anyaberkut

InterDigital, Inc. (NASDAQ:IDCC) specializes in researching and developing new wireless, video, and emerging technologies to drive innovation in entertainment and telecommunications. IDCC monetizes its services through a licensing business model and has secured 30 licenses worth roughly $2.5 billion in the last three years. Moreover, recent patent renewals with Panasonic and Samsung Electronics showcase how embedded in today’s tech giants is IDCC, which supports its long-term prospects. In my valuation analysis, I conclude that IDCC is likely undervalued at the current levels, and I posit a $141.91 per share price target, rating it a “buy.”

A Patent-Based Operation: Business Overview

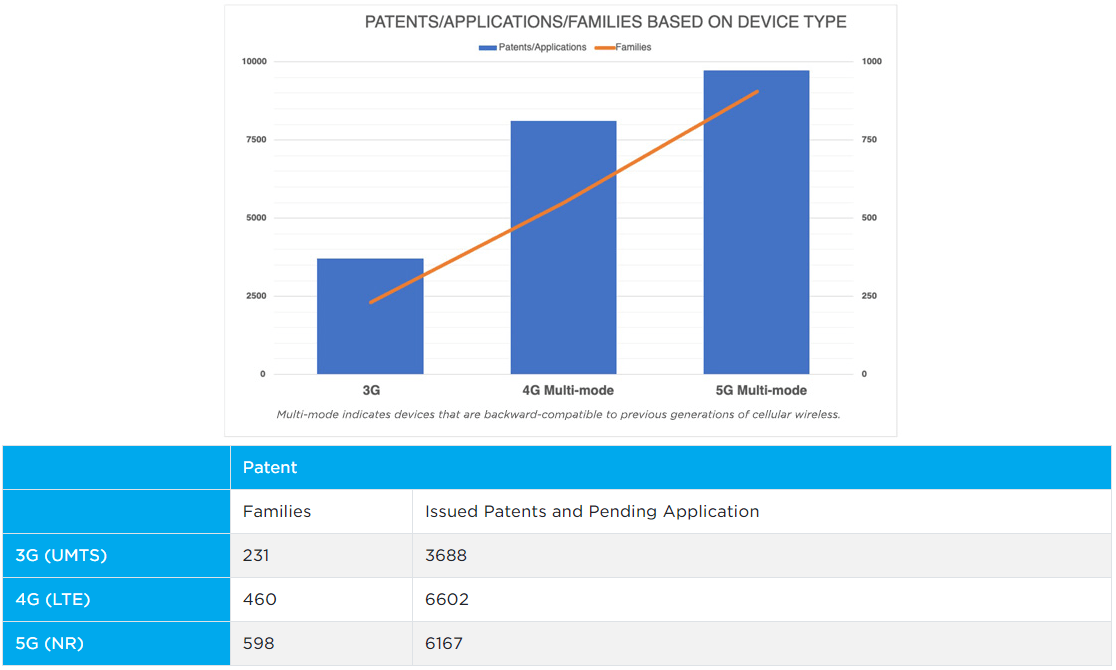

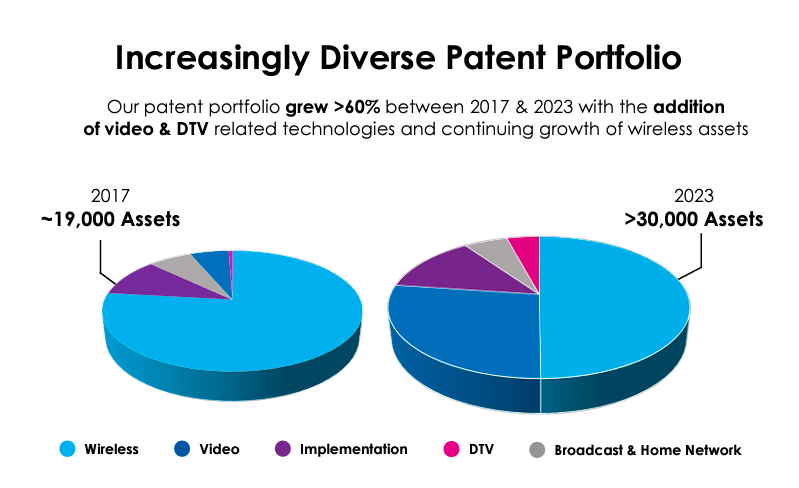

InterDigital is an innovative technology company researching and developing wireless, video, and artificial intelligence for mobile devices, networks, and services worldwide. The company was founded in 1972, and it went public in 1981. IDCC is based in Wilmington, Delaware. Its business has evolved, and today, IDCC mostly monetizes its IP through licensing agreements with manufacturers and service providers. IDCC is a particularly interesting company as its R&D efforts drive forward telecom and entertainment with enhanced connectivity and video innovations. IDCC has been closely related to contributions towards telecom standards such as 2G, 3G, 4G, and 5G. Today, IDCC holds thousands of patents in the US and internationally, over a thousand specifically related to mobile communications.

Source: IDCC’s website.

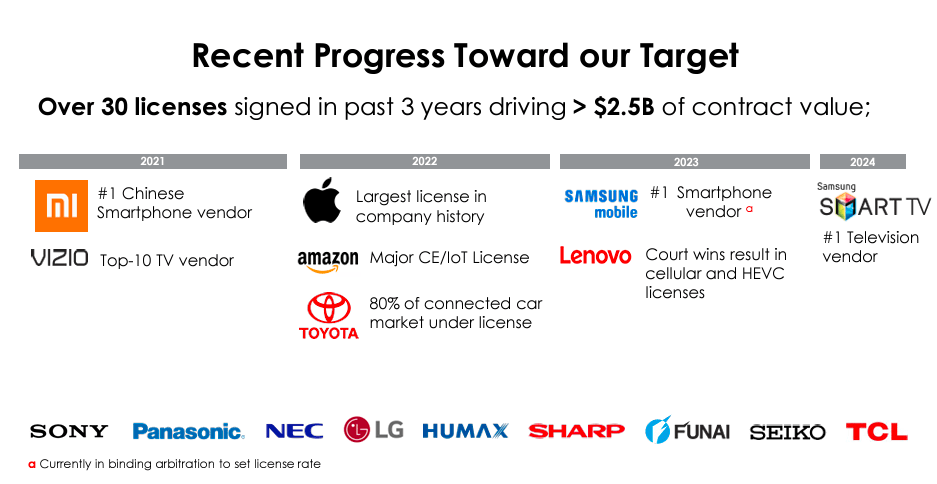

Furthermore, IDCC collaborates with partners from the industry, governments, and academia. In the past three years, IDCC delivered 30 licenses, driving $2.5 billion in contracts to clients such as Vizio, Apple, Amazon, Toyota, Lenovo, Samsung Smart TV, Sony, Panasonic, NEC, LG, Humax, Sharp, Funai, Seiko, and TCL. So evidently, IDCC is actively participating in the forefront of its niche, and its licensing agreements signal that major players recognize the company as such.

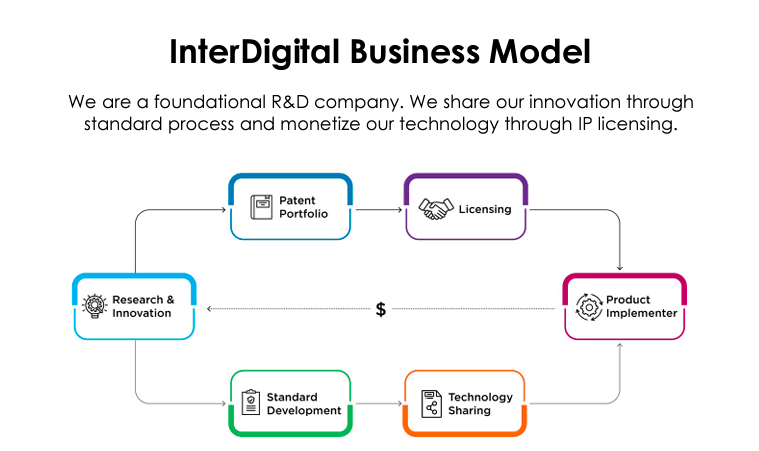

Additionally, IDCC also has relevant IP in wireless through the IEEE Standards Association and other organizations like IETF, ATIS, and ITU-R to conform the Wireless Standards Group to innovate in 5G system architecture, 5G RAN air interfaces and protocols, future Wi-Fi technologies, and IA applied to wireless. Overall, you can think of IDCC as a company focused on R&D, which generates patents and contributes to evolving technology standards. These patents and contributions are monetized via licensing and other agreements.

Source: InterDigital 26th Annual Needham Growth Conference, January 18, 2024.

Similarly, IDCC is in consortium with Next G Alliance, pre-standards groups, and universities, aiming to innovate standards around wireless technologies in the Future Wireless North America Group. This team works in advanced air interfaces, artificial intelligence, and machine learning [AI/ML] in wireless. Future Wireless Europe’s joint development is made through consortiums and industry collaboration among Horizon Europe, 6G-IA, and ETSI. These advanced research teams work to create future technology beyond 5G, which essentially positions IDCC’s IP for the next leg of telecom innovations.

Beyond Traditional Telecom IP: VR, AR, and AI/ML

IDCC’s Video Lab develops fundamental research to conceive new devices for improved multimedia experiences using lower energy consumption and data bandwidth through innovative video coding, computer vision and graphics, streaming, and artificial intelligence. This lab creates video solutions licenses for High Dynamic Range [HDR] technologies to amplify the range of color and contrast, providing more lifelike images using immersive standards like VVC Versatile Video Coding [VVC], Point Cloud Compression [PCC], and MPEG Immersive Video [MIV]. These standards are significant technological improvements for delivering data using current devices and network infrastructure. This enhances video compression for virtual reality [VR], augmented reality [AG], and 3D video. In other words, this is another key pillar of IDCC’s IP, especially as VR and AR increase adoption along with the growing metaverse narrative.

Source: InterDigital 26th Annual Needham Growth Conference, January 18, 2024.

Also, in the Video Lab, the teams include the 2D Video Standards Group, which explores novel video coding and transport technology for multimedia content. Here, the Immersive Standards Group develops codec schemas for wireless mixed reality experiences, and the MetaVideo Standards investigate new solutions for more efficient distribution and coding of video content using AI-based technology. Hence, IDCC is also a play on how AI will impact and become part of future technological standards in the industry. This is particularly promising as AI will undoubtedly push telecoms to create standards incorporating AI/ML, and IDCC’s IP portfolio will likely be well-positioned for that.

Source: InterDigital, Sidoti Conference, March 2022.

Indeed, IDCC’s AI Lab focuses on high-impact research using AI/ML to deliver the new era of wireless and immersive technologies related to blockchain and quantum computing. With these goals, the AI Lab uses mainly deep learning to develop solutions and support internal workflows. Besides, the Lab employs natural language processing [NLP] to analyze patents. Current research topics in this Lab include AI for Dynamic Wireless Environments, Deep Video and M2M Compression, and Quantum Computing for Future Wireless Communications. In short, IDCC is truly at the center of these evolving technological standards, and given the ongoing disruption in telecoms, I foresee IDCC’s IP portfolio will continue generating generous licensing revenues.

InterDigital’s Collaborations and Financial Outlook

More recently, on January 10, 2024, IDCC renewed its patent license agreement with Panasonic Entertainment & Communication for High-Efficiency Video Coding [HEVC] patents and digital TV licenses covered by the IDCC and Sony joint licensing program. Similarly, on January 16, 2024, IDCC signed a patent license agreement with Samsung Electronics, clearing up the previous dispute in arbitration. This agreement grants IDCC, Sony, and Samsung participation in a joint licensing program for ATSC 3.0, HEVC, Versatile Video Coding [VVC], and Wi-Fi technologies for digital TVs and Computer display monitors. Although I couldn’t find the agreement terms, they were likely substantial as HEVC, VVC, and Wi-Fi technologies are key for Samsung. It’ll be interesting to hear management’s commentary on this agreement in their upcoming earnings call, though IDCC recently hinted that they outperformed their previous guidance.

Source: InterDigital 26th Annual Needham Growth Conference, January 18, 2024.

In fact, we already have a relatively good idea about what we should expect from their report. The company’s financial outlook is mainly positive, as on January 16, 2024, IDCC announced that the company expects a Q4 2023 GAAP net income of roughly $34 million, with an estimated revenue of $105 million. The diluted earnings per share are anticipated to be around $1.20 above the expected $0.70 to $0.80 due to a value allowance against deferred tax in foreign assets.

Likely Undervalued: Valuation Analysis

However, from a valuation perspective, I think it’s better to take a step back and look at the bigger picture. As long as the company’s next report isn’t a complete disaster that forces me to reconsider my assessment, I believe a reasonable approach would be to look at IDCC’s revenue run rate since 2013. To do this, I simply averaged the company’s yearly revenue figures since 2013, which I estimate at $437.4 million per year if we include TTM data. Using the same approach, I calculated the average annual EBIT margin at 34.8%, with a standard deviation of 17.3%. This is key because IDCC’s operating margins have historically been volatile, so it’s a data point worth considering.

Source: Seeking Alpha.

Therefore, my approach yields an average annual EBIT run rate of approximately $152.3 million. Using one standard deviation for the EBIT margin, IDCC’s yearly EBIT could fluctuate between $76.8 and $227.8 million. Moreover, using the sector’s median forward EV/EBIT multiple of 21, I calculated my bear, base, and bull case price scenarios for IDCC. This is because the “fair value” enterprise value can be obtained by multiplying this median multiple with my previously estimated EBIT values. Then, I adjust those results for IDCC’s cash and total debt of $1.08 billion and $0.63 billion, respectively.

As a result, my approach yields price targets of $80.30, $141.91, and $203.53 for the bear, base, and bull cases, respectively. Given that my base case suggests a price target of $141.91 per share, I lean towards a bullish stance, rating it a “buy” at the current levels. My base case implies a potential upside of roughly 36.3% using today’s prices.

Investment Thesis Risks

However, it’s worth mentioning that IDCC does have its risks. I believe the main ones are litigation and regulation-related, as these are intricately tied to its patent-based business model. For instance, if the upcoming US elections result in elected officials that somehow change patent laws or weaken their enforcement, then IDCC’s prospects would significantly worsen.

My bear case is $80.30 per share. (Source: TradingView.)

Also, if IDCC has to spend significant amounts of capital on legal expenses to enforce its IP rights, it could drag its financials. In fact, we’ve already seen this happen to some extent with the recent patent dispute with Samsung. In this case, the dispute was resolved relatively quickly, but it’s possible that it won’t be as simple in the future. Lastly, my bear case scenario does contemplate lower EBIT margins, which are theoretically plausible using IDCC’s historical data. If EBIT margins worsen to that extent, it would be reasonable to conclude that the stock’s fair value could be much lower. However, I think these risks are mostly superseded by the base and bull assumptions I previously mentioned throughout this article.

Good Buy: Conclusion

Overall, I think it’s reasonable to be bullish on IDCC’s long-term prospects. This is a unique company with a patent-based business model with significant repeat revenues embedded in it. As a result, I estimate that its EBIT base and bull case run rates are sufficient to imply that IDCC is undervalued at these levels. Thus, despite the previously discussed risks, I rate the stock a “buy” with a $141.91 price target.

Q2 2024 Earnings Call Transcript")