PM Images

Investment Thesis

Jack Henry & Associates (NASDAQ:JKHY) reported results on the 6th of February, beating EPS and revenues. The price has moved up 2.1% since the results and I believe there is significantly more upside in this share price. The company sports a wide moat that focuses on providing payment processing services primarily to the financial services industry. The company has a strong record of organic growth and recently made a significant investment into a cutting-edge fintech company. My valuation has the share price up 20% from current levels.

Background

JKHY offers technology solutions and payment processing services. The company targets customers through three pillars of execution. The first pillar, Jack Henry Banking, targets community banks and institutions with payment processing systems, business intelligence, and bank management software. The second, Symitar provides core data processing for credit unions. And finally, ProfitStars offers highly specialized core products and services that include imaging and payment processing.

They generated $2.08 billion in revenue in 2023 with their Core segment that includes Jack Henry Banking and Symitar forming 31% of revenues. Their processing and payments solutions that include ATMs, debt and credit card transactions form 36.9% of revenues and their complementary offering forms the remaining 28.1% of revenues.

Due to the nature of the switching costs involved, different areas of their business have a wide moat over the competition. Core processing is how banks manage their loan and deposit accounts to post daily transactions. Given the nature of how core processes are integrated into banks, they rarely switch providers due to employees often being trained on the original systems and the risk of business interruptions. Furthermore, customers usually sign multi-year contracts and JKHY boasts a 99% retention ratio excluding customers lost because of bank acquisitions.

In comparison to competitors, JKHY has focused on organic growth which has allowed them to execute on their sole niche and build a strong service. It has not been uncommon for competitors to acquire other firms in order to join the market, but some of these companies while larger need to maintain multiple platforms which can hinder growth.

However, JKHY is at a disadvantage in terms of size for the payment segment. This segment is highly scalable and benefits from increased size, which is reflected in being JKHY’s lowest-margin business.

Financials

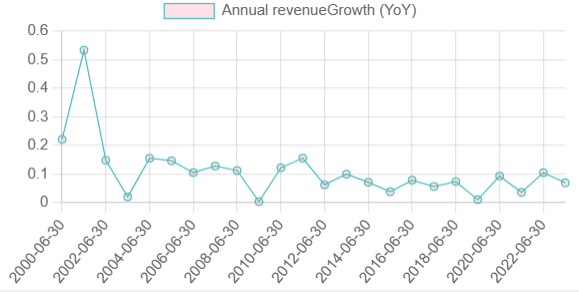

JKHY operates in the presence of some serious competition that include Visa (V) and Mastercard (MA). Their market share in the industry isn’t that large but the company has a stable 7.13% CAGR over the last 5-years, which ranks below the median, but as mentioned acquisitions have been rife in this industry and JKHY has traditionally focused on organic growth. Despite the slower growth in comparison to peers the company shows good stability, and this is forecast to continue with the industry as a whole expecting to remain on its trajectory of fast growth over the next couple of years.

Author’s Calculations

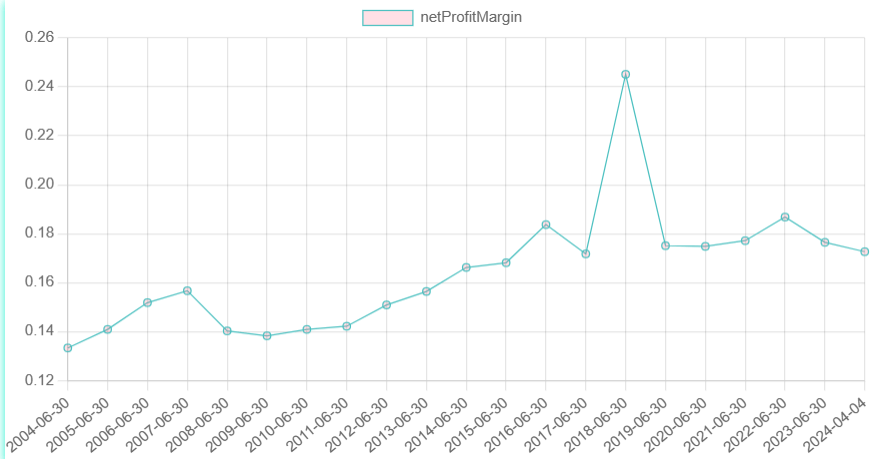

During the period between 2008 and 2017, EBIT margins expanded as costs fell, topping over 25%. But with higher investments into R&D and a slight increase in SG&A, EBIT Margins have contracted to settle around 23%. Net Margins also show good stability and this alongside well-managed working capital produces strong free cash flow.

Author’s Calculations

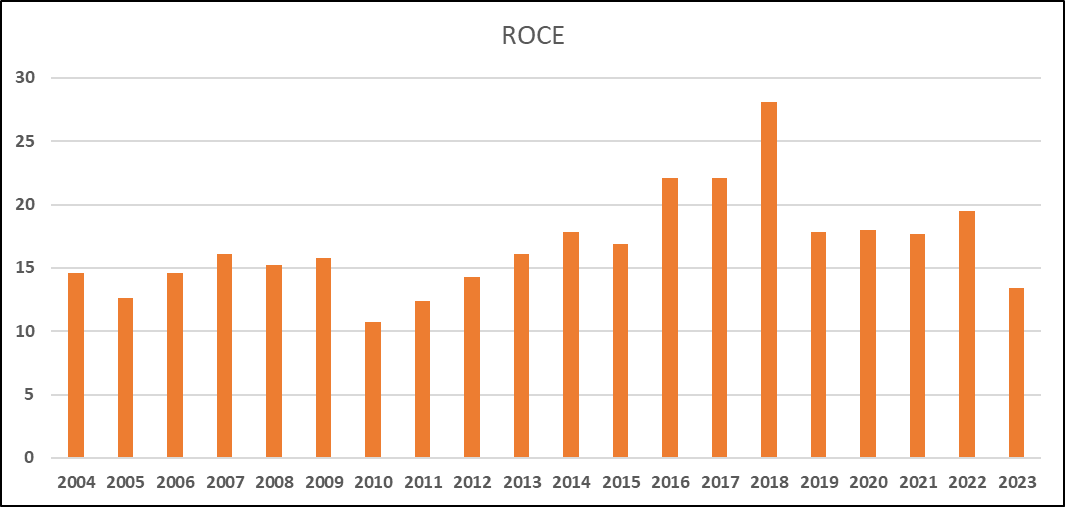

Despite being a highly capital-intensive business the levels of profitability and accretive working capital result in high levels of return on capital (including Goodwill) that easily surpass its cost of capital.

Author’s Calculations

Net Debt to sales stands at 12% and increased in 2023 due to the Payrailz acquisition. I can’t make out the maturities of the obligations but with $260 million in debt and the company generating over $300 million in free cash flow, they are in a fine position to service the principals.

The company has a diverse capital allocation strategy that involves investing for organic growth, making acquisitions, paying a dividend yield of 1.2%, and repurchasing shares.

As mentioned JKHY beat on both top and bottom line. EPS grew 10.9% from last year’s quarter and revenues improved 8%. Top-line growth was driven by growing services and support processing and strong momentum across Core, Payments and Complimentary. Core rose 7.9%, Payments grew 6.5% and Complimentary increased 7.3%. Operating Margins increased 60 basis points to 21.8%.

During the results, JKHY revised their revenue guidance from $2.211-$2.232 billion to $2.215-$2.228 billion, effectively narrowing the expected range. And EPS was revised up from $4.98-$5.04 to $5.09-$5.13 due to an expected 35 basis point move up in operating margins.

Revisions

Revenue revisions are up on where they were 6 months ago but have marginally softened over the last month. Interestingly, revisions here are very stable, the majority of companies experienced significant upgrades early in 2023 to only be downgraded later in 2023, which is not the case here. On an earnings basis, the very long-term trend is down, but again over the last 6 months EPS revisions are up.

Revenue Revisions (Seeking Alpha)

JKHY has been active in winning new business and was recently selected by First State Bank to provide customers with payment processing services. This is one of a plethora of recent wins for the company and I believe is a good sign of a strong business environment. I also believe these recent wins alongside the introduction of Banno Business will continue to drive revenue revisions.

Valuation

Author’s Calculations

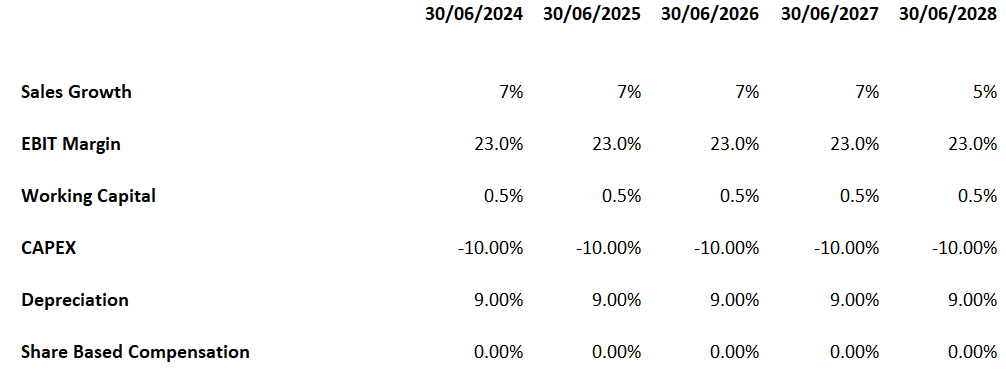

When valuing JKHY I have used a P/FCF multiple of 38x (marginally below the 5-year median) with a WACC of 9.6% (GuruFocus) to arrive at a share price target of $196. This is with EBIT Margins remaining stable. However, if the current long-term trend in SG&A margins continues, we could see JKHY regain EBIT Margins closer to 25% and that would significantly increase my target price.

Due to the nature of how the company collects revenues, it results in a large deferred revenue balance that is incremental to cash flow, so I have used a 0.5% level in relation to sales. And for CAPEX I have used the long-term median of -10%.

Author’s Calculations

Being a wide moat company that compounds well results in a very high multiple. All valuation multiples tracked by Seeking Alpha are above the sector median. That being said, I believe JKHY has a competitive edge aligned with a current strong business environment that shouldn’t result in multiple contraction over the near term.

Risks

Any weakness in the banking sector might lead to banks delaying the purchase of technology. Also as the technology ages, banks might look for alternative products narrowing the moat of JKHY. However, the company seems to invest heavily into R&D and I can’t knock the 99% retention ratio.

Also, disruption in the banking sector from online payment providers such as PayPal and Square offer minor concern. However, these companies have had to decrease fees in order to stay competitive.

Conclusion

JKHY is a steady compounder with a strong moat. Their services are heavily integrated into banking operations and this is reflected in the multiple. The recent beat on earnings and revenues is a strong sign, and I believe it will continue due to the recent business wins. Furthermore, I like the shape of revenue revisions here and believe the company will keep warranting upgrades in the future.

Q2 2024 Earnings Call Transcript")