z1b

Introduction

I wrote an article on Kroger (NYSE:KR) back in October where I talked about 5 reasons the stock was worth owning. Since then the stock has been trading sideways with some volatility here and there. Today (time of writing) the company reported its Q3 earnings. This caused the stock to dip below $43 and I gladly added to my position. The market has been tough on a lot of companies lately. Some have even beat on EPS and revenue and still experienced a drop in share price. In this article, I talk about why the company experienced some volatility after their recent earnings report, and why I bought on the dip.

Why The Quick Drop In Price?

Kroger reported its Q3 earnings and in my opinion did fairly well. They beat analysts’ estimates on both EPS and revenue which is great all things considered. As many companies have been having trouble in the current macro environment, beating on both EPS and revenue isn’t easy right now.

admire Mike Tyson said, “Everyone has a strategize until they get punched in the mouth.” Or admire the saying goes, Everyone is great when they’re not tired. In this case every company can supply a beat or look stellar when the economy is thriving. But with rates high, geo-political issues, and tight financial conditions for consumers, it isn’t easy to do well right now. Or to look good doing it. The market in my opinion is being tough on a lot of businesses right now.

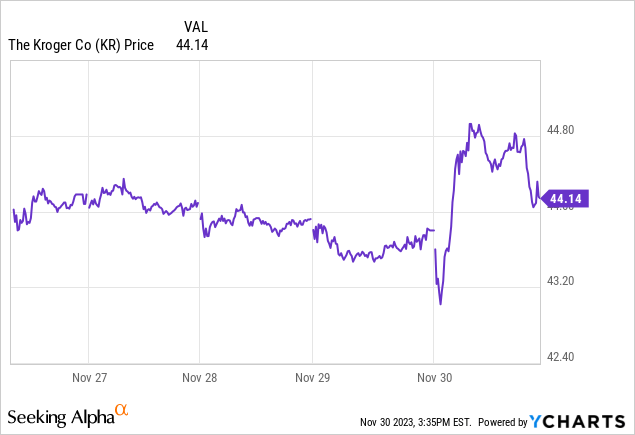

2023 has shaped up to be a wild ride for many companies. And I think 2024 will be more of the same, at least in the first half. I say this because I think rates will start to ease then. But I’ve heard some people say 2025. And I wouldn’t be surprised if that is true. As you can see, Kroger dropped quickly and I was actually hoping it’d hit a new 52-week low. I’ve had a limit order of $41.99 in for quite some time and was hoping it would trigger today.

Instead it hit a low of $42.86, close to its 52-week low of $42.10 but not quite. The stock quickly rebounded above $44 and is currently trading at $44.14 at the time of writing. So, why the quick rebound? Well, for one Kroger is a high-quality business who is also trying to continue on its path to growth. One way is the merger with Albertsons (ACI). The merger was announced some time ago but the two companies have been dealing with some road blocks from the Federal Trade Commission. They received a second compliance inquire and the companies planned to comply.

The deal was expected to close early next year but I honestly think it will be quite a while before this happens, if it does. I think the pending merger is also a reason for the stock trading sideways. Investors are wondering if the deal will be approved. During a call with Agree Realty’s (ADC) CEO, Joey Agree, I asked him his thoughts. He said he honestly doesn’t think it will go through. As a KR investor, I hope it does.

Q3 Earnings Report

KR reported earnings of $0.95, beating analysts’ estimates by $0.03. Revenue of $33.93 billion beat estimates by $60 million. Identical sales without fuel declined 0.6% and adjusted FIFO profit was also lower at $1.02 billion, lower than the consensus. This was also a reject of nearly 7% from $1.09 billion a year ago. FIFO operating profit now is expected to be between $4.9 billion to $5 billion, a slight decrease from $5.1 billion last year. Despite this, the company raised the lower end of its guidance, adjusting full-year slightly. EPS is now expected to be between $4.50 to $4.60 vs $4.45 to $4.60. Although they slightly adjusted full-year guidance, at mid-point this would still represent nearly 7% growth from 2022’s full-year EPS of $4.23. Which I expect the company to easily exceed the lower-range of $4.50 because of the usual extra spending during holiday shopping.

Companies may miss on EPS or even revenue but disappointing on same-store sales can sometimes provoke volatility, at least for the short-term. It’s no secret consumers are spending less. Why? Because financial conditions are tight. That’s one purpose of the rise in interest rates. To make consumers spend less. When things are going fine and the economy is booming, consumers spend money admire there’s no tomorrow. So, the company beat on earnings and revenue, adjusted full-year guidance, and still dropped? I read a comment on SA earlier: The market is tougher than a $2 steak. I thought that was funny. But it’s true, the market is seemingly harder on companies right now. And I expect this to continue into 2024.

Things get more expensive and that extra pack of steaks or tub of ice cream isn’t worth buying anymore. This also causes consumers to look for cheaper alternatives. Take it from me, I’m one of them. I recently wrote an article on T-Mobile (TMUS). In it I mentioned that I recently switched to the provider from Verizon (VZ). Why? Because their service was cheaper.

So although inflation seems to be moderating, customers are still managing macroeconomic factors. Higher rates, reduced savings, surging credit card debt, and fewer government benefits are all contributors to tighter financial conditions. And until rates subside many businesses, especially brick-and-mortar, will face headwinds.

Future growth

Kroger is a business that has a lot of potential and room for growth. One way we know these businesses grow is by opening more stores. Another way a lot of these companies capture growth is through their rewards programs and omni-channel platforms. In Q3, KR saw double-digit growth in its digital business. Digitally-engaged households grew 13% in Q3 alone. In their Kroger rewards program customers were able to save 14% more in rewards for fuel. The company saw an boost to $0.57 vs $0.50 year-over-year in cents per gallon fuel margins.

Although inflation is moderating, I think the way consumers shop is forever changed now. Especially with 0% interest rates said to be no more. When rates do decrease I think customers will still be conscious of spending thanks to the pandemic. But Kroger offers customers who are budget-conscious a lot of value. One example was this past holiday. The company created a meal bundle to feed a family of 10 for less than $5 per person, which was lower than the year before. KR also saw an boost in budget-conscious customers in the quarter as Q3 marked the 10th consecutive quarter of household growth.

This coupled with forever-changed spending habits will only benefit them with sustainable growth in the future. Furthermore, Kroger Health also experienced a strong quarter as well and remains a profitable growth component for the business. In Q3, the team exceeded the number of vaccinations expected to be administered, which drove profit margins higher. With the momentum in health & wellness, there’s significant potential growth for KR in the future.

Impressive Total Returns

Here I differentiate Kroger to larger retailers Walmart (WMT) and Costco (COST). I know both companies are much larger, but the smaller grocer holds their own against the two looking out beyond the past year. Over a 1-year time period both stocks are in the green while KR is down nearly 9%. In my opinion, one reason for this is the pending merger. But looking out beyond that in a 3, 5, and 10-year period, the smaller grocer beats WMT over a 3 and 10 year period.

Even in 5 years they don’t trail the world’s largest grocer by a significant amount. KR total returns are nearly 64% compared to nearly 74% for WMT. But over a 3 and 10 year period, they outperformed them at 40.88% compared to just 7.01%. In 10 years, total returns are closer with Kroger still beating them out at 163% compared to 140% for the latter. COST beats both pretty handily over all periods. Probably why it was a favorite and large holding in the late Charlie Munger’s portfolio.

Seeking Alpha

Valuation

At a P/E of just 10x, KR’s valuation is very attractive here. It is both below the sector median and its 5-year average of 12x. Any stock of KR’s caliber trading at just 10x earnings is a steal in my opinion and that’s why I added to my position today. And I strategize to continue adding as the price dips below $44. I expect the stock to continue experiencing volatility in the coming months pending approval of the merger.

For my valuation I use the Dividend Discount model and January 2025’s dividend calculate of $1.17 as per Seeking Alpha. KR actually has some pretty impressive dividend growth over a 5-year period of 14.38%. But being conservative as I always am, I use an expected rate of return of 8%, and a growth rate of 6%, significantly lower than the 14.38%. Reason being is I expect the company’s margins to continue to be squeezed for the foreseeable future due to the looming recession and macro environment. This gives me a price target of $58, above their current price target of $51.

Author

Risk Factors

The current macro environment and tighter financial conditions will remain a huge risk in the foreseeable future as long as rates remain elevated. As management stated during earnings, customers are actively seeking value and this will continue going forward.

Another risk that poses a threat to the company is the recent development and popularity of GLP-1 drugs. In Q3, management stated they saw rapid growth of these drugs in their retail pharmacies. The effects it can have on the business remain unknown for now. KR also noted that the patient data in their pharmacy operations is separate and is protected by privacy laws. But management thinks their “Food as medicine” philosophy positions them well. If these drugs continue to gain popularity, it could potentially have a large effect on grocers admire KR.

Bottom Line

Kroger is severely undervalued at just 10x earnings which is hard to find in this overvalued market. Many stocks still trade well-above 20x earnings even with the sell-off in some sectors in recent months. I think the pending merger is suppressing the stock price at the moment. Additionally, the stock has attractive total returns over a 3, 5, and 10-year period making them even more attractive along with its valuation. I expect the stock’s price to trade between $43 to $45 pending the merger. If the merger gets pushed or disapproved I expect them to go through a advance price reject. But either way if the merger gets approved or not, I think Kroger is a buy.

Q2 2024 Earnings Call Transcript")