Bambu Productions

Overview

I’ve covered some other Collateralized Loan Obligation funds here, but they’ve usually had a focus on below investment grade credit quality in order to provide double-digit yields. Janus Henderson AAA CLO ETF (NYSEARCA:JAAA) takes a different approach by providing exposure to the CLO space while simultaneously offering exposure to these debt instruments that have a majority of focus on triple-A rated quality. The primary objective of JAAA is to provide high-quality CLO exposure and to deliver risk-adjusted returns that are comparable to traditional fixed income assets while having a lower level of volatility.

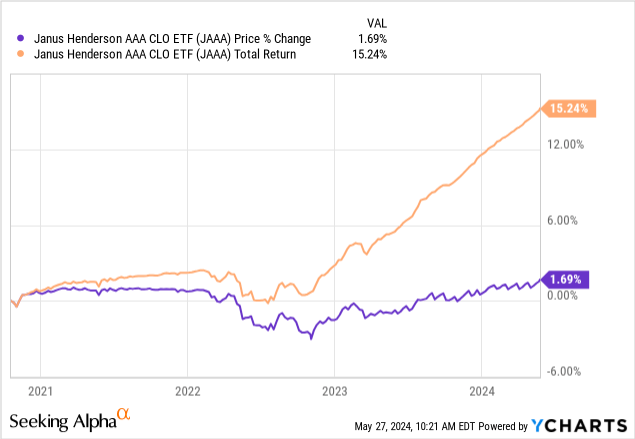

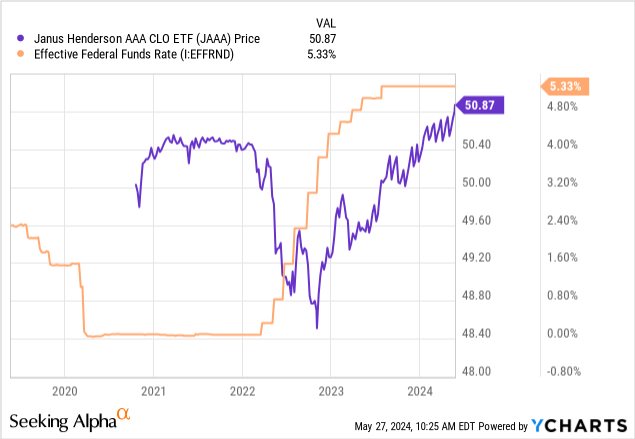

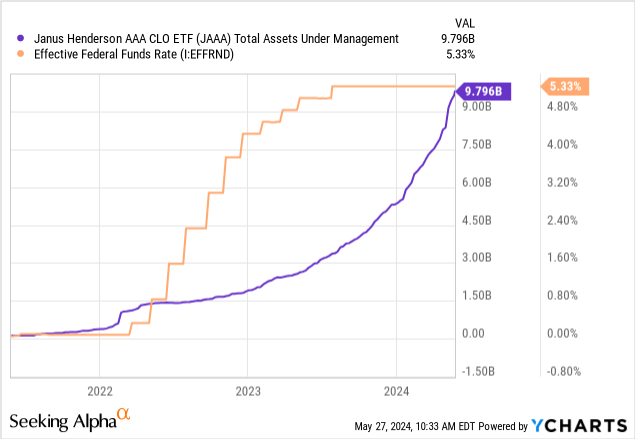

Something very notable here is that this level of CLO exposure was not possible for retail investors until the creation of this fund. We can see how the price has remained relatively stable while the total return profile soared to new heights once interest rates began to increase. JAAA’s CLO exposure is floating rate debt and can pull in higher levels of net investment income as a result. While this has a positive effect with rates rising, the opposite would play out if rates were to decrease over time. I fear that the train has already left the station and the best chance for entry was already missed as interest rates are expected to now decrease in the near future.

The current dividend yield is about 6.3% and the main appeal of JAAA is the high level of dividend income that it can provide. This is an asset that is best utilized by income-focused investors that may be nearing or at retirement age and depend on the income generated from their portfolio of investments. If you are looking for some level of price growth, JAAA is probably not the fund for you. JAAA is a newer fund with an inception in 2020. The net annual expense ratio of JAAA sits at a very reasonable 0.21%.

With the exception of 2022, the price of JAAA has remained relatively stable and within the same consistent price range. The dip during 2022 may be linked to the fact that interest rates were aggressively hiked during the mid-point of that year. However, the price has moved back up since then and still presents an attractive opportunity for entry. CLOs are an interesting asset class that tends to be perceived as more risky than they actually are. CLOs fared quite well through most of the uncertain times in recent history, such as the Covid fall and the global financial crisis.

Risk Profile & Portfolio

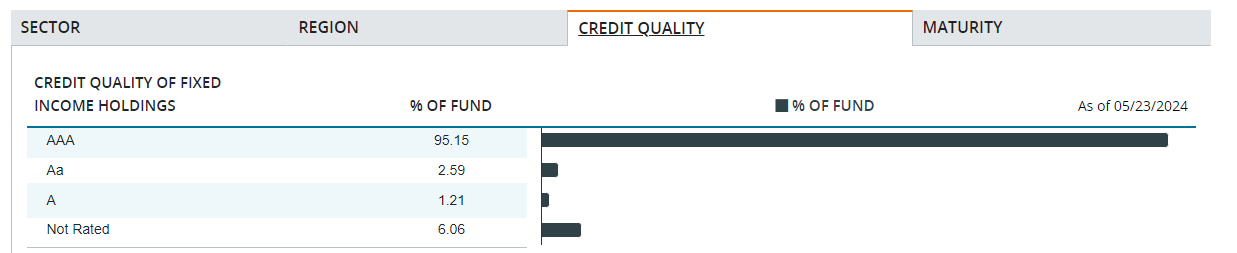

For some brief context, CLOs are an asset class that pools together different collections of loans and labels them each into different tranches at different levels of risk. CLOs are typically designed to provide higher returns than bond alternatives. When it comes to collateralized loan obligations, they typically have a reputation of containing below investment grade holdings within. This is how they are able to produce such a high yield most of the time, as higher risk can result in higher rewards for investors. However, that is not the case for JAAA as the majority of the holdings within are rated AAA, the highest credit rating possible.

Janus Henderson

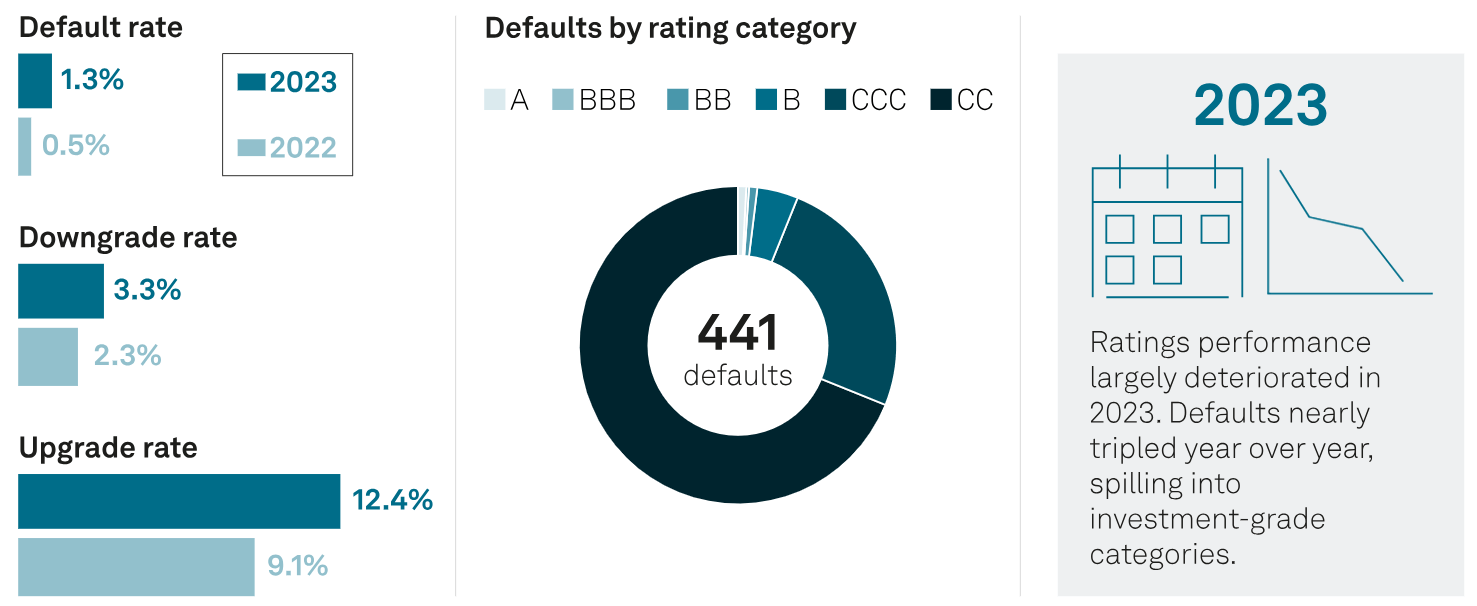

Despite popular belief, CLOs above a BBB rating rarely go through defaults. S&P Global analyzed the default rates for 2022 and 2023 and discovered that the average default rate was only 1.3% for 2023. We can also see that most of the defaults happen within the ‘below investment grade’ range, where the credit quality is rated BB+ and below. Since over 95% of the debt within JAAA is rated AAA, we don’t have to worry about there being a large possibility of defaults within this ETF. We can see that the default rate increased from 0.5% in 2022, up to 1.3% in 2023. However, it seems that the rate of upgrades is greater than the rate of downgrades here year over year.

S&P Global

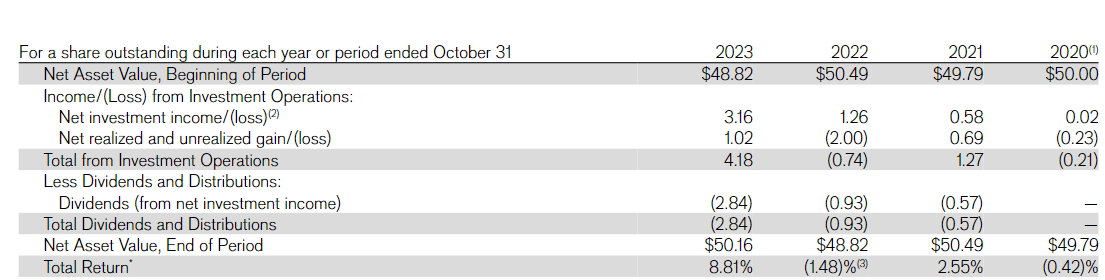

Additionally, the debt investments within JAAA are mostly made up of floating rate loans. This focus on floating rate debt means that as interest rates rise, so does the interest income that JAAA can collect from borrowers. Even though higher interest rates can translate to higher income, it can also put additional stress on borrowers as their obligated debt payments rise. If the business is not performing as expected, these debt payments can become troublesome and cause defaults. Taking a look at the 2023 annual report, we can see that net investment income for the year was $3.16 per share, which fully covered the distribution of $2.84 per share. We can see that net realized gains also totaled $1.02 per share, which helped the fund’s NAV grow year over year.

JAAA 2023 Annual Report

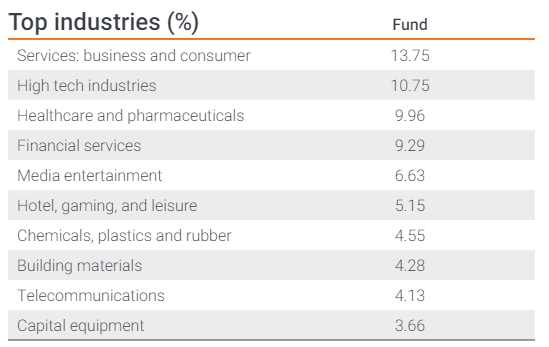

The fund’s assets sit around a value of $9.8B and remain highly diversified across industries. This focus around diversity also helps mitigate any sort of concentration risk or vulnerability to one specific sector or industry, thereby decreasing the risk of defaults. There are currently 367 individual holdings within the ETF. We can see that the breakdown includes a majority focused on service-based businesses, amounting to 13.75% of the fund. This is followed by high-tech industries at 10.75% and healthcare and pharma making up 9.96%.

JAAA Factsheet

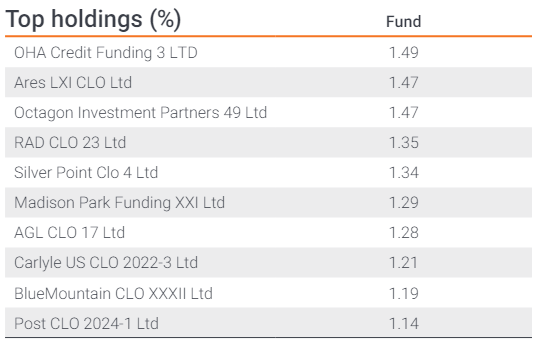

This level of diversity if further built upon on an individual holding basis, as none of the top holdings account for a weighting of more than 1.5%.

JAAA Factsheet

Dividend

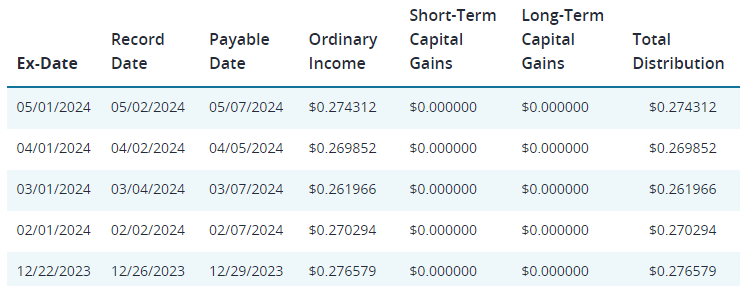

As of the latest declared monthly dividend of $0.2743 per share, the current dividend yield is 6.3%. The monthly aspect of the dividend is what makes this such a great tool to be utilized for income investors nearing or at retirement age. If you depend on the income generated from your portfolio, JAAA would be a great option to ride out the higher interest rate environment. This is due to the floating rate exposure within JAAA. As interest rates rise, JAAA is able to pass along the higher interest income along to shareholders with increases to the dividend.

The dividend has raised by a whopping CAGR (compound annual growth rate) of 112% over the last three-year period. For reference, the dividend throughout Q1 of 2021 was about $0.0521 per share and since grown by over 5x this to the current $0.2743. While the higher rates have definitely been a benefit to JAAA, the opposite would be true if rates start to come back down from these highs. Firms like Morgan Stanley believe that interest rate cuts may happen as soon as September of this year.

However, other estimates see rates remaining unchanged for the year, since inflation still remains higher than expected and the labor market remains strong. I personally think that the days of near-zero rates are behind us, and we are likely to remain in a higher interest rate environment. Even if rates do happen at the end of the year, I believe that they will likely be very light and may reduce the dividend by a bit.

Janus Henderson

One thing that should be considered is that the dividends received from JAAA are not tax-friendly. These distributions have historically been entirely classified as ordinary income, which is taxed at higher rates. Ordinary income has much less favorable tax treatment compared to qualified dividends received, and should be considered if you are depending on this income to fund your lifestyle expenses. Therefore, JAAA may be best utilized when held in a tax-advantaged account such as an IRA.

Interest Rates – Valuation & Vulnerability

It’s no coincidence that the distributions began to massively increase around the same time that interest rate hikes begin. JAAA’s price initially retracted when rates started to rise, but then ultimately rose to new heights as they were able to pull in higher amounts of net investment income through higher interest payments. Since the inception of this fund is so short, we don’t really have a set of historical data to reference in a decreasing rate environment.

With this in mind, I believe the train had already left the station and the best time for entry was already missed. As rates increased, investors started looking for ways to benefit from this move. Look at how quickly the assets under management started to rise here alongside the rise of interest rates. I do not expect the Fed to continue raising rates here, so I believe the best time for entry was over a year ago when rates initially started to get hiked.

While the price range is admittedly small, I still believe that the best way to take advantage of these sorts of funds is to get the best entry price as possible. I stay cautious of recommending to start a position at this current level because you’d essentially be entering at all-time highs while there looms the possibility of dividend cuts as a result of lower interest rates. This would be a double negative and because of the short history here, it’s difficult to determine exactly how much the dividend may get cut.

Takeaway

JAAA has greatly benefited from the rise of interest rates, but I fear that the train has already left the station here. I do not expect further interest rate increases that can propel the dividend higher. Even though we are likely to remain in a higher interest rate environment due to higher level of inflation and a strong labor market, there’s still the possibility that interest rate cuts ultimately reduce the dividend and share price.

Since the credit quality within this ETF focuses on the top quality debt, the risk profile here is quite attractive with a low level of historical defaults. While the monthly dividend can be highly appealing to investors that are specifically focusing on income generation, a fund like JAAA should probably not be utilized by an investor looking to capture the total return of price appreciation.

Q2 2024 Earnings Call Transcript")