SDI Productions

A Quick Take On InnovAge Holding

InnovAge Holding Corp. (NASDAQ:INNV) provides a healthcare service delivery platform for capitated care to high-cost, dual-eligible seniors in the U.S.

I previously wrote about INNV in March 2023 with a Hold outlook on slow expected revenue growth.

InnovAge Holding Corp.’s results will likely continue to be hampered until the other two of its California PACE centers are fully removed from state sanctions, and the firm can improve its enrollment mix.

I remain Neutral [Hold] on INNV for the near term.

InnovAge Holding Overview And Market

Colorado-based InnovAge has developed its InnovAge Platform to reduce unnecessary spending while focusing on the patient encounter and improving outcomes.

The firm is led by president and CEO Patrick Blair, who has been with InnovAge since 2021 and previously was Group President of Bayada Home Health Care and held various senior positions at Anthem.

The company’s primary offerings include:

-

Interdisciplinary care teams

-

Community-based care delivery model

-

Multi-modal approach.

INNV operates in the PACE (Program of All-inclusive Care for the Elderly) system. More than 150 PACE programs are serving over 70,000 patients in 32 states and the District of Columbia.

The firm has PACE centers in Colorado, California, New Mexico, Pennsylvania and Virginia.

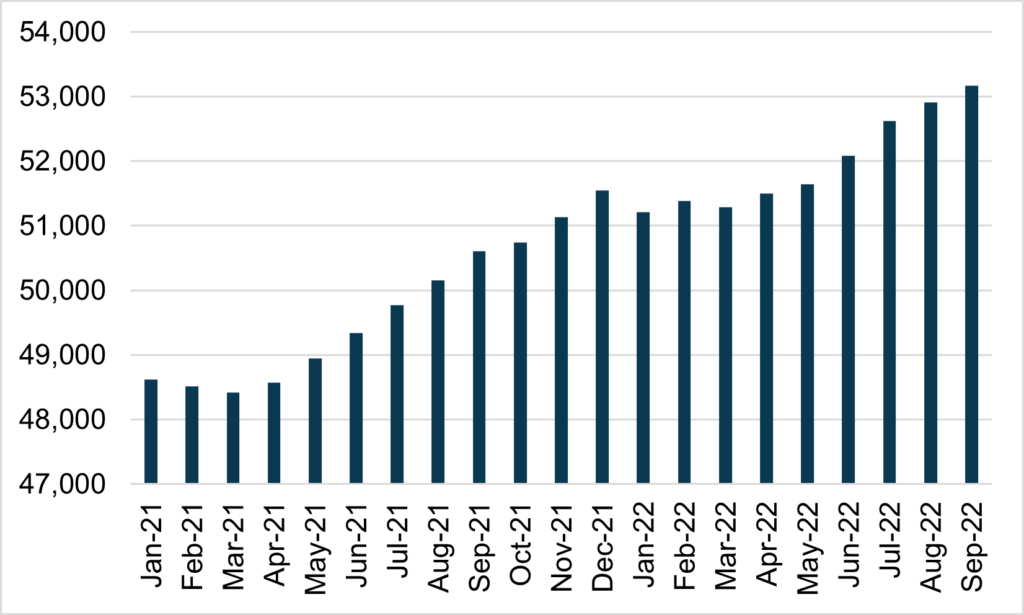

According to Health Dimensions Group, the amount of dual-eligible PACE enrollment from January 2021 to September 2022 was as follows:

Health Dimensions Group

Also, according to a 2020 market research report by Mark Farrah Associates, the top five companies accounted for 47% of the U.S. Medicaid managed care market in 2019.

The top five companies were:

InnovAge Holding’s Recent Financial Trends

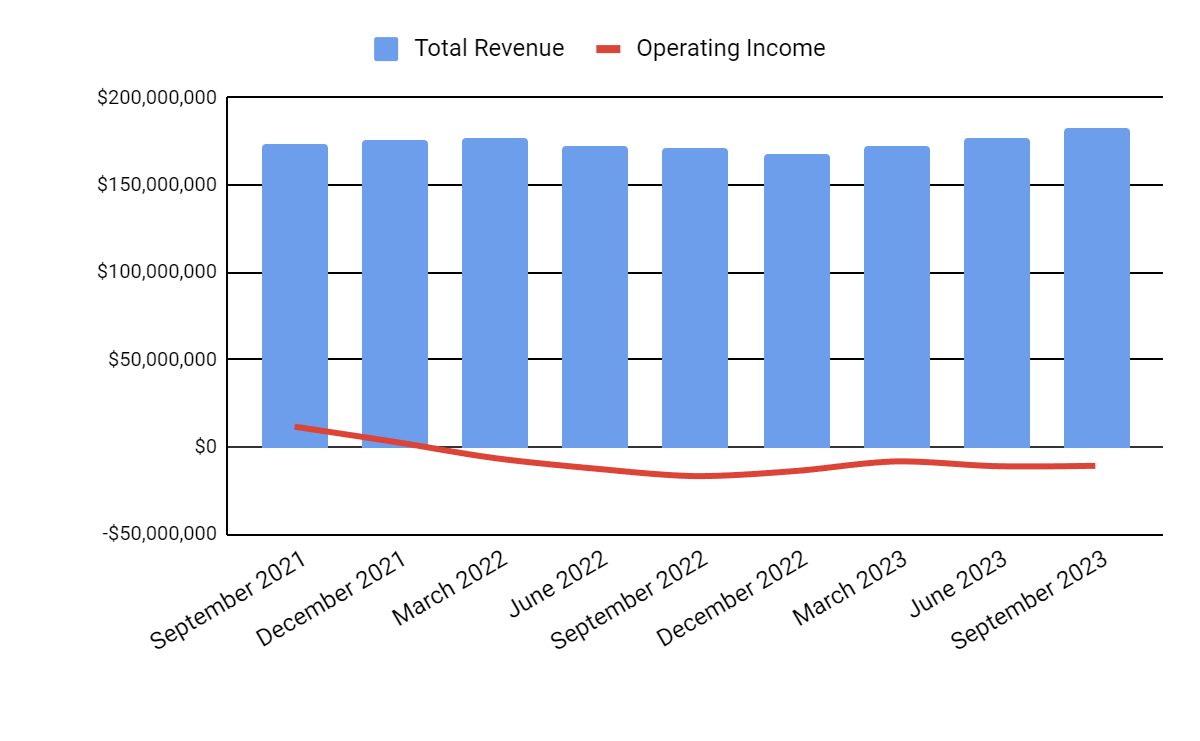

Total revenue by quarter (blue columns) has restarted growth since Q4 2022 due to an increasing census count; Operating income by quarter (red line) has worsened sequentially because of some delays due to enrollment application processing delays outside of its control.

Seeking Alpha

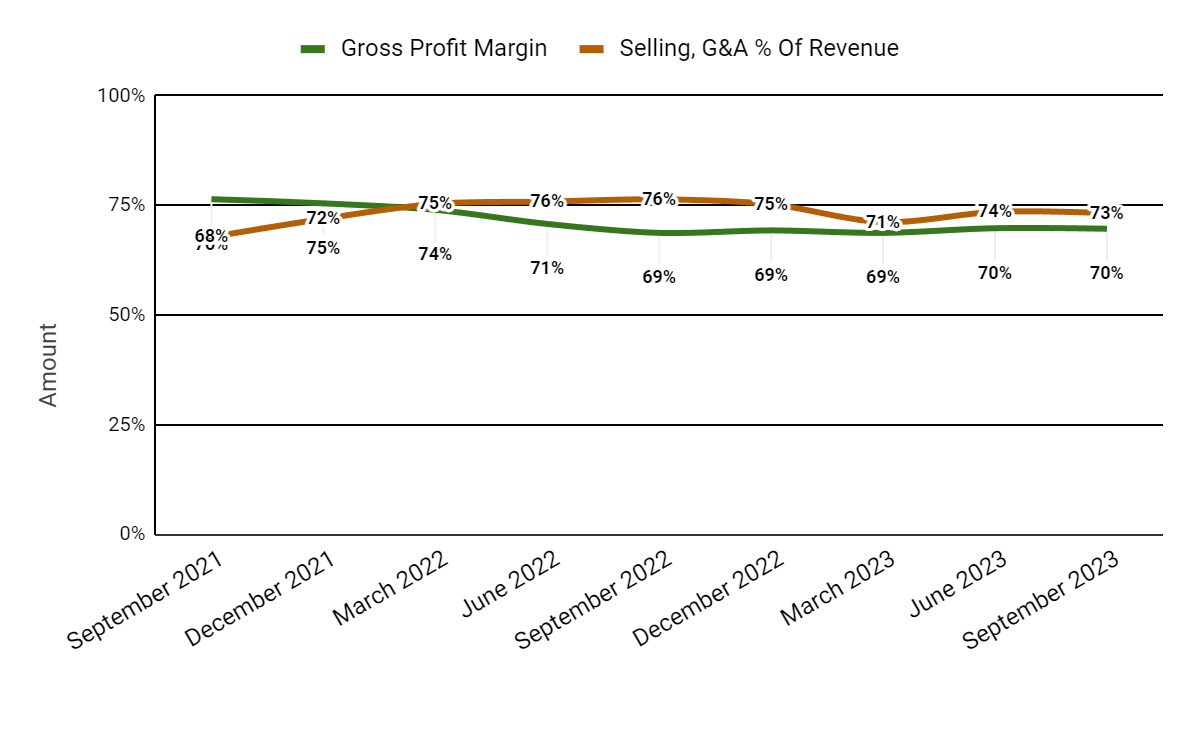

Gross profit margin by quarter (green line) has varied as a result of higher external provider costs; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have trended lower due to greater revenue on only slightly higher SG&A costs.

Seeking Alpha

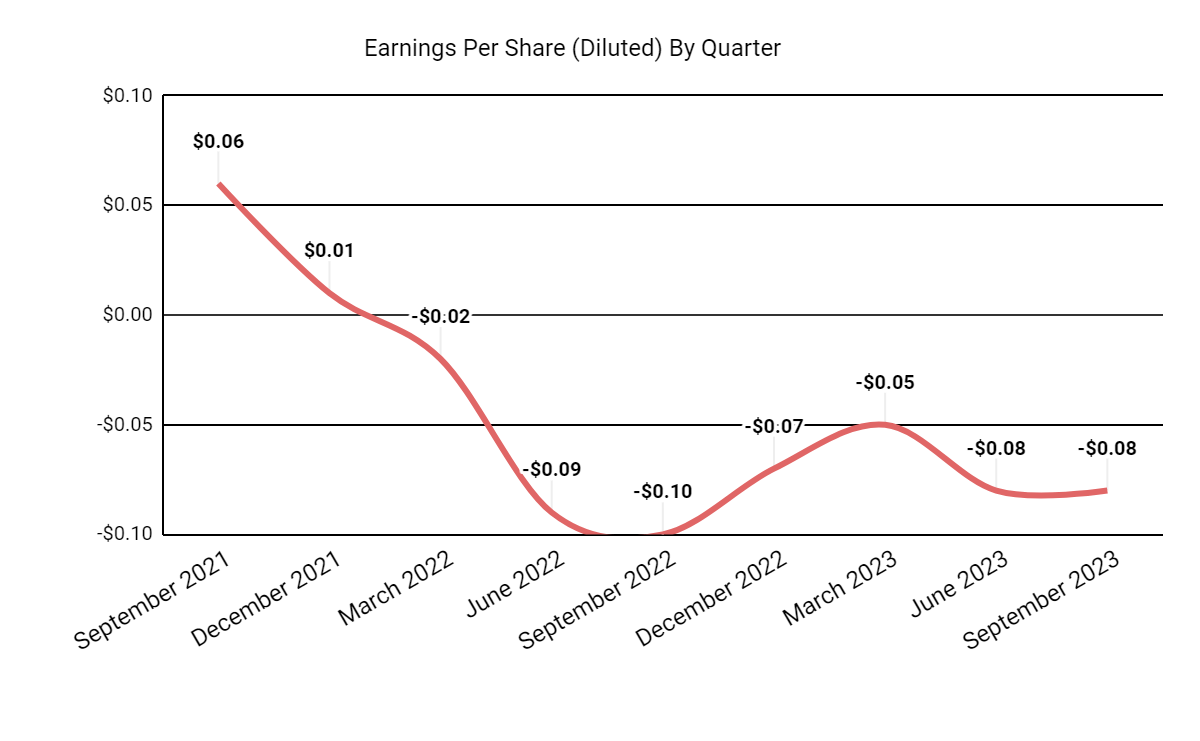

Earnings per share (Diluted) have remained materially negative, with little meaningful progress toward breakeven:

Seeking Alpha

(All data in the above charts is GAAP.)

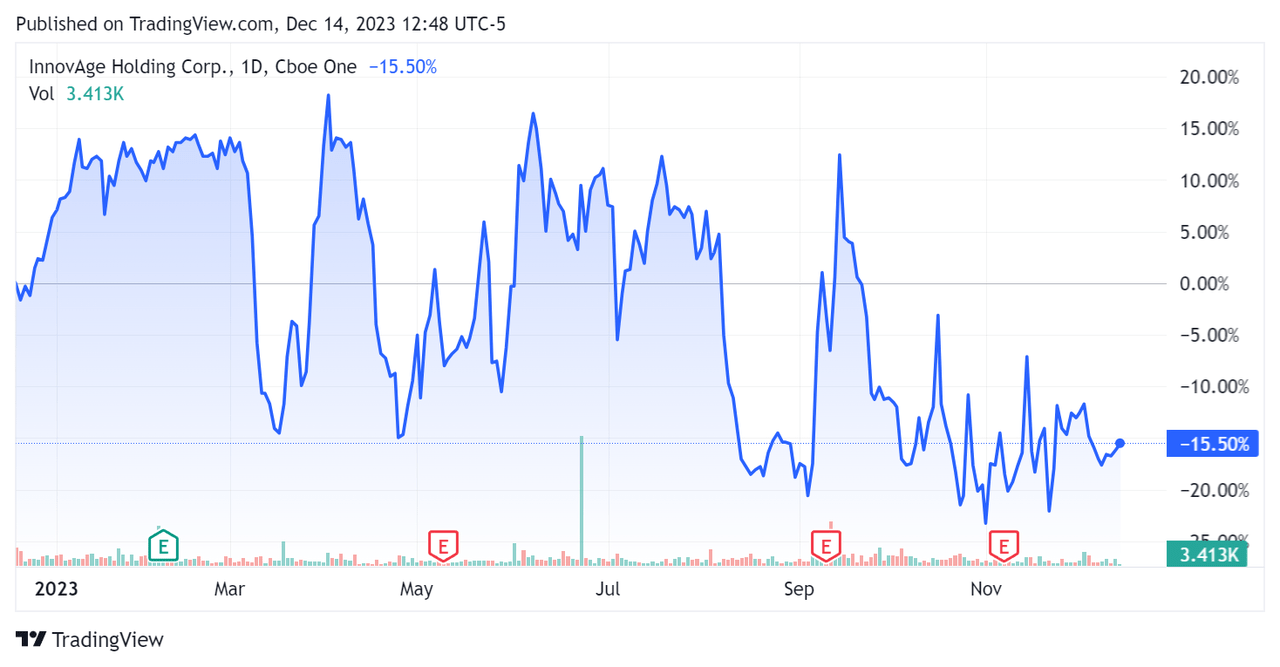

In the past 12 months, INNV’s stock price has fallen 15.5%:

Seeking Alpha

For balance sheet results, the firm ended the quarter with $135.2 million in cash, equivalents and short-term investments and $67.8 million in total debt, of which $3.8 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash used was ($44.2 million), during which capital expenditures were $18.3 million. The company paid $5.2 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For InnovAge Holding

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure (Trailing Twelve Months) |

Amount |

|

Enterprise Value / Sales |

1.1 |

|

Enterprise Value / EBITDA |

NM |

|

Price / Sales |

1.1 |

|

Revenue Growth Rate |

0.4% |

|

Net Income Margin |

-5.4% |

|

EBITDA % |

-3.9% |

|

Market Capitalization |

$779,300,000 |

|

Enterprise Value |

$768,030,000 |

|

Operating Cash Flow |

-$25,880,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.28 |

|

Forward EPS calculate |

$0.04 |

|

Free Cash Flow Per Share |

-$0.33 |

|

SA Quant Score |

Hold – 2.53 |

(Source – Seeking Alpha.)

Commentary On InnovAge Holding

In its last earnings call (Source – Seeking Alpha), covering FQ1 2024’s results, management’s prepared remarks highlighted the quarter’s results as in line with previous expectations.

The company’s patient census increased to 6,580, or 2.8% growth sequentially.

Management believes the firm is “still in the early innings, post-sanctions, and on the path to unlocking the full potential” of the company.

In the Colorado market, it is achieving increased utilization of its labor force, which is assisting in rebalancing its participant mix, leading to increased PMPM (Per Member Per Month) expense over time.

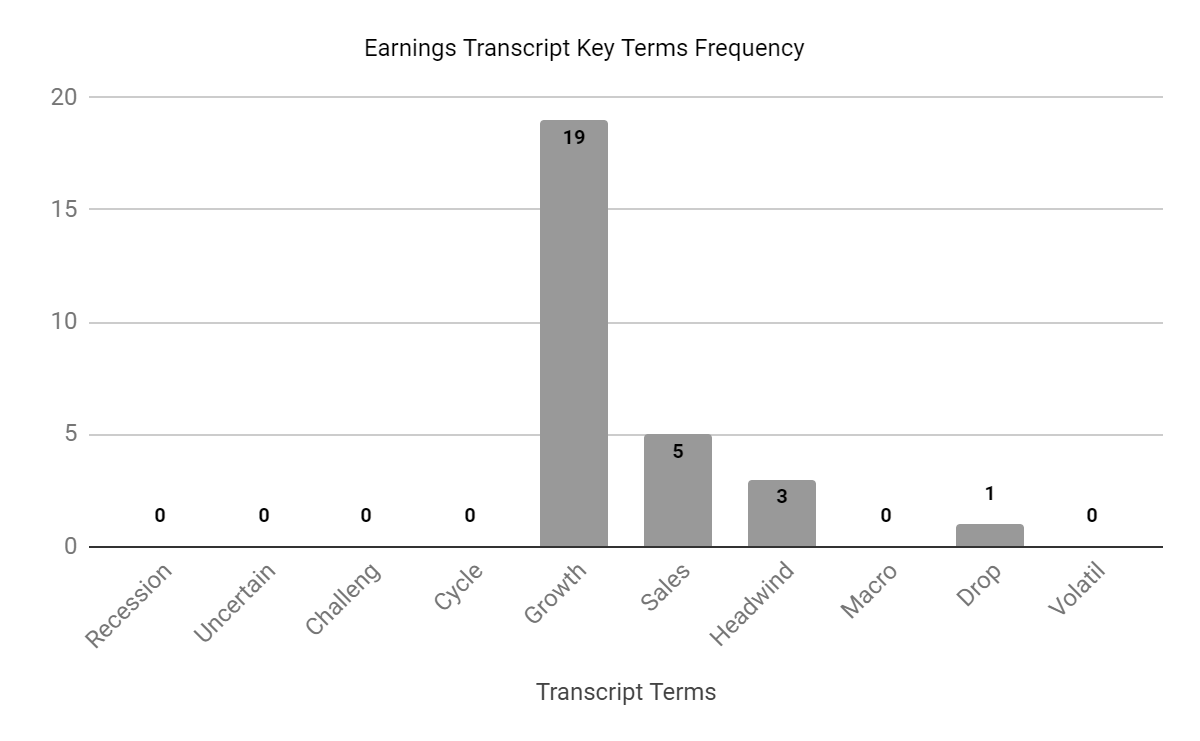

I prepared a chart showing the frequency of a variety of keywords and terms used by management and analysts:

Seeking Alpha

The chart referenced headwinds the company has faced due to enrollment delays through some of the various partners that perform assessments and process applications.

Analysts questioned the leadership about enrollment trends, guidance, external provider costs and patient acuity.

Management said that it is seeing positive momentum and better growth rates in markets that have been live for some time already, and that momentum is giving them confidence in their previous expectations.

External provider cost increases have occurred due to increases in ER utilization (expensive), and while they’re seeing reductions in inpatient utilization, those who are admitted are in more serious condition.

On patient acuity, management said that the mix of new participant members is looking more normal, so the population mix is becoming less costly over time.

For the quarter’s results, total revenue rose 6.6% year-over-year and gross profit margin inched up 0.9%.

Selling and G&A expenses as a percentage of revenue dropped by 3.1% YoY, a positive signal, and operating losses were reduced by 35.5%.

The company’s financial position is moderate, with currently ample liquidity, some debt but a material amount of free cash used in the past four quarters, so the company will need to cut its cash burn.

Looking ahead, full FY 2024 revenue growth is expected to be around 10% versus FY 2023’s growth rate of 1.86% over FY 2022, so growth appears to be improving.

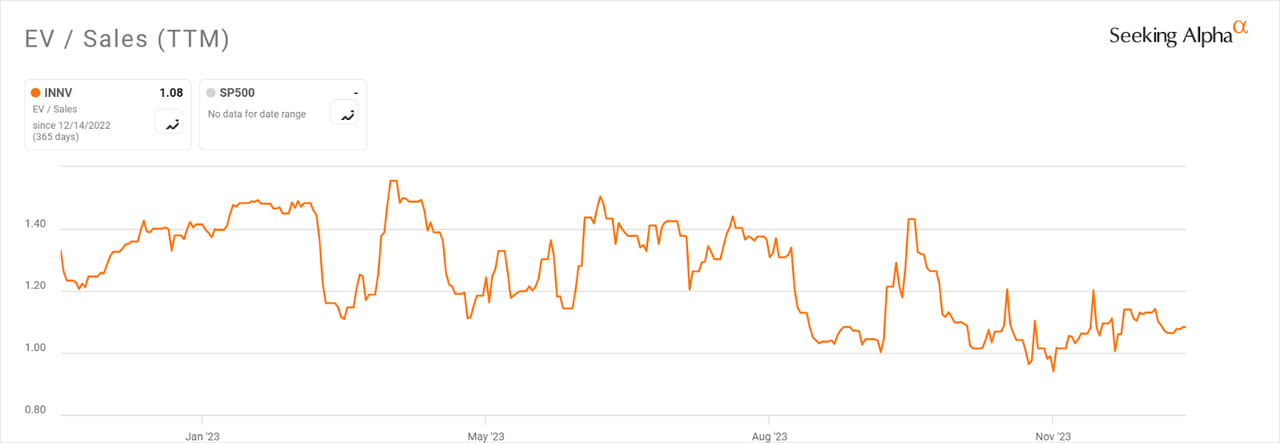

In the past twelve months, the firm’s EV/Sales valuation multiple has been all over the place, trending slightly lower, as the chart from Seeking Alpha shows below:

Seeking Alpha

A potential upside catalyst to the stock could include ongoing improvements in enrollment mix and growing activity through its Sacramento, California, PACE center.

However, results will likely continue to lag until the other two of its California PACE centers are fully removed from state sanctions, and the firm can improve its enrollment mix.

I remain Neutral on INNV for the near term.

Q2 2024 Earnings Call Transcript")