bee32

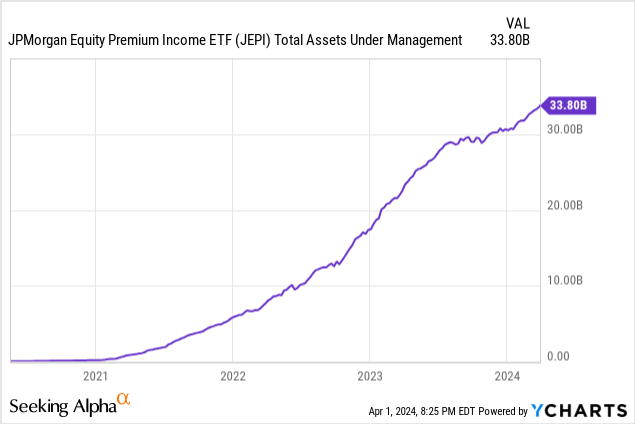

JPMorgan Equity Premium Income ETF (NYSEARCA:JEPI) is probably the most popular covered call fund out there with its total assets approaching $35 billion. The fund has attracted a lot of attention from investors who are seeking income in recent years. Although the fund has been around for only a few years in its current shape, it originally started as a mutual fund in 2019 under JEPIX (JEPIX) which it still exists as a mutual fund but it’s basically the same fund as JEPI. I’ve covered this fund before in the past with my most recent article from last year titled JEPI: Here Is Why It’s Underperforming In 2023 And May Continue To Do So.

Performance

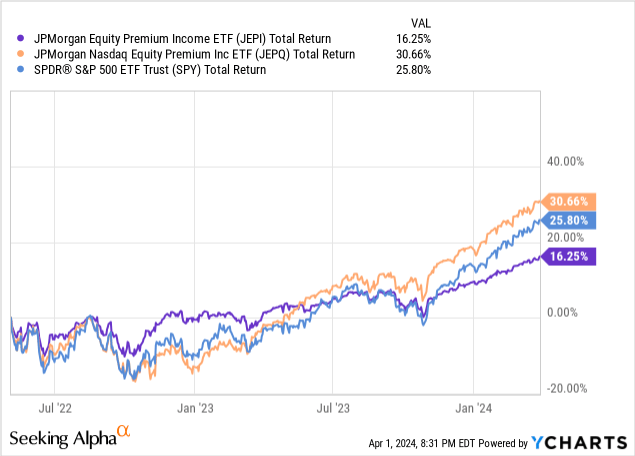

The fund hasn’t had a bad performance perse but it’s been underperforming the overall market as well as its sister fund JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) which is a similar fund that focuses on tech stocks and writes covered calls against Nasdaq index instead of the S&P 500 index. In the last couple years, JEPI had a total return of 16% including reinvestment of dividends whereas JEPQ almost doubled that with a total return of 31%. During the same period the overall market’s (SPY) total return came at 26% which was better than JEPI but worse than JEPQ.

The Low Beta Problem

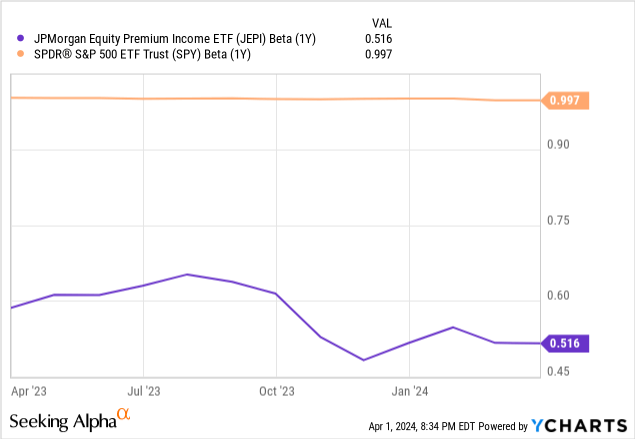

One of the biggest challenges with JEPI is that it chooses a basket of low volatility stocks which have a beta of 0.80 on average which means these stocks are about 20% less volatile than the overall market. As a matter of fact, JEPI’s own beta is even lower than that as it sits at 0.52 which means that JEPI has 48% less volatility than the overall market. What does that mean for investors? It means that for every $1.00 that SPY rises, you can expect JEPI’s holdings to rise 80 cents and JEPI itself to rise 52 cents. This is because JEPI holds a bunch of low beta stocks and writes covered calls against them which further reduces its overall beta. On the positive side, for every $1 that SPY drops, JEPI’s holdings will only drop 80 cents and the fund itself is expected to drop only 52 cents so beta works both ways.

Low beta works to your advantage during red years and it works against you in green years. The problem is that historically the market is green far more often than it is red. In the long run the market tends to go up and we tend to have about 4-7 green years for each red year on average so having a low beta portfolio is more likely to play against you than work for you.

Maybe Caution is Warranted

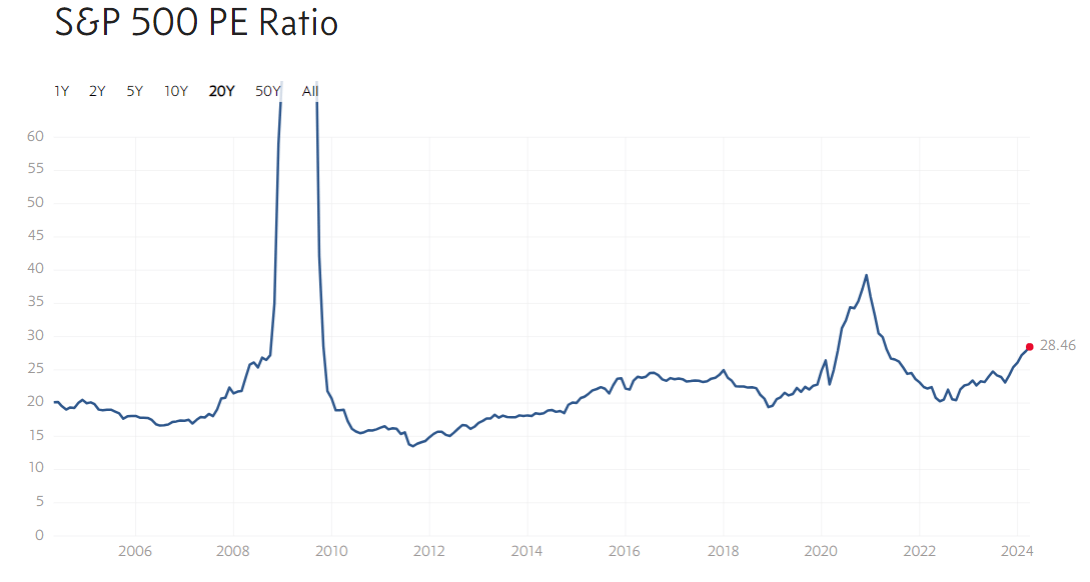

Having said that, one could also make the counter argument that since the markets have been going up for quite some time and they are enjoying historically high valuations, maybe we are overdue for the market to have one or more red years. Currently S&P 500’s P/E ratio is 28.46 on GAAP basis and this is the highest it’s been in quite some time if you don’t count a brief period in 2020 where earnings dropped quickly very significantly due to pandemic lockdowns which temporarily pushed our P/E ratio to almost 40 but that was a unique period where earnings were suppressed for two quarters. The current P/E ratio gives us an earnings yield of 3.51% which doesn’t give us much upside especially considering that risk-free treasury rates are hovering around 5.5% and even with anticipated rate cuts from the Fed, they are unlikely to drop below 4% anytime soon. If you are in the bearish or super cautious camp, JEPI would make more sense for you indeed but it is still likely to underperform in the long run.

S&P 500 Valuation (multpl.com)

A Word on Dividends

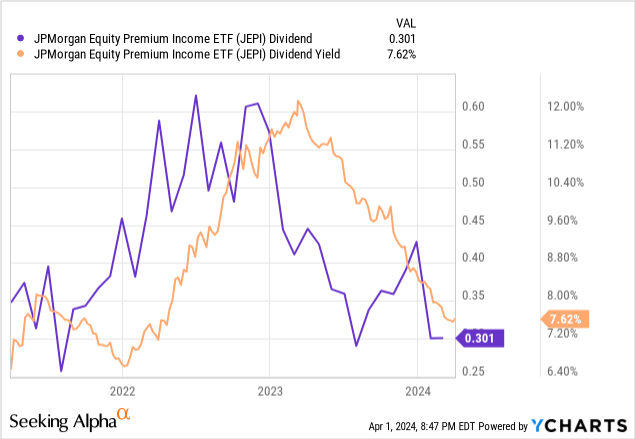

Often times people say that they don’t care if their holdings underperform the overall markets because their purpose for investing in those holdings is simply to generate income. The general thinking is that as long as I keep receiving those generously rich dividend distributions, why should I care about where share price is headed or whether my fund beats the overall market or not? The issue is that JEPI’s dividend distributions haven’t exactly been very stable in the last few years. We’ve seen the fund’s dividend yield fluctuate between 6% and 12% while its monthly dividend payments fluctuated between 25 cents and 60 cents so this is a wide range. To make the matters worse, currently both the actual payments and dividend yield seem to be much closer to the bottom of this range than the top. Since early 2023, dividend yield has been on an almost constant decline dropping from 12% to 7%.

Harvesting Volatility

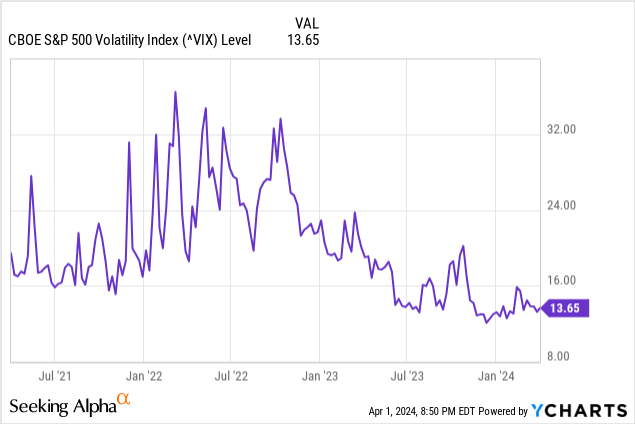

Part of this is because volatility has been dropping overall. Measured by VIX for the overall market, volatility is considered the bread and butter of covered call funds because that’s what they harvest when they write covered calls. VIX is calculated by looking at the implied volatility of S&P 500 calls one month out which is what JEPI sells so JEPI’s income generation power will be directly correlated with the behavior of VIX. This also raises another issue with JEPI. This means that when the market is performing the best, JEPI’s dividends will get the smallest. When the overall market is highly volatile, JEPI’s dividends will get bigger and bigger. Remember, JEPI is already making a rather neutral bet by investing in low beta stocks and it’s already expected to underperform in share price when the overall market is rising but now it turns out that even the dividend is at the mercy of the market’s performance as it will inverse the market performance for the most part.

Verdict

This actually means that JEPI might still have a place in your portfolio for the sake of diversification and risk management but I don’t see it as your main play unless you are neutral or bearish about the market in the next few years. If you have a bullish portfolio you can supplement it with JEPI as a rainy day fund and in case the market heads south but it probably should be a small part of your overall portfolio.

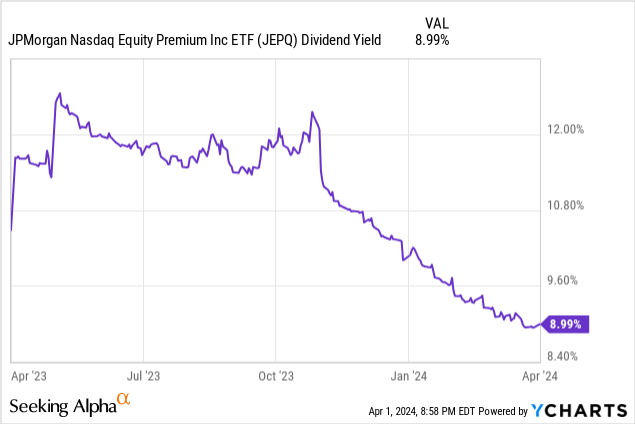

I like JEPQ better than JEPI because it doesn’t limit itself to low beta stocks although it limits itself to tech stocks. Also it generates a slightly higher yield because it sells calls against Nasdaq which is slightly more volatile than the S&P 500. Although it yields less than it used to, it still has a yield of 9% which is a bit better than JEPI’s 7%. JEPQ probably offers less downside protection due to the nature of stocks it’s holding though, so that’s another thing to consider and keep in mind.

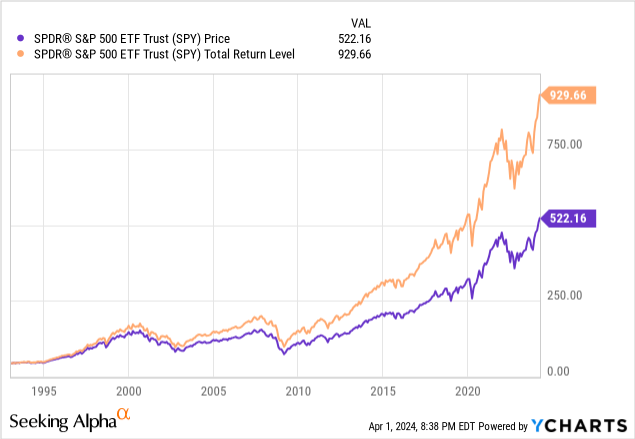

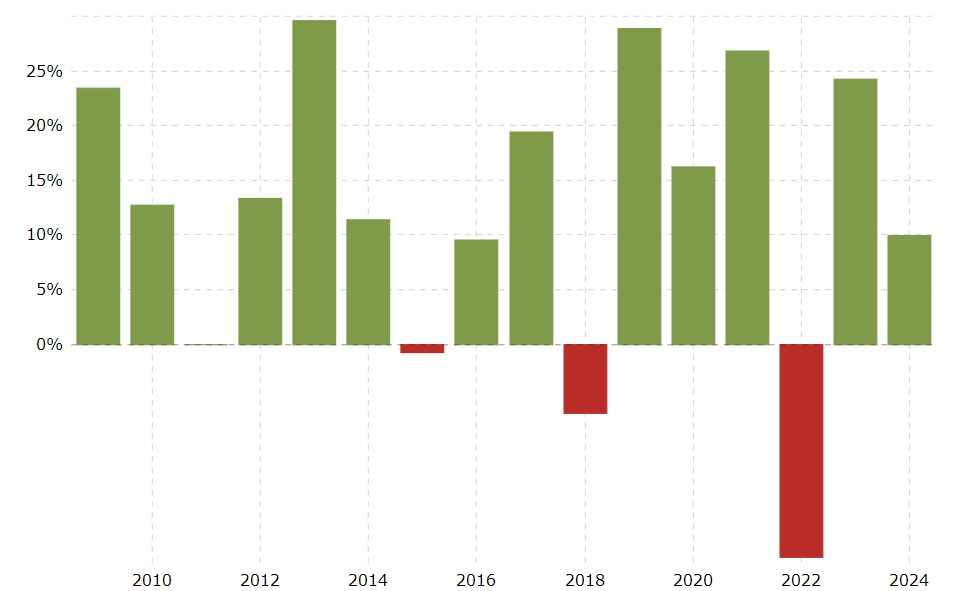

Whether you are bullish or bearish on the overall market in the short term, history tells us that the market climbs up in the long run and any given year is far more likely to be green than red. In the last 15 years we’ve had only 3 red years and only one of them was truly red when you think about it. Technically 2015 was also a “red year” but it was actually flat after adding dividends and 2018 was only slightly red after adding dividends. I am not saying that the next 15 years will look like this but we are more likely to have green years and decades ahead of us than red ones so you don’t want your long term portfolio to be overly cautious.

S&P 500 Annual Performance (macrotrends.net)

In conclusion, I would still keep JEPI as part of my portfolio but limit my exposure to it to about 10-15% in the long run.

Q2 2024 Earnings Call Transcript")