mcdc/E+ via Getty Images

Loma Negra (NYSE:LOMA) is facing many headwinds now. They accumulated a lot of debt in the past two years and used it for dividend payments. Now that the macroeconomic situation in Argentina is uncertain, causing market participants to wait for signs of improvement, the company is caught with high debt levels, high interest payments, and uncertain revenues. Not the situation anybody wants to be in.

Business Overview

Loma Negra is an Argentinian cement, masonry cement, aggregates, concrete, and lime producer that has approximately 45% market share in Argentina. Their main competitors are Holcim (OTCPK:HCMLF), Avellaneda, and PCR. Loma’s main market is the greater Buenos Aires area. The competition in the market is mainly limited to the areas where the production facilities of each company are located. This is due to high transportation costs for cement, which limit the ability of each producer to effectively compete over long distances. The imports of cement to Argentina therefore represented only 0.1% of total cement consumption in February 2024, which is negligible.

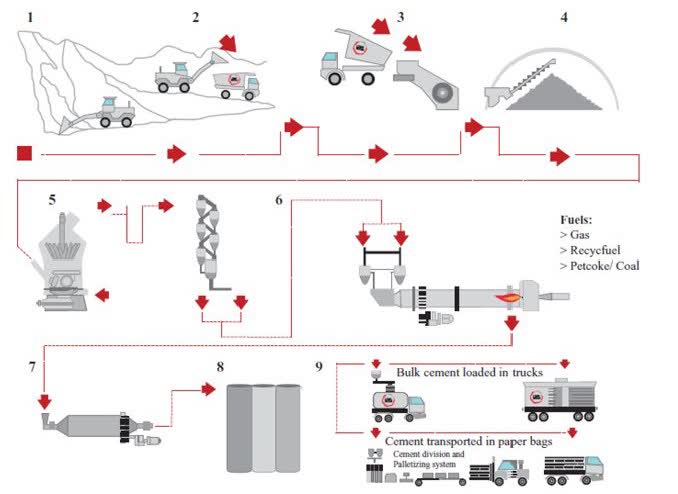

The business model is not hard to understand:

- At first, they have to extract limestone and clay and transport them to the crushing plant, where the rocks are converted into small stones.

- Then the crushed pieces are milled together and burned at temperatures exceeding 1,400 degrees Celsius.

- After the burning, the material is cooled and stored in silos. From there, the cement is dispatched to a packing station or bulk silo and distributed to customers.

Cement production (Loma Negra 2022 Annual Report)

They also own and operate six limestone mines, which should be sufficient for 149 years of cement production, and they are contracted to operate the Ferrosur Roca freight railway network with a distance of 3,100 kilometers. The railway contract may be canceled this year by the government.

Macro And Industry Outlook

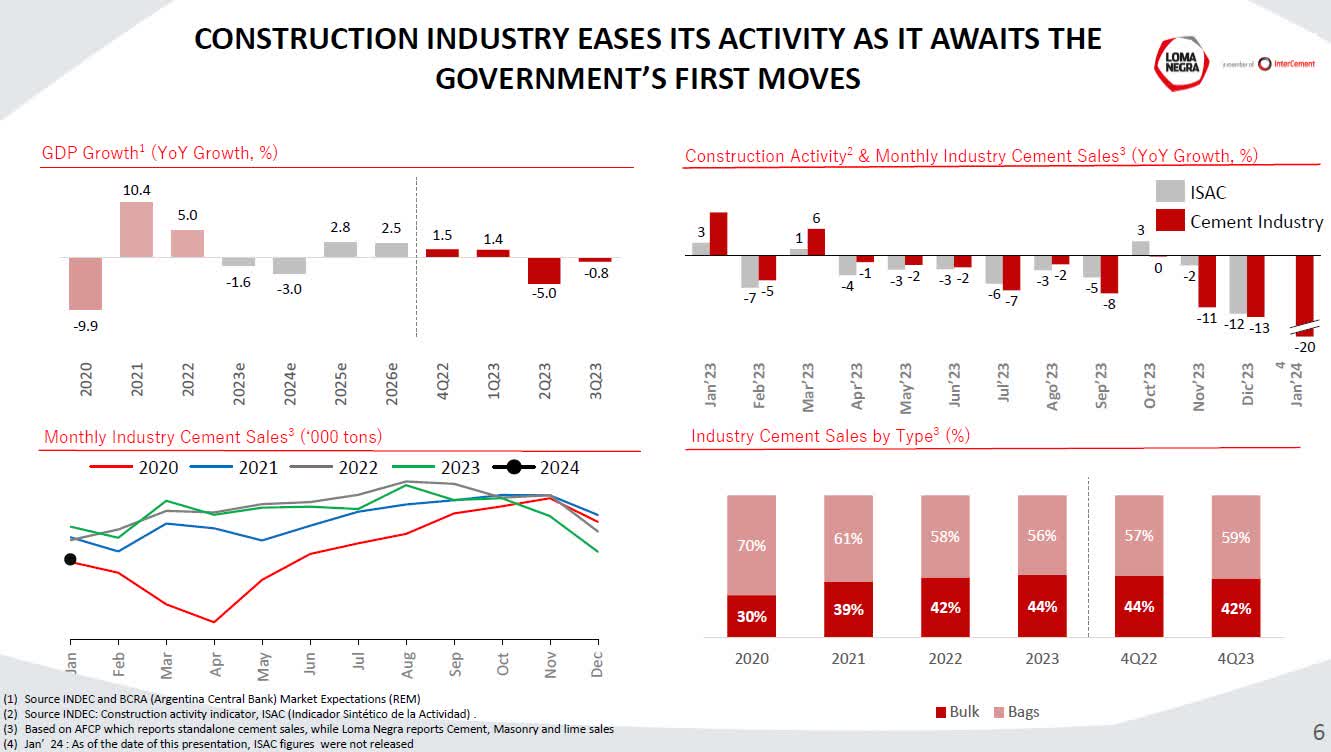

For Loma Negra and the other cement producers, the construction activity and GDP outlook are very important. Unfortunately, it is expected that Argentina’s GDP will decline in 2024 by 3.0%. Significant weakening in construction activity and cement sales started in November 2023 after the Argentinian elections, and as you can see in the picture below, monthly cement sales in December 2023 reached volumes last seen in January 2020, and in that year the country experienced a 9.9% decline in GDP.

Loma Negra 4Q23 Results Presentation

Unfortunately, this situation got worse as the monthly cement consumption in February 2024 declined by another 10.8% from the already low January 2024 consumption and reached 689,425 t, which is 23.5% lower than in February 2023, with no sign of improvement anytime soon.

You can feel the pessimism from the Loma Negra Q4 2023 earnings call:

When we dive into the numbers for our industry, we can see that after a positive October, the construction activity indicator shows a significant drop in the last two months of the quarter, deepening the drop in January. Following this trend, cement dispatches showed a double-digit decrease in November and December and a sharp drop in the first month of 2024. After several months of election process volatility, sales in the national cement industry are being affected by the political transition and the consequent effects of tighter economic policies.

…concrete operation experienced a slowdown due to a macroeconomic uncertainty, while public works enter standby mode after the elections awaiting future definitions.

…the electoral process and the subsequent change in administration have induced uncertainty, impacting the level of activity. Industry and stakeholders are cautious and awaiting the government’s initial action and the stabilization of key economic indicators.

The future outlook is negative, so let us see how this translates into business finances.

Business Financials

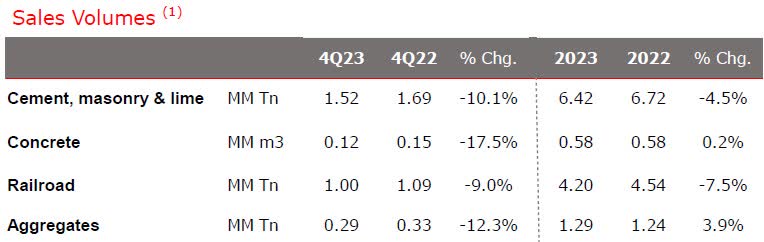

Sales volumes in all product segments were down in 4Q23, and given the negative information on cement consumption in February 2024, the situation this year should be even worse.

Loma Negra 4Q23 Results Presentation

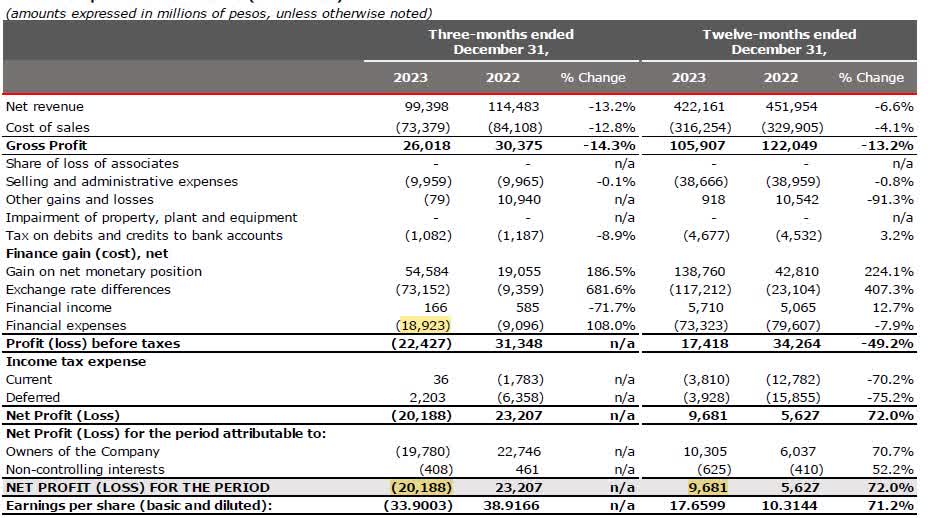

The negative development in 4Q23 is also reflected in the income statement for FY2023.

Income statement (Loma Negra 4Q23 Results Presentation)

So the company was able to produce ARS 9.681 billion in net profit for FY 2023, which translates into US$9.63 million (when I use the parallel ‘Dollar Blue‘, which is now ARS 1005 for US$1). For countries with very high inflation, I prefer to use the parallel ‘Dollar Blue’ rate, as it, in my opinion, better reflects the true exchange rate. Just for information, the official exchange rate at the time of writing this article was ARS 850 = US$1.

Considering that the market cap of Loma Negra is US$832 million, this gives us a P/E ratio of 86 for a company with declining sales. It’s better to own Nvidia (NVDA), which has a P/E ratio of 79, and it is probable that its revenues and net profits will grow. The financial expense of debt is another issue, but more on that in the debt section below.

You may say that this is a different type of company, and we should focus more on the cash generated and distributed (or at least, which can be distributed) to shareholders. That’s a fair argument, so let us check the cash flow.

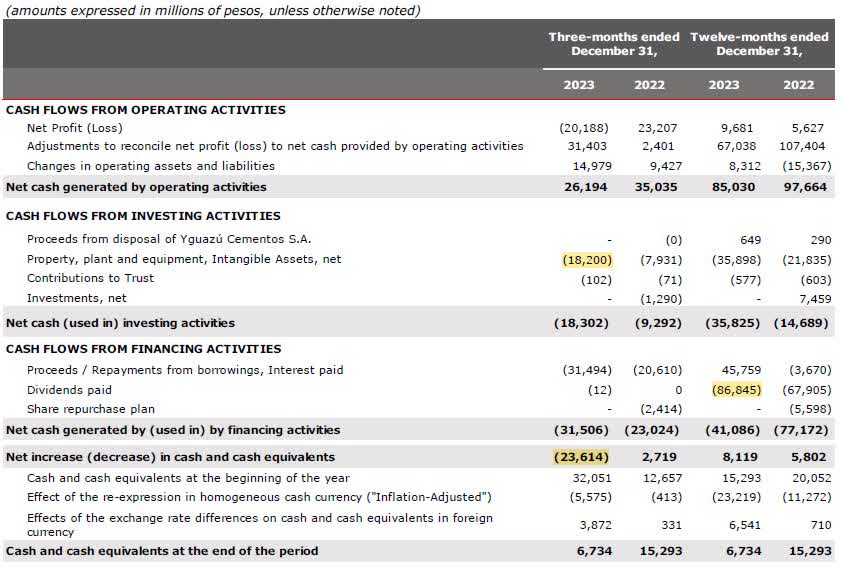

Cash Flow Statement (Loma Negra 4Q23 Results Presentation)

The details of financing cash flow are also interesting.

Financing Cash Flow (Loma Negra 4Q23 results)

In 2023, the company generated operating cash flow of ARS 85 billion and spent almost ARS 36 billion on CAPEX. This gives us ARS 49 billion available for financial expenses. They also borrowed ARS 212 billion and paid ARS 86.8 billion (US$120 million) as a dividend and ARS 165 billion as interest and debt repayment. If they did not take on additional debt, the cash generated by operations after the CAPEX deduction would not be enough for the interest payments on debt. Doesn’t that sound like a zombie company to you?

Another thing that worries me is Capex in 4Q23, which reached ARS 18.2 billion at the time of declining revenues. The company provides only information that it was used as maintenance capex and for the “project of adapting dispatch facilities to use 25kg bags”, but there is no information available about how long it will take to finish the project or how much they will spend on it.

The dividends had a huge impact on the total return received from the stock since January 2022, but given the declining sales volumes and high debt, you should not expect them anytime soon.

Debt Is An Issue

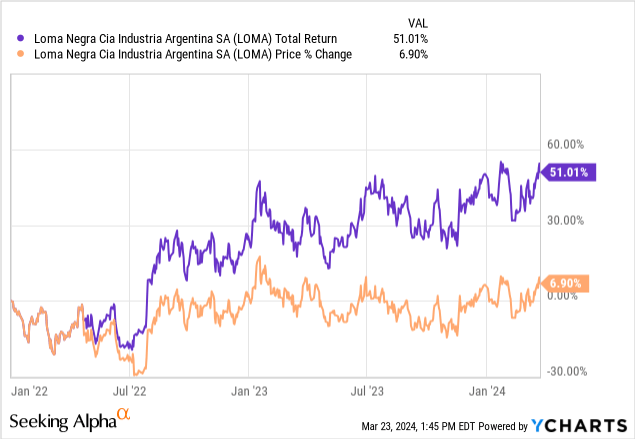

What you certainly do not want is to find yourself in the situation Loma Negra is in now. The debt accumulated in previous years is now an issue as the declining sales will, with a high probability, negatively influence profit and cash flow. That all comes at a time when the future outlook for the Argentinian economy is bad and you have to repay US$41 million in debt this year and pay high interest payments on the remaining debt.

Loma Negra 4Q23 Results Presentation

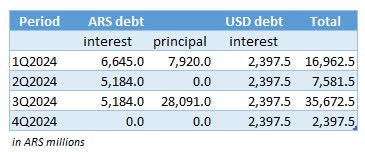

From the 4Q2023 results, we know that as of December 31, 2023, the company has a debt of US$182 million, of which 76% was in USD (US$137 million) and 24% was in Argentinian pesos (ARS 36,011 million). The debt in pesos is maturing this year, and the interest rate is set at BADLAR + 2% p.a. The BADLAR rate is 71.81% as of March 21, 2024. Remaining USD debt has an interest rate between 6% and 7.5% (for my calculation, I will use 7%) and matures in 2025 and 2026. I will assume quarterly interest payments. After my calculations using the current parallel ‘Dollar Blue’ rate, the company will need approximately the below-mentioned amount of money for interest and principal payments.

Table: Author

Just for the interest payments in 2024, they will need ARS 26,000 million, which they do not have as the cash on the balance sheet by December 31, 2023 was only ARS 6,700 million, and the projection for future cash flow is gloomy (more on that later). For me, the situation is clear. The company has to take on new debt at any cost or issue new shares or sell assets or default on debt. None of these scenarios is favorable to shareholders.

Future Profitability Projection

For my future profit projection in 1Q2024, I use 1Q2023 sales volumes lowered by 23% (as we know that the cement consumption in February 2024 is 23.5% down YoY) and apply product prices from the last quarter. As I expect inflation to continue, revenue in each quarter increases by approximately 10% until the last quarter, when I expect market recovery and a reduction in the inflation rate. As the part of interest expense is in USD, I have also adjusted USD interest payments by expected inflation.

Profit projection (Table: Author)

After my calculation, I expect a FY2024 net loss before taxes of ARS 6,600 million, not taking into account exchange rate differences as it is impossible to predict.

Risks To My Thesis

There are also risks associated with my investment thesis. Below, I try to highlight two of them.

The macroeconomic and political situation in Argentina is influencing activity in the construction sector. In my thesis, I assume that economic activity and construction sector activity will be subdued until 4Q2024. If this is not the case and the economic activity recovers in the second or third quarter, Loma Negra will benefit and the results will be better.

Inflation in Argentina can influence future revenues, costs, the interest rate on the Argentine peso and the exchange rate to the USD. In my thesis, I assumed that there would be 10% inflation growth each quarter until 4Q2024. If the government is successful in suppressing inflation, this should have a positive effect on the interest rate for the Argentine peso and the exchange rate for the USD. In such a case, the company will need less money for debt repayment, and this should positively influence the bottom line.

Conclusion

Loma Negra is facing many headwinds now. The company accumulated a lot of debt in the past two years due to frivolous management decisions that were used for dividend payments. Now that the macroeconomic situation in Argentina is uncertain (you may also ask, when was it certain and predictable? …fair question, but I do not have an answer.) causing companies and people to wait on signs of improvement, the company is caught with high debt levels and high interest payments. At the same time, the bottom line may take a significant hit too.

Loma Negra is now in a situation nobody wants to be in: declining profits, uncertain outlook, high debt and approaching debt maturities. For me, the company is a stock to avoid now.

I bought shares in Loma Negra during 1Q2022, when the company had negative net debt and the investment cycle was ending. My investment thesis paid well, and I made 51% on my investment. Thank you, guys (in the management). Now the company is a completely different animal, and after you have read my article, you know why I sold my whole position. I hope you will get value from my article and wish you a successful investing journey.

Q2 2024 Earnings Call Transcript")