Michael Burrell/iStock via Getty Images

Stock Snapshot

With cold season here in many parts of the world, many of us are going through many boxes of Kleenex tissues lately. In that light, today’s research note covers the parent company of that brand, Kimberly-Clark (NYSE:KMB).

Some quick facts about this Dallas Texas-based company are that they are in business +150 years, saw +$20B in sales in 2022, have a brand reach in 175 countries, and 45,000 employees worldwide.

Besides being behind the Kleenex brand of tissue boxes, it also owns Cottonelle toilet paper, Scott paper towels, Huggies diapers, and Kotex tampons, among other things.

The common theme here is that these are household brands found in supermarkets across America, but more importantly they are consumables that need to be replenished frequently, driving continued demand for products appreciate this as a household necessity.

Scoring Matrix

This article uses a 9-point scoring matrix that holistically considers multiple angles of the stock, with an emphasis on dividend-income potential for investors and fundamental trends from the key accounting statements such as the balance sheet and income statements, as well as a future-looking outlook on this stock.

I continue to evaluate this methodology in my own portfolio, on stocks I don’t cover here, and it is my standard for building a long-term dividend-income portfolio that grows each year. So, I personally have a capital stake in this approach being successful.

Today’s Rating

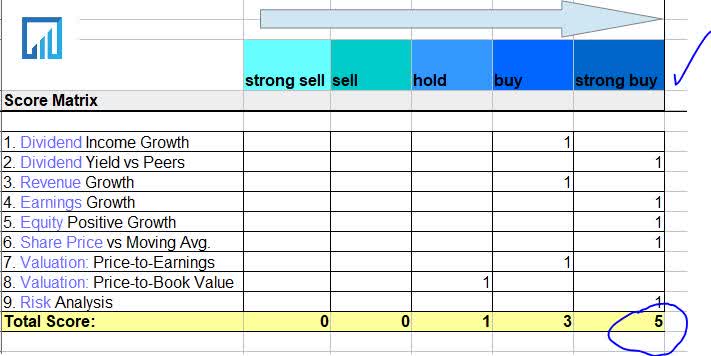

Kimberly Clark – score matrix (author analysis)

Based on the score total in the score matrix above, this stock is getting a rating of strong buy.

Compared to the consensus rating on Seeking Alpha, I am being more bullish than the consensus which appears to be neutral and cautious.

Kimberly Clark – rating consensus (Seeking Alpha)

Dividend Income Growth

This section uses dividend growth data to explores the 10 year dividend income growth for a hypothetical investor owning 100 shares, to ascertain whether this stock is a great dividend income opportunity.

Kimberly Clark – dividend 10 year growth (Seeking Alpha)

What this data tells us is that the annual dividend went from $3.11 in 2013 to $4.64 in 2022, a 49% growth over 10 years.

So, a 100-share position in this stock would have achieved $311 in annual dividend income in 2013, growing to $464 by 2022.

If we extrapolate to 2032 using that same growth rate, which of course is not guaranteed, we assess an annual dividend of $6.91 in 2032 ($691 dividend income), a 122% growth vs 2013.

For this reason, I will call this a buy, on the basis of positive dividend growth in the last decade but also a continued commitment this year to return capital to shareholders.

According to their Q3 release this October:

The company returned $1.3 billion to shareholders through dividends and repurchases.

Dividend Yield vs Peers

This section uses dividend yield data to contrast the trailing dividend yield vs 2 or 3 similar peers in the same sector, to ascertain if this stock presents the most competitive dividend yield on capital invested.

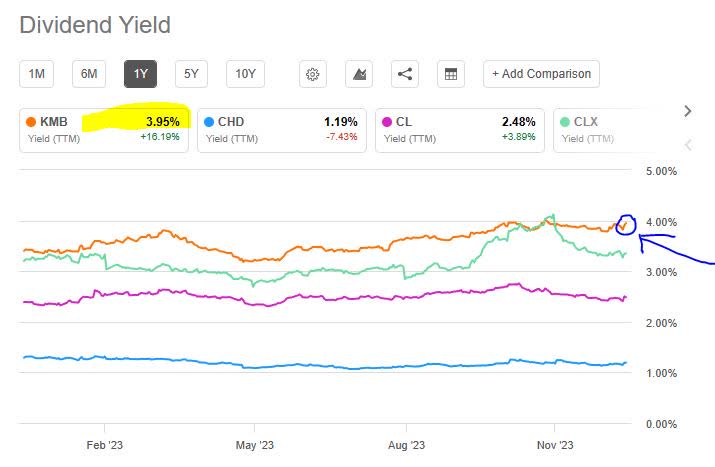

Kimberly Clark – dividend yield vs peers (Seeking Alpha)

In the chart above, which is one of the tools provided by Seeking Alpha, I am comparing my focus stock Kimberly-Clark with three peers in the consumer products segment.

These are Church & Dwight (CHD), Colgate-Palmolive (CL), and Clorox (CLX). What these all have in common is that they are the parent companies behind long established brands we shop for in the supermarket, and they produce consumables (tissue, toilet paper, toothpaste, etc.) which households have to keep refilling every so often, so the steady demand is there.

In this peer group, Kimberly Clark led the pack with a trailing dividend yield of 3.95% (same as its forward yield), while Church & Dwight was last in the bunch with a yield of 1.19%.

Also notable is the history of steady and uninterrupted quarterly dividend payouts from this company, and a quarterly dividend per share of $1.18 currently.

I will call this a strong buy in this case, on the basis of nearly 4% yield vs key peers as well as dividend stability and a quarterly payout of +$1 per share.

Revenue Growth

This section explores this company’s revenue growth trends over the last year, using data from the income statement.

What we can learn from this data that is relevant to an investor is that total revenue grew to $5.13B in Q3 vs $5.05B in Sept 2022, a positive but slight +1.5% YoY growth.

Gross profit grew even better as it saw $1.83B in Q3 vs $1.54B in Sept 2022, an +18% YoY growth.

As to some drivers of this success, the company in their Q3 presentation spoke of “continued sequential improvement in volume and gains in price/mix.”

advance, we can see that the tissue business saw growth momentum in FY23:

Kimberly Clark – top line growth (company Q3 results)

Also notable to cite is that their full-year outlook for top-line growth was revised upward, as was the outlook for operating margin and adjusted EPS growth:

Kimberly Clark – fy23 outlook (q3 results)

In this category, I will call this one a buy, on the basis of positive but low YoY revenue growth, impressive gross profit growth, and an improved top-line outlook for FY23.

Earnings Growth

This section explores this company’s earnings (net income) growth trends over the last year, also using data from the income statement.

What this metric tells us is that the company saw net income (earnings) of $587MM in Q3 vs $467MM in Sept 2022, a +25% YoY growth.

Looking at the longer trend of profitability, the company had improved earnings in three of the last four quarters vs the quarter ending Sept 2022.

One notable cite, particularly in the current high interest-rate environment and high cost of debt financing, is that their interest expenses dropped to $56MM vs $69MM in Sept 2022, a 23% YoY reject.

Total operating expenses, however, did enhance on a YoY basis.

What the company had to say in their Q3 release about non-interest costs were:

$75 million in lower input costs, partially offset by other manufacturing costs of $30 million, planned increases in marketing, research and general expenses, coupled with higher incentive compensation levels. Unfavorable currency effects impacted operating profit by $135 million during the quarter.

In this category of earnings I will call it a strong buy, on the basis of double-digit YoY earnings growth, declining interest expenses, and the EPS growth outlook adjusted upward for FY23. As far as earnings sustainability going into 2024, since they produce “essential” household items that get consumed and replenished regularly, there is a natural demand.

We also saw the effects of the toilet paper craze during the pandemic year, when supermarkets were running out of it due to hoarding. In my opinion products appreciate these are a must-have on grocery shopping lists, along with diapers for those with kids. However, there is also competition. So, if input costs continue to fall in 2024 I think it could direct to more stable prices for the end customer, causing more buying perhaps.

An interesting article from BBC in June highlighted how a major supermarket chain in Britain cut toilet paper prices due to the falling price of pulp, which is used to make the paper.

Equity Positive Growth

This section explores this company’s equity (book value) growth trends over the last year, using data from the balance sheet.

Impressively here too, the company grew total equity to $840MM in Q3 vs $583MM in Sept 2022, a +44% YoY growth.

An impact to equity is long-term debt, and for this company it actually declined to $7.61B in Q3 vs $7.88B in Sept 2022, a modest 3.4% YoY reject in debt.

This is another call for a strong buy, on the basis of double-digit equity growth YoY along with declining debt loads.

Share Price vs Moving Average

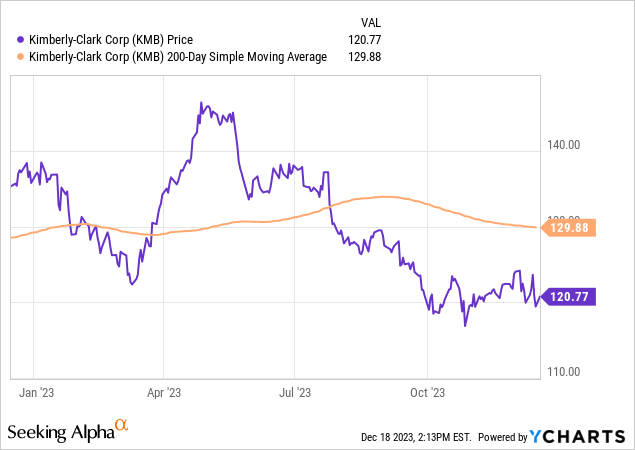

This section uses the yChart tool to examine the current share price compared to the 200-day simple moving average, to infer if it currently presents a buy, hold, or sell opportunity. The 200-day SMA is my standard long-term trend indicator I prefer for its simplicity and smoothing out the price movement.

It is clear from the yChart above that the current share price of $120.77 (as of this article’s writing) is still in bearish territory trading +7% below the 200-day SMA.

It has been trending below the moving average since this summer and is currently around $20/share lower than its spring highs pushing +$140/share.

I will call it a strong buy at this price, combined with the fact that I can snag a nearly 4% dividend yield, for a company that has shown YoY growth in top-line and bottom-line figures as well as equity.

Valuation: Price-to-Earnings

This section uses valuation data to examine the forward P/E ratio and whether it presents an undervaluation opportunity or appears overvalued.

We can see from the data that the forward P/E ratio of 22.50 is +19.6% above its sector average which is lingering around 18.81.

In tying this multiple of 22.5x back to my earlier discussion on earnings results and the share price, what has occurred is the share price has been in bearish territory while earnings have grown by double-digits. So why the high multiple then?

While the price multiple seems high, it is lower than peers Colgate-Palmolive (P/E of 28.11), Church & Dwight (P/E of 28.97), and Clorox (P/E of 37.52).

advance, all of them have relatively high share prices to begin with, the lowest of them being in the upper $70 range.

So, what is driving this multiple for Kimberly Clark I think is a high share price of +$120 despite it trading below its moving average.

Based on this approach, I will call it a buy in this category rather than a strong buy, since the valuation is above the sector average but also is below three key peers in this segment that I think are relevant if I was looking to pick one of these for my portfolio.

Valuation: Price-to-Book Value

This section uses valuation data to examine the forward P/B ratio and whether it presents an undervaluation opportunity or appears overvalued.

What is interesting in this metric is that the forward P/B ratio is a multiple of 49.18, which is 1,563% higher than the sector average that is hovering closer to 2.96, earning an “F” grade from Seeking Alpha.

In helping to grasp this high multiple of 49x, let’s consider the share price and equity we talked about earlier. Although the share price has been trending below the moving average and equity has grown (which ought to have lowered this valuation metric) at the same time when looking more closely we see that the share price itself is rather high at +$120/share while total equity/book value is only $840MM.

As you can see in the balance sheet, this company’s assets of $17.15B are largely overshadowed by total liabilities of $16.31B, or 95% of total assets. Part of that story is also the $7.6B in corporate debt, which has declined YoY but still is impacting equity. It is understandable considering this is a very capital-intensive business with many facilities, overhead, and a global supply-chain. It is not unusual in this sector to see a lot of debt financing, since for example its peer Colgate-Palmolive is sitting on $8.69B of long-term debt on its balance sheet.

So, I would not call it a buy at this multiple of 49x book value which is clearly excessive, but rather a hold in this case. In this category for a buy I would be looking at no more than 4x to 5x book value to stay not more than a few points above the sector average, or if possible drop below it.

Risk Analysis

This section identifies a key risk to consider about this company and what its probability and impact could be to the business.

We know from go through that this business has proven to be pandemic-proof, so in the event of another one and a paper hoarding binge it can only favor this company. As far as recession risk, I think that will have low impact since this company sells household essentials that simply must be bought and replenished regularly.

However, the downside risk could come from continued price inflation, thereby leading customers to increasingly select cheaper store brands rather than name brands.

In my opinion the levels of price inflation we have seen in the last few years should be at a plateau now, and on a course to stabilize.

Consider the following from a Dec. 18th article in Reuters:

The sharp rise in inflation that forced global central banks to drive up interest rates at the fastest pace in decades looks poised to continue to subside in coming months, though risks persist, World Bank economists said in a blog to be published Monday.

However, don’t just take the word of Reuters alone. Here is more evidence of easing inflation according to a Dec. 16th article from financial media giant CNBC:

The consumer price index in November increased 3.1% from 12 months earlier, down from 3.2% in October, the U.S. Bureau of Labor Statistics said Tuesday.

“There is still a lot of disinflationary pressure in the system,” which will likely drive inflation even lower heading into 2024, said Sarah House, senior economist at Wells Fargo Economics.

So, in the category of risk I will call this stock a buy because I think the expected declining inflation can only benefit its consumer sales, which are already a household necessity as it is.

Quick Summary

To summarize, I am going long /bullish on this stock today, contrary to the more cautious outlook from the consensus ratings on Seeking Alpha.

Positive drivers of my bullishness are a nearly 4% dividend yield that beats several peers, proven dividend income growth, earnings and revenue YoY growth, equity growth, and share price trending 7% below its 200-day average.

The high multiple on price-to-book value is concerning and speaks to what appears to be a relatively high share price in general combined with equity that is rather low at below $1B, since on paper this company’s liabilities seem to eat up most of its assets.

The risk of inflationary pressures on the prices of consumer products should stabilize and calm down going into 2024, as some reports imply.

I really love this stock on paper at least (literally and figuratively), and I would add it to a diversified portfolio to gain exposure to the household products sector since this is a business with a consistent demand driven by households needing to replenish these types of products regularly.

Kimberly Clark – brands (company website)

Q2 2024 Earnings Call Transcript")