MIKE THEILER/AFP via Getty Images

Performance assessment

M/I Homes (MHO) has been one of my best performing picks in 2023. Since my last coverage of the stock till 2 February 2024 when I changed my ‘Buy’ stance into a ‘Neutral/Hold’, this pick has returned +148.02% compared to the S&P500’s +28.46% in total shareholder return terms, leading to +119.56% alpha.

Thesis

After this great alpha run, I have a neutral/hold stance on MI Homes because:

- Homebuilding backlog points toward a slowdown

- There is downside risks to margins

- Valuations are inexpensive, which curbs my bearishness

Homebuilding backlog points toward a slowdown

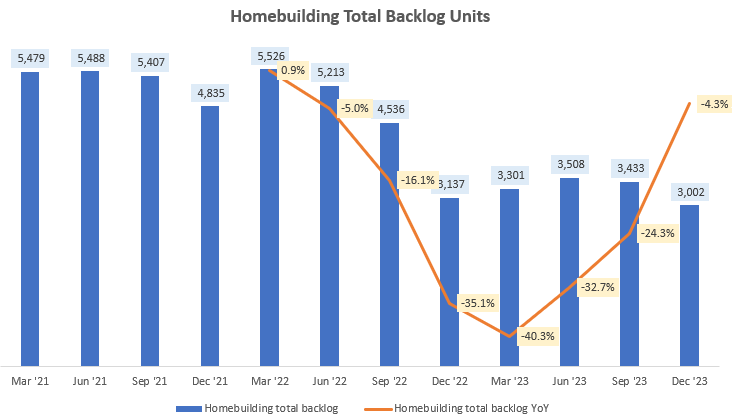

Homebuilding Total Backlog Units (Company Filings, Author’s Analysis)

MHO’s backlog is leading indicator of future revenues. And over the last few quarters, the backlog units have shrunk and are yet to post a meaningful rebound. In fact, in Q4 FY23, there was a steeper 12.6% QoQ fall.

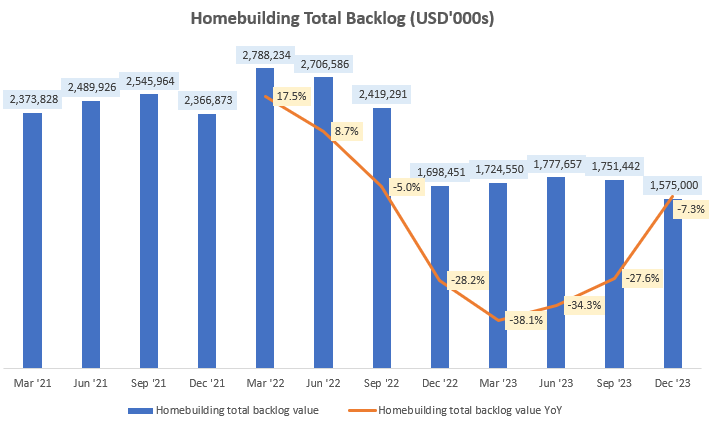

Homebuilding Total Backlog Value (USD’000s) (Company Filings, Author’s Analysis)

In nominal terms, you can see that the YoY percentage declines are worse than in volume terms. This is because of a trend down in the average selling price, driven by a higher proportion (53% as of Q4 FY23) of the company’s Smart Series mix, which relates to a more value/affordable product.

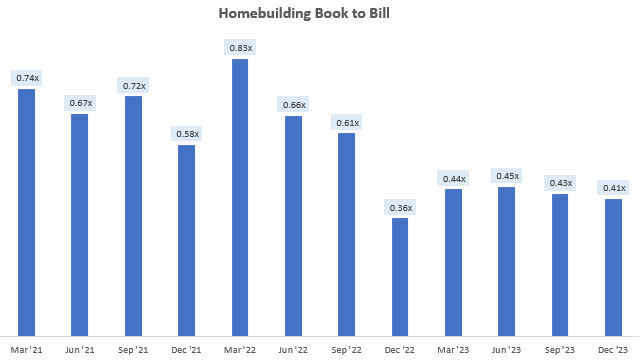

Overall, this has led to a weaker book to bill profile for the company; down from the ~0.7x range to low 0.4x:

Homebuilding Book to Bill (Company Filings, Author’s Analysis)

But why may this be happening?

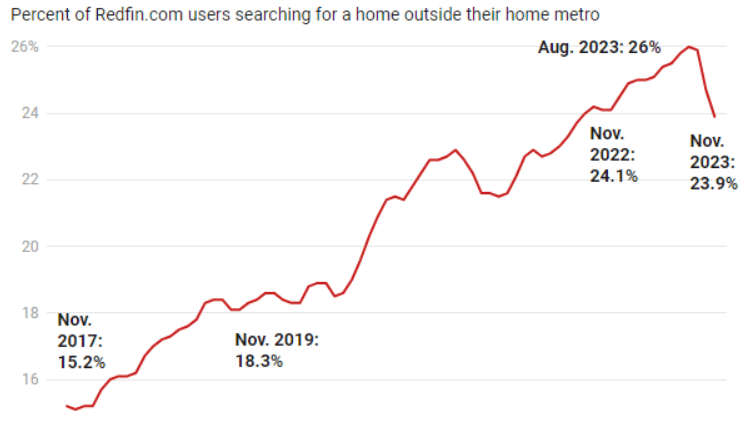

In my last article on M/I Homes, a part of my bullish thesis was based on strong relocation trends boosting demand for homebuilders. That part of the thesis has played out very well. However, there are signs that it is coming to an end:

Portion of Redfin Users Looking to Relocate (Redfin User Search Data)

November 2023 marked a sharp 210bps decline in the 6-year relocating % trend according to Redfin (RDFN) data. A saturation in work-from-home shifts and reduced affordability were cited as key reasons for the declining tick.

Homebuilding makes up 98% of the overall revenue mix. Hence, I view the slowdown in backlog as a warning signal for weaker revenue conversion ahead.

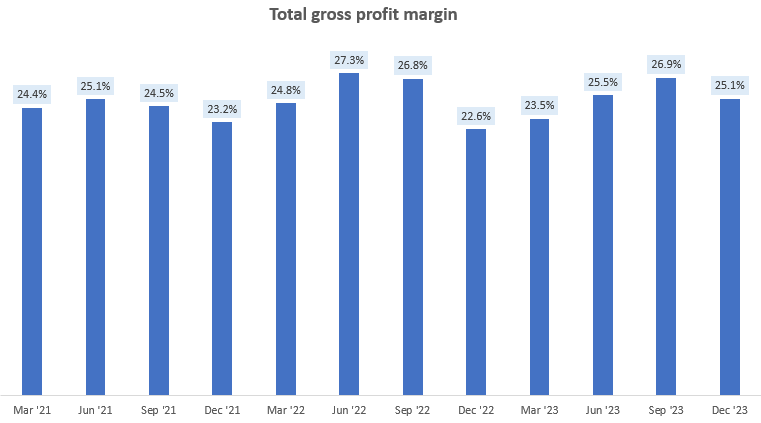

There is downside risk to margins

Total Gross Profit Margin (Company Filings, Author’s Analysis)

In the Q4 FY23 earnings call, M/I Homes’ management said that whilst there are land and labor cost pressures, they would be able to maintain gross profit margins at 25% giving the following reason:

[We will]… continue to produce really high-quality affordable product… Well-located communities will sell, and they will sell at really good margins…

– CEO Robert Schottenstein in the Q4 FY23 earnings call

This tells me management is relying on potentially favorable market conditions for pricing of their homes to offset the certain higher land and labor costs. In other words, there is reliance on a favorable variable element to offset an unfavorable fixed element of gross margins. Now, Redfin research noted that:

Home prices generally increased more in popular migration destinations [where M/I Homes is largely present] than they did in expensive coastal metros during the pandemic, making the case for moving a bit less compelling

– Redfin Housing Migration Trends, November 2023

Given this context, I believe there could be downside risks to gross margins.

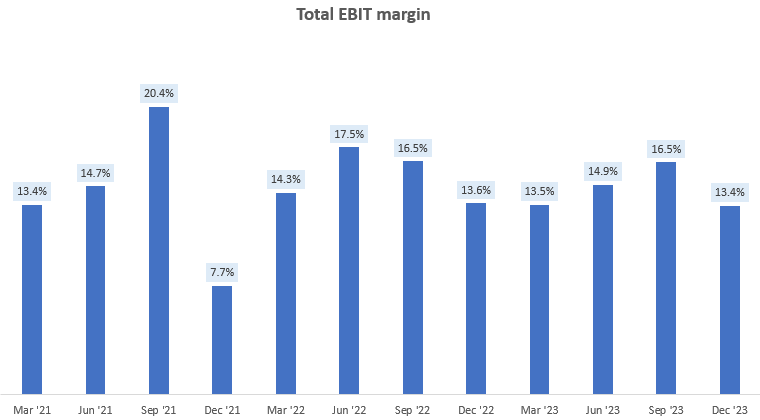

Total EBIT Margin (Company Filings, Author’s Analysis)

MHO’s EBIT margins also saw a sharp QoQ downtick of 310bps. 180bps is explained by a tick down in gross margins, leaving 130bps of higher operating cost intensity relative to overall revenues. In the Q4 FY23 call, management said this was due to:

higher incentive compensation, increased real estate taxes on our inventory levels and the cost of having more communities.

– CFO Phillip Creek in the Q4 FY23 earnings call

These mostly sound like sticky changes to me. Hence, even if gross margins remain stable as management has tried to assure, I perceive margin erosion risk due to higher opex spend intensity too.

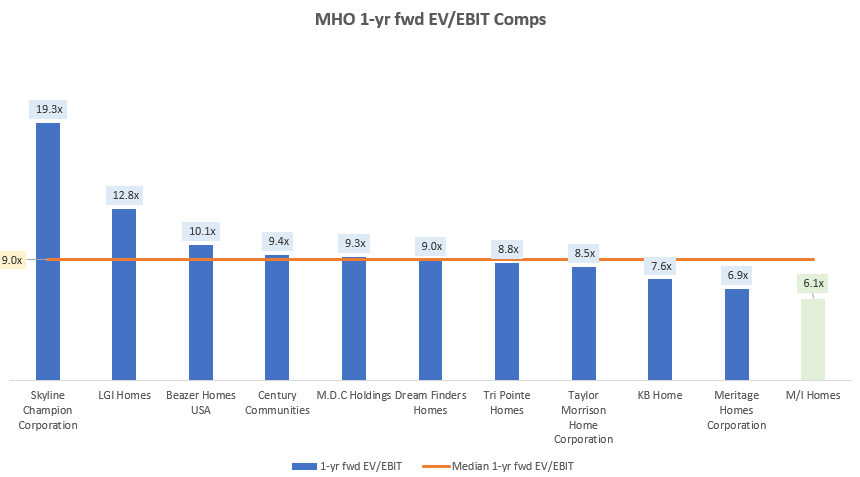

Valuations are inexpensive, which curbs my bearishness

MHO 1-yr fwd EV/EBIT Comps (Capital IQ, Author’s Analysis)

Peers set includes Meritage Homes Corporation (MTH), Century Communities (CCS), M.D.C. Holdings (MDC), Beazer Homes USA (BZH), Skyline Champion Corporation (SKY), Tri Pointe Homes (TPH), Taylor Morrison Home Corporation (TMHC), KB Home (KBH), Dream Finders Homes (DFH), LGI Homes (LGIH) and of course M/I Homes (MHO)

As can be seen from the chart above, MHO trades at a LTM EV/EBIT of 6.1x. This is at a 32.4% discount to the median multiple of 9.0x. This discount is steeper than 14.6%, which is what it was when I first covered M/I Homes. Due to this lower valuation, I am hesitant to express a clear bearish view on the stock, despite the headwinds anticipated.

Technical analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do.

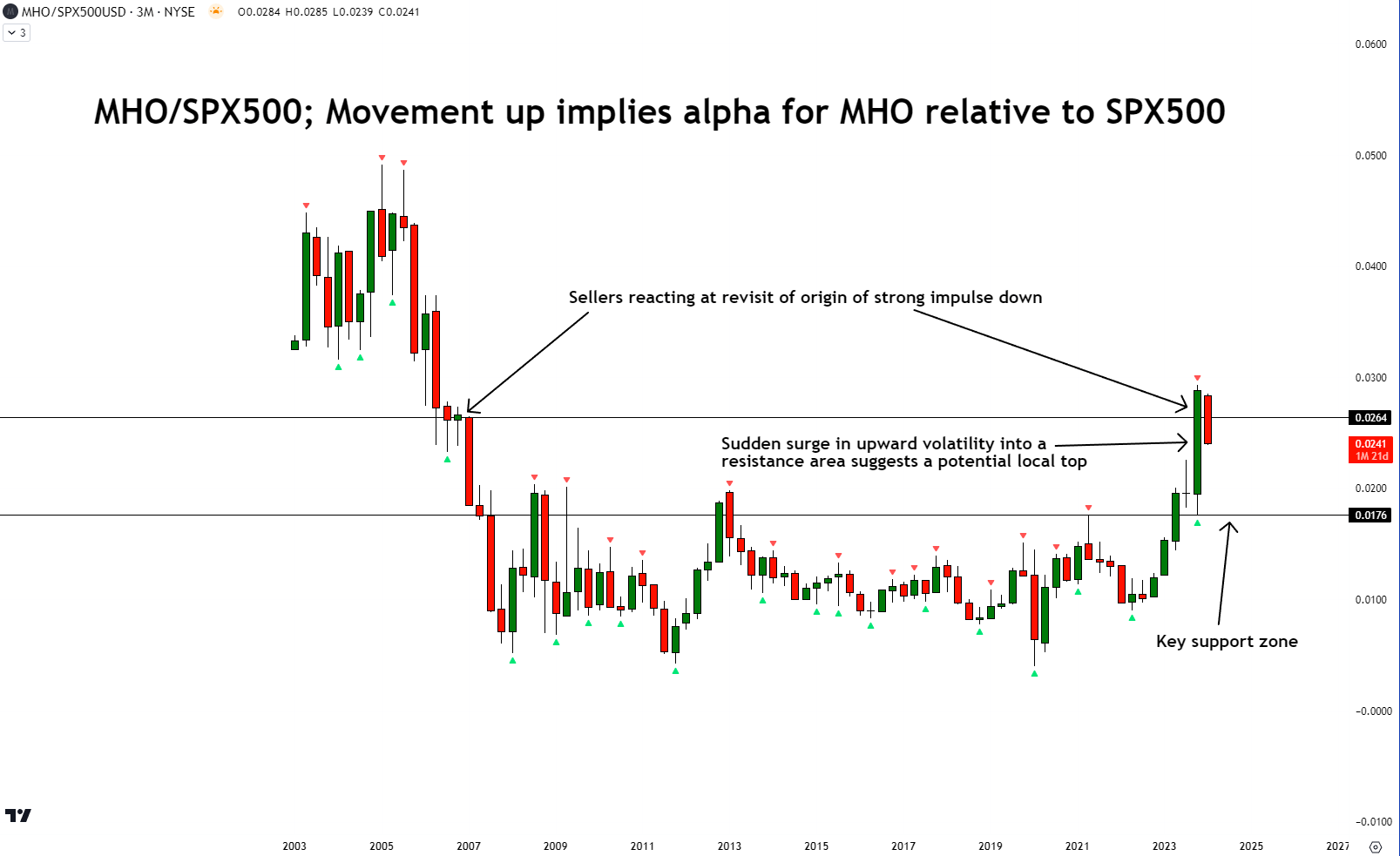

Technical Analysis of MHO vs S&P500 (TradingView, Author’s Analysis)

In the quarterly (every candle refers to a calendar quarter) relative ratio chart of MHO vs the S&P500 (SPY) (SPX), I see the ratio prices reacting at a key resistance level. Importantly, the approach to the resistance level was after a sudden acceleration, albeit without any progress via a breakout of the resistance zone. This indicates to me that a local top may be formed as the ratio prices fall back toward the support zone highlighted. And this would imply negative alpha ahead for MHO vs the S&P500.

Key risk

Something that made me rethink my neutral stance assessment was management’s bullish tone in the Q4 FY23 earnings call. However, upon a closer hearing of the commentary, I realized that management’s was optimistic mostly on sales conversions. However, my thesis is based on a slowing and shrinking backlog pipeline. I do not have any reason to believe the sales conversion over the next few quarters would be poor as the company executes and recognizes revenue from progress in its backlog. However, over the medium to longer term, the headwinds in backlog growth must translate into revenue growth. As I think the market is more responsive to that leading indicator, I feel more confident in my view.

Takeaway

M/I Homes was one of my top performing picks in 2023, generating almost 120% alpha over the S&P500. However, I believe that MHO’s golden year of outperformance is coming to a halt since backlog and book to bill figures are shrinking, warning of future revenue slowdown. Moreover, on the margins side, I see downside risk to gross margins and potentially structural headwinds from higher opex intensity. Technical analysis is also showing that MHO’s alpha train has encountered a powerful obstacle. The one saving grace that is keeping me from expressing a clear bearish view is the valuations as M/I Homes is trading at a 32% discount to comparable peers.

Rating: ‘Neutral/Hold’

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Q2 2024 Earnings Call Transcript")