Debt issued by publicly traded commercial real-estate investment trusts (REITs) has been in rally mode to start 2024, even in the battered office sector.

“Shopping centers were a four-letter word for a long time,” according to Alex Snyder, a portfolio manager who focuses on REITs at CenterSquare Investment Management. Now, in a post-pandemic remote-work environment, “office” is a dirty word, he noted.

But as office-vacancy rates surge in many cities and landlords face higher borrowing costs, Snyder also sees budding optimism around office-REIT debt, which is backed by the entire company, whereas the same borrower’s property-specific debt may still look pretty risky.

“Would I buy debt issued from 2015 to 2020 on a single-asset at par? There is no way,” Snyder said. “Would I buy corporate-office debt at a discount? Absolutely.”

Read: Big-city office buildings log 26% price drop from a year ago, report shows

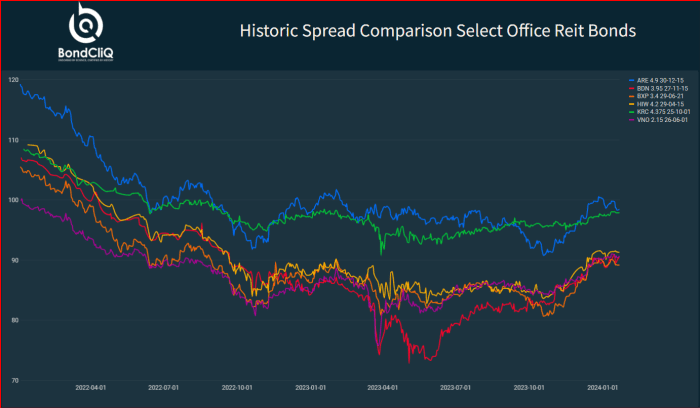

The following graphic shows the path of corporate-bond spreads for six major office REITs since the Federal Reserve began dramatically raising interest rates in early 2022.

Office REIT debt is rallying to kick off 2024.

BondCliQ

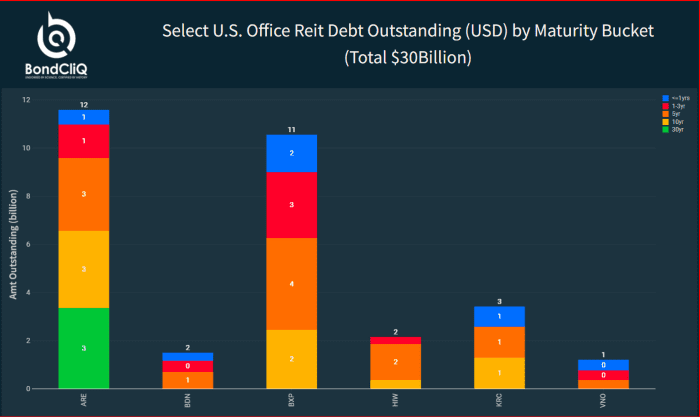

Office giant Boston Properties Inc.

BXP,

has seen its five-year bond spreads compress in January to about 90 basis points above the benchmark 10-year Treasury rate

BX:TMUBMUSD10Y

from roughly 105 basis points in early 2022, according to BondCliQ.

Boston Properties focuses on top-shelf office buildings in big cities. It has about $11 billion in outstanding corporate bonds, according to BondCliQ data. Its bonds due in five years or less have been trading at average yields of about 5% to 5.5%.

Office-REIT debt is maturing.

BondCliQ

Risk assets have rallied since Fed Chair Jerome Powell in December signaled that a pivot to rate cuts was likely in the coming months. The S&P 500 index

SPX

and Dow Jones Industrial Average

DJIA

have both now climbed above record levels set two years ago.

The new year also has brought a surprising wave of fresh bond issuance by REITs, including from office landlords with exposure to cities slow to recover post-COVID.

The first three weeks of January saw $5.8 billion in corporate-bond issuance from REITs, more than the supply seen in January in each of the past four years, according to Informa Global Markets.

Among the issuers was Kilroy Realty Corp.

KRC,

a REIT focused mostly on Class A properties in Los Angeles, San Diego and the San Francisco Bay Area, which borrowed $400 million through a 12-year bond deal at a roughly 6.25% coupon.

“That’s really strong pricing,” said Snyder, especially considering ongoing uncertainty around office-property debt and also given how bond issuance from office REITs had largely stalled in the past year.

Meanwhile, the Dow Jones Equity REIT Index

XX:DJDBK

has climbed more than 18.6% in the past three months, even as it’s slipped 1.5% lower on the year so far, according to FactSet.

Kilroy and Boston Properties did not immediately respond to requests for comment.

Q2 2024 Earnings Call Transcript")