SimplyCreativePhotography/E+ via Getty Images

Janus International Group, Inc. (NYSE:JBI) is a key supplier of the self-storage industry (63% of 2022 sales), providing products for facility and door automation, access control technologies and roll up and swing doors.

It also has operations in the commercial segment (37% of sales), providing doors used in industrial facilities, offices, and retail spaces. While the Company is a small operator in the sector, now it represents the segment with the highest weight on the Company’s revenue.

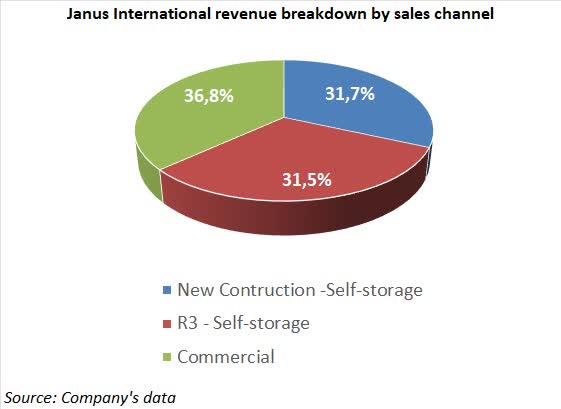

Company operations are divided into three sales channels:

- New Construction self-storage: the channel serves companies building new facilities or expanding the existing ones. Janus International mainly works with institutional investors (REITs), which have a 30% share of the total self-storage market. Such investors have gained market share over the last few years, growing at a faster pace than small non-institutional companies.

- R3 self-storage: restoration, rebuilding, and replacement (“R3”) of damaged or end-of-life products. Based on the company’s estimates, approximately 60% of active self-storage facilities are more than 20 years old and therefore require modernization and/or repairs.

- Commercial: the channel sales of products and services to offices, shops, industries, and e-commerce companies.

Source: Company’s data

With regard to geographical diversification US represents 93% of total sales and the Rest of the World (Europe and Australia) the remaining 7%.

Investment thesis

We believe that the company could record sustained organic growth rates over the coming years as all business segments could benefit from several positive elements.

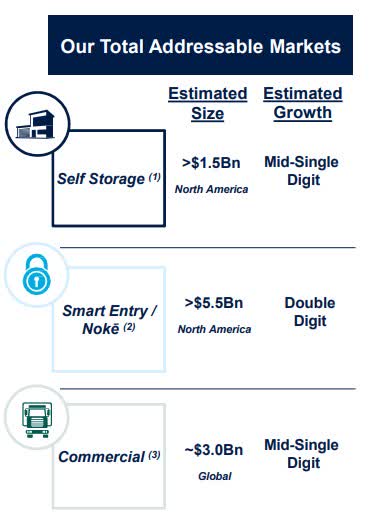

The population and personal spending solid upward trend should sustain operations in the new construction channel. Positive for the sector is also the downsizing of living spaces as the house prices increase. Furthermore, the self-storage companies consider the actual high occupancy rate (above 90%) non-optimal. High occupancy rates and rising demand could incentivize investments in additional self-storage capacity. The Company expects a mid-single digit growth rate for the segment.

As indicated above, the need to modernize or repair old facilities could support the R3 segment. In particular, the Smart Entry/Kone system could benefit from this trend, whose potential total addressable market has been estimated at USD 5.5 billion by the Company. The Company estimates a double-digit growth rate for the R3 segment.

The commercial channel could benefit from the positive trend of the US economy and from the solid e-commerce growth rate, which requires the use of new storage spaces. The segment could expand at mid-single digit in the medium term.

The last positive element is the potential development of international activities. In Europe, for example, the self-storage market is expected to grow at 5.95% CAGR in the period 2024-2029. Furthermore, except for the UK, all other European countries have a limited penetration rate and could record high growth rates in the medium to long term.

Source: Company’s investor presentation

M&A operations

M&A operations have been an important growth driver for the company over the last few years, and we expect the trend to continue in the coming years. However, with interest rates remaining at the highest level of the last few years over the next few quarters and the net debt/EBITDA ratio only slightly lower than the range considered optimal by the company (1.8x versus 2-3x), we believe that the company would implement only small acquisition with the aim to purchase niche products and to develop them, as it happened with Noke, acquired in 2018. We think that transformative acquisitions are not likely in the foreseeable future.

However, following the last few months strong rally (1-year performance +37%; year-to-date +15.9%), we believe that the stock already reflects the company’s growth perspectives and that it is fairly valued. Our DCF model leads to a valuation of USD 14.2, slightly below Wednesday’s closing price of USD 15.1.

We think that only revenue and EPS growth significantly higher than our estimates or positive pieces of news on the M&A front could push prices further upward.

Q4 ’23 and FY 23 results

The company announced that Q4 ’23 and full-year 2023 data will be published on February 28. We expect the data to confirm the solid growth trend already indicated by Q3 results. According to consensus estimates, total revenues in 2023 are expected to rise by 6.6% to USD 1,086 bn, with EBITDA growing by 25.8% to USD 285.5 million and EPS at +27% (USD 0.93).

Valuation

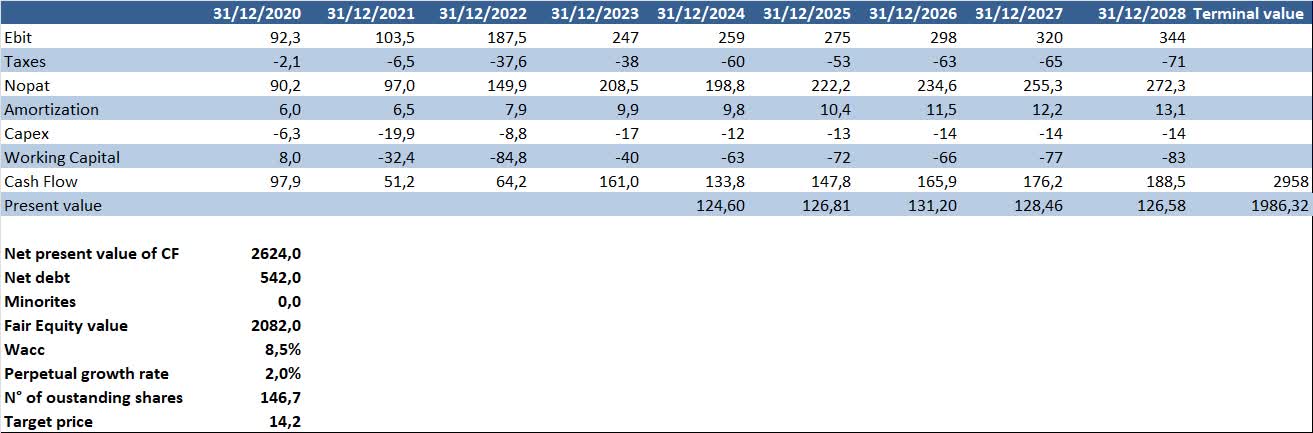

We valued the company using a DCF model based on the following assumptions:

- EBIT grew at 6.8% CAGR in the period 2023/2028. For the period 2024-2025, we consider a consensus estimate and for the period 2026-2028, we pencilled in EBIT to expand in line with the Company’s estimates of business segments.

- Average capex of 1% of revenue per year in the period 2023-2028.

- WACC of 8.5%, reflecting the 75% equity/25% net debt capital structure.

- A perpetual growth rate of 2.0%, in line with the long term expected US real GDP growth rate.

Source: Company’s data, RadaEcowatch estimates

It returns a USD 14.2/share target price, with a 6% downside potential from February 14, 2024, closing price.

The view from the street

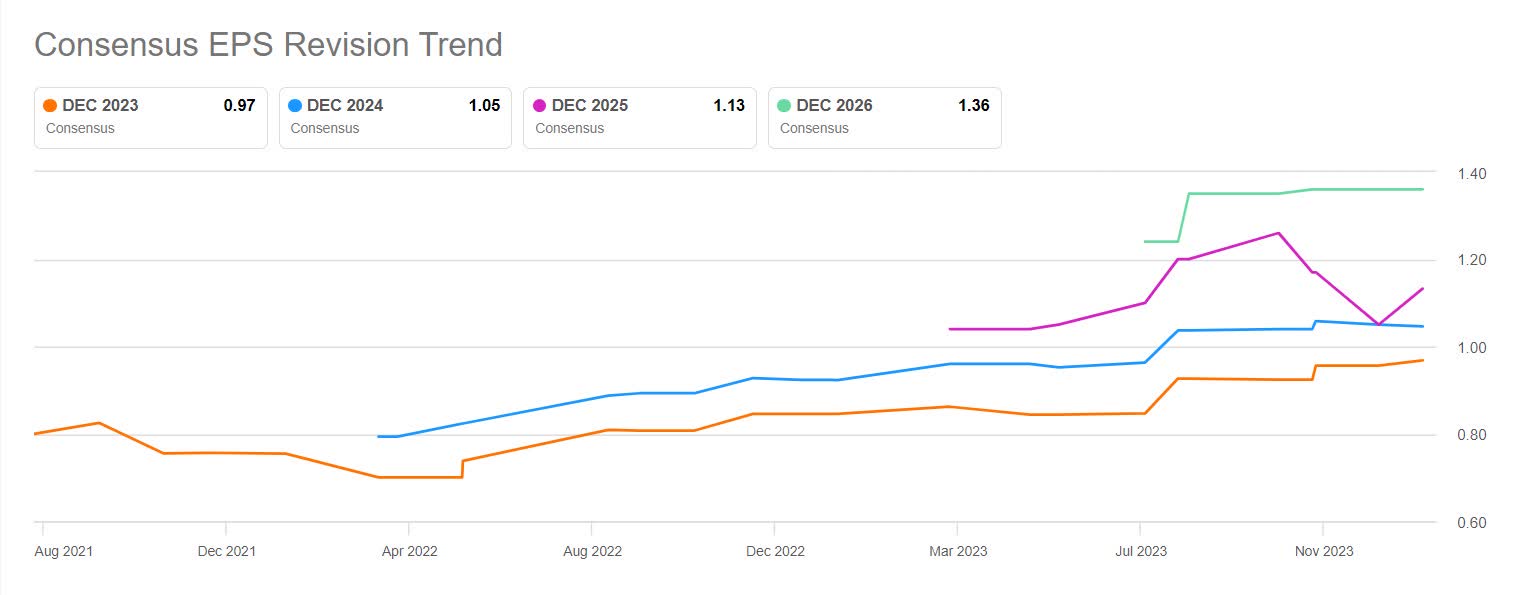

Due to a limited market capitalization (USD 2.2 bn), the stock is covered by only six equity analysts at U.S. investment banks. They have a positive view of the stock, with 4 Strong Buy, 1 Buy, and only 1 Hold recommendations. Moreover, analysts have revised upwards EPS estimates over the past few months. For example, the consensus estimates for 2024 EPS rose from USD 0,93 at 2022-end to USD 1,05 at 2023-end while consensus estimates for 2025 EPS rose from the initial USD 1,04 in March 2023 to USD 1,13.

Source: seekingalpha.com

What could go wrong?

We identify two main sources of risk for Janus International. The first is the US economy’s strong recession. In the self-storage sector, it could have the consequence of postponing investments both in new buildings and in renovations, especially if interest rates remain high for a while.

Indeed, self-storage companies (i.e., Cubesmart and Public Storage) during the 2007-2009 recession responded to declining occupancy rates and falling rents by reducing capital expenditures.

The Commercial sector should also suffer from an economic slowdown as declining activities in the industrial and retail sectors could lead to lower investments.

A further negative element could be a surge in steel prices, which represents 62% of commodity spending in 2022. A surge in prices would reduce profit margins, with limited room for maneuver in the short term.

Source: tradingeconomics.com

Conclusion

Janus International is an interesting long-term growth story, but we believe that it is correctly valued at current prices. In our opinion, only a growth rate significantly higher than our estimates or transformative M&A operations could further push prices upwards. We would turn buyers of the stock only below USD 12,0/share.

Q2 2024 Earnings Call Transcript")