Kimberly White

Innoviz and Design Deals

I wrote about Innoviz (NASDAQ:INVZ) in August after the company had a lot to announce on the path to growth with specific indications around BMW Group (OTCPK:BMWYY) and the relationship toward second-generation sensor InnovizTwo as a future B sample to be tested by it. Innoviz is a lidar company that won a design deal for the supply of lidar to BMW in 2018 with a sensor called InnovizOne. When the company went public via the SPAC route, it documented a potential of $2B from this collaboration in the so-called order book.

Six years later, the BMW I7 will be equipped with InnovizOne, providing an unspecified amount of revenue to Innoviz through its partner Magna International (MGA). Innoviz will be paid for the lidar components assembled by its tier 1 partner into the cars at low margins, motivating the company to become tier 1 in future deals. As my recent article about Luminar (LAZR) mentioned, 2024 will be a crucial year for the lidar companies. It will be a year of potential growth for Luminar as it showcases its manufacturing prowess. For Innoviz, it will be an opportunity to reaffirm its self-promoted reputation as one of the top companies in the lidar industry by securing large-scale design deals and potentially dominating the market.

Innoviz technology included in InnovizOne is based on MEMS, which utilizes microelectronic mirrors that scan the scene. In the second generation, InnovizTwo, a polygon or galvo mirror executes the scanning. The sensor is larger than the older version but uses less power with only one laser source versus three in InnovizOne. It provides 20 times better image quality and is 70% less costly, likely because of the reduction in EEL laser use.

In 2022, Innoviz won a design deal with Volkswagen (OTCPK:VWAGY) with InnovizTwo for unspecified brands and models. During Q2, 2023, as mentioned earlier, Innoviz stated it was negotiating with BMW for second-generation lidar design and the development of various software kits, including the Minimum Risk Maneuver system – offered in conjunction with the B-sample development program. Along with this news, Innoviz updated investors that it was developing a new piece of hardware, a computing module called InnovizCore. In the company’s words, the increased computing power strengthened software offerings and served as a base for future growth. A dedicated AI computing module directly connected to a vehicle’s operating system would provide Innoviz with a platform to do much more on the software side, including integrating data from other sensors, such as the radar or camera, and enabling over-the-air (OTA) updates.

The Update

To my surprise, yesterday Innoviz published news titled “Innoviz Announces Operational Realignment to Expand Cash Runway and Optimize Path Towards Profitability and Free Cash Flow,” given the following points:

Realignment actions will be implemented during the first quarter of 2024 and are expected to reduce cash outlays by $22-$24M annually. Anticipated savings are to be derived primarily from the transition of the InnovizOne program to series production and the concentration of future investments on the InnovizTwo sensor and perception software suite. Those actions would reduce Innoviz’s workforce by 13%. In addition, Innoviz made a point that it is concentrating investments on the InnovizTwo sensor and perception software platform, and by doing so, the company is reducing its investments in initiatives, including the Minimum Risk Maneuver (MRM) software solution and the InnovizCore AI compute module, along with other previously unannounced initiatives.

So, all initiatives from August have come to a surprising stop.

Q2 2023 Innoviz Presentation (Innoviz Technologies Inc.)

Based on the slide above, the discussed B sample for the second-generation relationship with BMW indicated the mentioned initiatives, including Core and MRM, as part of it. Hence, their reduction/elimination today left some unanswered questions about that relationship’s future. There is certainly an expectation that BMW will continue to be interested in InnovizTwo and the company’s perception software, which will likely be a detail most awaited for the Q4 update.

Profitability, Where?

Further, I was intrigued by the company, including its profitability path and free cash flow in the headline. I found no references to the path of free cash flow in the body of the news; I wondered how Innoviz finds the reduction of $22 to $24M of cash influencing its path to profitability or free cash flow.

I wanted to examine these statements by reviewing Innoviz’s financials for YTD 2023. I also looked at the current forecast for 2024 and 2025.

The most common formula of free cash flow would be the one used by Luminar, and it is:

FCF = operating cash flow – capital expenditures or investing activities cash flow.

Here is a YTD one for Innoviz in thousands of dollars:

(79,033) – (9,156) = (69,877)

A negative free cash flow indicates precisely that cash is depleting. Looking at the statement of profit, Innoviz has a loss of $93M for the year to date. The operating cash flow loss, as illustrated for three quarters, was $79M. That represents $26M of operating cash flow loss per quarter.

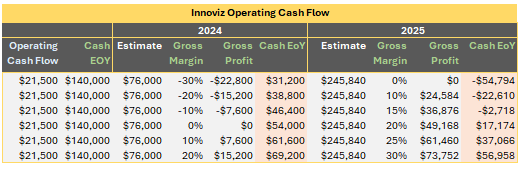

Therefore, on an annual basis, saving $24M would result in spending $81.3M. Using the statement from the news, “cash savings are expected to begin in the first quarter of 2024 with run rate savings expected to be achieved by the end of the second quarter of 2024,” in my analysis, I assumed Innoviz has two-quarters of $26M operating cash losses ending with Q1 2024. Therefore, Innoviz would enter 2024 with $140M, then Q1 would be $26M, and three quarters after would be just $20M for a total of $86M. I put this in the table below by averaging each quarter to $21.5M for 2024. For 2025, I adjusted the $6M out.

I also utilized the forecasts accumulated by SA for 2024 and 2025.

Innoviz Operating Cash Flow (Author, SA )

As with Luminar, when the analysis shows operating cash loss was more significant than the cash at the end of the year, it would trigger the equity sales to boost the cash levels.

Unfortunately, every single scenario in the model has resulted in equity sales. There is another caveat: The gross margin for Innoviz year to date is –157%. I used a variety of gross margins ranging from negative 30% to plus 20% in 2024 and from zero to 30% in 2025. Still, despite those optimistic assumptions, Innoviz runs out of cash in all scenarios and would lose more of it at current gross margins.

Conclusion

In conclusion, despite adjustments made, Innoviz’s financial outlook has not seen a positive shift in the business model. The absence of indications for profitability or free cash flow over the next two years is evident to me. As I await Innoviz’s Q4 update on February 28, the pressing question seems to be not if there will be subsequent financing but rather when it will occur. The ability of Innoviz to confirm its relationship with BMW and already secured design deals with others under these financial conditions also poses a question of feasibility. Since my initial “hold rating,” Innoviz has experienced a 54% decrease in value, but given the evolving landscape, maintaining this rating seems prudent until the upcoming Q4 report.

Q2 2024 Earnings Call Transcript")