Maskot

Introduction

iShares U.S. Medical Devices ETF (NYSEARCA:IHI) is an exchange-traded fund that provides investors with exposure to U.S. companies that manufacture and distribute medical devices, whereas the portfolio is constructed so as to align with its benchmark index, the Dow Jones U.S. Select Medical Equipment Index.

The last time I covered IHI was back in December 2021, at which time I believed IHI would underperform. This has indeed occurred; while 2022 was a bad year for almost all equities, we have seen all-time highs being safely breached across the major indices since the end of 2022 (i.e., very strong recoveries, at least in the United States). When I last covered IHI, the ETF’s share price was $63.18 (on publication; or $61.78, the price I used in my model). Today, the share price is $56.63, and so it makes sense to revisit, especially in light of a different macroeconomic environment.

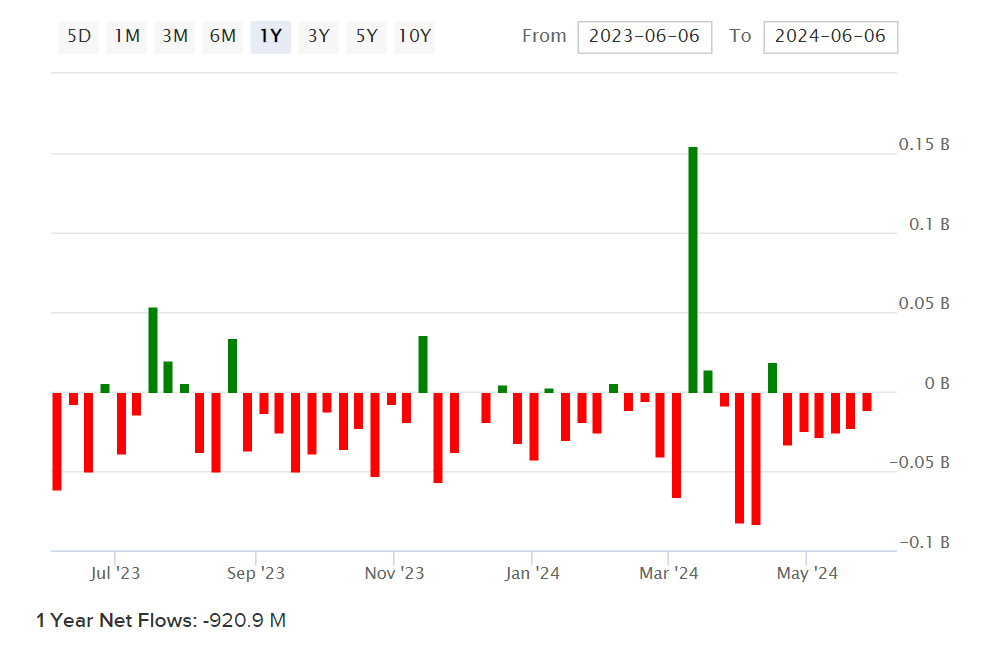

I think before, I was probably right that inflows into the ETF were excessive, and driven by sentiment that was built upon a higher-than-reasonable likelihood of an extended pandemic with elevated long-term demand for medical devices. I am revisiting IHI, in case sentiment has swung the opposite direction, creating an opportunity in terms of valuation. As can be seen from the chart below, inflows are now negative on a 12-month trailing basis (to the tune of about -$921 million, almost a billion).

ETFDB.com

Cyclical Positioning

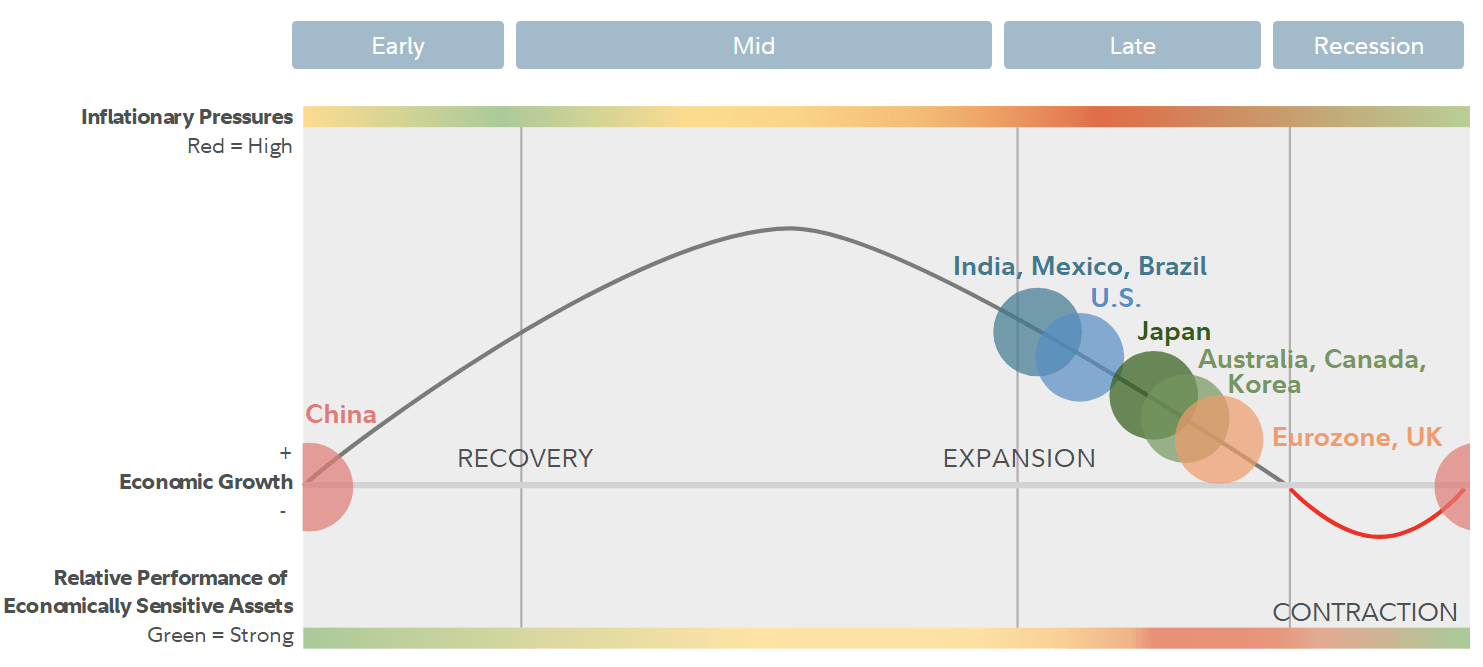

In theory, “Healthcare” as a sector exposure is considered “Defensive”, since demand is likely to be robust over the long haul, in a way that is not as dependent as most other sectors on the cyclical position or health of the economy. That makes sense. Medical devices could, however, be at least partially sensitive, with spending cutbacks more likely in economic downturns, even in healthcare. I often look to Fidelity’s business cycle positioning chart to see where we are, as it is largely accurate. As of Q2 2024, Fidelity estimates that the United States (along with a few other major geographies) is in the early part of the “late stage” of the current U.S. business cycle.

Fidelity.com

The United States has been behind China for quite some time. However, so far, it would appear that the U.S. has quite impressively staved off recessionary fears, and continued to chug along. Bar a “black swan” event, it is probably that over the next 12-18 months, we might see a gradual increase in the interest in so-called defensive sectors like healthcare, but not necessarily with an outright earnings recession. Positionally then, this could support IHI as a general investment thesis (cyclically).

Valuation

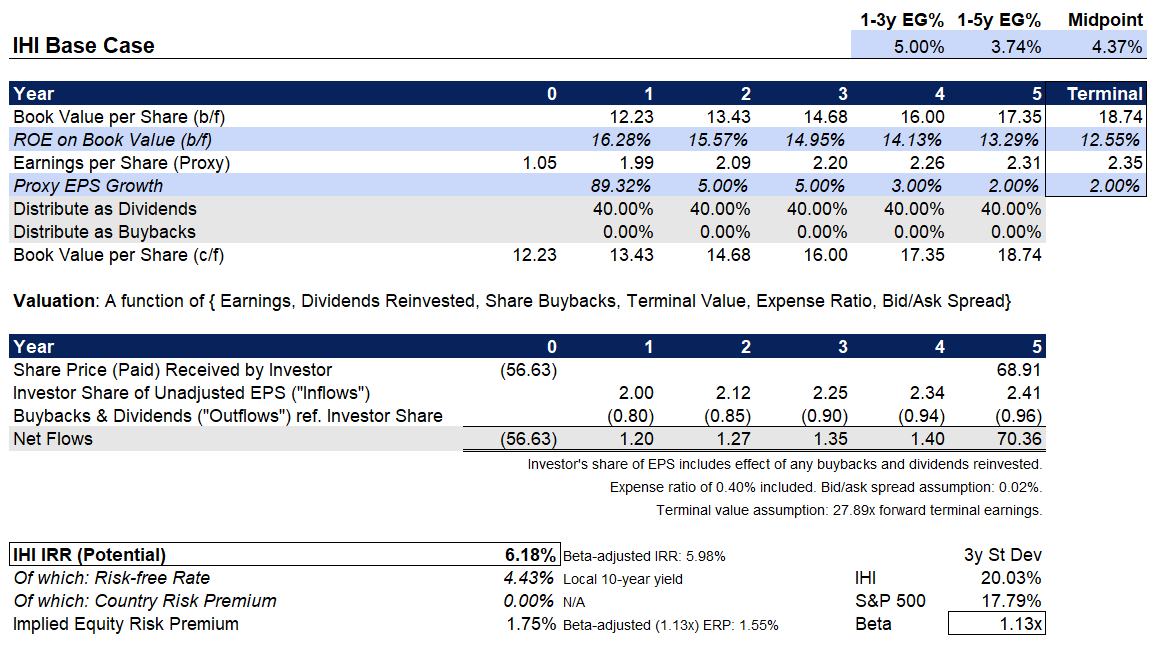

As a reference, we can use IHI’s benchmark index’s most recent factsheet (as of May 31, 2024) to build the starting values. Also, it is worth noting ahead of time that the fund’s expense ratio is 0.40%, which is not cheap; meanwhile, its bid/ask ratio is 0.02%, which is fair (the shares are liquid and regularly traded). In the factsheet referenced, the trailing price/earnings ratio was 52.8x, while the projected price/earnings ratio was 27.89x. This implies a roughly 89% jump in forward-year earnings; this is likely to be a case of a lower earnings base, and an expectation of normalized earnings going forward at the portfolio level.

The price/book ratio was 4.54x, with an indicative dividend yield of 0.87%. All considered, the data implies a forward return on equity of 16.28% and a distribution rate of profits (into dividends) of about 40%, retrospectively. Meanwhile, Morningstar provides us with a three- to five-year earnings growth rate, on an analyst consensus basis, of 8.04%. Aside from the near-term “jump” in the earnings basis, I will bear this 8% prediction in mind as I construct the valuation.

Looking beyond the first year ahead, in which case I will take the analysts’ consensus per IHI’s benchmark index factsheet (as above), thereafter I will assume that the forward return on equity softens/matures through to year six in my analysis, as a reasonable (I think) and conservative assumption. I will assume that earnings growth actually runs at 5% per year in the first couple of years, before falling to about 2%, in order to support a softer return on equity trend (from 16.28% in the first year, through to about 12.5% in year six). This helps to build in some margin of safety relative to consensus estimates.

Integrating all other information, including dividends, the expense ratio, and bid/ask spread, and assuming a constant forward price/earnings ratio of 27.89x (as at present), we arrive at a headline IRR of 6.18%. With a current 10-year U.S. yield (“risk-free rate”) of 4.43%, the equity risk premium (or “ERP”) is 1.75%.

Author’s Calculations

The implied IRR is low. The implied ERP is also low, especially given that, in spite of the fact that healthcare stocks are considered more defensive, the beta of the fund (on a three-year, monthly basis, in relation to the S&P 500) is 1.13x (i.e., 13% more volatile than the S&P 500 index, on average).

There were only 51 holdings as of June 6, 2024, a tenth of the S&P 500’s number of constituents, which is probably helping to drive the beta of the fund. The largest holding is Abbott Laboratories (ABT) at 16.21%, an American multinational seller of medical devices, diagnostics, branded generic medicines and nutritional products. The next largest holding is Intuitive Surgical (ISRG) at 13.19%, a large medical robotics company. The third-largest holding is Stryker (SYK), at 10.58%, another large and profitable medical devices company with a relatively diversified product portfolio. While these companies are sound, these three stocks represent just under 40% of IHI’s total assets under management, so there is a fair amount of concentration risk, and one wonders whether it would make sense to simply purchase these three stocks outright for the time being (instead of investing in IHI).

At the portfolio level, what happens if I adjust the average forward earnings growth rate and return on equity? If I allow the forward return on equity to hold up over 14%, with an earnings growth rate between year one and year three of 7.5%, the implied IRR and ERP rise to 8.97% and 4.45%, respectively. Raising this earnings growth rate to 8% raises the IRR and ERP further to 9.57% and 5.14%, which is about where we would need these numbers to be in order to justify saying that IHI is at “fair value”.

Verdict

I think that IHI is probably in the realm of fair value at present, albeit without much of a margin of safety, and therefore likely provides investors with a reasonably good entry point. Long-term shareholders, unlike at the end of 2021, are likely to generate a healthy long-term return by holding IHI at present prices (around $56-57/share).

However, risks include concentration risk, and there being little margin of safety in the earnings growth numbers.

Perhaps there is one supportive factor besides valuation, in that a slowing economy and possibly recession in 18-24 months’ time (or longer, as the case may be) could drive up the demand for more defensive sectors like healthcare, thus lifting IHI’s share price. However, the valuation is already in the realm of fair, and the portfolio is not particularly well diversified (given only 51 holdings). It is also always possible that earnings could adjust downward slightly in a slowdown, counter-balancing any improved valuation effect.

I do like the defensiveness of investing in healthcare companies, and I think IHI offers good value, especially relative to the last time I covered the fund. However, I think with recent outflows and an update in the market’s perception of IHI, the fund is now likely set to generate headline returns (with dividends reinvested) of 6-10% over the next five years, which is right around the fair value bracket. Therefore, I would take a neutral stance.

Q2 2024 Earnings Call Transcript")