The artificial intelligence (AI) revolution is being supercharged by the “Magnificent Seven” stocks of Microsoft, Amazon, Alphabet, Apple, Tesla, Meta Platforms, and Nvidia (NVDA -5.55%).

With the exception of Apple and Tesla, each of these AI stocks has handily beaten the S&P 500 over the last year. Nvidia stands out in a league of its own, however.

The stock is up nearly 260% in the last year, and the company has added a trillion dollars of market cap in less than 12 months. With such a meteoric rise, investors may be thinking that they’ve missed the boat.

Let’s dig into the current state of Nvidia’s business and, more importantly, take a look at what catalysts could be in store for future growth. Now could be as good a time as ever to begin building a position in this monster AI stock.

What goes up must come down, right?

Nvidia manufactures graphics processing units (GPU) that are used across an array of generative AI applications, including accelerated computing and machine learning. Demand for the company’s flagship A100 and H100 chips is staggering, and it doesn’t seem to be slowing down.

Nvidia recently reported financial results for its fourth quarter and fiscal 2024, which ended Jan. 28. For the full year, the company generated $60.9 billion in revenue — up 126% year over year. But what’s even more encouraging is the company’s margin expansion and profitability growth.

In fiscal 2024, Nvidia’s gross margin was 72.7% — an increase of nearly 16 percentage points over the prior year. On top of that, the company’s free cash flow of $27 billion surged sixfold year over year.

With a financial performance like this, the music eventually has to stop, right? I wouldn’t bank on that just yet.

Image source: Getty Images.

Nvidia could just be getting started

Despite Nvidia’s record growth last year, the consensus among Wall Street analysts is that the ride could just be getting started.

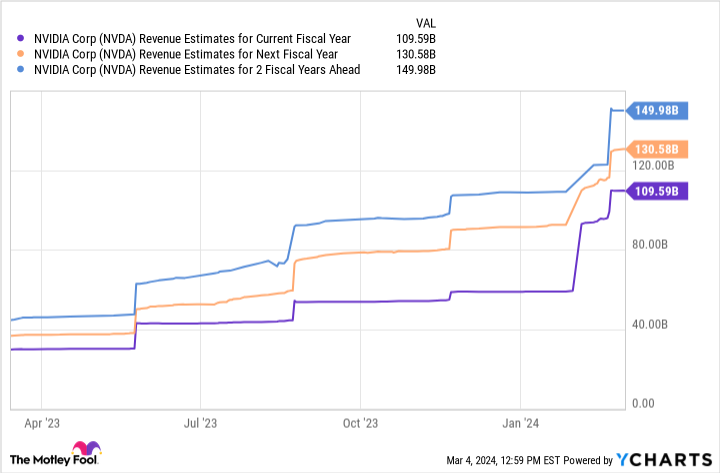

NVDA Revenue Estimates for Current Fiscal Year data by YCharts.

Nvidia is expected to increase its top line by roughly 78% this year, followed by modest growth over the next couple of years. Admittedly, forecasting beyond one year can be more of an art than a science. As an investor, I’m not placing too much credence on estimates beyond fiscal 2025.

One of the reasons I’m suspicious that the estimates above could be conservative is that investors are now just learning about some intriguing new catalysts. For starters, news broke a couple of weeks ago that Nvidia is an investor in voice-recognition software company SoundHound AI.

The terms of the partnership are not entirely known. However, Nvidia is just the latest big tech company to explore AI-powered voice assistants. Cohorts including Apple, Microsoft, Amazon, and Alphabet have all invested significantly in similar technology — thereby signaling that voice recognition could be a lucrative pocket of the overall AI landscape.

In addition, during the fourth-quarter earnings call, investors learned that Nvidia also has a budding enterprise software business. While it’s still early innings for Nvidia on the software front, I see many reasons to be optimistic about this endeavor. Namely, it shows that the company is already expanding beyond semiconductor chips.

Moreover, software tends to carry much higher margins than hardware development. Given that competition in semiconductor manufacturing will likely rise over the next few years, I wouldn’t be surprised to see some margin deterioration, as Nvidia will likely lose some of its pricing power.

Nevertheless, it appears the company is already looking to outmaneuver such a dynamic by complementing its core data center operation with a software component.

Is it too late to invest in Nvidia?

During fourth-quarter earnings, Nvidia CEO Jensen Huang made a bold statement when he declared that “accelerated computing and generative AI have hit the tipping point.” On the surface, you might think this means Nvidia’s rocket ship may be returning from orbit. But that’s not the case.

Rather, Huang went on to explain his philosophy in further detail. He believes that the installed base for data center infrastructure could double within the next five years. Given Nvidia’s commanding position in this market, combined with the catalysts outlined above, investors have several reasons to believe that there could be substantial upside in Nvidia stock.

Hans Mosesmann of Rosenblatt Securities recently slapped a $1,400 price target on Nvidia stock — implying roughly 60% upside from current trading levels. Whether or not Nvidia reaches this price, the bigger picture remains.

All things considered, secular trends fueling spend in artificial intelligence (AI) are expected to not only stay but actually rise significantly over the next several years. Given Nvidia’s unique position across both hardware and software, coupled with an increasing number of use cases and applications, I see Nvidia’s growth journey as just beginning.

Now could be an interesting time to begin using dollar-cost averaging to build a position or add to an existing holding in Nvidia stock.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")