Pgiam

Innovative Industrial Properties (NYSE:IIPR) has been in the doghouse for over a year at this point. That might change over the coming quarters as the possibility of a federal rescheduling may dramatically improve the credit profile of the tenant roster. In the meantime, IIPR continues to work through the troubled tenants in its portfolio. Wall Street appears concerned that there will be a never-ending sequence of troubled tenants, but this view is arguably already priced into the stock. I am downgrading the stock from “strong buy” to “buy” due to valuation, but remain of the view that the pessimism is overdone – the strong balance sheet and low valuation offer a wide margin of safety for value-minded investors.

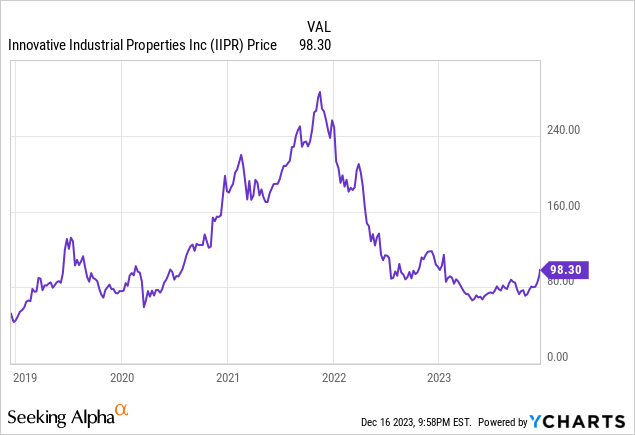

IIPR Stock Price

While there have been some short-lived rallies along the way, IIPR still remains far below all-time highs. In hindsight, the stock never should have traded so high in the first place, but these current levels are too extreme in the other direction.

I last covered IIPR in August where I named the stock a top pick in the cannabis sector. I remain of this view even if the multistate operator (‘MSO’) tenants may be getting more attention from investors.

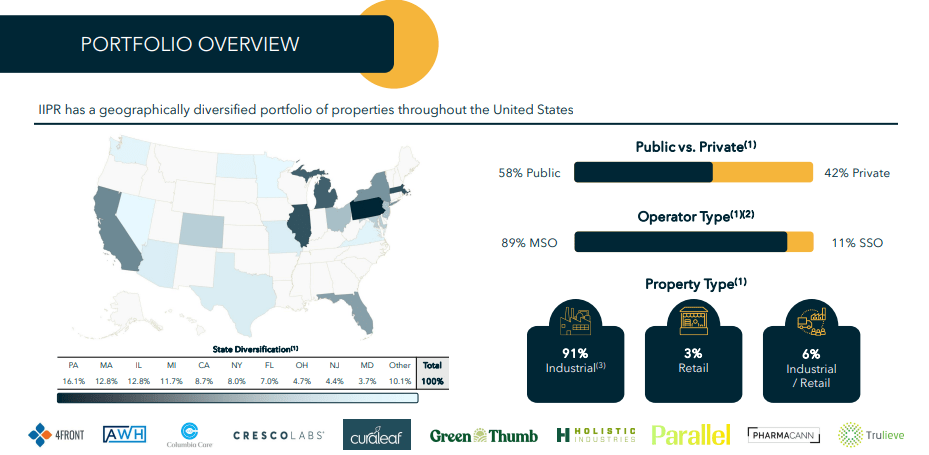

IIPR Stock Key Metrics

IIPR is a triple net lease REIT which means that its tenants are responsible for real estate taxes, insurance, and maintenance costs. That is the same lease structure employed by the more well-known peer Realty Income (O). The main difference is that IIPR has a focus on cannabis properties, with the vast majority of its properties being cultivation facilities. IIPR’s tenant roster includes some of the top names in the industry including Green Thumb Industries (OTCQX:GTBIF) and Trulieve (OTCQX:TCNNF).

2023 Q3 Presentation

In its most recent quarter, IIPR generated $77.8 million in revenue, representing 10% YoY growth. Adjusted funds from operations (‘AFFO’) was $2.29 per share, representing 7.5% YoY growth. AFFO is often considered a more accurate proxy for earnings for REITs due to adding back depreciation & amortization expenses. Experienced REIT investors may be wary that oftentimes AFFO is not a perfect earnings proxy due to the landlord having significant recurring CapEx, but as noted above that is not the case here due to the net lease structure. That $2.29 per share in AFFO comfortably covered the dividend of $1.82 per share.

Sale and leaseback transactions have stalled in the cannabis space, preventing IIPR and others from fully taking advantage of the higher interest rate environment. Many operators already have highly leveraged balance sheets and might not be so eager to take on more leverage at this time.

2023 Q3 Presentation

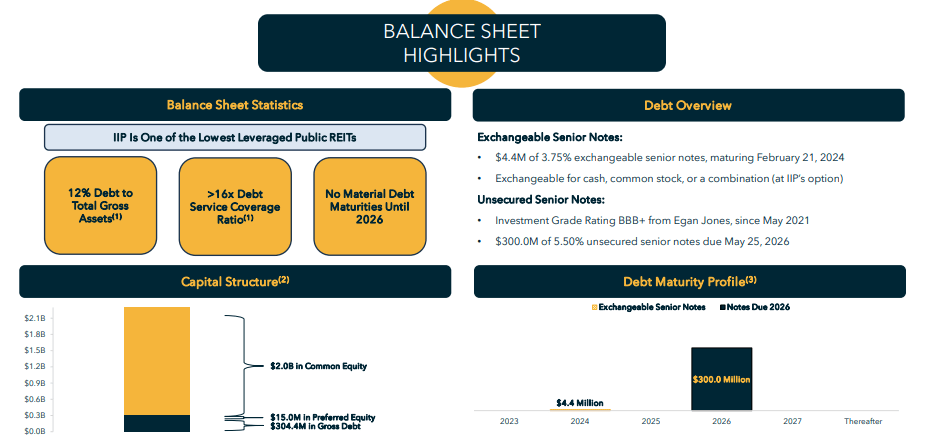

IIPR ended the quarter with just around $300 million in debt, representing around 1x debt to EBITDA, far below the typical 5x to 7x range seen at more conventional NNN REITs. The strong balance sheet is an important offsetting factor in the risk profile.

2023 Q3 Presentation

While the surface-level operating metrics were solid, Wall Street is understandably more concerned about the trouble potentially brewing under the surface. Rent collection stood at 97% during the quarter. That included $2.2 million of security deposits applied in connection with various amendments, which are expected to be paid back over the next 12 months. Excluding these security deposits, rent collection would have stood at around 94%. The $2.2 million in uncollected rent was related to tenant Parallel’s default property in Pennsylvania. On the conference call, management noted that they have concluded their litigation of this property, winning $15.5 million in damages and regaining ownership of that property. Management also noted that Parallel is currently on rent on their two properties in Florida. IIPR is still “actively exploring all options” for both the repossessed Pennsylvania and Texas properties. The Texas property was regained in March and is in early stages of development.

Tenant Green Peak had been placed into receivership in March. Since then, IIPR has regained possession of the Summit building property (a cultivation facility) as well as two retail locations. Management notes that the receiver is paying rent on the remaining properties. In October, following a court approval of a sale of Green Peak’s assets, the new buyer assumed the leases for the remaining cultivation facility and three retail locations “with no changes to terms.”

Management noted that for the Summit property referenced above they have “signed an LOI for that entire property.” Hopefully, the company can execute on bringing in a new tenant quickly.

In Massachusetts, tenant Temescal had a lease amendment that saw IIPR reduce base rent for certain months and boost rent for the remainder, and has started “paying rent in September, which has been fully collected through October.”

Why have I noted all of these tenant issues? REIT investors in general expect rent to be paid without drama. It is clear that there is plenty of “drama” at IIPR, even if the company has been able to minimize the impact on overall revenues thus far. With resolved tenant cases seemingly replaced in tandem by new tenant issues, IIPR now appears to be faced with an indefinite overhang. Wall Street may be concerned that there are additional tenant issues to be uncovered, but IIPR does not have at its disposal any way to speed up the resolution.

Is IIPR Stock A Buy, Sell, or Hold?

IIPR stock is priced at attractive levels. The stock is trading at just around 12x consensus FFO estimates. That places it at some discount to the 14x multiple at O in spite of the fact that IIPR has a stronger balance sheet and around 3% annual lease escalators. Whereas O and other conventional NNN REITs may face great headwinds from higher interest rates, IIPR is far more insulated from such headwinds and higher interest rates may even verify to be a tailwind once the acquisition pipeline picks up.

Seeking Alpha

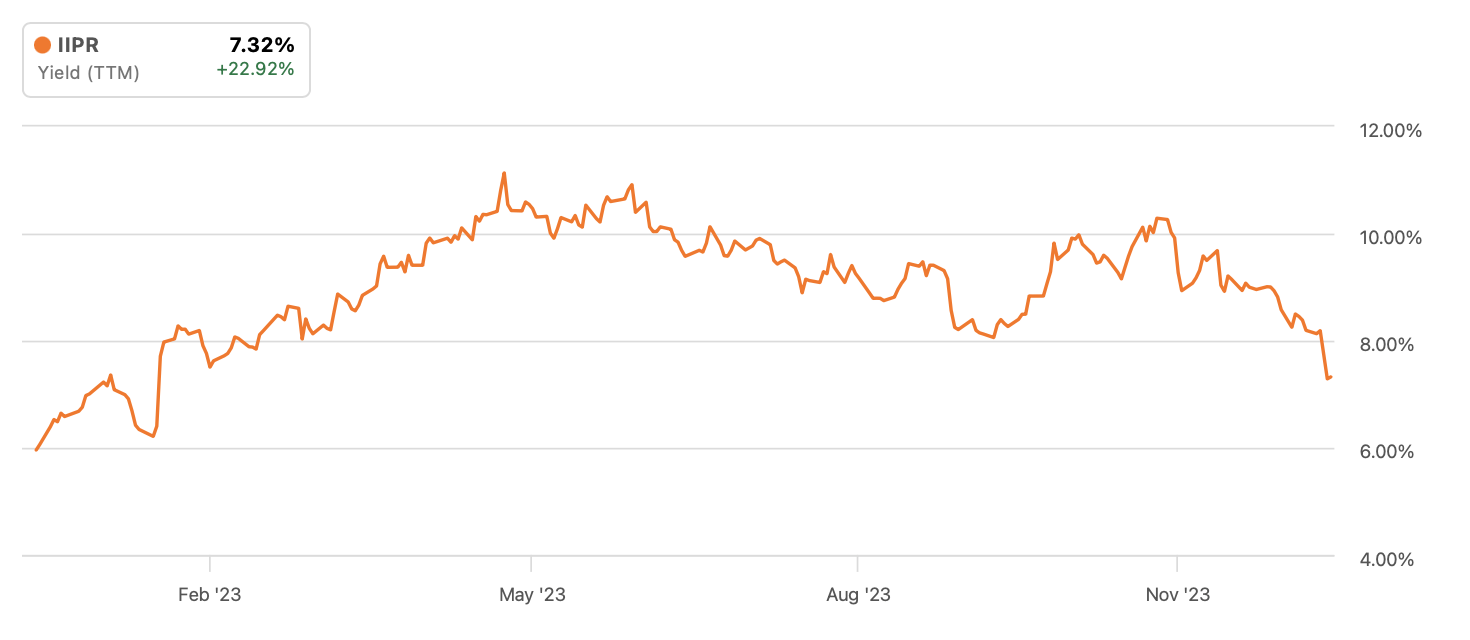

At a 7.4% dividend yield, IIPR looks very appealing to income-focused investors.

Seeking Alpha

Whenever a stock has a yield so high, we must wonder: what are we missing? It is clear that Wall Street is concerned about the prospects for a dividend cut, but I now make the case that this pessimism is priced in. For starters, it is important to note that IIPR’s properties arguably have strong barriers to entry due to regulatory restrictions (if nothing else, the smell from cultivation facilities makes it difficult to empower new competing facilities).

2023 Q3 Presentation

That means that even if a tenant defaults on their rent obligations, perhaps due to poor execution or too much debt, IIPR may be able to find replacement tenants without too many issues (the company has executed solidly on this front though its operating history is limited).

There is an important catalyst to consider. Back in October of 2022, President Biden had issued an executive order calling for an FDA review of cannabis’ classification. This summer, the HHS issued a recommendation to the DEA calling for cannabis to be re-scheduled to arrange II. That reclassification is expected to end “280e taxes,” which essentially force cannabis operators to pay corporate income tax based on gross profits. This would direct to a dramatic improvement in fundamentals across all of IIPR’s tenants and effectively crush the tenant quality bear thesis. It feels admire a matter of time before the DEA re-schedules cannabis to arrange III, but the stock is instead pricing in more tenant difficulties.

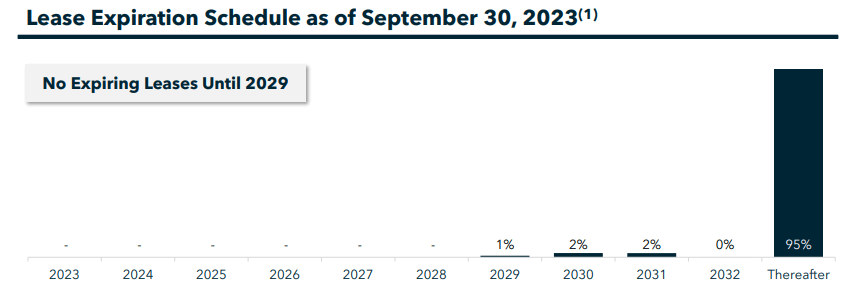

Some investors may be concerned that ongoing legislative reform may be a negative for IIPR. This could not be advocate from the truth. Besides the above discussion regarding the improvement to tenant quality, we must recollect that the current leases are tied to the corporate entities and IIPR has a very long weighted average lease term.

2023 Q3 Presentation

This means that even if cannabis operators get full access to the capital markets, they are not legally able to “back out” of these current leases. IIPR would have at least a decade’s worth of time to continue growing its portfolio prior to any lease expiration event. If IIPR was trading at over $200 per share, then I might be more concerned about tail-end lease renewals, but not when the stock is trading at less than $100 per share.

I continue to expect IIPR to eventually re-rate higher to around a 6% dividend yield. Between that multiple expansion potential and the 3% annual lease escalators, I expect solid returns for patient investors from here.

What are the key risks? The main near-term risk is if the DEA issues an announcement stating that they intend to go against the HHS recommendation. I hold little confidence that the Senate will be able to pass any positive legislative reform, at least in the near term, given the persistent gridlock. I view the prospects of DEA re-scheduling as being not only likely but also critical for legislative hopes. The longer-term risk is if the legal cannabis model fails. It is possible that state governments falter to restrict the illicit market, which may make it infeasible for legal operators to function profitably (due to having to charge higher prices). IIPR has quite a bit of cushion to reduce rents to accommodate tenant struggles, but shareholders would likely encounter some losses if stabilization does not occur or if legislative reform takes too long. I am of the view that the landlord has superior bargaining power in any tenant restructuring negotiations, but such processes are typically messy.

I am downgrading IIPR to “buy,” but reiterate my bullishness due to the strong balance sheet which helps to more than offset the messy near-term outlook.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")