zbruch

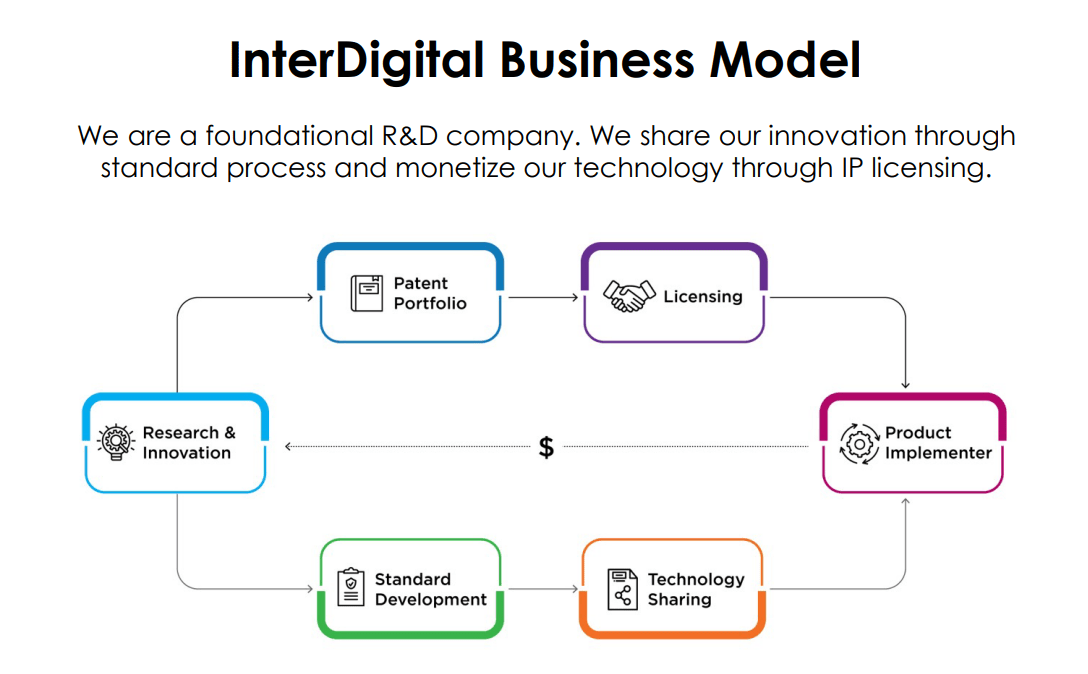

Business Overview/Investment Thesis

InterDigital (NASDAQ:IDCC) is a prominent research and development company that specializes in wireless, visual, and adjacent technologies. Its core focus is in designing/advancing wireless communication technologies along with developing cellular technologies. Additionally, the company is a leader in video compression and streaming technologies. InterDigital is at the forefront of harnessing Artificial Intelligence to enhance its video coding and support emerging technologies such as 6G networks. The company operates globally (United States, China, South Korea, Japan, Taiwan, and Europe).

IDCC Investor Relations

In terms of my investment thesis for InterDigital, I believe there is ~11% upside at current levels for the stock based on my DCF analysis that I will outline below. Overall, my thesis for strong growth for the company is due to its strong focus on research and development, coupled with its extensive patent portfolio. Both of these, in my view, position the company to capitalize on growing demands in the marketplace for connectivity and immersive experiences.

Revenue Growth Drivers

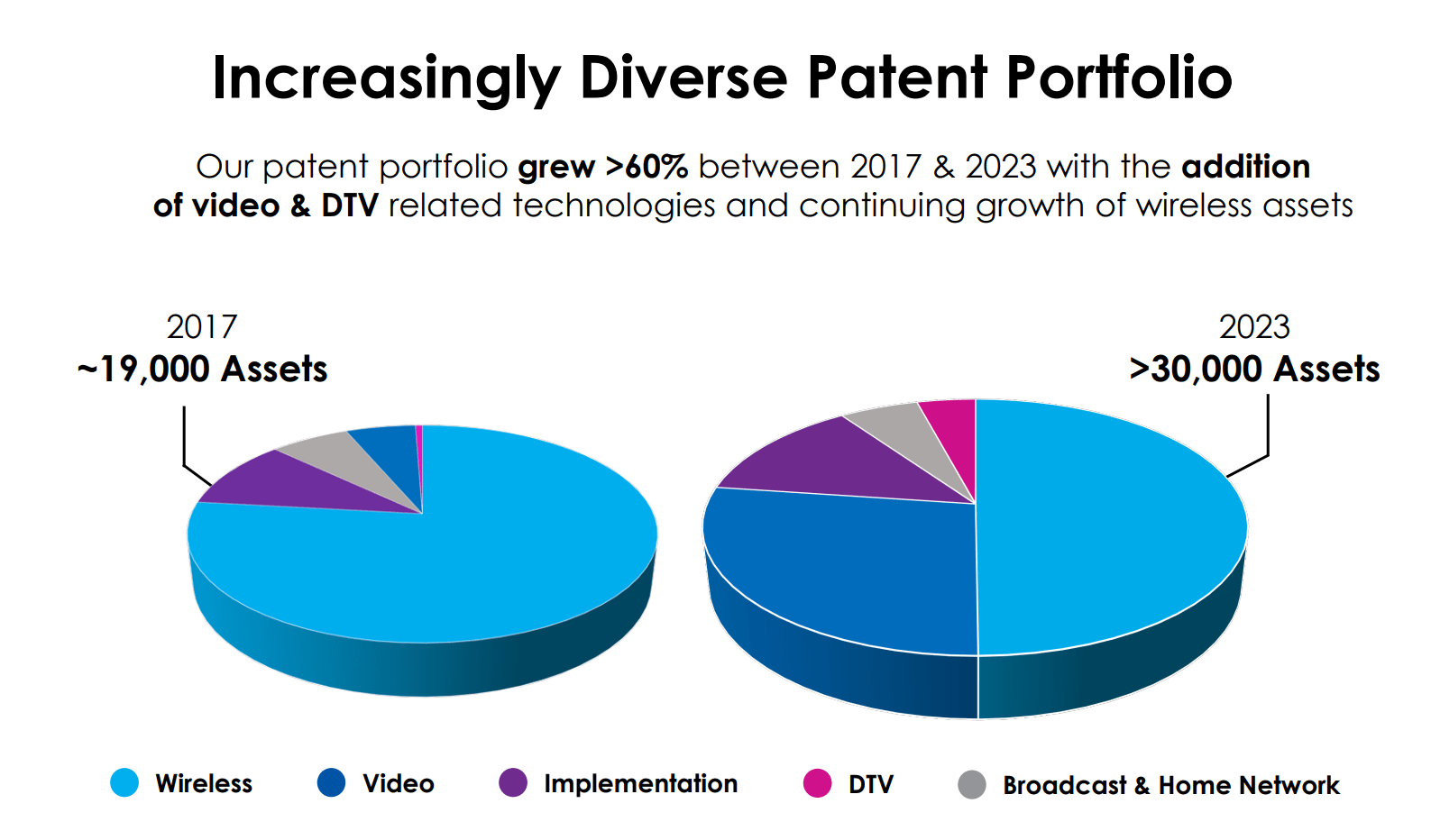

InterDigital’s primary revenue stream comes from its patent licensing agreements, which prove revenue stability and a recurring source of income for the company. This revenue is bolstered by renewals and new agreements with key players in need of wireless connectivity including Apple (AAPL), Samsung (OTCPK:SSNLF), and Amazon (AMZN). I believe this industry is only growing as work from home and Covid has created structural demand for connectivity in work places and to easily communicate from anywhere in the world. As a result, the company has a runway for growth in creating new patents to help serve this need.

IDCC Investor Relations

The company has grown its patents from ~19,000 in 2017 to >30,000 in 2023, a 56% increase. I see this only accelerating as the pace of wireless/video connectivity increases over the coming decade.

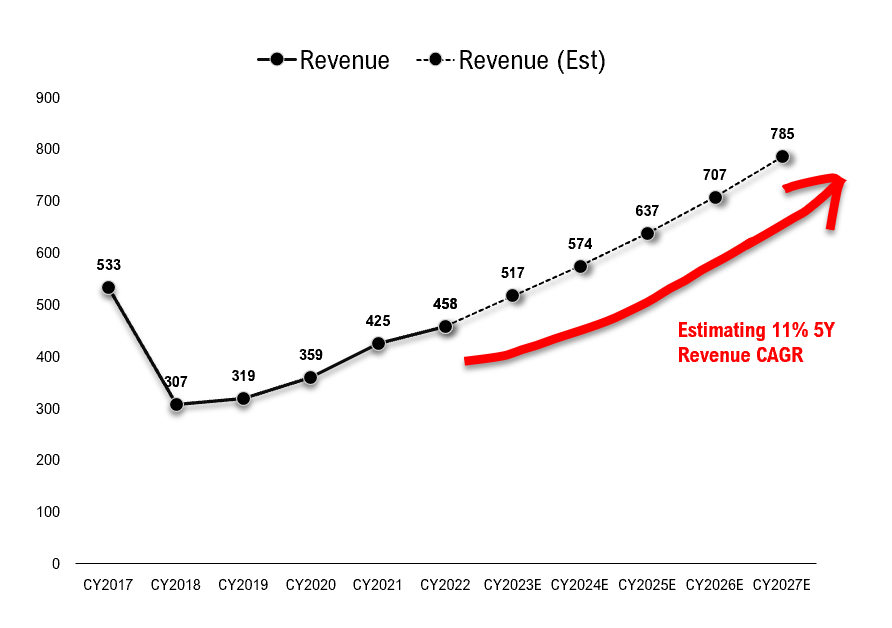

This leads me to my revenue growth assumptions for the company, which can be found below.

I assume an 11% CAGR for revenue over the next 5 years.

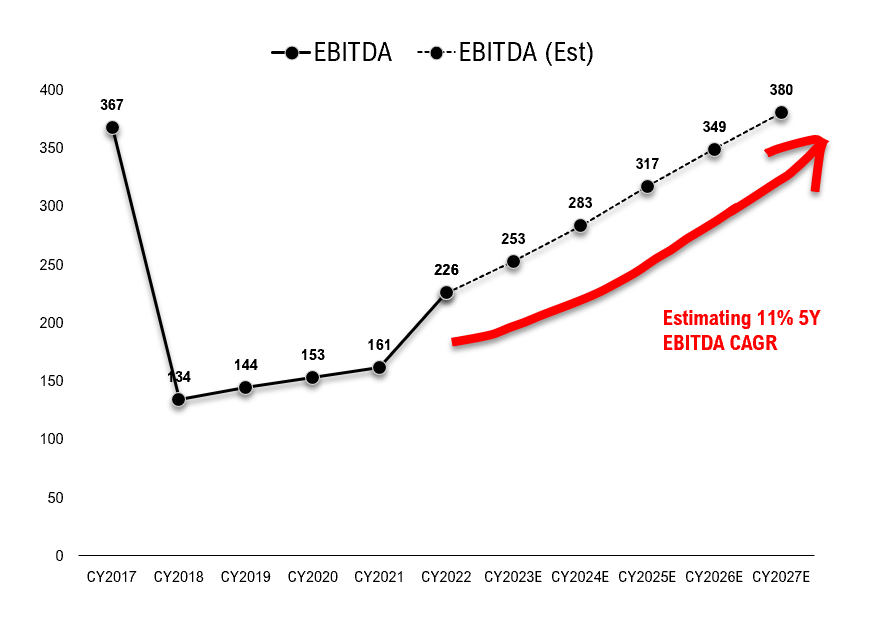

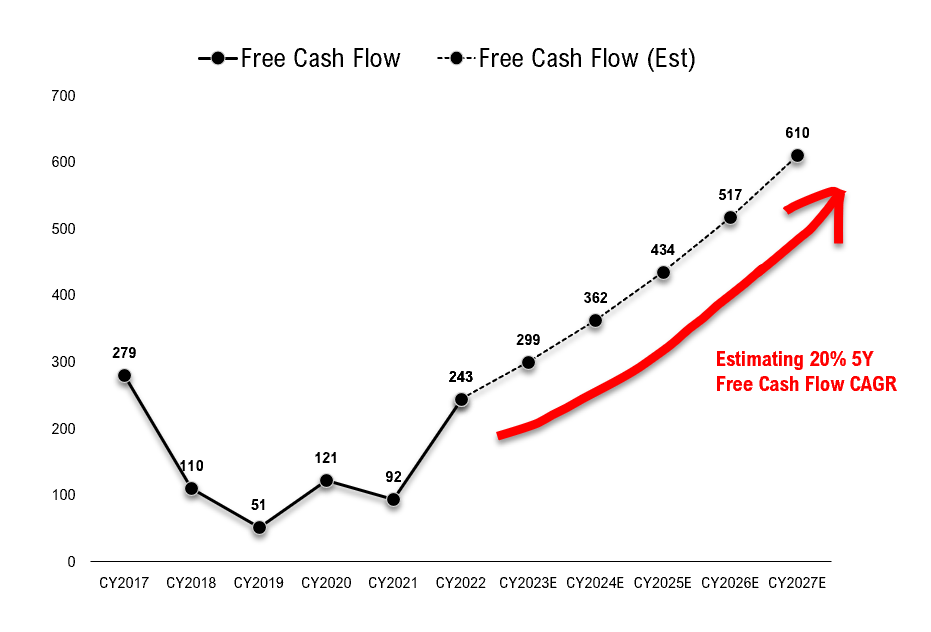

The Black Sheep Estimates + 10K SEC Filings

In terms of EBITDA/Free Cash flow, I see the company growing these categories at 11% (EBITDA) and 20% (Free cash flow) clips over the next 5 years.

The Black Sheep Estimates + 10K SEC Filings The Black Sheep Estimates + 10K SEC Filings

My optimism of strong EBITDA/Free cash flow revenue growth potential is due to the high margin business that InterDigital is creating.

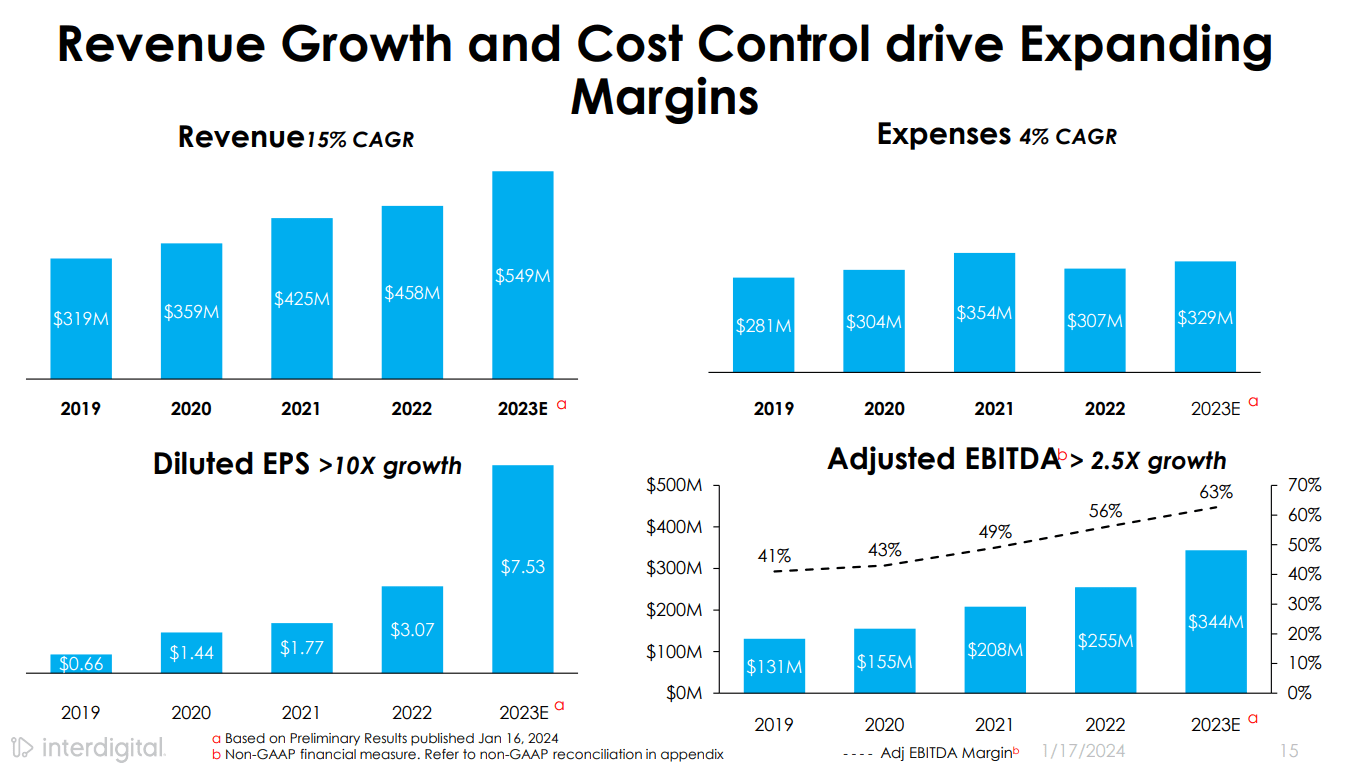

Take a look below, in the company’s Needham Tech conference slide deck, management highlighted its EBITDA growth and high (15% revenue CAGR) vs its 4% expense CAGR.

IDCC Investor Relations

If management is able to continue to deliver on this on a forward basis, that would make for strong free cash flow and EBITDA generation for the company.

Shareholder-Friendly Initiatives

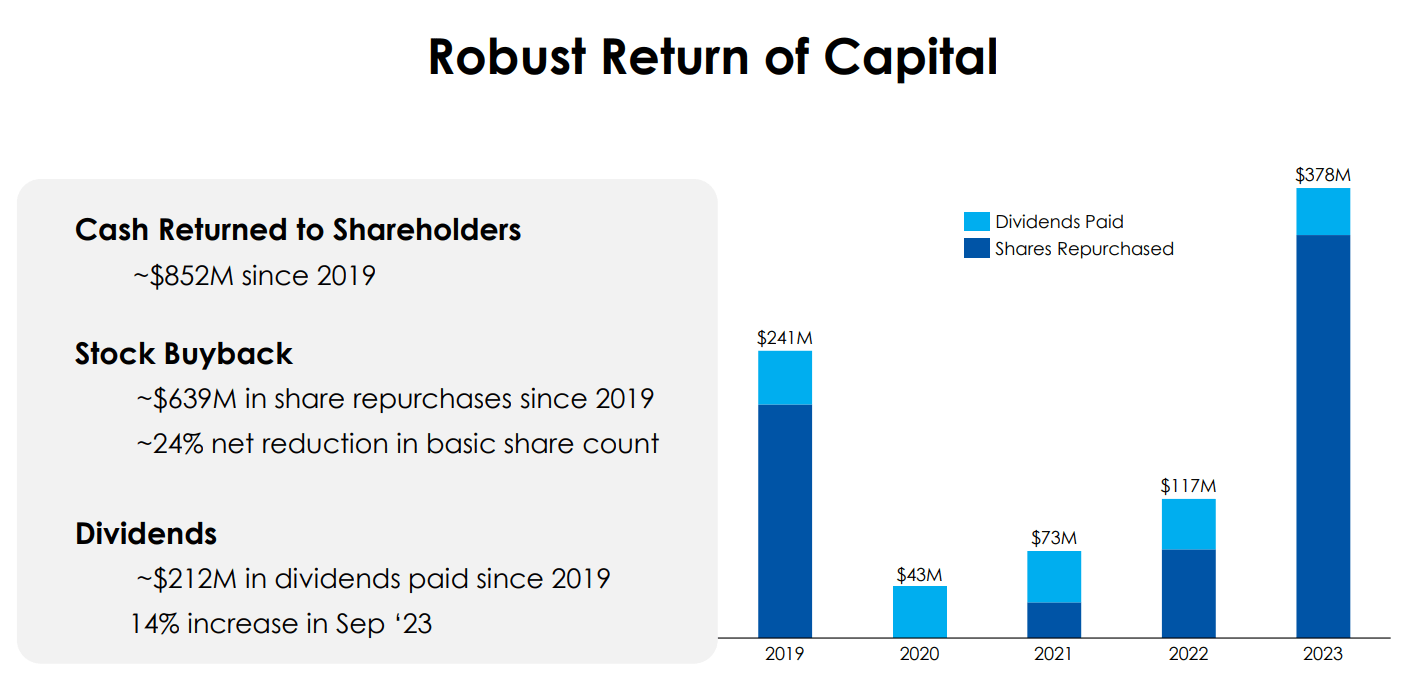

Not only is InterDigital delivering on its growth initiatives, but it is also employing shareholder friendly plans for capital redistribution.

IDCC Investor Relations

Take a look above, InterDigital has returned ~$852M since 2019 to its shareholders through the forms of both dividends and buybacks. I find this particularly attractive for shareholders, as they can be assured that management is on their side when it comes to driving returns.

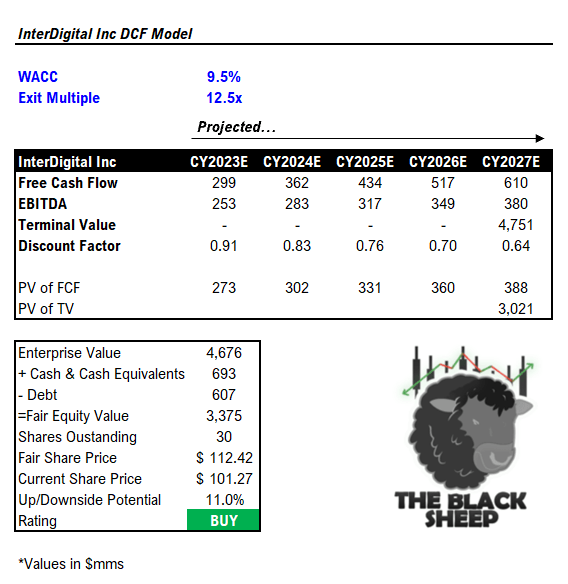

Valuation/DCF

Given my optimistic revenue, free cash flow, and EBITDA forecasts outlined above, below you will find my DCF model.

The Black Sheep and 10K SEC Filings

After summing all free cash flows, terminal value, discounting at the proper rate, adding net cash, and dividing by shares outstanding, I come to a final share price of $112.42, 11% above current levels.

This offers an attractive risk/reward for investors and leads me to my “buy rating” on the stock.

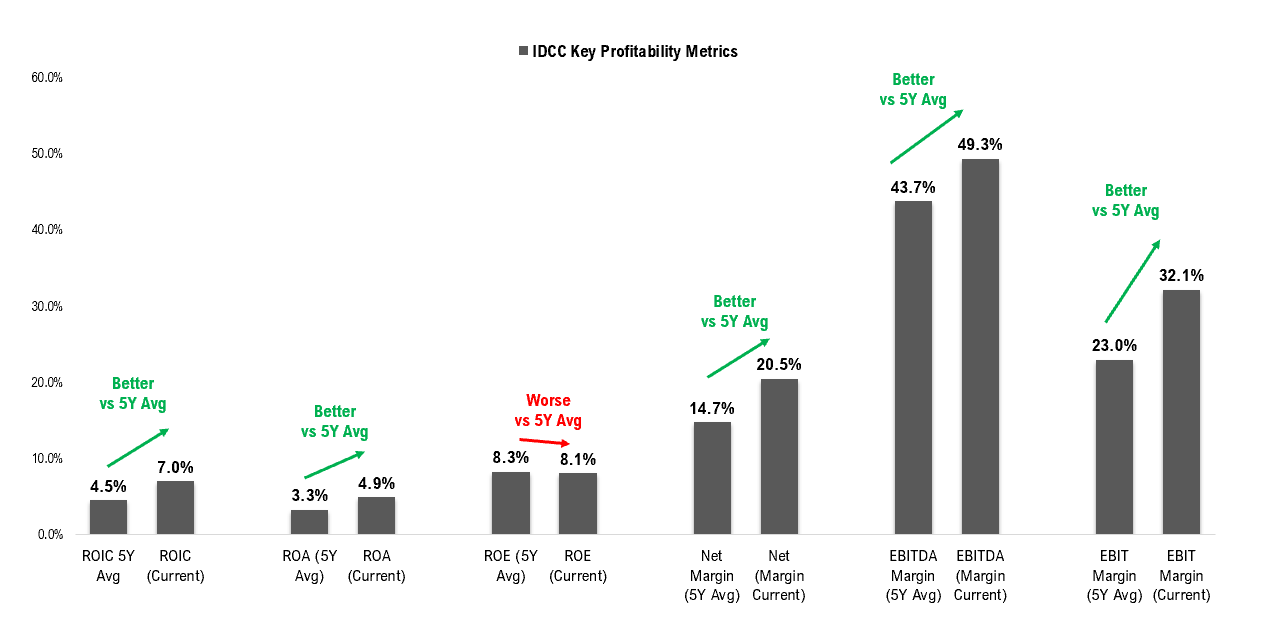

Profitability

In terms of profitability, 5 out of 6 of the key profitability metrics I track are currently above their 5-Year averages, respectively. The 6 metrics are ROIC, ROA, ROE, Net Margin, EBITDA Margin, and EBIT Margin.

The Black Sheep

$IDCC has seen improvement on all fronts except for ROE, but I don’t see this as an issue as ROE has barely budged from its 5Y Avg (only slightly decreased – so not a huge reason for concern).

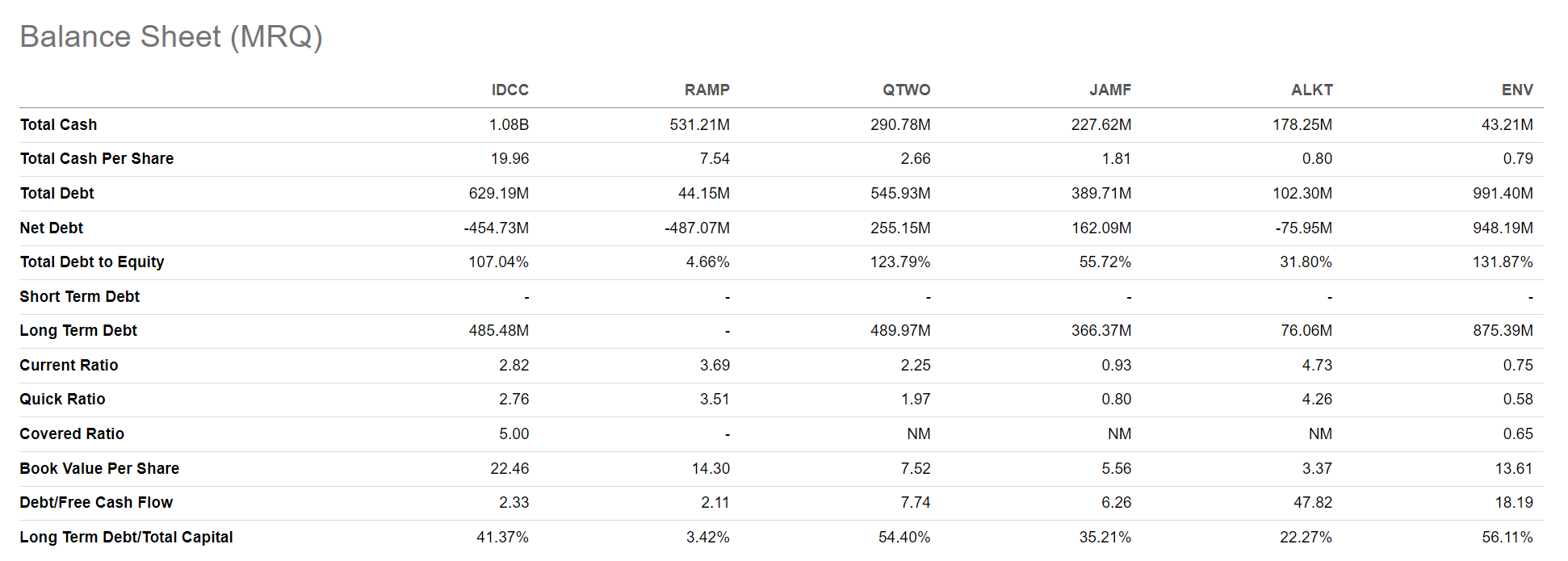

Balance Sheet/Competitive Landscape

In terms of the company’s balance sheet, $IDCC is in a strong financial position.

Take a look below:

Seeking Alpha Premium Feature

The highlights, in my view, are:

- Total cash of $1.08B (market cap is $2.63B, meaning 41% of the company’s total market cap is cash).

- Net debt is negative, meaning the company has more cash than debt (that’s a positive)

- Current and quick ratio both above 2 (very strong)

Comparing to its peers, this group all seems to be in “solid financial positions,” however $JAMF and $ENV both have current/quick ratios <1, which I view as unfavorable.

Also, $IDCC has the highest cash per share and has one of the lowest total net debt levels vs its peers. The only company with less net debt is $RAMP (-455M for IDCC vs, -487M for RAMP).

Taken together, IDCC’s balance sheet is in a strong absolute and relative position vs. its peers, which I view favorably for shareholders.

Key Risk

The main risk that I see for IDCC is the potential for its large customers (Think Apple and Samsung) to start creating patents in-house. We have seen this sort of consolidation with industries such as semiconductors, and thus, the small players tend to get wiped out as a result. I do not foresee this happening as IDCC’s patent portfolio is quite diverse/broad, but it is something to keep an eye on as the majority of its revenue comes from its in-house patent licensing.

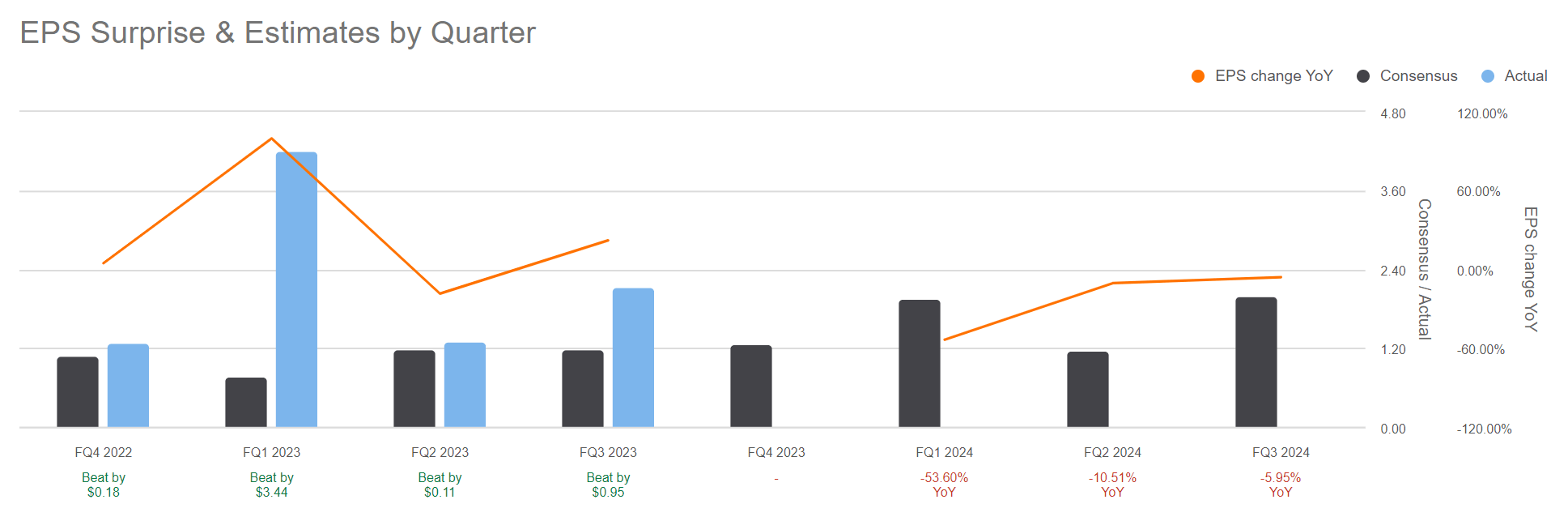

Earnings Preview

IDCC is slotted to report earnings before the bell on Feb 15, and consensus is calling for $1.26 in bottom line EPS.

Seeking Alpha EPS Surprise & Estimates Feature

When assessing earnings reports, I like to look at previous EPS estimates and see if the company has beat. It is the marking of a company whose management underpromises (guides low), but overdelivers (beats). That is a “shareholder-friendly company.”

Taking a look at IDCC’s past 4 EPS reports, the company has beat in each report by an average of $1.17. Here is a summary:

- FQ4 2022: Beat ($0.18)

- FQ1 2023: Beat ($3.44)

- FQ2 2023: Beat ($0.11)

- FQ3 2023: Beat ($0.95)

I see this trend continuing, considering the company’s track record in recent history of guiding low and beating on the bottom line. Hence, I am optimistic in the company’s EPS results coming in strong.

Conclusion

Overall, I see IDCC as a fantastic name within the IoT industry. The company is capitalizing on recurring revenue streams within its patent portfolio and working with some of the biggest names, including Apple and Samsung. The stock is cheap on an absolute basis, and based on my DCF analysis, the company has 11% upside from current levels. As such, I recommend a “buy” on IDCC stock at current levels.

Q2 2024 Earnings Call Transcript")