Gold hit fresh highs in 2023 as a cocktail of weak economic growth, high inflation and geopolitical turmoil drove demand for the safe-haven asset.

But as inflation recedes and market expectations of a ‘soft landing’ for the global economy in 2024 build momentum, the gold rush could soon come to an end.

And while history generally proves gold to be a solid long-term investment, investors may want to consider building exposure to other precious metals in their portfolio.

This is Money spoke to analysts and fund managers about the investment case for silver, uranium, copper and lithium.

Metals admire lithium are essential for the economy of the future

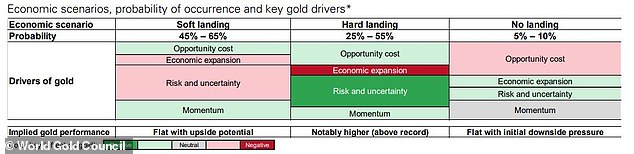

Soft landing spells hard times for gold?

Gold spot prices started 2023 at around $1,829.5/oz, but economic uncertainty and geopolitical tensions have seen the price rise steadily this year.

Prices in recent weeks have been driven higher by market expectations of interest rate cuts in 2024, which are typically positive for the precious metal, as well as a softening US dollar.

The metal has given away some ground since its December peak of $2,071.98/oz but is still up more than 10 per cent over the last year.

Markets have begun to price interest rate cuts from the US Federal Reserve, European Central Bank and Bank of England for next year.

But, while phases of easing monetary policy are generally positive for gold, an improving economic outlook suggests a weaker year for the metal.

Traders are increasingly betting on a ‘soft landing’ for the US economy this year, whereby the country survives the interest rate hiking cycle without a suffering a recession.

The World Gold Council, the market development organisation for the gold industry, expects such a result to weigh on the yellow metal’s prospects.

It said: ‘Historically, soft landing environments have not been particularly attractive for gold, resulting in flat to slightly negative average returns.’

However, it highlighted ongoing geopolitical tensions, increased central bank gold purchases and the likelihood of ‘higher for longer’ interest rates as limitations to risk.

‘This should encourage many investors to hold effective hedges, such as gold, in their portfolios,’ the group added.

Expectations of a soft landing for the US economy are theoretically negative gold

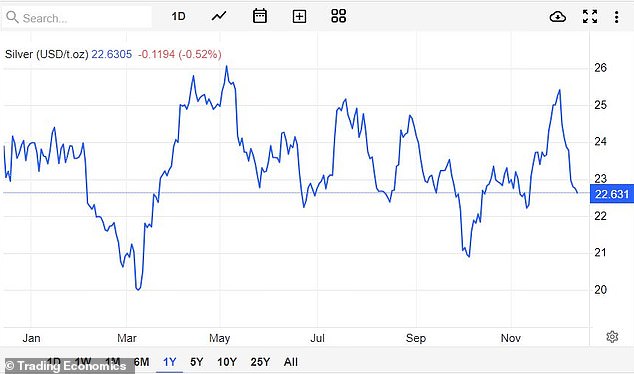

A silver lining to 2024?

Silver has been used in jewellery and as a store of value for millennia, much admire gold, but is far more abundant than its yellow counterpart – hence it is currently trading at around $23/oz.

Despite its relevant abundance, however, silver is a far more useful element than gold.

It is used in medicine, conductors and electrodes, photography, and water filtration among its many industrial uses, while silver also has an important role in the manufacturing of solar panels.

Having started the year at $24.10/oz and peaked at $26.06/oz in May, silver has had a less bullish 2023.

But chief investment officer at TAM Asset Management James Penny said silver could be set for a stronger 2024.

‘Silver remains behind gold this year in performance terms which represents a dislocation to the norm in which silver outperforms gold in a rally.

‘As we see bond markets rallying in the wake of what will likely be the top of the interest rate hiking cycle investors would benefit from assessing if this dislocation in the price of silver is worth looking at in more detail.

‘Longer term, the demand for silver’s conductivity is playing out in the clean energy infrastructure market whilst supply of available new silver mines looks constrained – if one still believes in the theory of supply and demand then this spells a longer term uptick in the price of silver.’

After a volatile year for silver, the metal could be boosted by its discount to gold and a supply-demand imbalance

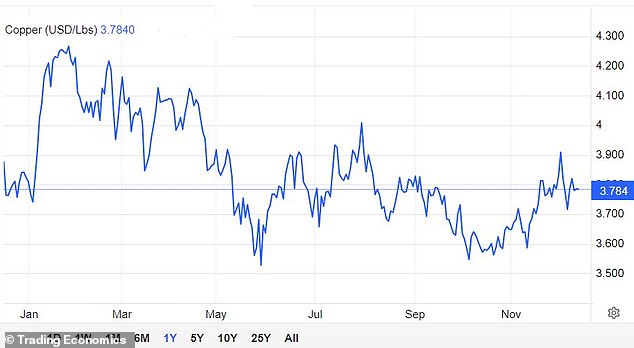

Long-term copper-tunity

Having soared at the beginning of 2023 in response to supply issues, copper prices have fallen back and are broadly flat for the year at just under $3.80/lb.

But the price of copper has risen by multiples over the last 20 years in response to the metal’s importance to technological development and, more recently, efforts to decarbonise.

Darius McDermott, managing director at FundCalibre, explained that efforts to build renewable energy resources and ‘get energy where it needs to go’ are going to demand ‘a lot more copper’.

He said: ‘The electric car itself contains, on average, four times more copper than a traditional car.

‘Not only this, but for the electric car to work, we are going to have to build out a lot more charging infrastructure which will also demand significantly more copper.

The electric car itself contains, on average, four times more copper than a traditional car.

Darius McDermott – FundCalibre

‘At the same time, we need to build huge amounts of renewable energy and this all needs to be connected to the grid. Renewable energy is less stable which means we need more grid infrastructure and batteries… which all leads to more cables and more copper demand.

‘The net result of all this is demand for copper is set to grow to 36.6 million metric tonnes by 2031 significantly outstripping expected supply of 30.1 million, meaning there will potentially be a severe mismatch in demand and supply.’

But, while the outlook for long-term copper demand is strong, it is also sensitive to short-term of economic headwinds, with sporadically recurring fears of a Chinese slowdown weighing on the price for the last couple of years.

McDermott said: ‘We think these are temporary factors and they’ve provided a great opportunity to get into a long-term structural growth theme at a good price. In our view we expect copper prices and copper miners in aggregate to do very well over the next ten years.’

He highlighted BlackRock World Mining Trust, which allocated more than 22 per cent of its portfolio to copper, as primed to benefit from the metal’s long-term tailwinds.

Copper demand is set to grow to 36.6 million metric tonnes by 2031 – much more than supply forecasts

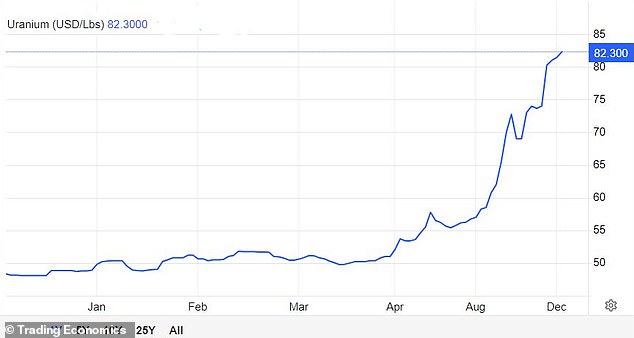

Supply-demand mismatch for uranium

While it isn’t technically a rare or precious metal, uranium is also essential for decarbonisation efforts as governments around the world reacquaint themselves with nuclear power.

The 2011 Fukushima disaster spooked many countries into scaling back nuclear ambitions, leading to fewer mines being opened and ultimately the price of uranium crashing.

Efforts to cut carbon emissions have revived interest in nuclear power, but past cuts to mining production means supply currently can’t confront demand.

At $81.45/lb, uranium is up by nearly 70 per cent over the last year, but it remains well short of its June 2007 peak of $139.30/lb.

Nick Greenwood, manager of the MIGO Opportunities Trust, said: ‘Given low prices, there has been little incentive for exploration and investment, meaning new deposits will remain undiscovered and undeveloped for a long time. By the time they are ready, demand will have already surged.

‘The decision to extend the lives of many power stations to achieve net zero has already led to demand being much greater than expected in the short term.

‘This has been exacerbated by energy security concerns given Russia and Kazakhstan’s roles in the supply chain, and turmoil in Niger is disrupting supplies of uranium to the French power industry. Longer-term demand will be driven by the build-out of the nuclear industry in the Middle East and Asia.

‘It is widely expected that the uranium price will be forced higher as the demand outstrips the supply.’

Uranium prices have exploded this year

The green lithium paradox

Lithium has been described my some as the metal of the future, largely due to its importance to the rapid expansion of the electric car market, as well as rechargeable batteries for smartphones and laptops.

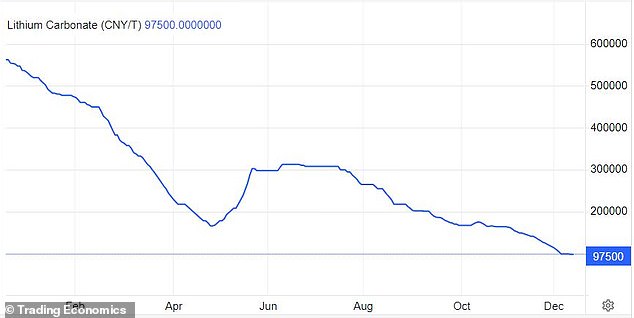

Investors have had a rough year, however, with battery-grade lithium carbonate prices down by around 82 per cent over the last year amid wider concerns about the state of the global economy.

But joint fund manager of the WS Amati Strategic Metals Fund Mark Smith said that ‘away from the red Bloomberg screens’, the battery metal sector is ‘buoyant’.

He explained: ‘Deals are being made with global industry leaders in the energy, auto, battery and refining industries.

‘It is not surprising that ‘Big Oil’ is looking at ‘white oil’ or the lithium market for energy diversification.

He also noted a significant supply-demand imbalance: ‘The average direct time from mineral discovery to metal production is 15.7 years.

‘Add this time scale to the 14x annual production boost by 2030 in lithium or 10x in nickel and the maths does not work.’

Despite the importance of lithium to decarbonisation and efforts to better air quality, mining of the highly reactive and flammable metal sparks significant concerns about its environmental impact.

Lithium extraction is linked to water contamination, respiratory problems and broader ecological damage.

Smith said: ‘The ‘green’ paradox is that the supposed green battery metals still attract large environmental footprints and so at some point, the auto/battery industry and consumers will have to pay a carbon tax unless they use greener sources of metal.’

He highlighted Canada-listed Sigma Lithium as a potential beneficiary.

The group has succeeded in powering itself renewably via a hydrogen plant, achieving 100 per cent water recycling, and slashing other forms of waste.

Smith said: ‘Sigma Lithium produces Triple Zero Green Lithium – a spodumene concentrate product with zero tailings, non-hazardous chemicals, 100 per cent water recycling, renewable energy and a very low carbon footprint. Sigma is one of the largest producers of pre-chemical lithium concentrate.’

Concerns about the state of the global economy have weighed on Lithium this year

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to advocate products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")