Neilson Barnard

In our last coverage of Icahn Enterprises L.P. (NASDAQ:IEP), we pointed out that the distribution was nowhere near safe, despite the large initial cut. We expected another one within a year and felt the risks were materially skewed to the downside. Investors have put those warnings on snooze and the stock is flat since then, providing a nice, albeit market-lagging, total return.

Seeking Alpha

With an estimated NAV out from the company and immediate refinancing risks behind it, we update our outlook for the next 12 months.

Refinancing

Refinancing is one of the most important focal points for the timeline of a distribution cut in our view. Last time around we told investors that just straight up on basic math and valuation, you can have a negative view, but the refinancing is the catalyst that is likely to shape how things play out.

We doubt this gets refinanced at less than double digit rates so a pay down is probable. IEP has cash on the balance sheet, but the refinancing issues are big over the next 3 years.

So that first bond maturity would be our upper limit for how long things can go on. Even the cash amounts paid to the few that don’t reinvest, will become too much of a drain by then. Interestingly enough, option pricing has become a bit mixed and is no longer having a clear signal as to when the cut occurs. So we might actually get one or two more distributions at the current rate before the rug pull.

Source: First Cut May Be The Deepest, But The Second One Will Hurt More

Were we right about that? Well, sort of.

Icahn Enterprises L.P. (“Icahn Enterprises”) announced today that it, together with Icahn Enterprises Finance Corp. (together with Icahn Enterprises, the “Issuers”), consummated their offering of (i) $500,000,000 aggregate principal amount of 9.750% Senior Notes due 2029 (the “Initial Notes”) in a private placement not registered under the Securities Act of 1933, as amended (the “Securities Act”) (such offering, the “Initial Notes Offering”) and (ii) $200,000,000 aggregate principal amount of additional 9.750% Senior Notes due 2029 (the “Additional Notes,” and, together with the Initial Notes, the “Notes”) in a private placement not registered under the Securities Act (such offering, the “Additional Notes Offering,” and, together with the Initial Notes Offering, the “Notes Offering”). The Notes were issued under an indenture, dated as of the date hereof, by and among the Issuers, Icahn Enterprises Holdings L.P., as guarantor (the “Guarantor”), and Wilmington Trust, National Association, as trustee, and are guaranteed by the Guarantor. The net proceeds from the Notes Offering will be used, together with cash on hand, to redeem the Issuers’ existing 4.75% Senior Unsecured Notes due 2024 (the “2024 Notes”) in full on or around June 15, 2024. The 2024 Notes have been satisfied and discharged simultaneously with the closing of the Notes Offering.

Source: IEP Via PR Newswire

The refinancing almost hit the predicted double-digit rate. Market conditions loosened remarkably from the time of our last article (early November) to when the refinancing was done (mid-December). So that helped. IEP also chose a middle path where they did not refinance the entire 2024 tranche.

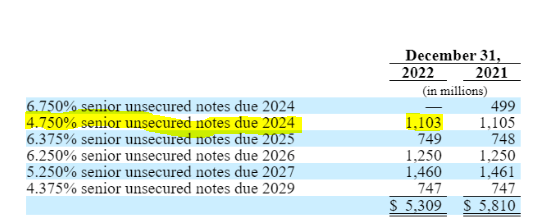

IEP 10-K 2022

They priced less than the total amount and even on that they had to pay 9.75%. Had they tried to refinance the whole stack, they likely would have got the double-digit rates. They did pay some of it from cash on hand, as we expected. IEP’s problems don’t really end here. As seen above, each year has substantial refinancings and the 2029 year, shown above, does not include the new notes of $700 million.

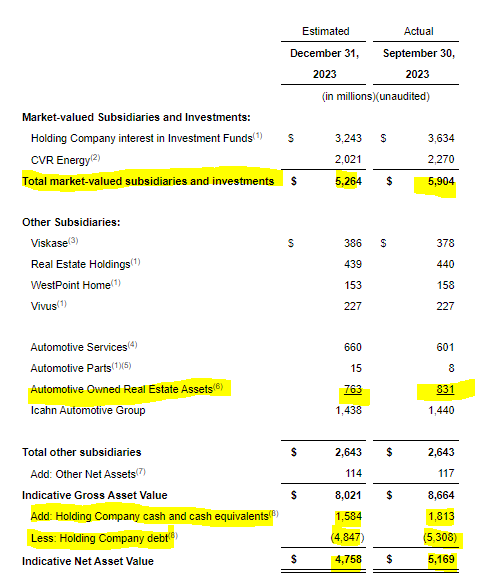

NAV

IEP updated its NAV, with an estimate for year-end December 31, 2023. It showed a substantial deterioration in the value of its main investments as of that date, relative to the previous quarter. Automotive owned real estate was also marked lower, though the cap rates there still seem a tad optimistic.

IEP Q4-2023 Release

We will note here that CVR Energy (CVI) is modestly higher today than it was trading at year-end. But the drop in holding company interest value is quite remarkable. It is possible that there was some liquidation there as well (rather than just market value drop). There are some telltale signs of that. If we examine the holding company cash movement, it has dropped less than what we would expect. The company’s cash should drop $400 million just on the refinancing described above. In addition, there are certainly distributions made in cash (versus in new units). So some liquidation is likely to have happened in this last quarter. The flip side is that the unit count is likely to explode up from its 410 million base and reach well over 425 million when the numbers are released.

How It Plays Out

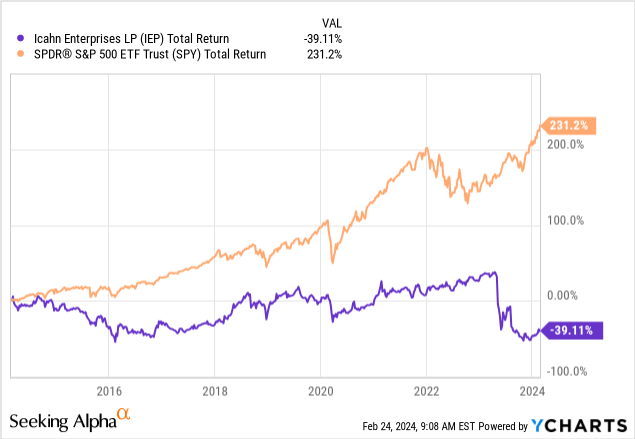

To have a bearish view, you don’t have to buy into the short seller report. You don’t even have to believe the distribution is not sustainable. All you have to do is believe everything the company tells you. They just told you that they refinanced 4.75% debt to with 9.75% debt. Their own NAV was $5.64 billion at the end of last year. Today it is $4.76 billion. Last year-end, we had 353 million units outstanding. Today it is probably over 425 million. So by their own calculations, NAV has dropped from $15.97 to $11.20 in one year. If you take that further into the actual liquidity risks here with refinancing the billions in debt over the next few years and the fact that most of IEP’s investments are not remotely liquid, you have to feel at least some stomach churn. Why are you paying $20.00 for the NAV, which they state is $11.20? You are, of course, doing it because you are chasing the distribution. You did not learn when the first cut came, and you still think that IEP can generate $4.00 on $11.20 of investments. Warren Buffett in his prime would not be able to do 35.77% annual returns on equity. IEP has done a total return of negative 39.11% over the last decade.

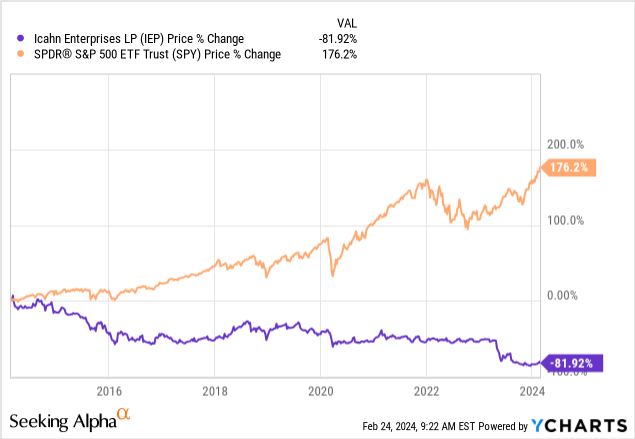

Those are total returns. This is how the price return looks.

You expect that chart above to deliver 35% return on equity currently if you are buying into distribution sustainability. So there are two things we can conclude from that. The first being there is no such thing as an efficient market. The second being that income investors will ride a stock to zero as long as they get “paid” (used really, really satirically here) to wait. We see IEP now poised for a sharp drop as market conditions tighten. While it did not go up with the market, we are fairly certain it will join it on the way down.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Q2 2024 Earnings Call Transcript")