Stanislav Maliarevskyi/iStock via Getty Images

Today I continue my quest to identify the best dividend companies in the market, analyzing Kontoor Brands (NYSE:KTB). Kontoor Brands is the parent company of two renowned brands: Wrangler and Lee which are mainly known for their denim products. Even though the company has some positive prospects, I see some major headwinds coming in the future and I would wait for a better time to buy.

I am going to discuss the stock price and the company’s business, I will talk about the company’s financials focusing on the latest Q4 2023 results, analyze possible growth catalysts and risks and I will finally conclude with a quick valuation.

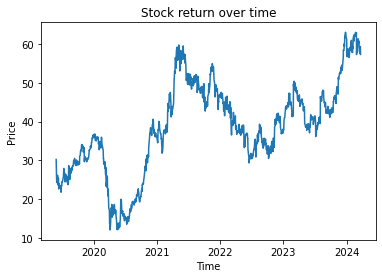

Stock Price

After the spin-off from V.F. Corporation (VFC) in 2019, the stock price increased by around 40% while in the same period the S&P 500 appreciated by around 81%. The underperformance of a stock in comparison with major financial indexes is a red flag, suggesting that investing money should be considered only after a major stock price decrease to maximize potential gains.

Stock price quotation over last 5 years (Author’s Python script using the library: Yfinance )

Company’s Business

Overview

The company manufactures and markets a wide variety of clothes under the brands: Wrangler and Lee, with a focus on denim. Over the years, the company was able to leverage its brand’s strength to establish a global presence.

The company’s revenues come from three different distribution channels:

- U.S. Wholesale, which accounts for around 72% of total revenues over the last fiscal year. This section includes all revenue coming from mass and mid-tier retailers, department stores, and e-commerce like Amazon (AMZN).

- Non-U.S. Wholesale, comprising around 16% of total revenues. The company’s global presence is primarily concentrated in developed markets.

- Direct-to-consumer sales account for the remaining 12% of total revenues and encompass both branded full-price and outlet stores.

I am concerned about the overexposure of the company to the U.S. Wholesale. Wholesale. In 2023, sales to the company’s top ten largest customers represented approximately 62% of total revenue, with Walmart alone accounting for about 36%. I may consider upgrading the stock whenever I notice a rebalancing between these three categories and an increase in online sales.

Manufacturing

Kontoor Brands adopts a dynamic manufacturing approach, leveraging a blend of in-house facilities and strategic partnerships with third-party manufacturers. Across several locations worldwide, the company operates its manufacturing facilities, focusing particularly on the production of its denim products. However, recognizing the necessity for scalability and agility in meeting market demands, Kontoor Brands also collaborates with external manufacturing partners.

This dual strategy empowers the company to uphold stringent quality standards while ensuring operational flexibility and efficiency. By retaining control over a portion of its manufacturing processes, Kontoor Brands can check product quality and craftsmanship. Meanwhile, engaging with trusted third-party manufacturers enables the company to effectively scale production and meet fluctuating market demands without compromising product quality.

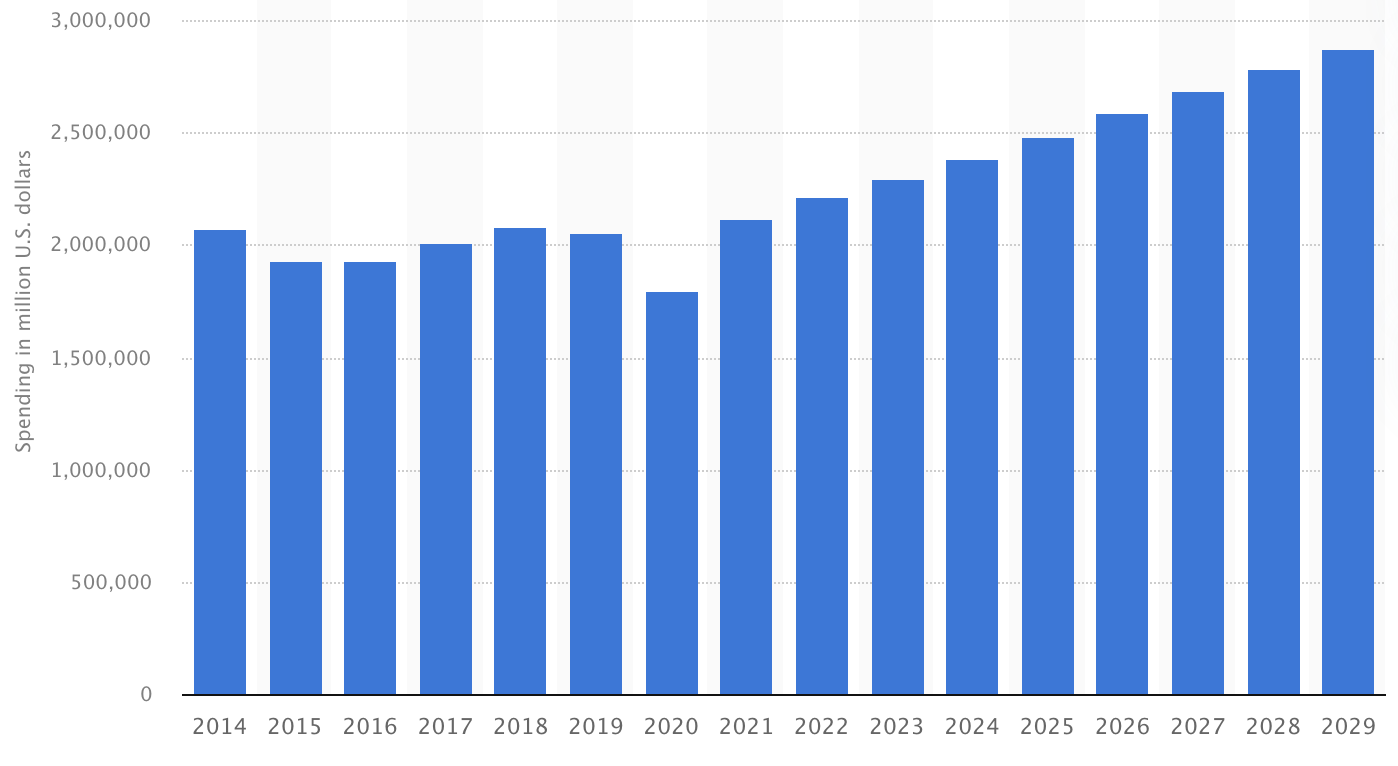

Clothing Industry

Kontoor Brands operates within the broader apparel industry and competes in the lifestyle apparel market, in particular in the denim and casualwear segment. The clothing industry is expected to grow around 20.5% in the next five years mainly driven by inflation and population growth.

While the long-term prospects for Kontoor Brands appear promising, with the potential for growth outpacing the market, I anticipate challenges in the short term. During the latest conference call, the management team indicated that they expect flat revenues for 2024. This forecast is concerning, especially considering the decline of approximately 8% observed in Q4 2023.

Industry forecast (Statista.com)

Company’s Financial

Income Statement

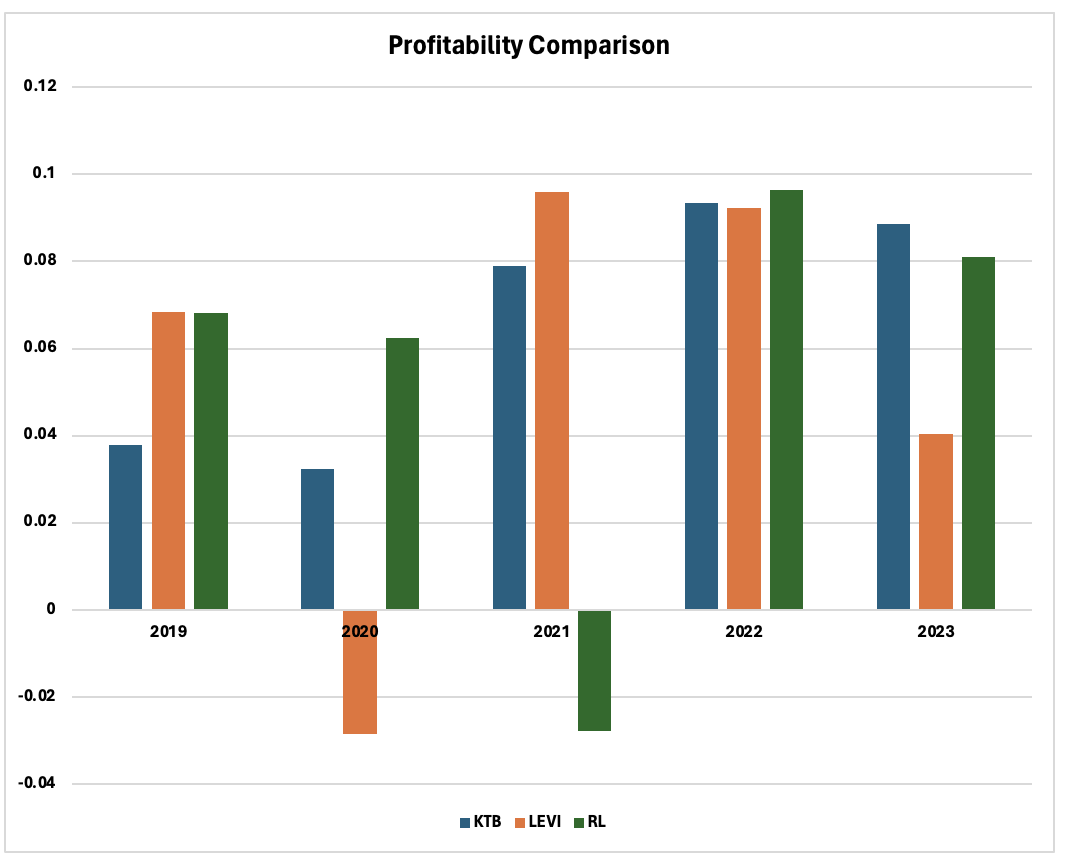

Despite the decrease in revenues, the company is improving its margins. When compared to two of its peers, Levi Strauss (LEVI) and Ralph Lauren (RL), the company has transitioned from being the worst-performing to becoming the best in class.

However, a huge concern arises: if the corporation fails to increase its top line, there may be limited potential for further improvement in the bottom line. This is because Kontoor Brands has already achieved a commendable net margin, which is considered to be at a good level within the industry. In fact, the company holds an A- profitability grade on Seeking Alpha.

Profitability comparison (Author’s Excel sheet)

Balance Sheet

The debt level is acceptable and it is decreasing. Considering the last data, it would require only 3.4 years to repay the total debt with the free cash flow level reported.

The company currently has more than $215 million in cash and equivalents and, as reported during the last call by the CEO, Scott Baxter, managers do not exclude an M&A operation in the future. I consider an acquisition a good idea at this point, it could potentially benefit Kontoor Brands by allowing management to leverage possible synergies and economies of scale. By integrating a new business into its operations, Kontoor Brands could diversify its product offerings, expand its market reach, and drive incremental revenue growth.

Cash Flow Statement

Kontoor can generate a good amount of cash every year. Its capital expenditure level is rather low to other companies and oscillates around 1% of total revenues. This data makes it very easy to make future possible free cash flow projections. The free cash flow produced is used to reward shareholders through dividends and share repurchases.

The company just reported an outstanding $357 million in cash generated from operations while it is expecting to go back at around $325 million for 2024. This is the most worrying data for an investor, it means that the corporation is going to go through difficulties mainly driven by a tough macroeconomic scenario that is lowering the overall consumer spending. Investors will have to carefully pay attention to this data over the next 12 months to check for any possible business detriment.

Growth Opportunities

As I discussed in the business overview section, the company is overly reliant on the U.S. market while both Europe and Asia represent a marginal part of total revenues. During recent conference calls the managers reiterated their cautious approach towards an expansion in these areas due to short-term economic softness. However, they expressed optimism that with the anticipated reduction in interest rates and the overall economy rebounding to a decent growth level, the company will intensify its efforts to expand in these areas.

In particular, the company is focused on China and managers have repeatedly expressed their enthusiasm for the company’s operations in the country:

As that market starts to open back up and develop, we feel very bullish about that long-term.

In particular, I am glad to notice that the company is focusing on direct-to-consumer channels which, in my opinion, is better than wholesale because it allows Kontoor to have stronger control over consumer experience and typically yields higher margins. During 2023 revenues from DTC increased around 9% while total sales decreased by 1%.

Risks

A complete list of risks is reported in the company’s 2023 financial report.

The main risk when it comes to Kontoor Brands is the macroeconomic environment, at least in the short term. Given the current scenario where inflation persists higher than expected, there’s a possibility that the Federal Reserve may delay lowering interest rates, impacting consumer spending on clothing. In such a situation, consumer expenditure on apparel may remain lower than anticipated throughout the year, potentially causing the company to report numbers lower than forecasts.

Another risk is the exposure that the company has towards some specific clients such as Walmart and Target which represent a huge portion of total revenues and expose the company to a very high risk, as any adverse developments with these key retailers could significantly impact Kontoor Brands’ financial performance. To mitigate this operational risk, I anticipate that the company’s management will focus on diversifying its customer base. By expanding its partnerships with additional retailers and exploring opportunities in different distribution channels, Kontoor Brands can reduce its dependence on any single client and enhance its resilience to market fluctuations.

Valuation

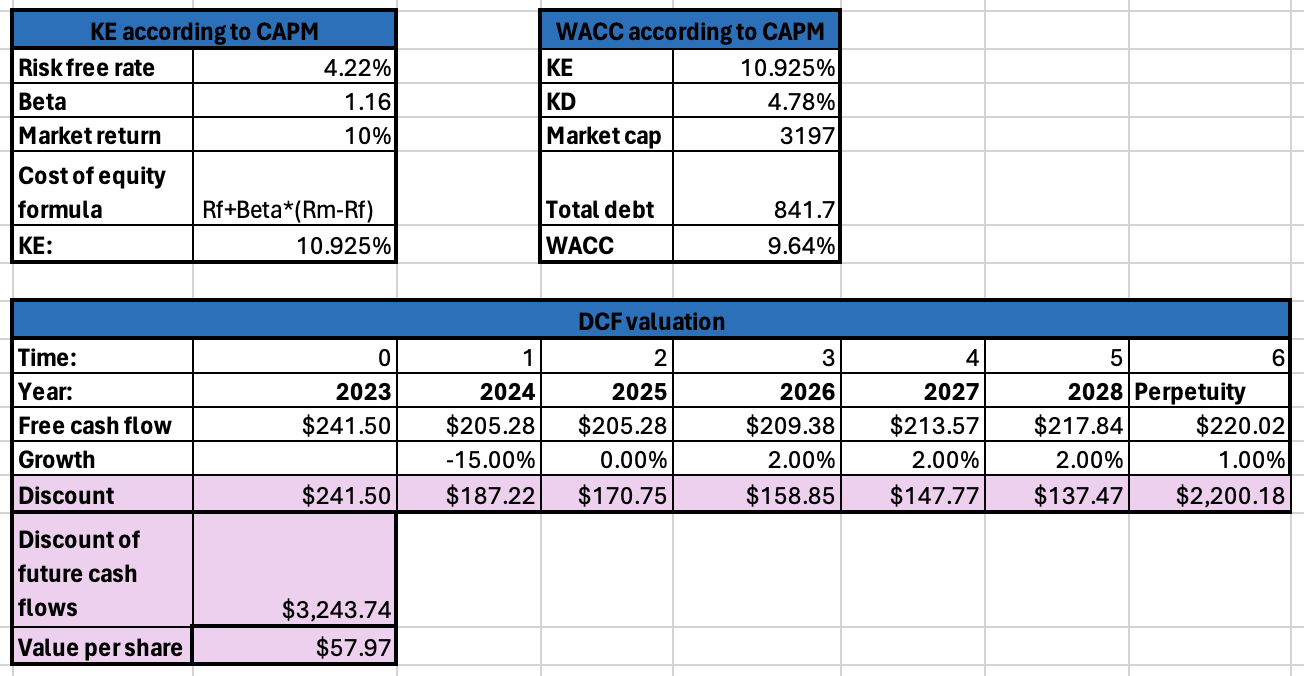

Since the company has a reliable free cash flow I decided to evaluate it through a discounted cash flow model.

Through the formulas reported below, I obtained a 10.93% as the cost of equity and 4.78% as cost of debt. I made a weighted average considering the company’s market cap and the company’s equity and I obtained a weighted average cost of capital (WACC) of 9.64% which I used as a discount factor.

Considering the expected decline in revenue and operating cash flow for next year and the capital expenditures that oscillate around 1% of total revenues I projected the future free cash flow and then discounted it back. Assuming a 1% as terminal value I obtained a fair value of $3,243 million, in line with the current valuation.

Company’s valuation (Author’s Excel Sheet)

Considering that the company does not have an economic moat or a clear competitive advantage with respect to its competitors and that it is facing some difficulties, I prefer to wait on the sidelines for a stock price decrease before investing in this company.

Conclusion

As both the market and the company’s stock are trading at all-time highs, I perceive Kontoor Brands as too risky. Additionally, considering potential future challenges, primarily related to the macroeconomic environment, I rate Kontoor Brands as a “hold” while awaiting clearer signals.

I would be inclined to reconsider my stance if the company decides to utilize a portion of its liquidity for a new acquisition. Such a move could inject fresh momentum into the business and potentially enhance profitability through economies of scale and synergies.

Q2 2024 Earnings Call Transcript")