DNY59

Thesis

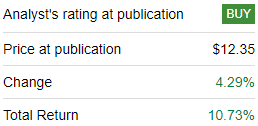

We last covered this name six months ago in a piece where we assigned this high-yield fixed income CEF a ‘Buy’ rating. The CEF is up significantly since we highlighted the opportunity:

Original Rating (Seeking Alpha)

In our initial piece, we highlighted the CEF’s discount to NAV, its classic HY build with a conservative leverage ratio, and the wide levels in credit spreads. The mix in the respective conditions created an ideal entry point into this CEF, an opportunity which was rewarded handsomely.

Fast forward to today, and the landscape has changed significantly. In this article we are going to revisit the PGIM High Yield Bond Fund (NYSE:ISD) and its performance and articulate why today’s price point no longer represents an attractive entry point, thus making this name a hold.

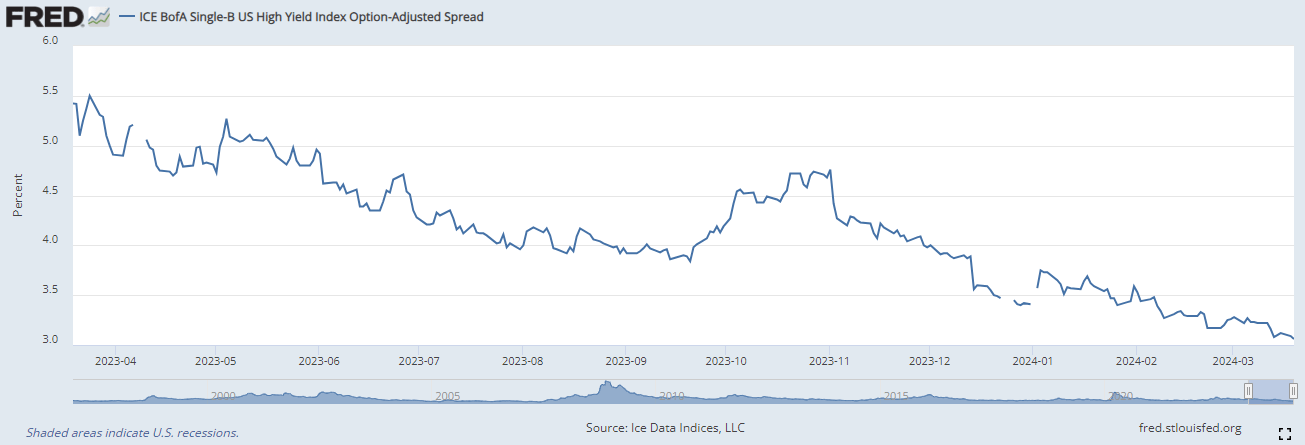

Credit Spreads Have Rallied Significantly

Single-B credit spreads for U.S. high yield have fallen to an astoundingly low 3.06% level:

Credit Spreads (The Fed)

The tightening in spreads has been dramatic in the past year, starting at 5.5%, and experiencing a kink higher in October 2023, before resuming their fall.

These are historic low levels, not experienced since the 2014-2019 period. The market is clearly pricing for a soft landing, and Powell’s speech on March 20th reinforced the view that the Fed is going to cut rates this year irrespective of the inflationary environment.

One can describe today’s credit environment as ‘goldilocks’, with a pervasive risk-on market tilt, and a historic low level in credit spreads. While all-in yields are not low, given Fed Funds are above 5%, credit spreads are. Retail investors should always focus on credit spreads when looking at high yield because that is where you are getting compensated for the default risk taken. You can obtain 5% rates by simply investing in short-dated treasury funds, however, the question is whether 3% is the right compensation for the credit risk taken.

We feel the market is too complacent, and any deviation from the current soft landing path can result in a massive credit spread repricing higher. In the best-case scenario, the soft landing materializes and investors keep clipping the 3% credit spread, with no real further upside here. Clipping the yield is the best-case scenario at these levels. The downside however is much more significant, with credit spreads being able to almost double from current levels if they were to revisit the levels seen in the beginning of 2023.

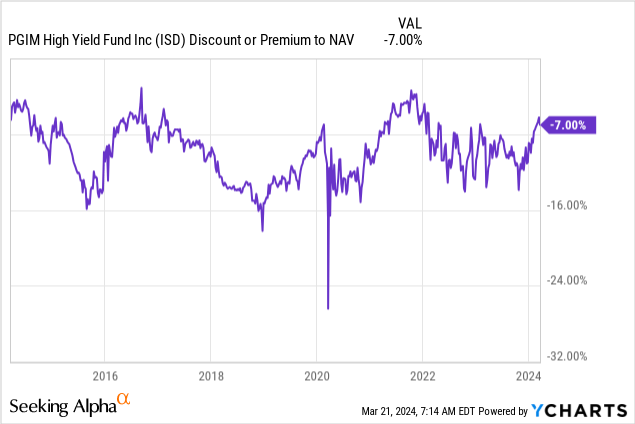

Discount To NAV Moving Towards Historic Highs

The discount to NAV for the CEF has narrowed, now being close to decade-long highs of -5%:

Most high-yield CEFs exhibit this beta with market conditions, where a rally in HY fixed income is well correlated with a narrowing of the discount to NAV. In the CEF space historic narrow levels should be sold, while very wide levels should be bought, all else equal with respect to the underlying build and credit risk taken.

ISD has simply repriced higher as anticipated, but we expect the name to trade at the current discount going forward, given the CEF pricing for the manager’s platform.

The z-score for the discount to NAV, which currently clocks-in at 1.9, tells the story of a stretched metric here, with a 1.9 standard deviation out against the mean for observable historic levels.

Analytics

- AUM: $0.42 billion.

- Sharpe Ratio: 0.07 (3Y).

- Std. Deviation: 10 (3Y).

- Yield: 10%.

- Premium/Discount to NAV: -7%

- Z-Stat: 1.9.

- Leverage Ratio: 22%.

- Composition: Fixed Income – U.S. High Yield

- Duration: 4.3 years.

- Expense Ratio: 1.48%.

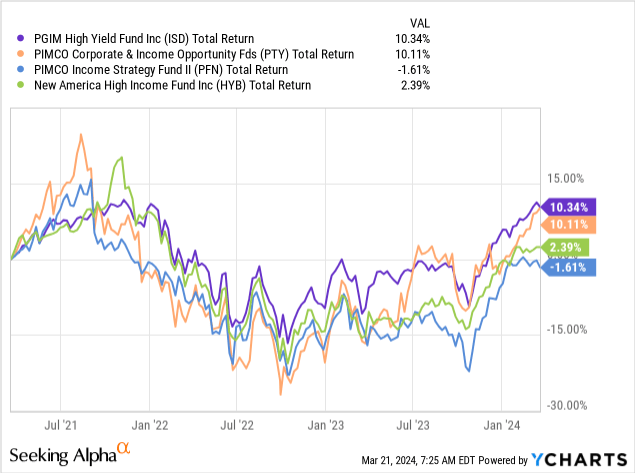

Performance Has Been Robust Making This CEF A Hold

The fund has delivered through this monetary tightening cycle when compared to some of its peers from large asset management platforms:

When we compare the CEF with its peers such as the PIMCO Corporate & Income Opportunity Fund (PTY), the PIMCO Income Strategy Fund II (PFN) or the New America High Income Fund (HYB), we can see ISD at the top of the cohort on a 3-year lookback. These are very robust results for the fund, and they speak highly regarding the portfolio management team.

To put it into context, ISD has been able to make a +10% return during one of the most rapid monetary tightening environments in recent history. That is no small feat, and shines a positive light on the fund managers here.

While the current price point is no longer appealing for an entry into the name, the CEF represents a solid choice to hold given its high dividend distribution and the ability of its management team to successfully navigate economic cycles.

Fund Composition Has Not Changed

Since we wrote about the name six months ago, the fund composition has not altered significantly:

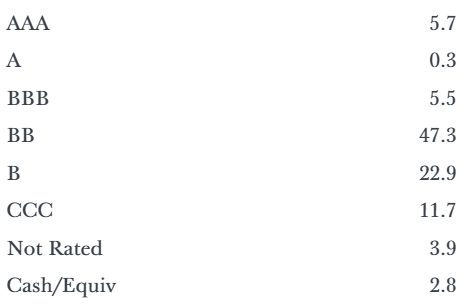

Ratings (Fund Website)

The credit quality of the portfolio has remained the same, with a BB/B weighting and a CCC bucket of roughly 11% of the underlying portfolio. This is a fairly classic build. The name has a slightly conservative tilt via its low leverage ratio and high concentration of BB names. We like this construction and feel this is an asset for holding a CEF in today’s goldilocks environment.

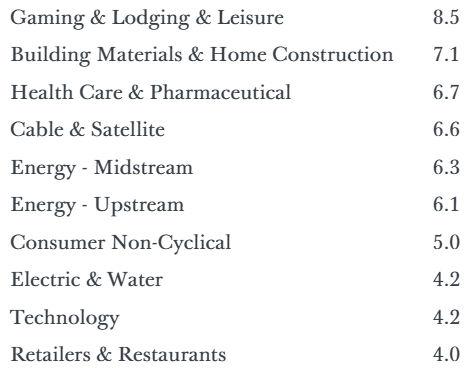

From a sectoral standpoint, the fund is well-diversified, with all of its sleeves coming in below 10% of the fund portfolio:

Sectors (Fund Website)

Gaming & Lodging represents the largest exposure at 8.5%, followed by Building Materials & Home Construction at 7.1%. Funds that take significant sectoral risks see their exposures top above 15% for any given industry group. This is not the case here.

Conclusion

ISD is a U.S.-focused high-yield CEF. The fund comes from Prudential Investment Management and represents a robust long-term performer. We covered this CEF six months ago with a ‘Buy’ rating, and the highlighted opportunity has proven to be very rewarding, with the CEF up significantly since. The factors that drove the initial ‘Buy’ rating have now run their course, making today’s entry point no longer attractive. With credit spreads at 5-year lows and the fund’s discount to NAV towards its historic high, ISD no longer presents an attractive entry point, but a robust hold for its 10% yield.

Q2 2024 Earnings Call Transcript")