Middle East.

Goldman Sachs in its Nov. 29th analysis predicts a drop in oil demand but also a potential spike in prices due to supply issues caused by geopolitical conflicts in the Mideast still ongoing:

The forecast reflects slowing oil demand growth arising from tighter financial conditions and still elevated US recession odds over the coming year.

If the war escalates, spot oil prices may encounter sharp but transitory prices increases. Potential oil supply disruptions from the war include tighter oil sanctions on Iran, Iran retaliating by attempting to block the Strait of Hormuz (a shipping passage which accounts for approximately 20% of global oil supplies), an Arab oil embargo, and other Arab producers cutting back on production.

In this case, I will call this stock a buy on the basis of a modest/mixed risk since we could see upside from these oil/gas companies if global oil supplies get squeezed. I am not sure also that the drop in demand will actually materialize, especially if we see a very busy spring/summer travel season. As I have written recently in my coverage on Delta Air Lines (DAL) where I was bullish, growth in travel demand has shown itself and airline stocks appreciate this one have been surging, and airlines obviously are dependent on oil/gas to function.

Quick Summary

To summarize, I am going bullish/long on Marathon Oil today because I see a nice buy opportunity to add some energy-sector stocks to a portfolio, while share prices are trending below the moving average.

Other positives are strong production outlooks, equity growth, and a rebound in dividend income growth after a slump. We also see nice valuation metrics on this one too.

The key risk is what will happen to oil prices in 2024, and from the evidence I see upside potential for this stock driven by stable demand for oil/gas combined with potential supply shocks due to geopolitical issues, a scenario we have seen many times before.

Q2 2024 Earnings Call Transcript")