SerhioGrey/iStock via Getty Images

This is my eighth Inovio (NASDAQ:INO) article following my most recent 06/2023’s “Inovio: Microcap Biotech Struggling To Find Traction” (“Traction“).

For those confused by Inovio’s lead therapy change from long time leader INO-3100 to its current lead therapy INO-3107, check out the Switcheroo section of Traction. Subsequent to Traction Inovio clarified the situation with VGX-3100 in 08/2023 when it announced:

INOVIO has decided to cease all further development of VGX-3100 as a potential treatment for cervical HSIL in the United States.

As I write on 02/04/2024, Inovio’s future fortunes are all about its INO-3107. This article will focus on Inovio’s ambitious plans to capture a near term FDA approval for this molecule.

INO-3107 is a relative newcomer to Inovio’s pipeline

Looking back though my earlier Inovio articles I note that INO-3107 was absent from its pipeline as included in 04/2019’s “Inovio: Good Times Ahead?”. However by Inovio’s Q2, 2019 earnings call, then CEO Kim was enthusiastic about its prospects noting:

…we have deployed our resources to rapidly advance INO-3107 to treat RRP, or recurrent respiratory papillomatosis. RRP is a rare orphan disease caused by HPV 6 and 11 infections, for which Inovio recently demonstrated clinical benefit in a pilot study.

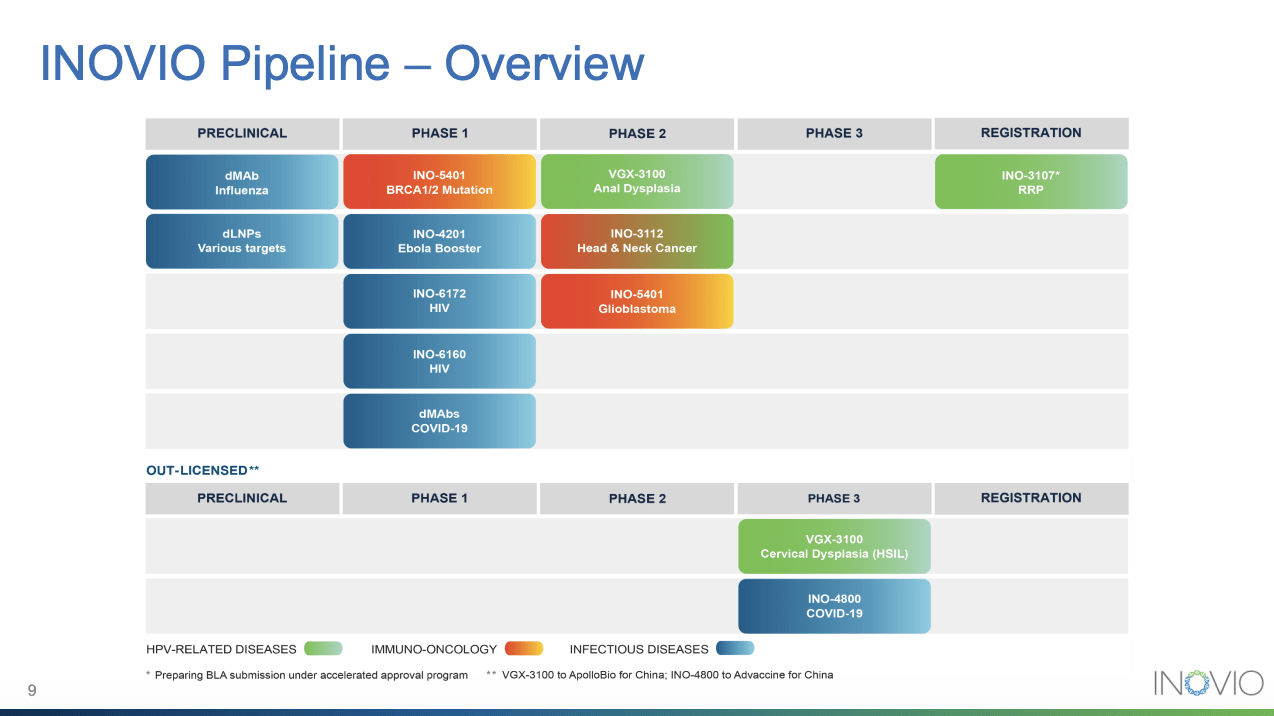

Inovio has moved rapidly ahead with its development of INO-3107. Inovio’s latest 01/2024 investor’s presentation (the “Presentation“) on its website accessed on 02/02/2024 lists the following pipeline slide:

inovio.com

This slide lists its INO-3107 as Inovio’s lead asset in a registrational trial. It notes its plan to develop INO-3107 in treatment of RRP with an accelerated approval BLA submission.

RRP is not a disease that has entered the everyday vernacular. It is a shorthand reference to recurrent respiratory papillomatosis. Traction notes how CEO Shea describes this awful affliction, it:

…attacks its victims with wart-like papillomas in the throat and in the airway. It is particularly nasty when these growths advance to impact breathing. Such an impact is most common in children because of the small size of their airways.

The current standard of care for treatment of RRP is surgery to remove the growths. Often recurrent surgeries are necessary; in some cases, over a patient’s life, many dozens of such surgeries. They devastate patients’ quality of life as they go through cycles dominated by preparation for, endurance of, and recovery from repeated surgeries.

Inovio envisions a potential 2025 launch for INO-3107

Inovio’s 08/2023 announcement of its Q2/2023 financial results with a strategic update first advised of its plans to file a BLA for INO-3107 in Q1, 2024. During its Q3, 2023 earnings call (the Call“) CEO Shea updated the situation advising of:

…significant progress advancing our lead candidate, INO-3107 for the treatment of … RRP. After two very important regulatory developments, we are closer than ever to … bringing the first DNA medicine to market in the United States. Specifically, in the third quarter of 2023, the FDA granted breakthrough therapy designation to INO-3107, based on clinical evidence indicating that it may demonstrate substantial improvement over existing therapies for RRP.

A couple of weeks following that breakthrough therapy designation, we received feedback from the FDA that data from our completed Phase 1 and 2 trial of 3107 could be used to support submission of a biological license application, or BLA, for review under the FDA’s accelerated approval program.

The referenced trial that Shea advised had advanced to pivotal status is labelled on clinicaltrials.gov as NCT04398433. The trial was a short one started on 06/15/2020 and completed on 12/15/2022. Officially titled “An Open-label Multi-center Study of INO-3107 With Electroporation (EP) in Subjects With HPV-6- and/or HPV-11-associated … RRP”.

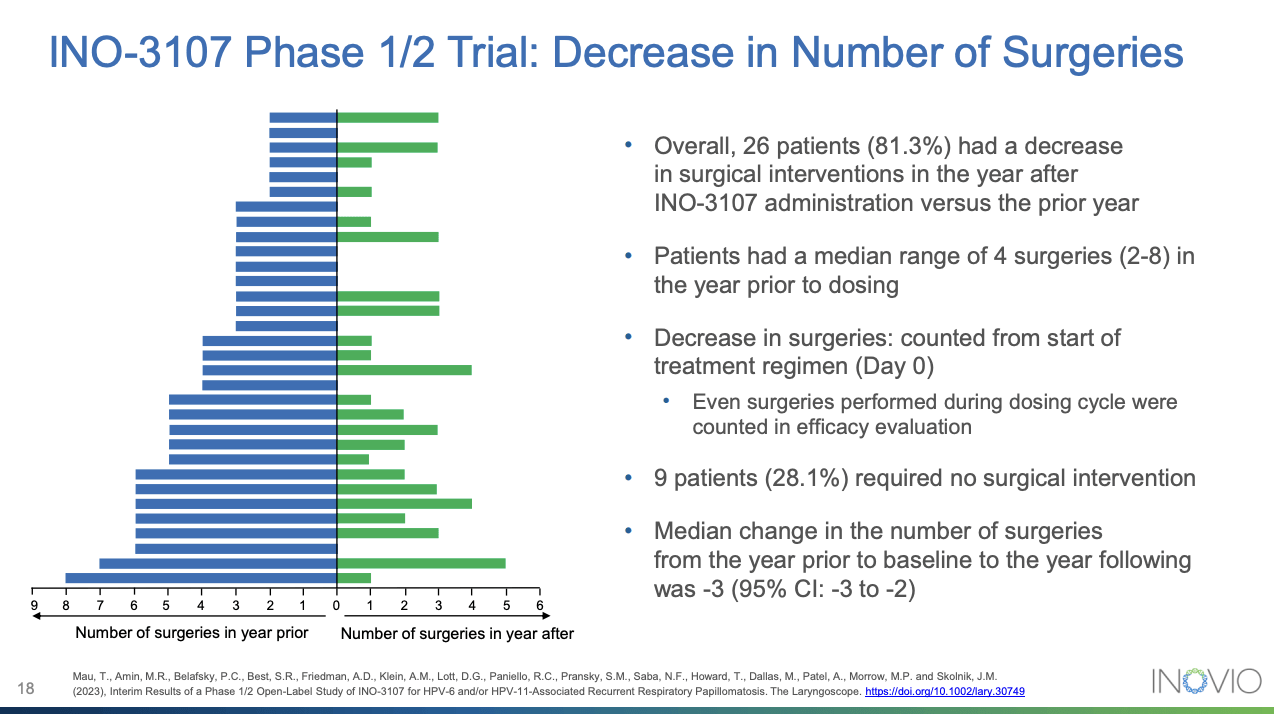

As a phase 1/2 trial with a mere 32 participants it was not an obvious candidate to support a later BLA filing. However that is what has happened. The trial results that have generated this unlikely situation are presented in graphic form by presentation slide 18 below; it shows a bar chart view with separate bars for each of the 32 trial participants:

seekingalpha.com

The blue bars on the left side of the chart show the number of surgeries for each of the 32 participants during the year prior to treatment with INO-3107. The green bars on the left side show the surgical interventions for each of the 32 patients during the year after treatment. Notably for nine of the patients there are no green bars on the right side, reflecting the nine patients who required no additional surgeries during the year following treatment with INO-3107.

The Presentation includes a variety of other slides highlighting various aspects of INO-3107. Notably they include:

- Slide 15 — captioned “Recurrent Respiratory Papillomatosis (RRP)” includes photos and basics of disease already covered plus its prevalence of ~14,000 active cases and incidence of ~1.8 per 100,000 new cases in adults;

- Slide 17 — captioned “INO-3107: Phase 1/2 Trial Design for RRP” with details about NCT04398433 its subsequently designated pivotal trial;

- Slide 19 — captioned “Immune Response – Patient in Phase 1/2 Trial” sets out graphs with INO-3107 effect on killer T cells;

- Slide 20 — captioned “Key Characteristics for INO-3107” setting out list for both key commercial and key clinical advantages of INO-3107;

- Slide 21 — “Key Catalysts for INO-3107” lists coming catalysts for INO-3107.

Despite an abysmal financial record, Inovio’s current liquidity should take it to an FDA decision on INO-3107

Per Inovio’s latest, its Q3, 2023 10-Q, Inovio has racked up an accumulated deficit of $1.6 billion over its lifetime. It has operated at a loss since its inception and expects to continue to do so for the foreseeable future. It had cash, cash equivalents and short-term investments of $167.5 million as of September 30, 2023. Its Presentation slide 35 pegs this as giving it a cash runway into Q2, 2025.

During the Call, CFO Kies reported on Inovio’s significant headway in reducing its operational spend for both Q3 and on a year to date basis. Presentation slide 4 reports how it has actually cut operating expenses in half in the first 9 months of 2023 versus the same period in 2022.

Kies advised that Inovio’s financial profile has changed with reductions in:

- drug manufacturing, clinical trial expenses, and outside services related to INO-4800 and other COVID-19 studies;

- employee and consultant compensation, including stock-based compensation;

- revenues from Department of Defense associated with INO-4800 which has been discontinued.

If INO-3107 should falter, Inovio’s investment prospects will be severely diminished

Inovio has generated significant shareholder angst and loss over its decades long efforts to commercialize its DNA medicines. As noted above its financial profile is unsteady. Bulls who elect to hold a position in Inovio can draw encouragement from its potential near term BLA filing.

Bears will hold back noting it lacks a track record of success in dealing with the FDA. It is common for inexperienced pharmas to misread their communications with the FDA. There are ever so many slips for pharmas twixt the cup of a planned filing and the lip of FDA approval.

Inovio is operating on a short leash. It has halved its spending at the expense of full development of its projects in development. In doing so it has extended its cash runway to Q2, 2025. This runway should be fine if it can indeed get its filing completed on schedule, and if the FDA accepts, processes and approves the filing on a timely basis.

Given Inovio’s long history of challenges the market will likely treat any hiccups with steep selloffs.

Conclusion

The risks of failure for drugs in development are daunting to be sure; how about the rewards for success? In Inovio’s case they are uncertain. We know that RRP can be massively damaging to infected patients in some cases. However there are potential limitations on the upside for INO-3107 even if approved.

Incidence of RRP depends to a significant extent on the prevalence of HPV vaccination. This should be considered a known unknown in terms of future incidence of RRP which will depend on the ebbs and flows of the culture wars. The two year cost of treating all cases of RRP in the US has been estimated at between $40-123 million. This suggests that INO-3107 will face limitations in its ability to charge for the treatment.

Q2 2024 Earnings Call Transcript")