For the first time in years, investors are struggling with what to make of Alphabet (GOOGL 1.52%) (GOOG 1.45%). The stock has continued to move higher, but the Google parent’s search engine has had more competition with the rise of ChatGPT. That stoked doubts about whether the “AI-first” company could be first in AI.

Nonetheless, investors should not fear it is too late to profit from this company. Here’s why.

The state of Alphabet’s AI

The doubts about Alphabet’s AI prowess are not without justification. Due to Microsoft‘s close relationship with ChatGPT creator OpenAI, consumers have more reason to turn to the Bing search engine instead of Google. Moreover, when it comes to AI, investors have tended to focus on companies such as Palantir, UiPath, or Nvidia rather than Alphabet.

However, to answer this competitive challenge, Google DeepMind has released Gemini, its most advanced generative AI model. The company claims Gemini can exceed state-of-the-art results in 30 of 32 academic benchmarks for large language models. Such results could convince investors that Alphabet will not be so easily surpassed in the AI field.

Other Alphabet businesses

Investors also have reasons for optimism that are less related to AI. Advertising revenue, which accounted for 78% of Alphabet’s top line in 2023’s third quarter, grew 9% year over year, suggesting that the long-awaited recovery in this market has begun.

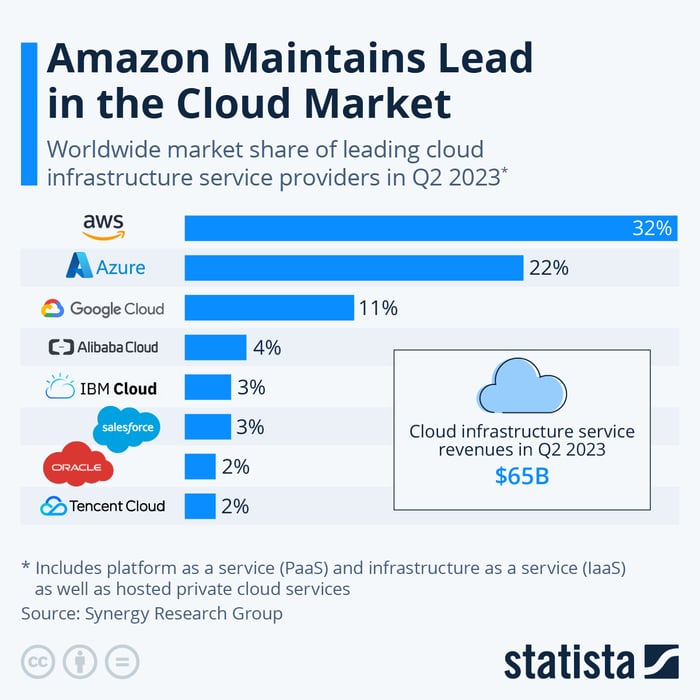

Moreover, Google Cloud, the company’s largest segment not directly tied to advertising, grew its revenue by 22% year over year in Q3. It is the third-largest cloud infrastructure provider, with an 11% market share as of Q2 2023.

Image source: Synergy Research Group.

Furthermore, Alphabet owns numerous businesses besides Google Cloud that are not broken out separately in the company’s financials. Verily Life Sciences and self-driving car company Waymo offer potential new avenues for revenue. They can also complement the company’s AI-related developments, creating a more urgent need to maintain a technical edge.

Alphabet by the numbers

Best of all, if Alphabet falls behind in any particular area, it holds the resources to catch up quickly. It held around $120 billion in liquidity at the end of Q3, and generated almost $23 billion in free cash flow in the period.

That may explain why the stock rose by about 54% over the past year, even if some investors doubted Alphabet’s position in AI. Despite that increase, Alphabet has the lowest P/E ratio among the “Magnificent Seven” companies, trading at just 26 times earnings. Such a valuation could induce some investors to add shares.

GOOGL PE Ratio data by YCharts.

Consider Alphabet stock

Considering Alphabet’s market position, cash reserves, and valuation, it is certainly not too late to buy shares. Admittedly, ChatGPT’s release caught investors off guard. Nonetheless, the release of Gemini shows that Alphabet still wants to be viewed as an AI-first company and will devote the resources necessary to maintain that claim.

Other businesses, like its crucial ad business and the emerging Google Cloud, have also shown signs of recovery. Considering its high level of liquidity and low valuation, Alphabet’s stock should remain an excellent choice for investors.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Will Healy has positions in Palantir Technologies. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Oracle, Palantir Technologies, Salesforce, Tencent, Tesla, and UiPath. The Motley Fool recommends Alibaba Group and International Business Machines. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")