WendellandCarolyn

Kite Realty Group Trust (NYSE:KRG), founded in 1960 and headquartered in Indianapolis, IN, is a REIT that owns, acquires, (re)develops, and operates open-air shopping centers and mixed-use assets across the country.

With a very well-diversified portfolio, remarkable recent growth, and a healthy solvency profile, this REIT seems to have a lot of potential. Additionally, its shares are trading at a significant discount to its NAV and the dividend yield appears to be relatively safe.

Portfolio & Performance

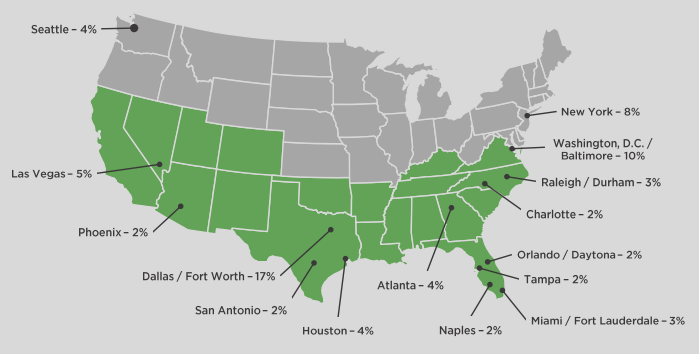

As of September 30, 2023, the REIT owned interests in 170 operating retail properties and 10 mixed-use assets, aggregating ~28.3 million sqft, located in 9 states.

Investor Presentation

The portfolio is mostly exposed to the state of Texas with a 26% exposure based on ABR, followed by Florida with an 11% exposure. It also has a 67% concentration in the Sun Belt.

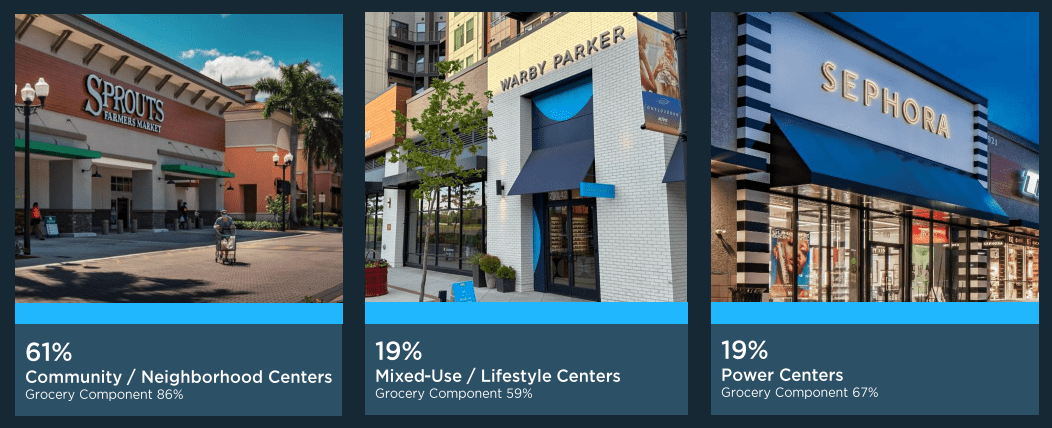

The properties are diversified based on the property type as well, with the grocery component being sovereign in all of them:

Investor Presentation

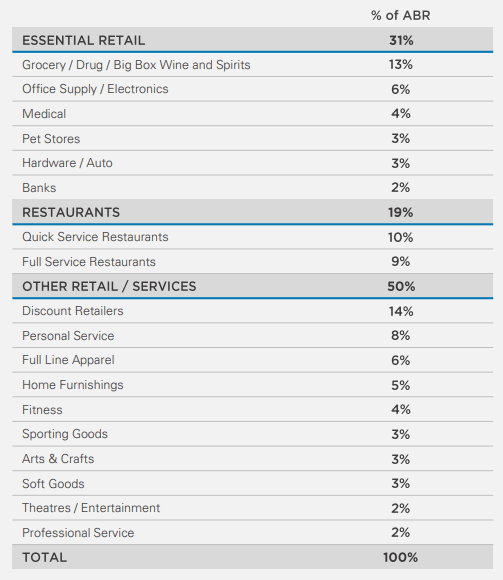

Its tenant base is also diversified, with 31% exposure to essential retail businesses, 19% to restaurants, and 50% to industries with a risk level between those two:

Investor Presentation

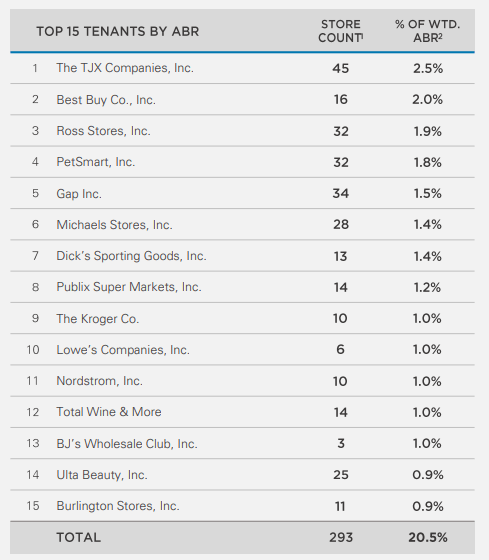

Moreover, it’s good to see that no tenant represents a large piece of ABR, with the top one contributing only 2.5% to it:

Investor Presentation

Now, the properties had a 91.6% occupancy in the third quarter of 2023, just 30 bps lower on a YoY basis. At the same time, same-store NOI marked a YoY 4.7% increase in 2023Q3. And as a result of the outperformance, management increased its same-store NOI growth guidance from 3.5% to 4.5%, as well as its FFO guidance by $0.03 per share.

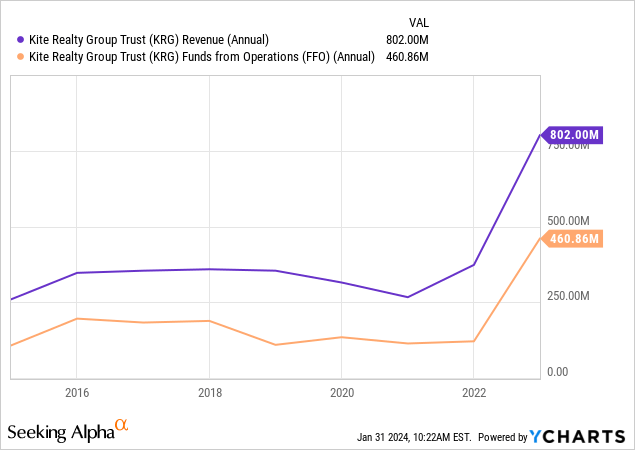

Zooming out a little, it seems that recent results greatly surpass those of the last couple of years. Below, I compare the increase from the average annual figures in the last 3 fiscal years to the last quarterly report’s figures annualized:

| Rental Revenue Growth | 73.93% |

| NOI Growth | 60.98% |

| AFFO Growth | 114.59% |

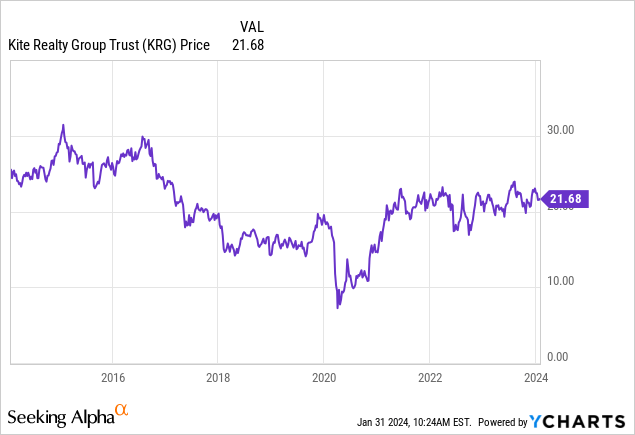

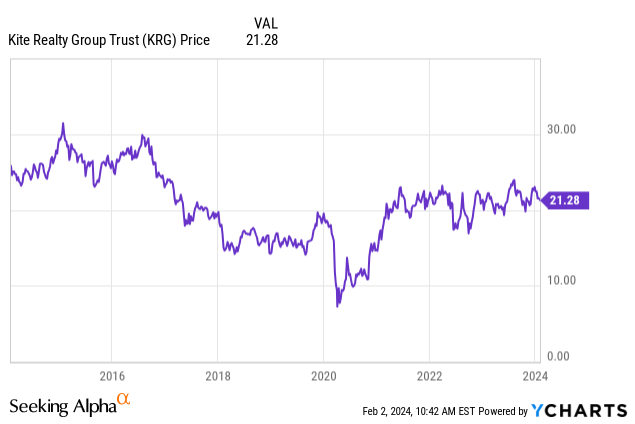

Going further into the past, however, it seems that the recent growth was not an extension of a long-term trend:

And as expected, the market has behaved accordingly:

Leverage & Liquidity

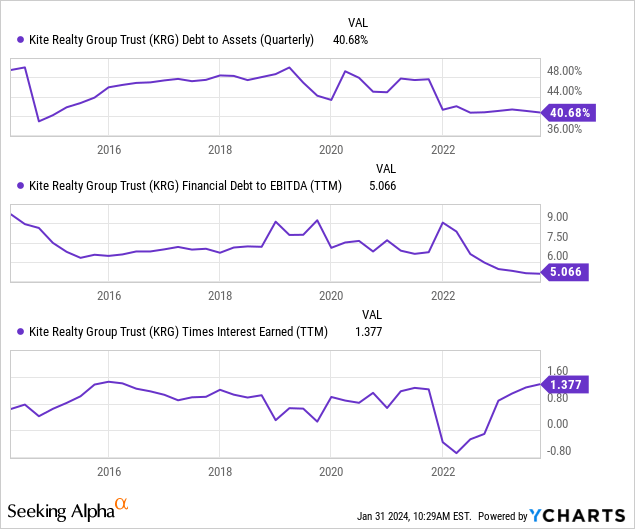

When it comes to its use of leverage, however, it seems to have been low for a long time. First, only 40.68% of its assets are financed by long-term debt. And its debt/EBITDA ratio is a very healthy 5x, which also depicts strong liquidity (an interest coverage of 1.3x helps in this too).

With a weighted average interest rate of 4.35%, the company also exhibits a low cost of debt these days since 93% of its debt is structured as fixed-rate. It’s also good to observe that the maturities for the next couple of years don’t represent a large portion of the total debt:

Investor Presentation

Dividend & Valuation

Kite Realty pays a quarterly dividend of $0.25 per share, which reflects a 4.72% forward yield. While this is a bit low these days, I think it is relatively safe for a dividend portfolio. They may have cut it two times in the recent past, but they have been raising it so fast in the last 4 years that it’s going to get back to the level it was back in 2019 very soon if they continue with that pace.

Seeking Alpha

At the same time, the payout ratio based on AFFO is 63.89%, a low enough level that leaves a good margin for more hikes and room for the business to expand.

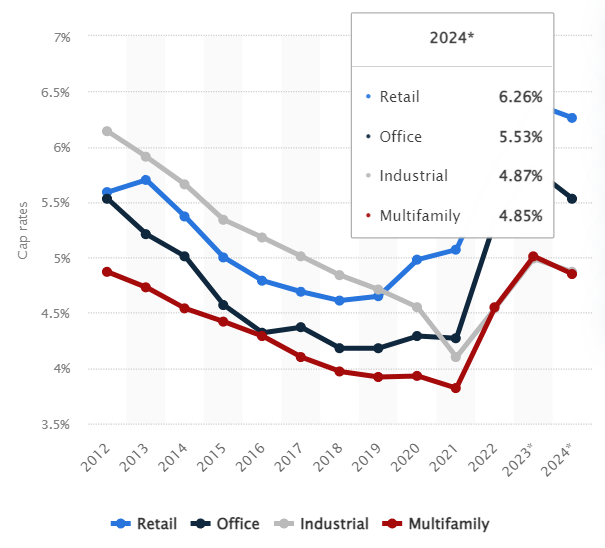

But most importantly, the shares of this REIT are trading at an implied cap rate of 7.34%. I think that with retail properties forecast to average a 6.26% cap rate in 2024, KRG looks undervalued right now.

Statista

Using that average, the discount to NAV ($27.04) is 21.69%, which reflects a good deal considering that there’s nothing seriously wrong with the business.

And while it has been a stranger to such a level since 2016, we should remember that the market only seemed to follow a trend of decreasing profitability. But that changed recently and not even the Fed rate hikes starting in 2022 were able to significantly disrupt the reversal (which you don’t see often with REITs).

Risks

The first risk has to do with the estimated NAV which could prove optimistic given a potential expansion of retail cap rates or a decline in the REIT’s NOI. While these scenarios seem unlikely, they nevertheless pose a risk to the accuracy of NAV calculation. Investors should make sure they monitor both cap rates and Kite’s operating results from quarter to quarter.

Additionally, there is an opportunity risk here. If the anticipated upside is not realized within a reasonable timeframe, the dividend returns may fail to compensate for the opportunity cost incurred; as we’ve already seen the yield is low right now.

Verdict

However, I believe KRG represents an opportunity within the REIT market and, therefore, deserves a buy rating at the moment. I like looking at the long-term picture, but if a turnaround is evident, as is the case here, it may not be relevant anymore.

What do you think? Did you find this useful or not? Don’t hesitate to let me know below. Thank you for reading!

Q2 2024 Earnings Call Transcript")