Thomas Brown/DigitalVision via Getty Images

Investment Thesis: I continue to rate MakeMyTrip as a buy at this time.

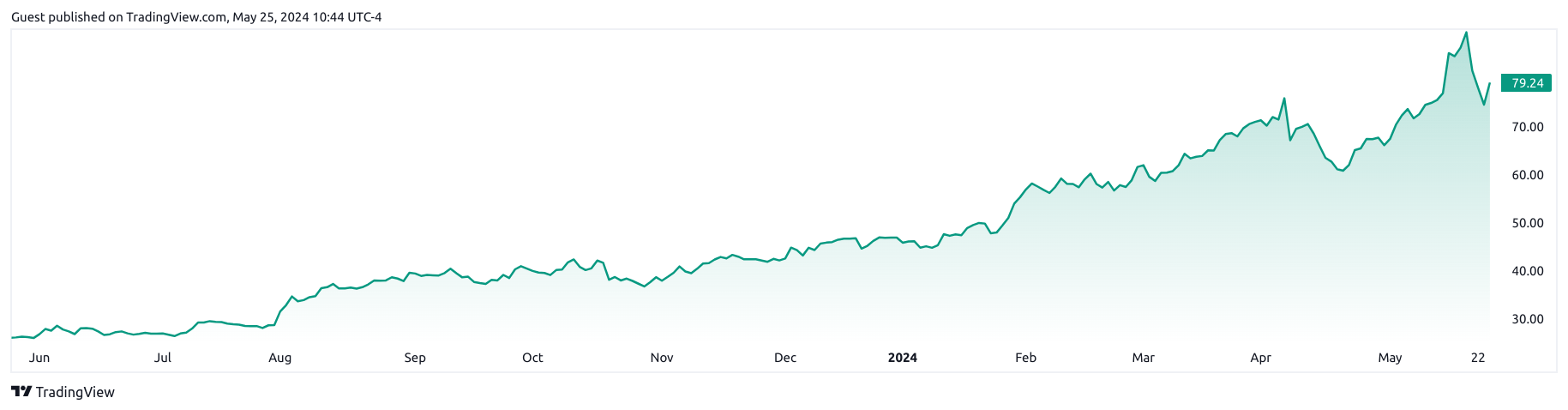

In a previous article back in February, I made the argument that MakeMyTrip Limited (NASDAQ:MMYT) could have upside potential to a $77 target price based on continued sales growth, but that I would still be monitoring growth in customer inducement costs across the Hotels and Packages segment.

ycharts.com

Since then, the stock has exceeded this target price – up by over 35% from my last article and trading at $79.24 at the time of writing.

The purpose of this article is to assess whether MakeMyTrip has the prospect for further upside from here.

Performance

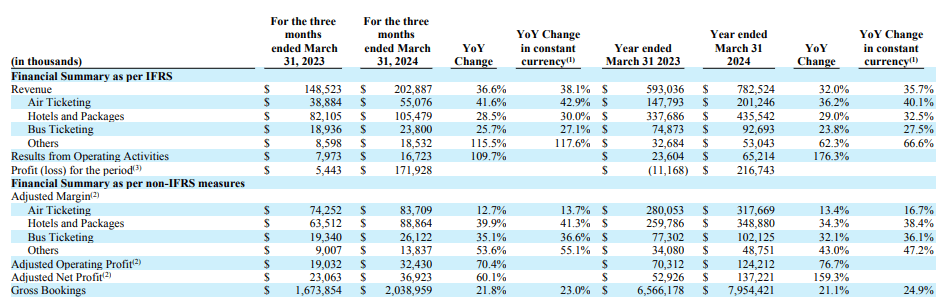

When looking at Q4 and FY 2024 results, we can see that revenue is up by 36.6% as compared to the prior year quarter, and up by 32% on a yearly basis:

MakeMyTrip Limited: Q4 and Full Year Earnings Release

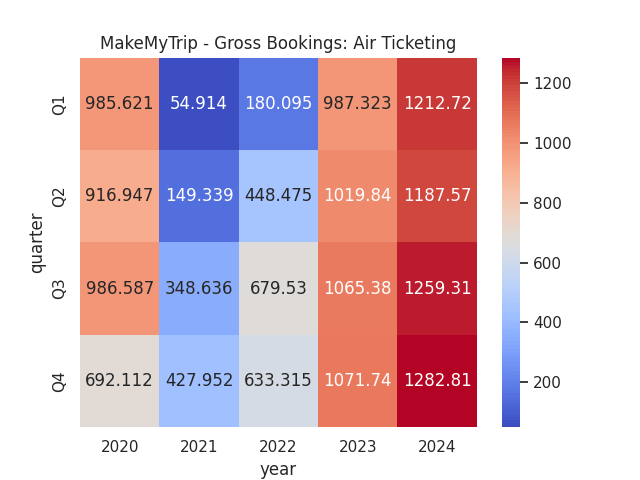

In terms of gross bookings for Air Ticketing, we can see that the same is up by 19.7% as compared to the prior year quarter, and 1.9% as compared to Q3 2024.

Figures sourced from previous MakeMyTrip Earnings Releases (Q1 2020 to Q4 2024). Figures provided in USD millions. Heatmap generated by author using Python’s seaborn visualisation library.

I had previously stated that I would be monitoring whether MakeMyTrip could ultimately bolster revenue growth across the Hotels and Packages segment while also reducing the rate of growth in customer inducement costs. With growth of 28.5% in Hotels and Packages revenue as compared to the prior year quarter, and 29% year-on-year – we have seen encouraging growth across the segment.

With respect to customer inducement costs, we can see that on a three-month ended basis, costs for Hotels and Packages grew by 42% and accounted for 30% of revenue in Q4 2024 as compared to the prior year quarter.

MakeMyTrip Limited: Q4 and Full Year Earnings Release

When looking from a yearly standpoint, we see that customer inducement costs are up by 36%, with costs now accounting for 28% of revenue as compared to 27% for the previous year.

MakeMyTrip Limited: Q4 and Full Year Earnings Release

My initial reason for expressing concern on customer inducement costs for Hotels and Packages was that the segment had been showing lower revenue growth as compared to other segments, at 21.5% for Q3 2024 as compared to the prior year quarter.

However, with Hotels and Packages revenue up by 29% for Q4 2024 as compared to the prior year quarter – I take the view that a rise in customer inducement costs is tolerable given that we are seeing growth in revenue as a result.

Risks and Looking Forward

My view on the above results is that the higher rate of growth we have been seeing across Hotels and Packages revenue is encouraging, and in spite of my prior reservation over higher inducement costs – the fact that we are seeing higher revenue growth justifies higher costs in the short to medium-term.

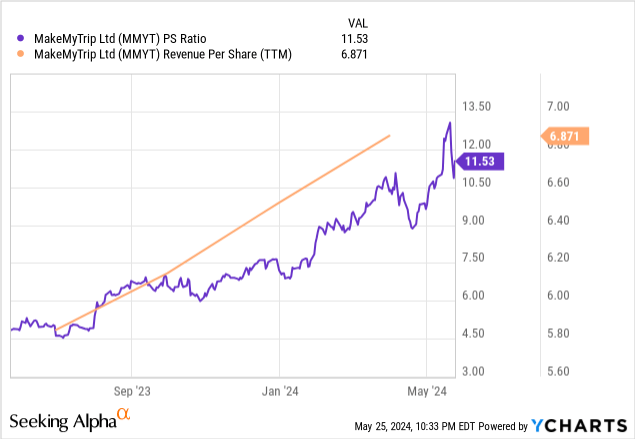

I had previously expressed my view that given a price to sales ratio of 8.646x for the stock back in February, we could see fair value of $77 for the stock if revenue per share continues to grow back to previous highs of $9 ($9 revenue per share * 8.646x P/S ratio = $77.81). Revenue per share at the time was trading at $6.519.

Since then, we have seen that the PS ratio has risen by 33.36%, while revenue per share is up by 5.40%.

Price to Sales Ratio

ycharts.com

From this standpoint, we can see that the growth in the price to sales ratio is significantly outpacing growth in revenue per share. In this regard, I take the view that the stock is trading at fair value at this time.

Going forward, I see MakeMyTrip as having the capacity to continue growing revenue across the Hotels and Packages segment – particularly given India’s strong domestic travel market. For instance, weekend getaways continue to increase in popularity and popular travel destinations such as Jim Corbett have seen 131% search growth. Moreover, spiritual tourism has also been seeing growth – with a 97% increase in searches on the platform over the last two years.

While I had previously expressed concern that MakeMyTrip might see a slowdown in revenue outside of the October to March high season for international travel to India, the country as a whole benefits from a strong domestic travel market, and for this reason I anticipate that we could continue to see strong revenue growth going forward.

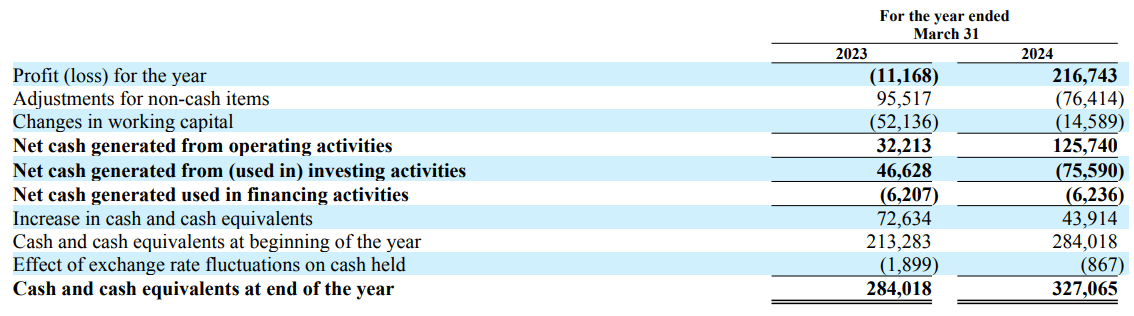

In terms of potential risks, it is notable that short-term loans and borrowings have increased substantially from USD 15.65 million in March 2023 to USD 216.818 million in March 2024 – due to non-current loans and borrowings having come due.

MakeMyTrip Limited: Q4 and Full Year Earnings Release

While the revenue growth we have seen has been encouraging, investors will be looking closely to determine whether the company has the capacity to service its short-term debt while continuing to invest in further revenue growth.

That said, we can see that the company has significantly grown cash and cash equivalents by 15% over this period – which indicates that the company is in a healthy financial position and has the capacity to service its current liabilities.

MakeMyTrip Limited: Q4 and Full Year Earnings Release

Conclusion

To conclude, MakeMyTrip has seen encouraging revenue growth and the increase in domestic tourism has been encouraging. I take the view that the stock is fairly valued at this time, but has the potential for longer-term upside given strong performance across the Hotels and Packages segment, as well as continued growth in domestic tourism.

Q2 2024 Earnings Call Transcript")