Kevin Dietsch/Getty Images News

In October 2023, I initiated coverage of Kaman Corporation (NYSE:KAMN) with a hold rating. Since then, quite a few things have changed, as the company received a bid to be taken private by Arcline. In this report, I discuss why being taken private was the best course of business for Kaman Corp.

Arcline Bid Values Kaman At $1.8 Billion

Arcline Investment Management, a private equity firm, has offered $46 per share in an all-cash transaction, giving the company a total enterprise value of $1.8 billion. Arcline Investment Management is a private equity firm focused on growth-oriented investment opportunities in the fields of biopharmaceutical technology, defense, aerospace, energy transition and specialty materials. The acquisition of Kaman Corp. is set to be completed in the first half of 2024 and the acquisition price provides a 105% premium over Kaman’s closing price before the acquisition was made public.

Kaman Stockholders Got A Good Deal

One major reason why I believe investors got a good deal is because Kaman had significant debt maturing in 2024 and when I went through the company’s investor presentations and results, it was not in the slightest clear how the company would be handling this debt. Its most recent cash and cash equivalents balance was $30.1 million, while its free cash flow was unlikely to be running in the hundreds of millions of dollars, which is what the company needed to pay down its $562.5 million in debt maturing.

Kaman Corp.

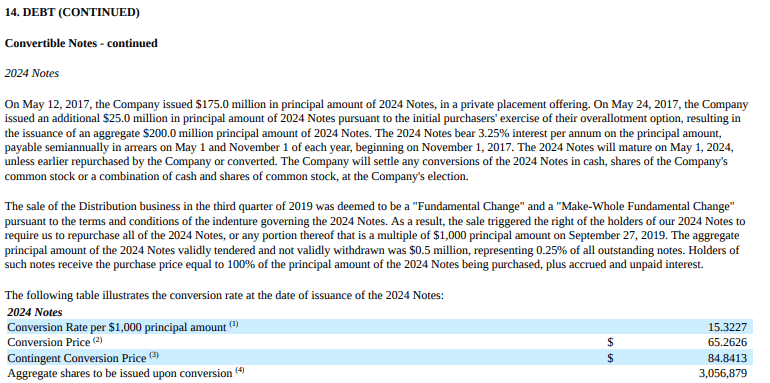

In Kaman’s 2022 annual report, the company pointed at a possible issuance of 3.1 million shares in case the convertible notes would be settled by a debt-to-equity conversion. This would result in a 10% dilution of shareholders. The other option would be exploring refinancing options, but one can wonder how successful the company would be in arranging refinancing in the current interest rate environment.

So, solely looking at the debt, Kaman Corporation being taken private and getting a premium for the shares is a true blessing for shareholders.

The Aerospace Forum

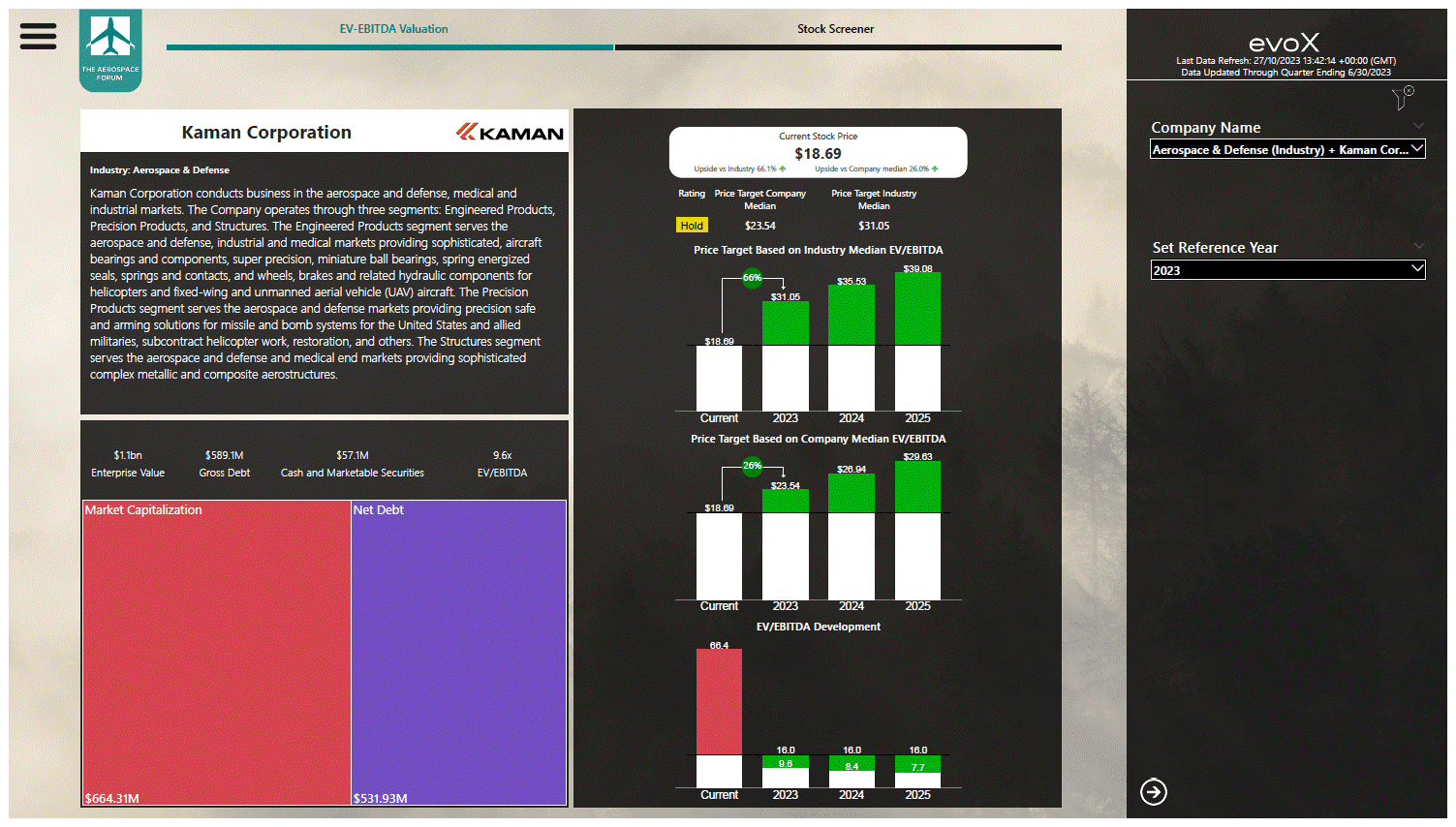

Another reason why I believe a $46 offer is a sweet deal is the fact that when processing the forward projections for Kaman Corporation back in October, there was no scenario where the company’s shares would be worth $46 a stand-alone business:

I ran the numbers for Kaman and driven by its weak three-year alpha, the company is a hold rather than a buy. Upside, however, does exist with 66% upside compared to a median industry valuation and 26% compared to its company median. Given that the company currently is trading at a multiple that’s significantly higher than the industry median, I would put a $31 price target on the stock with the note that in case the $199.5 million convertible notes due 2024 are not exercised and are fully paid off, Kaman will need to dip it its existing credit lines to pay for the notes on maturity. The company already has positioned for that by extending the maturity on the credit agreement to 2028, allowing the company to borrow from the credit line to pay for the notes.

Generally, I am looking for a premium of around 30% compared to peer valuation, and the acquisition price of $46 provides a 29.5% premium against my valuation for 2024. So, that is a great deal for shareholders in my view and the deal is even better when considering the median EV/EBITDA for the company providing a 55 to 70 percent premium based on 2025 and 2024 earnings as a reference.

Conclusion: Shareholders Got A Great Deal For A Mediocre Performer

When I analyzed Kaman Corporation in October, I could see the positive industry tailwinds but failed to see a tangible plan by the company to turn the current business environment into a sustained success while debt maturities were closing in. I do believe that the current bid for $46 is a great deal for investors and the best that could happen. Indeed, pre-pandemic this was a $60 stock, but in the current setting, there was no way in which such a stock price could be once again be achieved and management probably also had significant challenges seeing a value-creating path ahead.

Q2 2024 Earnings Call Transcript")