Robert Way

It has almost been two years since I published my last article about the French consumer goods company L’Oréal S.A. (OTCPK:LRLCF). When my last article was published, the stock was very close to a temporary bottom. Nevertheless, I didn’t see the stock as a bargain back then and I wrote:

L’Oréal is not really overvalued right now. And one might argue that you must pay a premium for great companies and that those stocks are hardly ever cheap. This might be true, and everybody must make that decision for oneself. In my opinion, L’Oréal is still a bit too expensive right now, and considering that we are most likely heading towards a recession, I don’t know if right now is the time to buy this undoubtedly great company.

In the meantime, the stock could reach its previous all-time highs again and we can assume that the stock is once again no bargain as it is trading for a 50% higher price (at least in U.S. dollar) but a lot can happen in two years and therefore let’s take another look at the company and the stock.

Technical Picture

We start by looking at the chart and similar to many other stocks, L’Oréal hit its previous all-time highs in late 2021. And after declining in 2022 (like many other stocks), L’Oréal reached its previous all-time highs again in April 2023 and is now once again trading at a similar level. To be precise, the stock is now trading a little bit higher than in December 2021 or April 2023, but I would argue that the stock could not really break out so far and we are pushing against a strong resistance level.

And similar to many other stocks it seems like a possibility for L’Oréal to form a double top and we might see lower stock prices in the coming months and quarters again.

Annual Results

Similar to the last few years, L’Oréal reported solid results for fiscal 2023 once again and the company is growing with a stable pace.

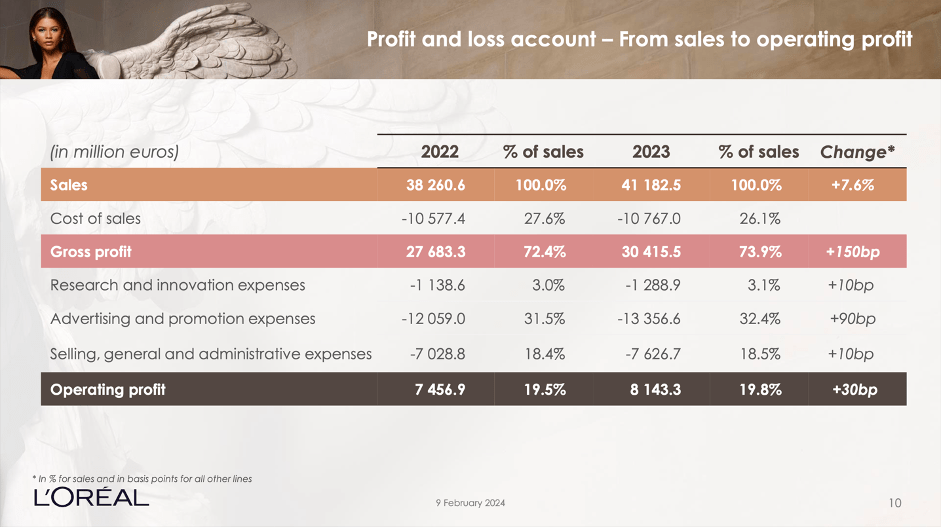

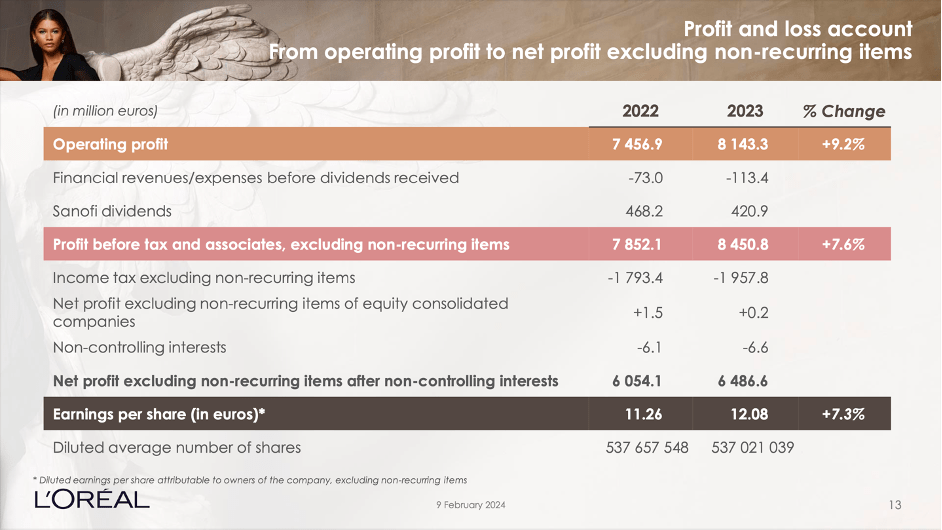

L’Oreal Q4/23 Investor Presentation

L’Oréal generated €41,183 million in sales in fiscal 2023 and compared to €38,261 million in fiscal 2022 the top line grew 7.6% year-over-year. Like-for-like sales increased even 11.0% year-over-year (these sales are based on a comparable structure and identical exchange rates). And not only the top line increased, operating profit also grew 9.2% year-over-year from €7,457 million in the previous year to €8,143 million in fiscal 2023. And finally, diluted earnings per share increased from €11.26 in fiscal 2022 to €12.08 in fiscal 2023 resulting in 7.3% year-over-year growth.

L’Oreal Q4/23 Investor Presentation

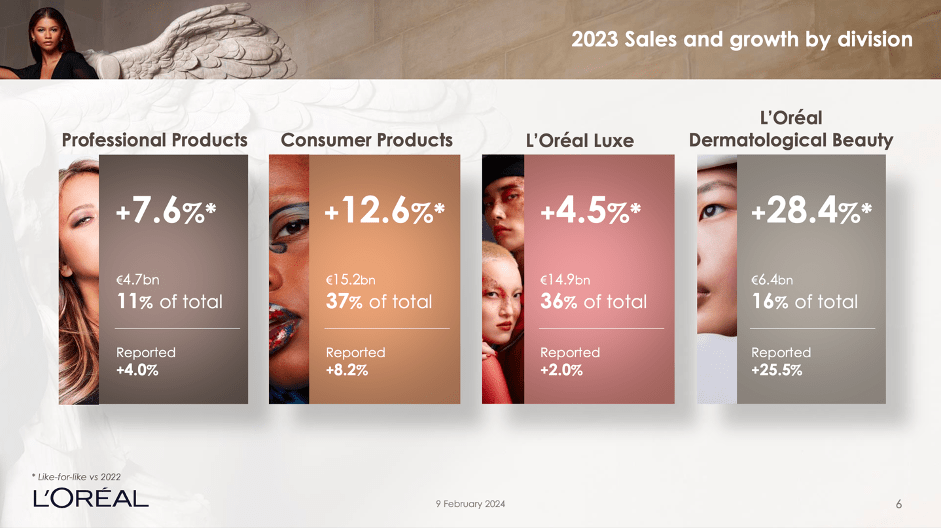

All four divisions, the company is reporting in, also contributed to growth:

- Professional Products generated €4,653 million in revenue and a like-for-like growth rate of 7.6%. The division clearly outperformed the professional beauty market, and that outperformance was supported by the focus on haircare and strengthening to omni-channel approach as well as conquering new markets. Especially the two biggest brands L’Oréal Professionnel and Kérastase grew with a high pace and the segment generated €1,005 million in operating income – resulting in an operating margin of 21.6%.

- Consumer Products increased like-for-like revenue 12.6% year-over-year to €15,173 million. And while the segment is generating the biggest part of revenue (slightly ahead of L’Oréal Luxe), it only reported an operating margin of 20.5% and therefore slightly less operating income (€3,115 million) than L’Oréal Luxe.

- L’Oréal Luxe also increased revenue but like-for-like revenue grew only 4.5% YoY to €14,924 million. Operating income was €3,332 million and the reported operating margin was 22.3%.

- Dermatological Beauty reported the highest top line growth of all four segments and like-for-like revenue increased 28.4% year-over-year to €6,432 million. The segment also has the highest operating margin of all four segments (26.0% in fiscal 2023), and this resulted in €1,671 million in operating income. The segment could keep the momentum it already had in the past and grew twice as high as the overall market.

L’Oreal Q4/23 Investor Presentation

Growth

Management seems to be optimistic for its business to continue growing in the years to come and in my opinion, we can share this optimism.

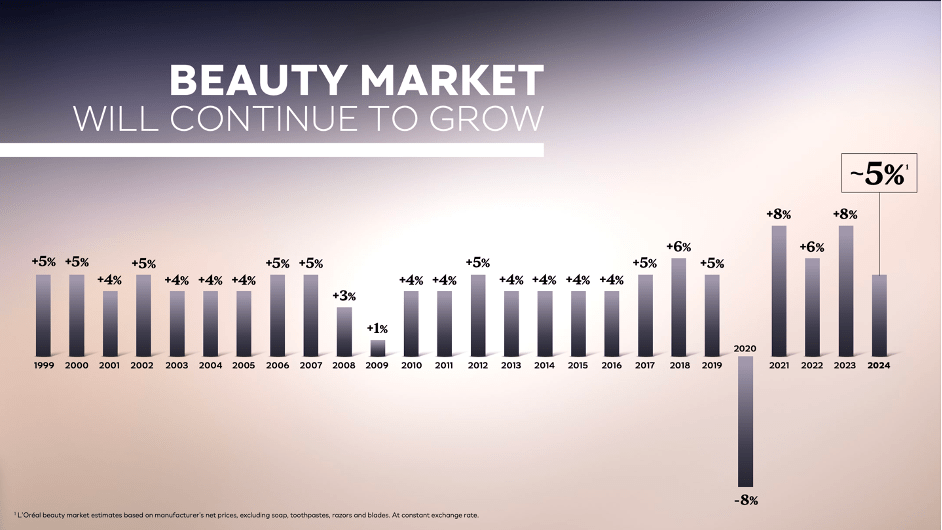

For starters, the overall market was growing with a solid pace in the last few decades, and we can be quite optimistic for these growth rates to continue in the years to come. Since 1999, the beauty market had to report declining revenue only in one year – 8% decline in 2020 due to the lockdowns associated with the COVID-19 pandemic. And in 2009, the market reported only 1% growth, but in all the other years the beauty market grew at least 3% annually and growth rates between 4% and 5% seem realistic. For 2024 management is expecting the beauty market to grow around 5% again.

L’Oreal CAGNY Presentation 2024

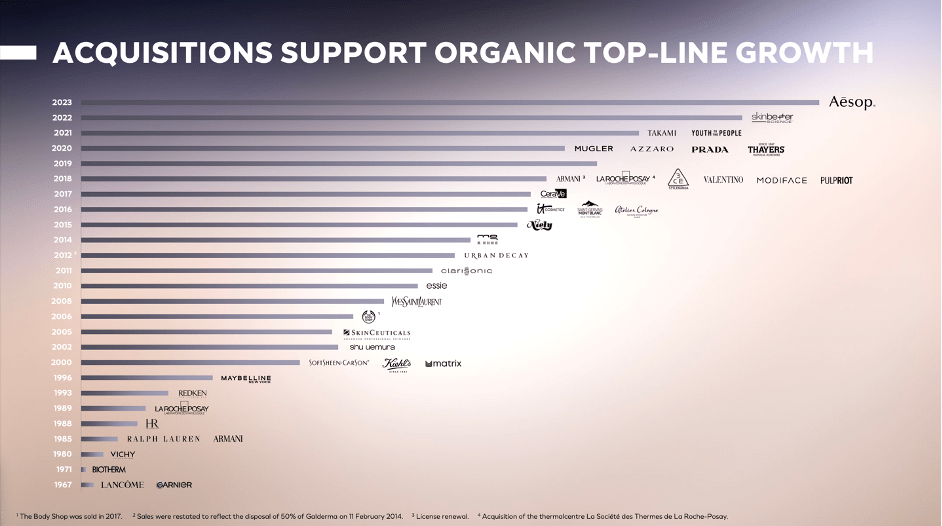

But L’Oréal might not just grow in line with the overall market but grow with a higher pace by outperforming the beauty market. This means the company must gain market shares from its competitors. In my last article I showed that L’Oréal outperformed the overall market (and was therefore gaining market shares), but while I think it is possible for the company to continue this path we should be cautious. However, L’Oréal can gain market shares by acquisitions – as the company has done in the past. Since 2014, the company has been acquiring other companies in every single year contributing to top line growth and expanding the market share of L’Oréal.

L’Oreal CAGNY Presentation 2024

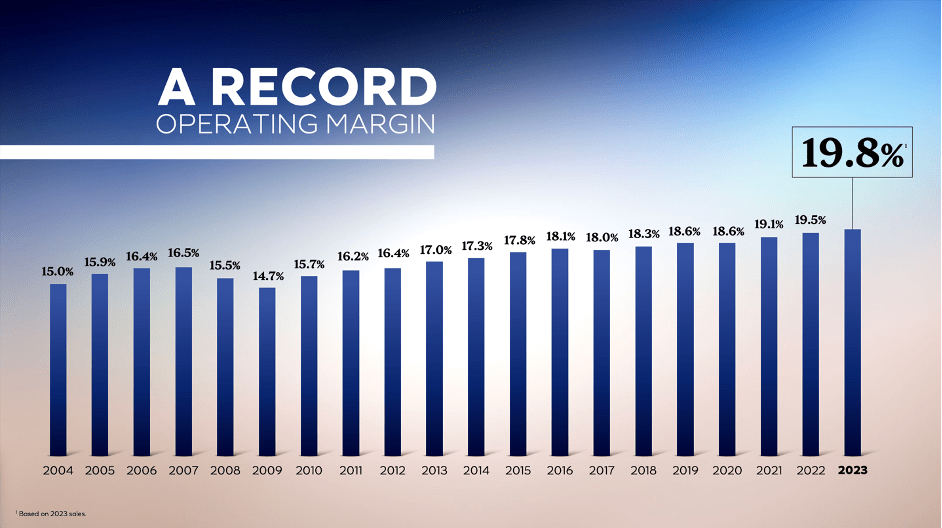

Aside from growing the top line, L’Oréal can also grow its bottom line by improving margins and when looking at the last 20 years management did a pretty good job of increasing the operating margin in most years. However, we should also be a little cautious here. During the Great Financial Crisis, the company had to report a declining operating margin two years in a row and for the next potential recession we have to assume a declining margins as well.

L’Oreal CAGNY Presentation 2024

Overall, we can assume that L’Oréal might be able to grow its bottom line at least 6-7% (maybe even slightly higher). And this can be achieved by a combination of top line growth (due to overall market growing, acquisitions and gaining market shares) and still increasing the operating margin slightly from year to year. Analysts are also quite optimistic that L’Oréal can grow its top line slightly above 6% annually for the next decade. When also assuming a slightly growing operating margin, top line growth might be even higher.

High Quality Business

When talking about future growth rates we see high consistency in the past, which is a good sign and is usually making it easier to make predictions for the years to come. And L’Oréal also seems to be a very stable business with a wide economic moat (that is also justifying the high valuation multiples to some degree – we will get to that).

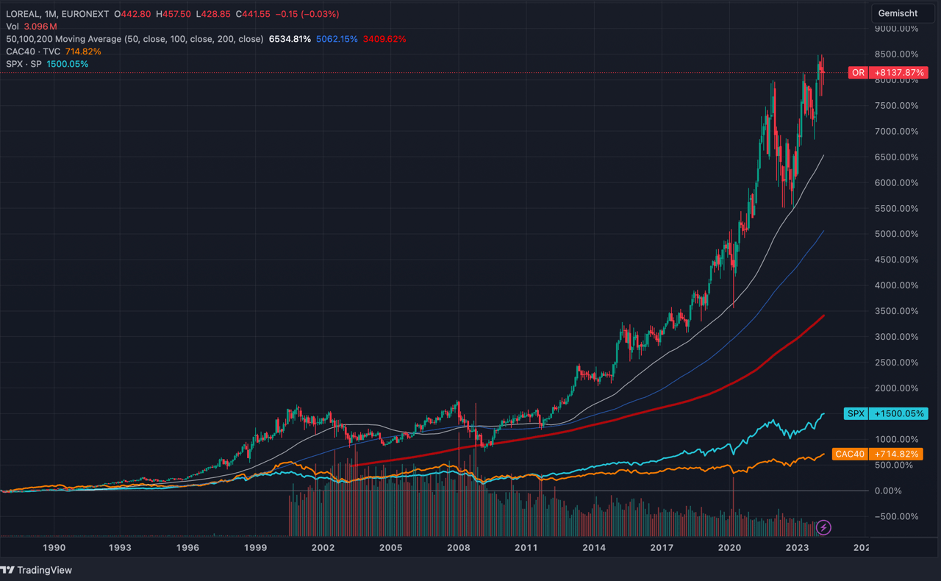

When looking at the last few decades, L’Oréal’s stock clearly outperformed the S&P 500 and as we are dealing with a French company, we can also compare the stock price to the CAC-40 making the outperformance even more impressive.

TradingView

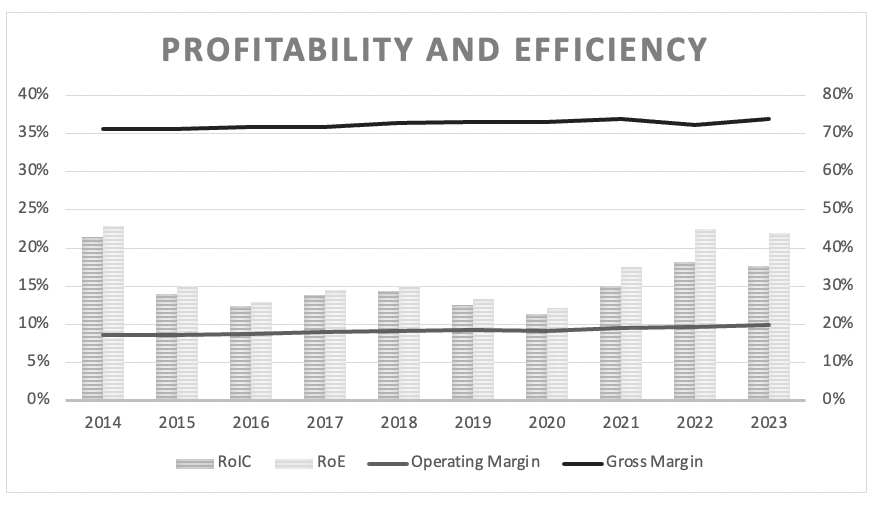

When looking at the gross margin and operating margin, we see extremely high levels of stability and consistency in the last ten years. This is showing pricing power of the company. Additionally, L’Oréal is reporting stable and high return on invested capital. In the last ten years, the average return on invested capital was 15.10%, which is a strong hint for a wide economic moat and a great and profitable business.

L’Oreal Operating margin, gross margin and return on invested capital (Author’s work)

I already wrote in previous articles that the economic moat of L’Oréal is mostly based on two different sources. On the one hand, the wide economic moat is based on scale-based cost advantages. And while this might not be the strongest moat a company can have, we also have several brand names on the other hand, which are contributing to the economic moat of L’Oréal. The company might profit from cost advantages as costs for research as well as advertising will become more “effective” when more products are sold. The costs for a major advertisement campaign are always the same for every company – and when L’Oréal can sell twice as many products than a competitor due to the campaign, L’Oréal has an advantage.

And even more important is the portfolio of brand names, L’Oréal has. In my first article I wrote about the brand names:

But more important than the scale-advantage is the company’s portfolio of different brands, which are an important intangible asset for the company. L’Oréal has not only several strong brands, but the portfolio is also well-balanced across mass, prestige, salon and dermatological channels and even when facing headwinds in one division (or segment), this could be balanced out by other divisions (or segments). The brands are important and valuable as L’Oréal can charge a premium from its customers because of the brand name. Additionally, it can increase the price a few percentage points (higher than inflation) every single year due to the brand name without losing customers.

Long-term Focus

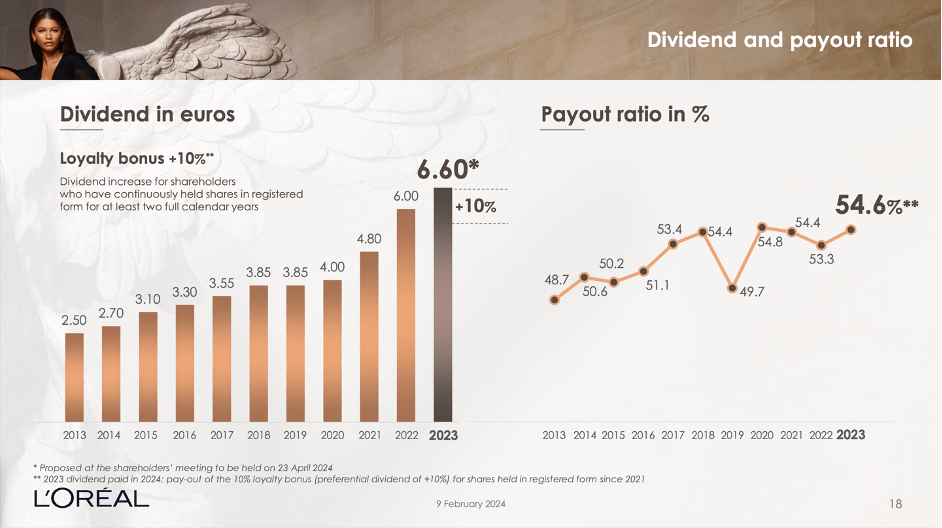

Aside from the wide economic moat around the business, we can also mention managements’ focus on long-term decisions (at least it seems like management is clearly focusing on long-term decisions, which is good for shareholders). First, the company is rewarding shareholders with registered shares that have been held for more than two calendar years with a 10% dividend bonus. And for fiscal 2023, management proposed a dividend of €6.60 – a 10% increase compared to the previous year.

L’Oreal Q4/23 Investor Presentation

A second reason why we can assume that L’Oréal is focusing on the long term is the shareholder structure. L’Oréal is a “family business” and controlled by the founder’s family, which is always a good sign (as I argued in my article about the strength of family-run businesses). Françoise Bettencourt Meyers and her family own 33.3% of the shares of L’Oréal and therefore have a great influence on the future path of the business. And when the founders’ family is still owning the majority of the shares and has the personal wealth tied to the business, decisions are usually made for the long-term and not for a short-term bonus or a stock price increase for a few months.

Intrinsic Value Calculation

And while L’Oréal seems to be a great business, growing with a solid pace, being controlled by the founders’ family that has a long-term focus and a wide economic moat around the business, it still seems not like a great investment at this point.

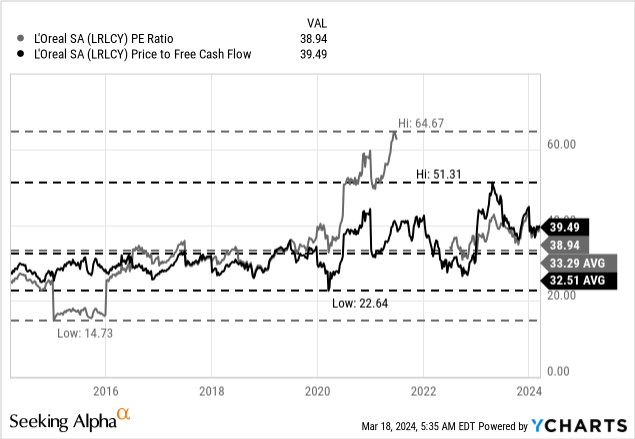

We can start once again by looking at the valuation multiples L’Oréal is currently trading for. Right now, the stock is trading for 39 times earnings per share as well as 39.5 times free cash flow. And valuation multiples close to 40 are high on an absolute basis and can only be justified by very high and consistent growth rates. We already saw above that L’Oréal is growing with high levels of consistency, but growth is rather in the high single digits than in the double digits and such high valuation multiples are probably not justified.

The valuation multiples are also high on a relative basis. When comparing the current multiples to the 10-year average of 33.29 for the P/E ratio and 32.51 for the P/FCF ratio, the stock is also expensive compared to its long-term average.

But as always, we are trying to determine an intrinsic value by using a discount cash flow calculation. As basis for our calculation, we use 535 million outstanding shares and a 10% discount rate. Additionally, we are calculating with the free cash flow of the last four quarters, which was €6,116 million. Now the more difficult question is the following: What growth rates are realistic for L’Oréal in the years to come? In my last article I assume 7% growth for the next ten years followed by 6% growth till perpetuity. This would lead to an intrinsic value of €306.78 for the stock. When being a little more optimistic (and it is possible to justify that optimism when looking at past EPS growth rates), we can assume 8% growth for the next ten years followed by 6% growth till perpetuity, which would lead to an intrinsic value of €329.30.

|

Timeframe |

CAGR |

|---|---|

|

Last 10-years |

8.99% |

|

Last 20-years |

8.62% |

|

Last 30-years |

10.42% |

|

Last 40-years |

9.13% |

When looking at past growth rates we could also be very optimistic and assume 10% growth for the next ten years followed by 6% growth till perpetuity. But even in that very optimistic scenario we only get an intrinsic value of €379.33 for the stock and L’Oréal would still be overvalued.

Conclusion

In my opinion, L’Oréal is not a “Buy” and certainly not a bargain. Especially when looking at the technical picture in combination with the high valuation multiples (and the stock being rather overvalued), I don’t think L’Oréal is the best investment we can make right now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")