Masafumi Nakanishi/iStock Unreleased via Getty Images

Although third-quarter GDP was revised down unexpectedly, the improved current account and cash earnings suggest a rebound in growth in the current quarter. Market speculation about the Bank of Japan’s possible policy turnaround at the December meeting has been amplified after recent remarks from Governor Kazuo Ueda and Deputy Governor Ryozo Himino.

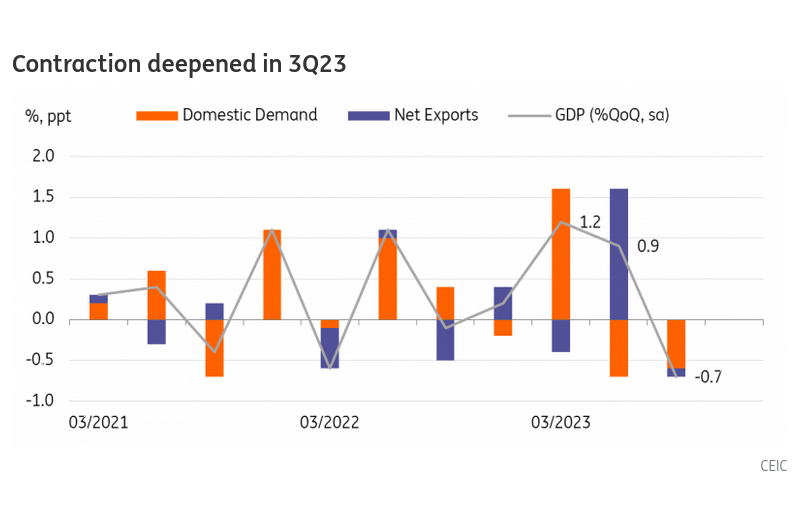

GDP contraction deepened in 3Q23

Third-quarter GDP was unexpectedly revised down to -0.7% quarter-on-quarter (seasonally adjusted) compared to the flash calculate and market consensus of -0.5%. The largest revision came from private consumption, which fell 0.2% (vs 0.0% in the flash calculate) and the inventory contribution to GDP, which was down by 0.2% ppt. The negative contribution of inventory should be a good sign for the inventory restocking cycle. But household spending still lagged amid high inflation despite relatively healthy labour market conditions, which should be a real concern for the Bank of Japan. We think that weaker-than-expected GDP could defend the Bank of Japan’s current easing policy at least for now.

Meanwhile, GDP for the first quarter was revised up meaningfully from 0.9% to 1.2% resulting in an upward revision to annual GDP. Thus, now we expect 2023 GDP to rise 2.0% year-on-year.

However, other data releases today – labour cash earnings, household spending, and current account – point to a rebound in growth in the fourth quarter, thus we believe that the BoJ will shift its policy early next year.

Contraction deepened in 3Q23

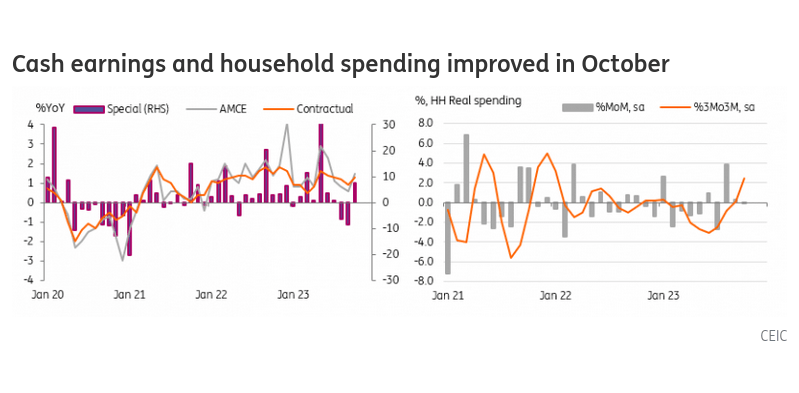

Labour cash earnings rose in October

Labour cash earnings rose 1.5% YoY in October (vs 1.2% in September, 1.0% market consensus) beating the market consensus. Contractual earnings gained steadily by 1.3% (vs 0.9% in September) while volatile bonus earnings (7.5%) rebounded after two months of declines. Also, hours worked bounced back 0.7% for the first time in four months, thus overall labour market conditions and earnings appear to have recovered in October. However, wage growth was still short of inflation growth, thus real earnings dropped 2.3% in October, although at a slower pace than the previous month’s -2.9%.

Nominal wage growth continues and is clearly faster than the previous year. Also, there are several news reports that big companies scheme to raise wages above this year’s level of growth. Thus, we believe that next year’s wage growth should speed up a bit more than the current year.

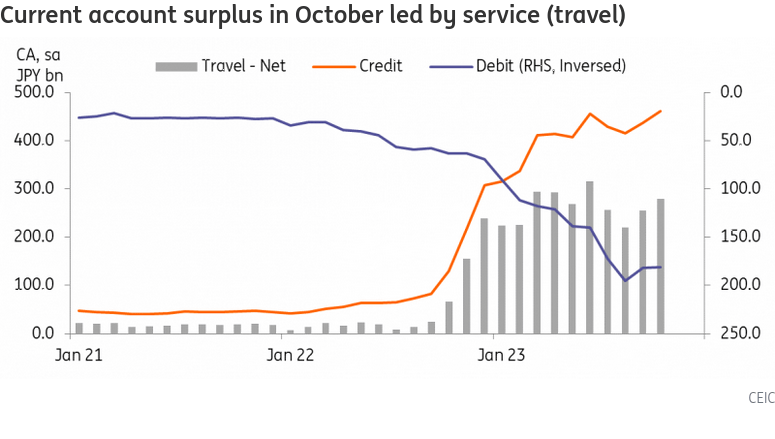

Current account surplus widened in October

In a separate report, the current account surplus widened more than expected in October to JPY 2.6tn (vs 2.0 in September, 1.8 market consensus). Despite the global headwinds, the current account surplus will likely widen in the coming months. Due to falling commodity prices, the merchandise account will turn to surplus while an influx of foreign tourists will help the travel account to remain in surplus. We expect the trade of goods and services to boost in the current quarter.

BoJ preview

Several remarks by the Bank of Japan, including Governor Ueda, have shaken the FX market quite strongly. Deputy Governor Himino said that ending the negative interest rate policy would have only a limited impact on the economy and Governor Ueda yesterday met with the prime minister, highlighting the importance of sustainable wage growth and inflation, which led to a fairly rapid shift in market sentiment betting on the Bank of Japan’s policy tightening. Dollar weakness is also supporting the sudden advance of the yen partially, especially ahead of today’s release of the US nonfarm payrolls data.

It seems appreciate the BoJ is paving the way to a gradual normalisation and giving the market a signal that the time is approaching. However, since these comments were made outside of the BoJ meeting, any sudden major change of policy is not expected this month. Yes, we recollect that Governor Kuroda surprised the market with a yield curve control tweak last December, but we believe Governor Ueda is unlikely to adjust policy without prior communication. Thus, we expect some changes in the statement and dialogue from Governor Ueda at the BoJ meeting on 18-19 December.

As we have previously argued, we think the Bank of Japan’s rate hike will come in 2Q24, most likely at its June meeting. By then, the BoJ will be able to confirm a solid wage boost with Shunto’s results. In terms of inflation, it will trend down early next year, but still core inflation, excluding fresh food, is expected to remain above 2%. Even if the BoJ carries out a rate hike, we believe that the Bank’s JGB buying operation will continue in order to avoid a rapid rise in long-term yields.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Q2 2024 Earnings Call Transcript")