The big news in banking this week is that Capital One Financial (COF 0.71%) is acquiring Discover Financial Services (DFS 1.37%). Capital One is the ninth-largest U.S. bank by assets, and Discover is a credit card network like Visa or Mastercard. Its model is more similar to American Express, just a lot smaller. Is that where Capital One is going?

What does this do for Capital One?

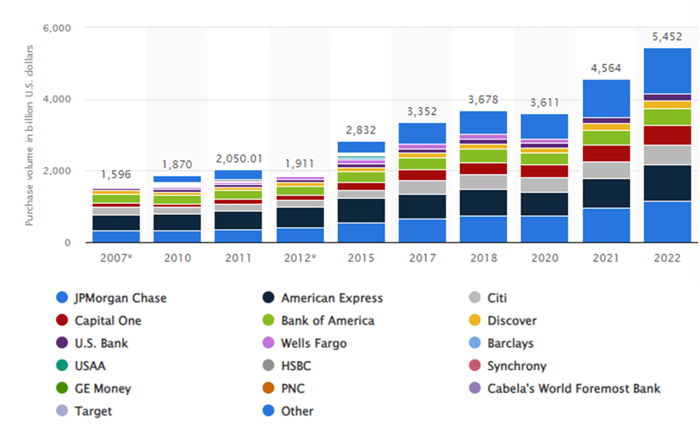

Capital One has revamped its credit card program over the past few years, leaning heavily on the American Express example of a large rewards program. This has helped it capture more credit card customers, and increased purchase volume has helped it offset the negative impact of higher interest rates on deposits, as well as increased its net interest income and margin.

Overall, credit card debt in the U.S. is growing. And while Capital One isn’t the biggest player, it’s growing its share.

Image source: Statista.

Discover issues its own credit cards, but it also has its own network, and that opens up new opportunities for Capital One. Acquiring Discover gives it more control over its credit card program and makes it more competitive. It gives it access to financial technology that complements its current infrastructure, differentiating it from the standard large bank.

The payments industry has changed with the advent of the digital payment industry, and there are all sorts of new payment methods today that rely on technology. This acquisition gives Capital One a larger global role in the future of payments.

The closed-loop system

On a deeper level, this could lead to a change in Capital One’s model that makes it more like American Express. Discover is the smallest of the four credit card networks and operates a closed-loop system like American Express.

Visa and Mastercard do not offer banking services nor underwrite the “loans,” or the credit customers use when they swipe their cards. They simply provide the network connecting the merchant, consumer, and bank, which lends the money for the purchase, and they work with an issuing financial institution. In contrast, American Express and Discover have a closed-loop system, where they act as their own issuing bank.

American Express has a specific niche with its target affluent clientele, fee-based cards, and robust rewards program. Discover doesn’t have that same niche, but Capital One’s acquisition will give the Discover network greater scale, and it could become more of a competitor in the mass credit card business. It could take this in several directions to stand out and offer something different from the American Express experience.

The Buffett connection

Capital One was in the news recently when Berkshire Hathaway took a position in it last year. Buffett loves bank stocks, so it wasn’t a surprise move. But why this one?

Capital One stock is trading cheaply right now at a price-to-book ratio of 0.9, or less than the value of its assets, and it’s also much cheaper than similar banks. It’s also consumer-facing, like Buffett favorite Bank of America. These characteristics appeal to Buffett’s approach to investing. American Express is also one of Buffett’s favorite stocks and Berkshire Hathaway‘s third-largest position, accounting for 8.7% of its equity holdings.

I wouldn’t say to jump into Capital One stock just because of this acquisition, which still has a few regulatory hurdles to pass before going through. But the stock did jump on the news because it could be a very exciting development for Capital One, and investors should stay tuned to see how it plays out.

Bank of America is an advertising partner of The Ascent, a Motley Fool company. American Express is an advertising partner of The Ascent, a Motley Fool company. Discover Financial Services is an advertising partner of The Ascent, a Motley Fool company. Jennifer Saibil has positions in American Express. The Motley Fool has positions in and recommends Bank of America, Berkshire Hathaway, Mastercard, and Visa. The Motley Fool recommends Discover Financial Services and recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")