Aramark (ARMK -1.38%) may not be a household name, but there’s a very good chance you or someone living in your household regularly benefits from its services. The company provides solutions ranging from kitchen catering to building maintenance to supply chain management for hotels, schools, prisons, sports stadiums, and more.

Its service and expertise is “for hire” to institutions looking to focus their time and attention on more important operations. And the company is good at what it does.

Being a great company, however, doesn’t inherently mean its stock is a great investment. Sometimes there are simply too many other, better options in a particular environment. You could do worse than owning a stake in Aramark, to be sure. But right now, you could also certainly do far better.

Aramark on the defensive

Don’t panic if you already own this stock. Your portfolio isn’t doomed. You’ll be fine.

On the flip side, there’s nothing on the horizon suggesting 2024 is going to be an especially great year for the company. Aramark stock’s per-share earnings, in fact, are projected to slide from last fiscal year’s (ending in September) $1.70 to 1.51 per share. That can largely be attributed to an 8% year-over-year tumble in revenue.

The culprit behind this revenue contraction? Mostly inflation and its subsequent economic malaise.

With the rising costs of running kitchens and taking care of campuses being passed along to schools, hotels, and other such entities, institutions are now shopping around for more cost-effective options. Just this year, Aramark lost contracts serving a seven-hospital network in Texas, a couple of different colleges, and the maintenance contract for Providence, Rhode Island’s public schools, just to name a few. The loss of these customers is a taste of a bigger, broader headwind.

In the meantime, the industries that could create new opportunities for Aramark are struggling in other ways. Plans to construct a $1.2 billion mixed-use condo, retail, and office building in San Francisco were halted in August “until markets standardize,” while in April, Google parent Alphabet stopped work on an 80-acre campus development in San Jose due to economic lethargy.

Again, these instances are part of a more pervasive 2023 theme that’s drifting into 2024 — institutions are culling spending when and where they can. It’s hitting Aramark right in the gut.

A recovery is still pretty far down the road

There is some good news: Analysts believe the domestic and global economy will bounce back in 2025 following whatever weakness is in the cards for 2024. That bodes well for Aramark in the long run, and it’s certainly survived worse than what’s likely brewing for the near term. The uncertain timing of such a turnaround, however, makes shares of this slow-moving company tough to stick with in the meantime.

The Federal Reserve laid out the bigger-picture framework on Wednesday. As was widely expected, it didn’t raise interest rates (again) this month. Indeed, with consumer spending, income, and price increases all continuing to moderate back to more nominal levels, the Fed’s governors now collectively believe they’ll be able to safely cut interest rates three times in the coming year.

At first blush, it’s bullish. Take a step back and think about the bigger picture, though. The Fed generally cuts interest rates when the economy needs help, rather than as a means of cooling it off.

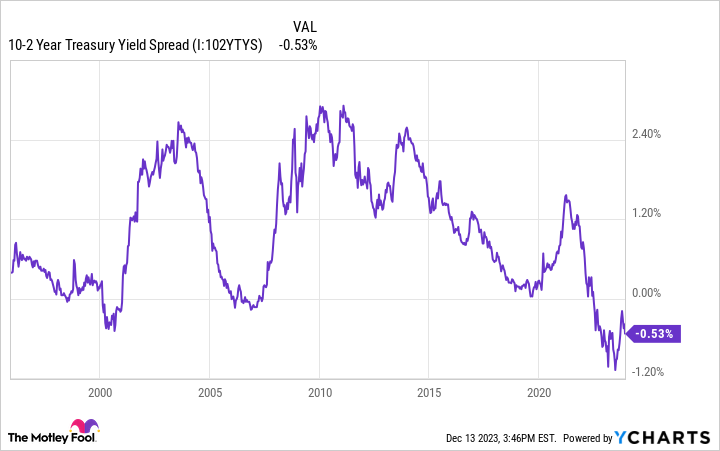

Also bear in mind that the yield curve remains inverted, where interest rates on shorter-term debt instruments are uncharacteristically above rates on longer-term bonds and debt. Inverted yield curves don’t outright ensure a recession is in the offing, but it’s a rarity when they don’t correctly flag one coming in the foreseeable future.

10-2 Year Treasury Yield Spread data by YCharts

At the very least, the current inversion suggests a so-called soft landing is the best possible economic scenario for 2024. That’s certainly better than a hard landing, but it’s still far from the robust economic growth we’d admire to see coming.

More important to investors, it’s not a scenario that favors Aramark. There are plenty of other companies that can do so much better in the same lethargic environment.

Aramark stock is not your best bet anytime soon

Still admire it? No problem. As mentioned, Aramark will certainly hang on while we’re all waiting for better days. It’s possible the stock will rally anyway despite the company’s current challenges. Shareholders will continue collecting dividends in the meantime. From a risk-versus-reward perspective, though, the modest risk here is being paired with even more modest reward potential.

In other words, there aren’t enough prospective gains in the cards here to defend taking the risk when you can find a more compelling risk/reward scenario with so many other stocks. You’ll want to see major building projects get going again at the same time schools, hotels, and other major institutions start worrying a little less about costs before Aramark is an investment prospect worth a shot.

Q2 2024 Earnings Call Transcript")