Annaly Capital Management (NLY 0.85%) currently pays a monster dividend. The mortgage-focused real estate investment trust (REIT) yields nearly 14%. That’s about 10 times the S&P 500’s dividend yield.

However, the mortgage REIT‘s high-yielding payout comes with a huge caveat: Annaly has cut its dividend several times in the past, including by 26% last year. Here’s a look at whether its big-time payout could be in trouble again.

Barely earning enough to maintain its reset dividend

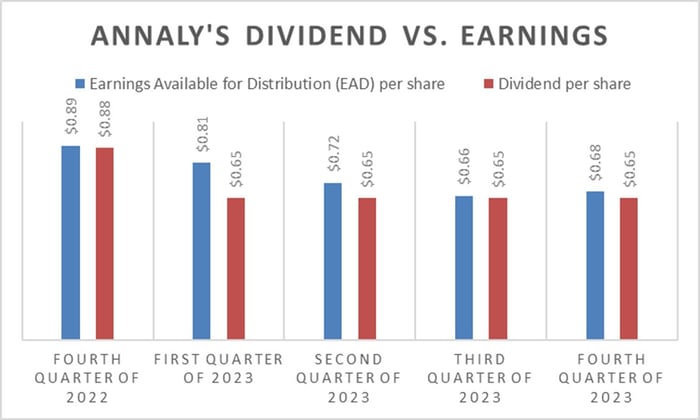

Annaly cut its dividend early last year due to the expectation that higher interest rates would weigh on its earnings available for distribution. That’s exactly what happened:

Data source: Annaly Capital Management. Chart by author.

As that chart shows, Annaly’s earnings declined through the first three quarters, nearly falling all the way down to its reset dividend level by the third quarter. However, it ended the year on a positive note.

CEO David Finkelstein commented on the company’s fourth-quarter conference call, “We outearned our dividend, with earnings available for distribution of $0.68 per share.” It achieved that result even though its leverage ratio declined to 5.7 times in the period (down from 6.4 times in the third quarter). The REIT benefited from improving conditions in the mortgage market and lower interest rate volatility.

Those improvements suggest Annaly’s reset dividend is on a more sustainable footing. As long as it can continue earning more than its dividend without taking on too much leverage, it should be able to maintain its current payment level.

A potentially troubling development

Dividend stability is a question on the minds of those who follow Annaly. An analyst on the company’s fourth-quarter call asked what many investors are wondering. Piper Sandler analyst Crispin Love queried:

Can you speak to how you’re thinking about the dividend level right now and sustainability in the current environment? You lowered your return assumptions across your strategies in the presentation. So, curious how that plays into how you think about the dividend level and core earnings power and returns relative to the $0.65 quarterly dividend?

The sharp-eyed analyst pointed out that Annaly’s latest investor presentation had the following illustrative returns for the current environment:

- Agency: 14%-16%

- Residential credit: 12%-15%

- MSR: 10%-12%

Those ranges were down from what the company provided in its third quarter presentation (17%-19% for agency, 14%-16% for residential credit, and 11%-13% for MSR).

Finkelstein answered, “We did moderate those return estimates, given the tightening that did occur later in the quarter.” However, he noted that the company did outearn its dividend in the fourth quarter, and “We do expect EAD to be contextual with the dividend (in the first quarter), which we feel good about.” That suggests its earnings should be around the dividend’s level in the current quarter.

Further, the CEO commented, “And at this time, our view is that it’s not our recommendation to the Board to make an adjustment to the dividend.” That means another dividend reduction isn’t currently in the plans.

However, Finkelstein cautioned that even though “we feel good about this quarter,” the company will “see how things progress throughout the rest of the year.” Those comments hint that if market conditions, return expectations, or earnings deteriorate, Annaly would consider another dividend adjustment.

The current dividend might not last much longer

Annaly Capital Management has struggled to sustain its dividend over the years. It has cut the payment several times due to the impact interest rates have had on its earnings. While the REIT believes it can maintain its current payment level through at least the first quarter, it could cut it again soon. Because of that, it’s not the best option for investors seeking a sustainable income stream.

Matthew DiLallo has positions in Annaly Capital Management. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")