spxChrome

Company Description

Legacy Housing Corporation (NASDAQ:LEGH) – Consumer Durables – Homebuilding

Founded in 2005, Legacy Housing Corporation (“the company”) is one of the leading manufacturers of prefabricated homes primarily operating in the southern United States. It offers a vertically integrated solution, from manufacturing to distribution (i.e., through 156 independent and 13 company-owned stores) and financing.

Legacy Housing Corporation’s mission is to address the growing demand for affordable housing in the United States fueled by increasing rental rates, elevated costs of site-built homes, and a refuse in homeownership among specific U.S. demographics. Specifically, the company targets customers with annual household incomes of less than $75,000, encompassing approximately ∿ 50%+ of all U.S. households according to the U.S. Census Bureau.

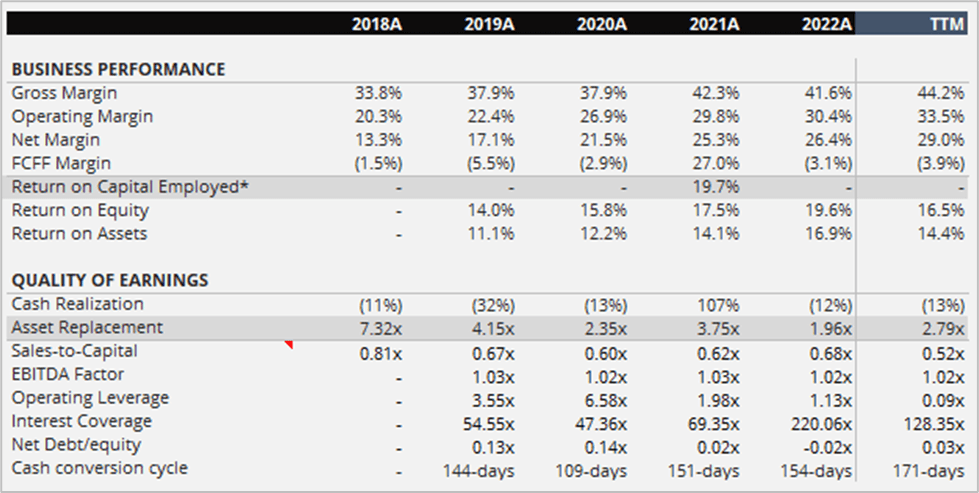

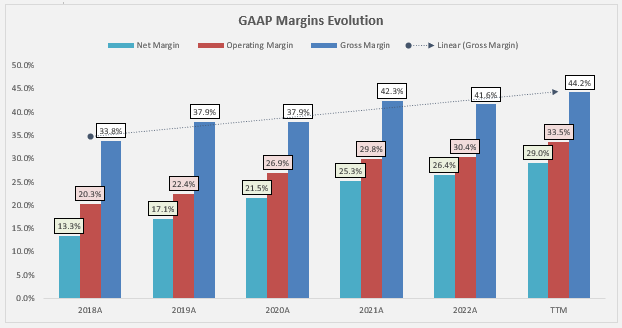

Business Performance

Classification – Fast Grower (i.e., Peter Lynch classification)

Legacy Housing Corporation is a capital-light (i.e., EBITDA factor of 1.02x TTM) business that, over the last four years, delivered an average ROE of 16.7% primarily driven by improving bottom-line margins.

Author’s Estimates

Income Statement

From 2018 to 2022, the top-line grew at a CAGR of 12.3% primarily driven by price/mix changes (i.e., average revenue per home manufactured being up ∿50%) rather than volume (flat around ∿ 3900 homes manufactured per annum), but even more impressive has been the growth in net income that averaged a CAGR of 33.2% driven by conservative management approach, cost-cutting initiatives, and higher capacity utilization among others.

Author’s Estimates

On a TTM basis, net income is down ∿1.1% YoY due to an industry-wide decrease in unit volumes that resulted in sales being down ∿10.1% YoY, partially offset by input cost deflation, efficient management of operating expenses, and the company’s ability to hold pricing steady by instead offering financing incentives.

Balance Sheet

The balance sheet is solid with an Interest Coverage ratio of 128.23x TTM. The cash conversion cycle stands at 171 days TTM (well above the historical 4-year average of 140 days), driven by lower turnover in A/R standing at 90 days (up from the historical 4-year average of 55 days) suggesting weakness on the demand side; and by higher turnover in A/P, suggesting low purchasing power with suppliers; partially offset by an improvement in inventory turnover currently standing at 95 days (vs historical 4-year average of 103 days).

Author’s Estimates

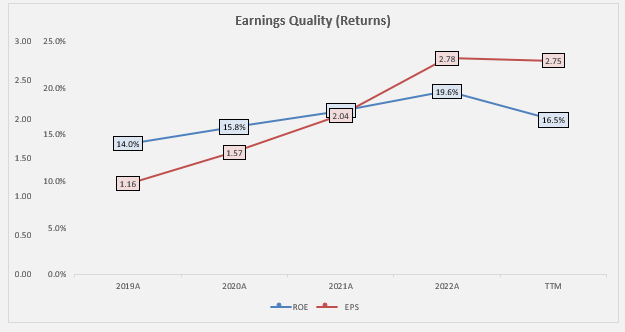

On the performance side, both ROA and ROE are above the 4-year historical average standing at ∿14.4% and ∿16.5% (above the cost of equity of ∿13.7%) respectively. In particular, ROE is driven by higher net margin, and lower financial leverage, and partially offset by lower asset turnover suggesting that the company is undertaking lower return investments.

Cash Flow Statement

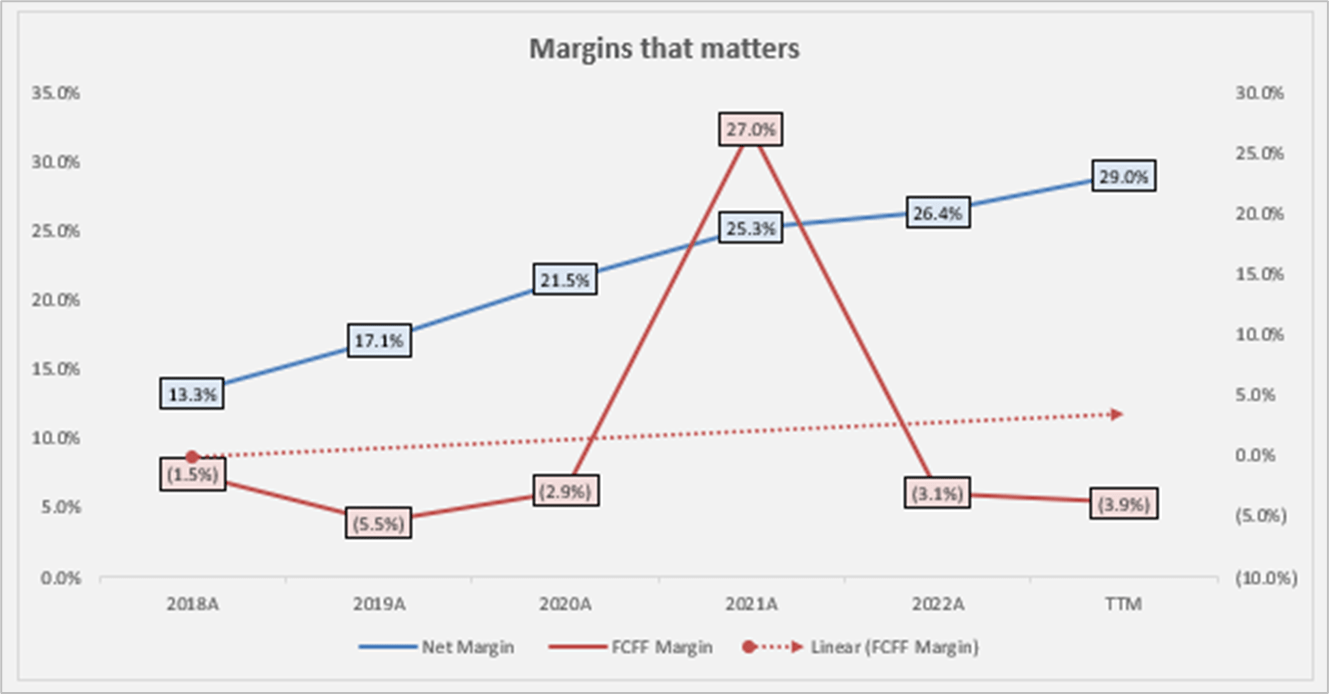

The business is capital-light with maintenance CapEx averaging ∿0.5% of sales per annum, and growth CapEx ∿1.9% over the last 5 years. In my opinion, the company is underinvesting, something that may boost a company’s financial performance over the short term, but it will hurt in the long run as delaying necessary investments may result in the company’s offerings becoming obsolete (i.e., lack of innovation), inability to capitalize on emerging opportunities (i.e., automation which can boost operational efficiency), and difficulty in attracting talent among others. Skyline Champion Corporation (SKY) for instance, one of the Legacy Housing Corporation’s competitors, seems to be more innovation-oriented with intensive R&D effort to build custom-designed automation technology to reduce labor requirements in physically demanding positions. Moreover, it invests in improving the online digital go through.

On the cash flow generation side, the performance seems to be very poor with the cash conversion standing at ∿-13.4% and FCFF margin at ∿-3.9% TTM. Furthermore, when comparing the operating cash flow trends of Legacy Housing Corporation to those of its closest competitors, such as Skyline Champion Corporation, it seems that the company is encountering difficulties in maintaining a positive operating cash flow. Skyline is demonstrating robust and consistently increasing cash flow, whereas Legacy Housing Corporation seems to be experiencing complete stagnation.

Author’s Estimates

In my opinion, the truth is somewhere in the middle. To conduct an apple-to-apple comparison we would need first to account for the fact that the company categorizes their investments in consumer and business loans within operating cash flows. Apart from that, it is also true that the working capital is managed inefficiently, something the company is aware of, as underlined during the 3Q23 earnings call:

“Our working capital is too high. We have too much raw material and finished goods inventory. We are working to reduce inventory and free up capital that can be reinvested back into the business.”

In summary, Legacy Housing Corporation, given its comparatively lower cash generation ability than competitors, faces constraints in financial flexibility for discretionary decisions, such as buybacks, and it needs external financing to preserve the expansion of its asset base.

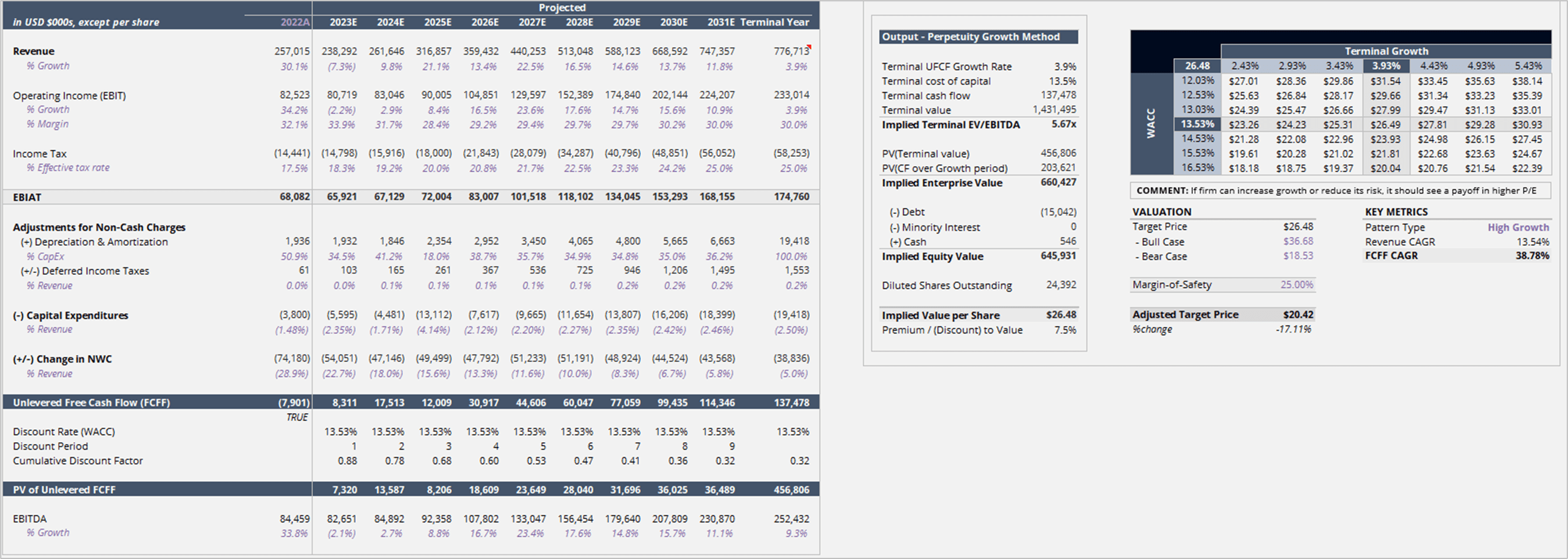

Valuation

Legacy Housing Corporation trades at a premium to its intrinsic value.

Author’s estimates

Under my conservative scenario, and incorporating a margin of safety of 25%, it suggests a target price of €20.42/share or a premium of 17.11% vs. the current price of €24.64/share. Under my scenario, I assume all three manufacturing facilities to reach their full potential, the opening of a fourth facility, operating leverage to drive strong free cash flow, and improved management of working capital among others.

However, once we differentiate Legacy Housing Corporation to its closest peers, Skyline Champion Corporation and Cavco Industries (CVCO) the company becomes more attractive. It currently trades at an EV/EBITDA of 7.36x TTM, which is below Skyline’s EV/EBITDA of 8.74x and Cavco’s EV/EBITDA of 9.03x TTM. In my opinion, the discount to peers is justified as both Skyline and Cavco, over the last 3 years grew their top-line 1.5 times faster, managed their working capital better, and are both cash-generative businesses with an FCF margin of 10.9 and 12.3% TTM respectively.

Catalysts

In my opinion, the following should represent a potential tailwind:

- Deterioration in housing affordability – as traditional housing becomes less accessible, the demand for more affordable housing options should grow.

- Easier immigration policies resulting in an increased flow of working-class immigrants in the Texas job market – the increased addressable population may drive demand for affordable housing solutions.

- Higher for longer interest rates – historically, higher interest rates have been associated with market share gains for manufactured housing.

Risks

There are a significant number of headwinds with the stock. In particular, issues by segment are:

- Deterioration in loan portfolio due to macro headwinds – macroeconomic headwinds could adversely impact the quality and performance of loans.

- Labor shortage – which may guide to increased labor costs, and potential delays in project timelines, hence, impacting overall profitability.

- Null to low switching costs – without significant barriers preventing customers from switching to competitors, the business is vulnerable to potential market share loss.

Final Remarks

In my opinion, Legacy Housing Corporation does not represent an appealing investment as it does not offer enough margin of safety.

In the long term, the analysis indicates that the company is well-positioned for strong performance. I believe the company can address working capital management issues effectively. However, the absence of significant barriers preventing customers from switching to competitors, coupled with the challenge of identifying a unique value proposition beyond price-affordability, makes me unwilling to invest in this company.

Q2 2024 Earnings Call Transcript")