wildpixel

The Company

MacroGenics, Inc. (NASDAQ:MGNX) is a $526-million market cap biopharmaceutical company based in Maryland that focuses on developing and selling antibody-based treatments for cancer. Their approved product, MARGENZA, is used with chemotherapy to treat metastatic HER2-positive breast cancer. They also have a pipeline of other potential cancer treatments in development. MGNX also works on therapies for autoimmune diseases and has collaborations with other biopharmaceutical companies.

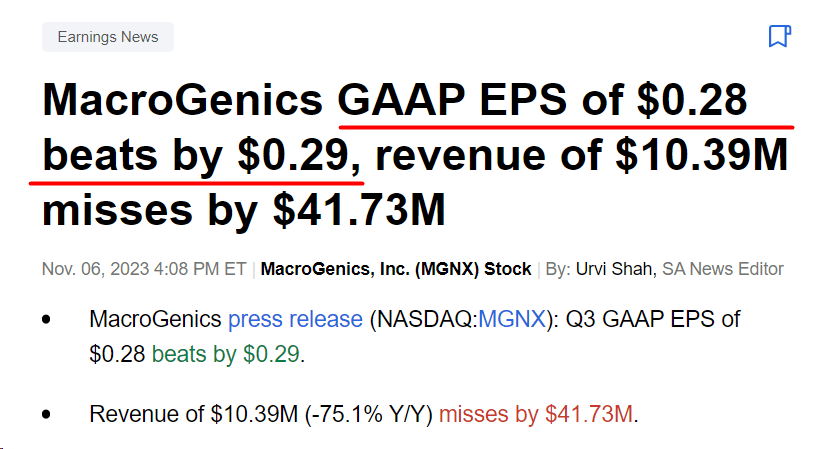

In Q3 2023, MacroGenics reported a total revenue of $10.4 million, down from $41.7 million in Q3 2022 due to a $30 million revenue recognition in the previous year. The revenue included $4.5 million in contract manufacturing and $4.7 million in MARGENZA net sales. Despite this reject, the company’s GAAP earnings per share amounted to $0.28, compared to a loss per share of $0.4 in the same period last year, beating the consensus by a wide margin:

Seeking Alpha News, author’s notes

MGNX’s R&D expenses decreased to $30.1 million (-37.5% YoY), and SG&A expenses decreased to $12.4 million (-19.2% YoY). This in itself is not a reason for the EPS growth mentioned above. The company received a $50 million milestone payment from Sanofi, resulting in a net income of $17.6 million, compared to a net loss of $24.8 million in Q3 2022.

MGNX’s 10-Q, author’s notes

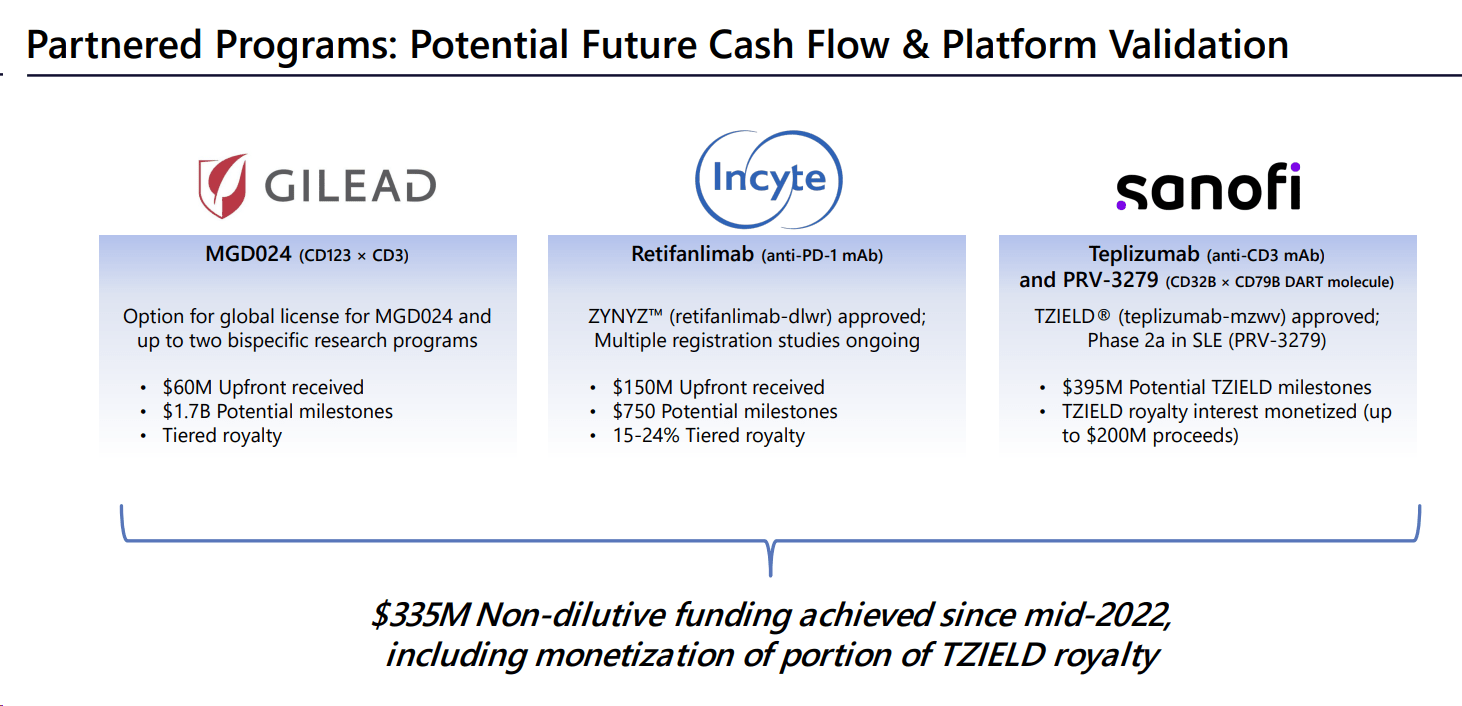

In general, MacroGenics has collaborations with Incyte (INCY), Gilead (GILD), Zai Lab, and Provention (now Sanofi’s subsidiary). These collaborations have brought significant non-dilutive funding to MacroGenics, including upfront payments and milestone achievements. For instance, the collaboration with Incyte has resulted in an upfront payment of $150 million and potential milestone payments of up to $650 million. The collaboration with Gilead includes a non-refundable upfront payment of $60 million and potential payments of up to $1.7 billion. The Zai Lab collaboration involves an upfront payment of $25 million and potential milestones of up to $140 million. Additionally, the collaboration with Provention could bring in up to $395 million in milestone payments. These collaborations contribute to MacroGenics’ financial position and maintain its ongoing research and development efforts.

MGNX’s IR materials

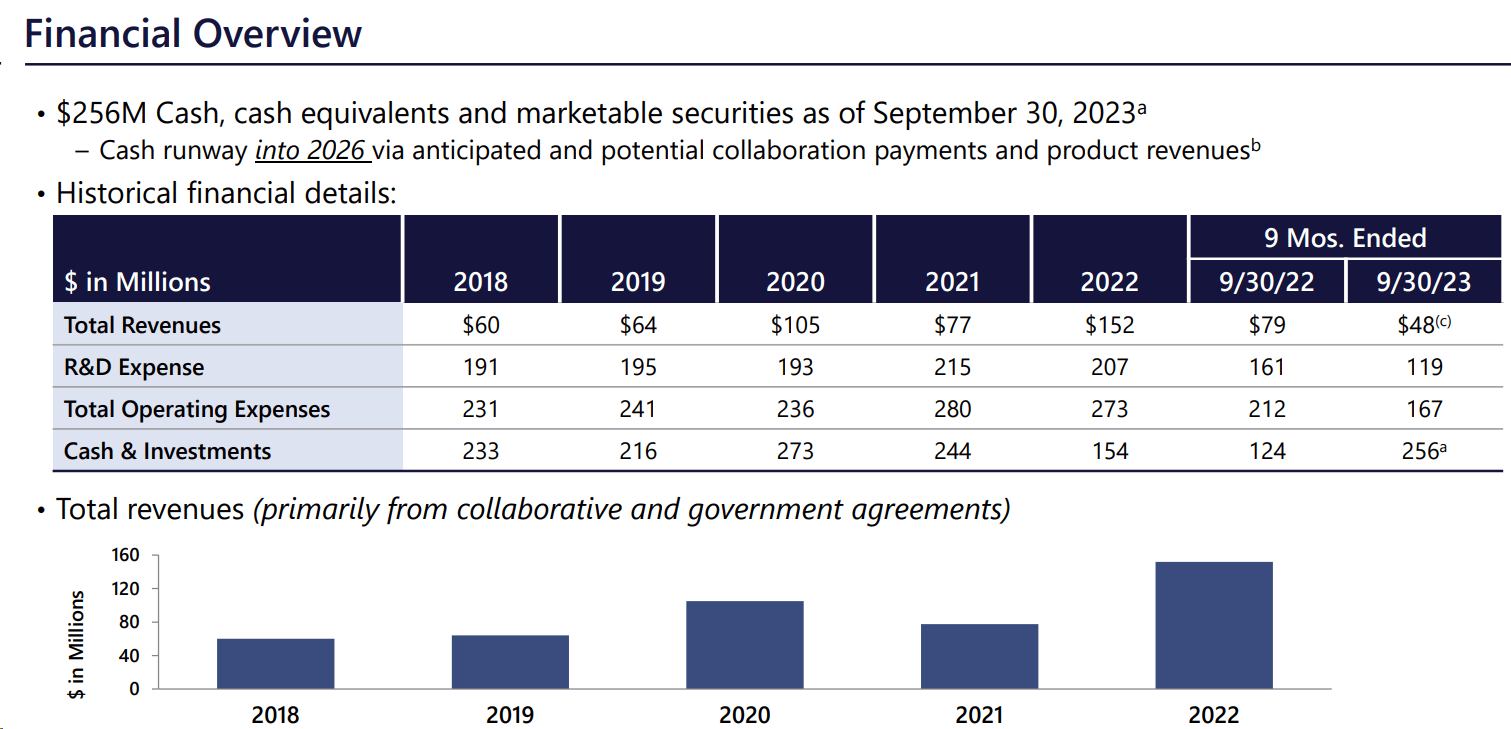

As of September 30, 2023, the cash balance was $256.4 million, expected to fund operations into FY2026, according to the management’s commentary. From a liquidity perspective, MGNX’s financial position looks more than solid – the company will not have to seek advance rounds of investment on unfavorable terms that severely dilute the stake of existing shareholders, which is very good for any small-cap company in the industry.

MGNX’s IR materials

MacroGenics has also provided updates on its key investigational drug programs, showcasing promising advancements. Vobramitamab duocarmazine (vobra duo), an antibody-drug conjugate targeting B7-H3, is in a crucial TAMARACK Phase 2 research for broad tumor applications. Lorigerlimab, identified as a dual-targeting DART molecule, exhibits early promise in metastatic castration-resistant prostate cancer, with an upcoming Phase 2 research anticipated. MGD024, an innovative bispecific drug, is rigorously tested for hematologic malignancies. Enoblituzumab gears up for a Phase 2 research in early 2024, emphasizing its potentially transformative impact on prostate cancer treatment. These updates highlight MacroGenics’ ambitious approach to addressing unmet needs within the competitive landscape of oncology therapeutics.

So with ‘secured financing’ for several years, a strong pipeline, and already solid collaborations with major healthcare companies, the future of MGNX looks promising.

But what about the stock’s valuation?

The Valuation & Expectations

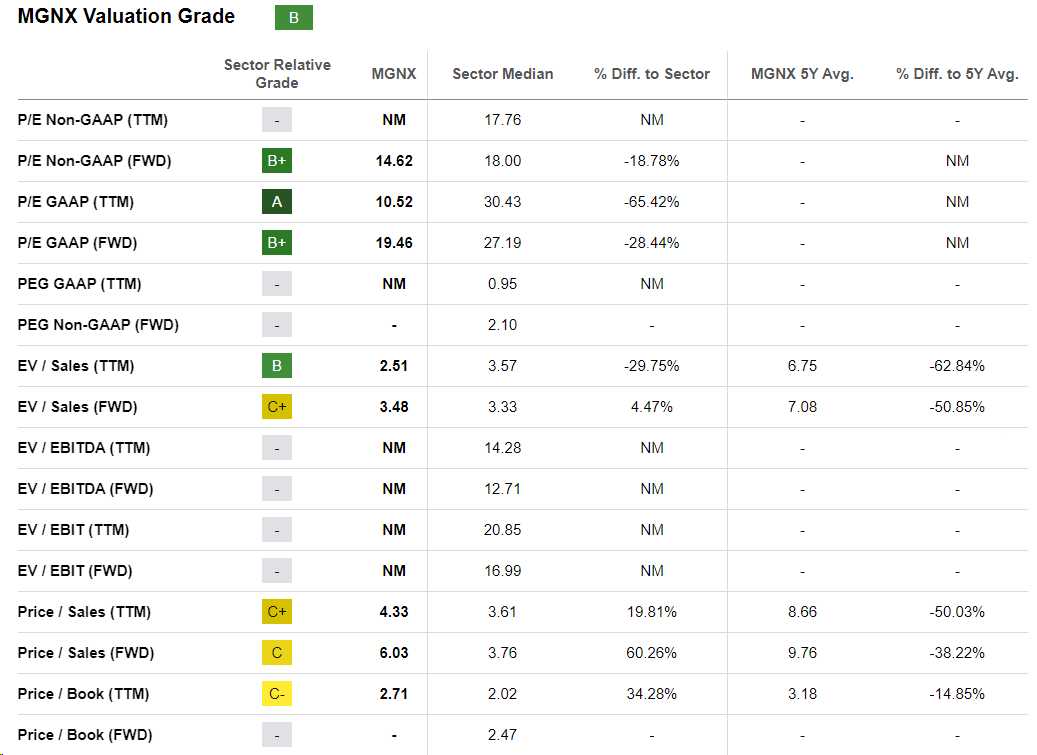

According to Seeking Alpha Quant System, MGNX has a ‘B’ rating, which is solid compared to most other names in the sector. However, the next-year price-to-sales ratio looks quite high:

Seeking Alpha, MGNX’s Valuation

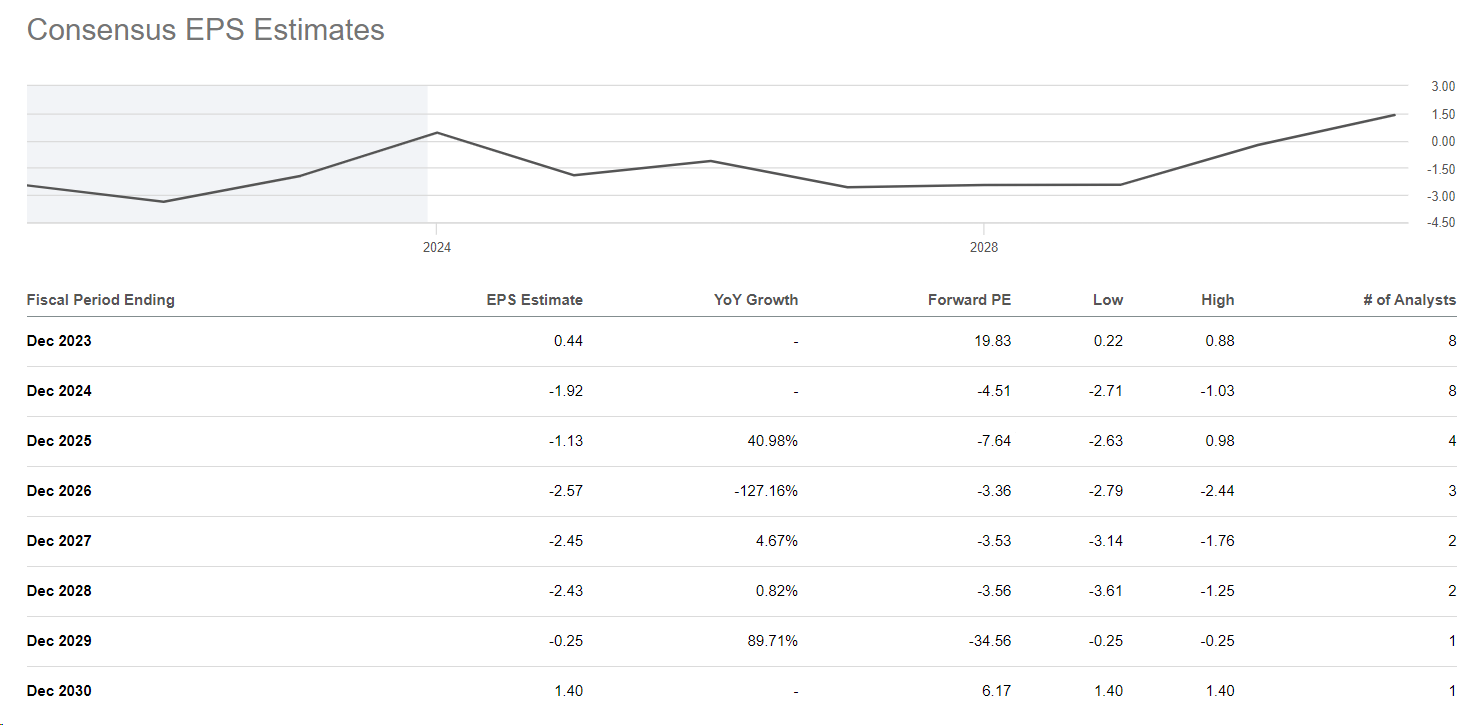

Due to the company’s rather unstable sales and profit structure, analysts can apparently only include R&D activities and results for the distant future in their forecasts – which is why the EPS estimates for FY2023 look admire a one-off event amid the next few years of deep losses:

Seeking Alpha, analysts’ estimates

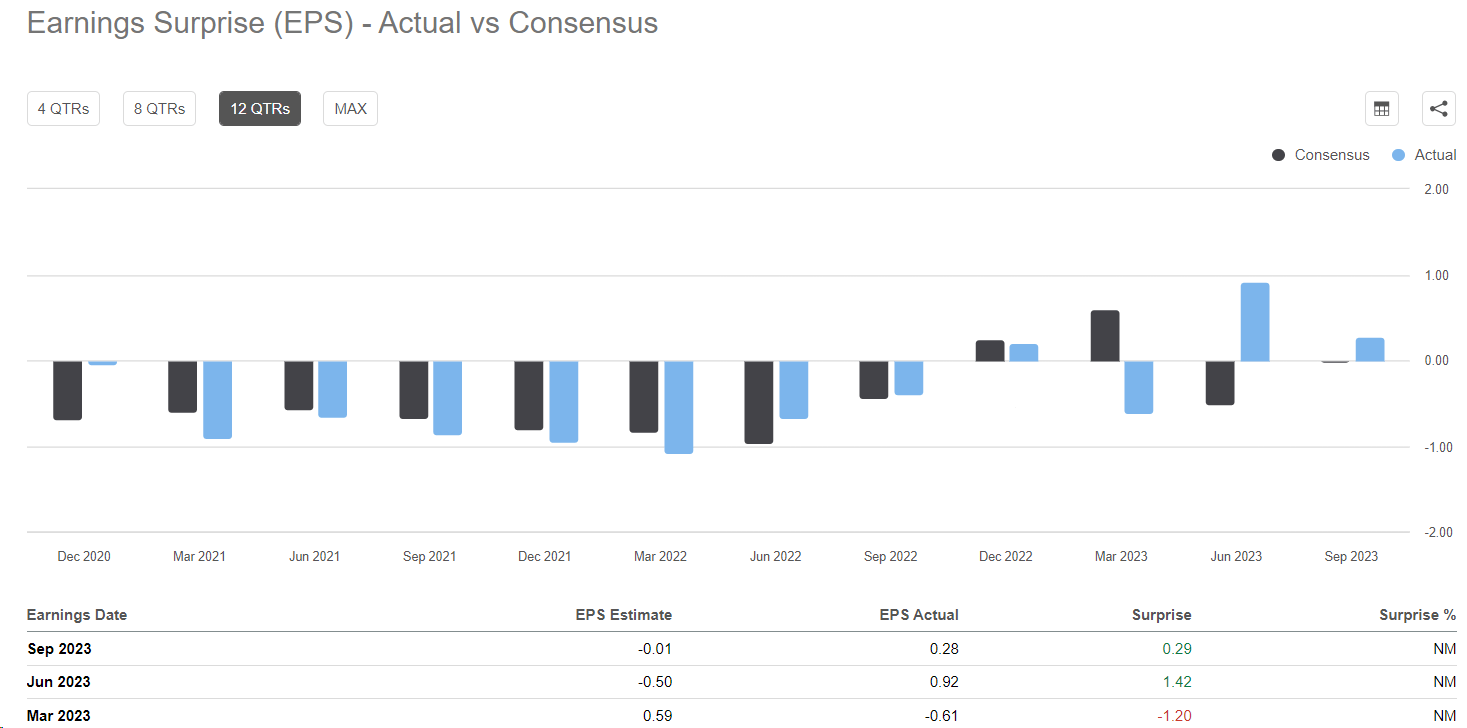

However, given the potential future payments from Sanofi and other partners, I think MGNX is likely to report much higher EPS figures in the coming quarters than currently priced in. This trend has already started in FY2023:

MGNX’s EPS surprises

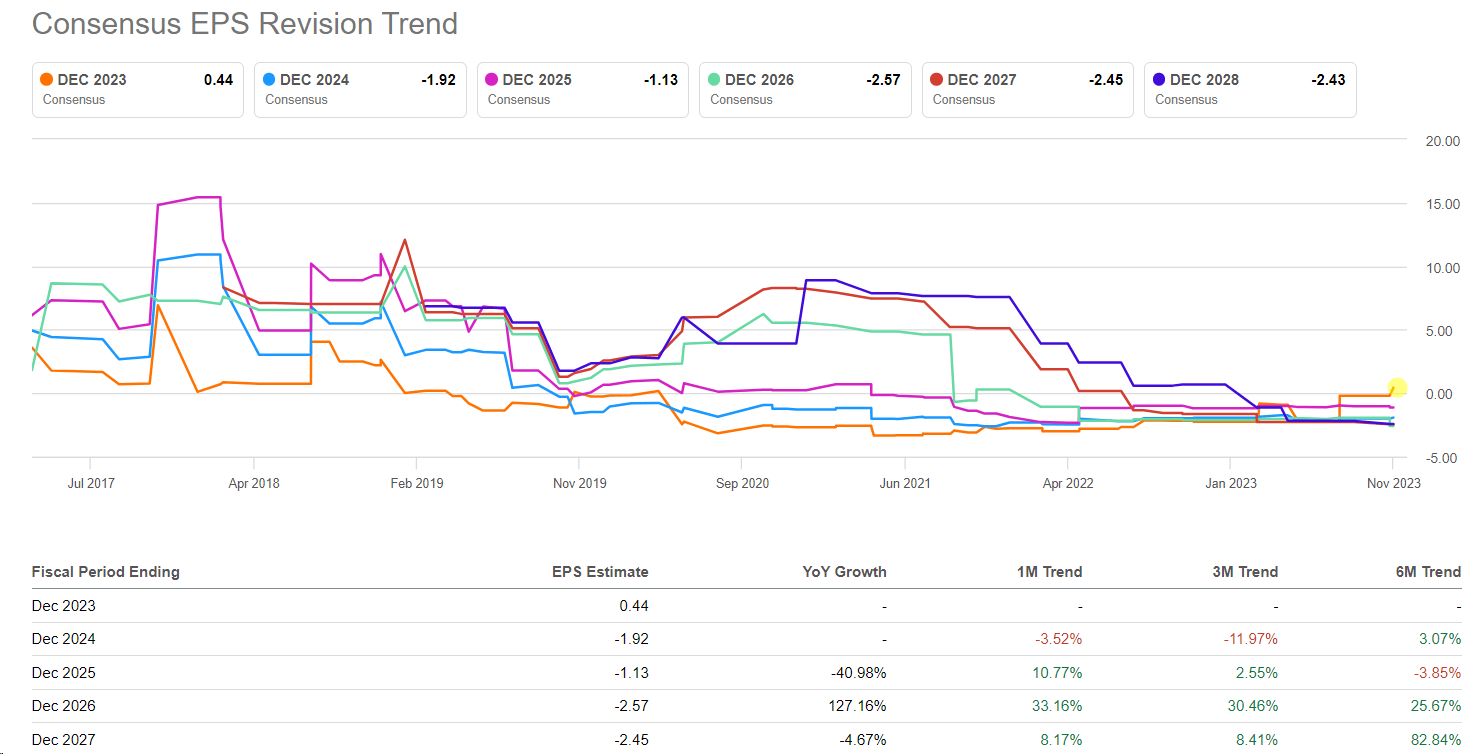

The company cannot be valued using conventional methods as its earnings will be highly variable in the future – this is what the market expects today, as far as we can see from the consensus forecasts. But it appears that analysts will have to revise their forecasts in a positive direction due to the company’s recent positive results – so far this has only happened for the FY2023 figures:

Seeking Alpha, author’s notes

If my assumption about the forthcoming revisions of EPS figures is correct, then we should very quickly see the accumulation of a discount in the company’s valuation – usually leading to an immediate rise in the share price if nothing interferes with it.

The Bottom Line

Despite the many positive aspects I have mentioned in this article, some risks hinder me from giving MGNX a ‘buy” rating this time. Firstly, I am a financier by training and have no particular knowledge of the healthcare sector. Also, the company has little historical financial data – analysts are forced to work only in the distant future, which makes their forecasts very sensitive to the smallest changes. Therefore, the slightest misunderstanding about the specifics of a company can furnish my conclusions about its attractiveness completely meaningless.

The inability to reckon an undervaluation (or overvaluation, which may also be the case) adds uncertainty to my reasoning.

In addition, the biopharmaceutical industry is renowned for its volatility, where factors such as drug approvals, clinical trial outcomes, or unexpected side effects can significantly influence stock prices. While the company boasts a robust pipeline, inherent uncertainties in clinical trials pose a risk, as success is not guaranteed, and regulatory approval remains uncertain, particularly for drugs in the early stages.

But despite all the risks, I think long-term investors should take a closer look at the company. At the very least, it is interesting to watch. I propose paying attention to the research of the other Seeking Alpha analysts – there is a lot of useful information there.

Thanks for reading!

Q2 2024 Earnings Call Transcript")